The car market is going though a moment...

On one hand, lots of positives.

The industry is benefitting from pent-up demand, growing inventories and lower prices for consumers.

On the other hand, some systemic concerns.

We're still grappling with higher interest rates, tightened auto lending and rising auto insurance costs.

But for the smartest operators I know... not much has changed.

They are still focusing on the basics. Nothing fancy.

Just delivering positive customer experiences and doing the basics really really well.

As for the not-smart operators... this is going to be an aggressive reversion to the mean.

Uninsured drivers by state:

1. Washington DC: 25.2%

2. New Mexico: 24.9%

3. Mississippi: 22.2%

4. Tennessee: 20.9%

The rate of uninsured motorists has increased over *30%* since 2019.

(Source: Insurance Research Council)

Our team is thrilled to announce some key additions to our Sales and Development teams to solve the customer financing challenges facing auto dealerships today. Joining us are Jamie Raymond, Brandi Bagley, Angela Kane, and Steve Miles.

https://t.co/mOImvGm9DX

Narrative violation:

Dealership service volume has officially hit a *5-year low* for the month of July.

5-YEAR-LOW.

(Service volume = auto repair and maintenance)

Here's why i'm struggling to reconcile this:

1) Average cost of a new car is at all-time highs

2) Average monthly payments are at all-time highs

3) Average age of vehicles on the road is at all-time highs

If people are holding on to their cars longer than ever before... Service volume should be rising?

Apparently not.

Seems like consumers are either forgoing vehicle service or are resorting to alternative options.

Will be keeping a close eye on this.

(Source: Xtime metrics)

My 30-second cheatsheet so you sound smart at the dinner table:

THE USED CAR CYCLE.

First, try to make sense of these 2 statements:

— 9 days ago, Blackbook reported that used car prices experienced the largest decrease since October.

— 9 hours ago, Manheim put out a report that used car prices marginally increased in the first half of August.

What is going on... Something doesn't make sense.

This is what I call the USED CAR CYCLE.

Before I explain what this means and why it matters, here's the current reality:

1) Used car supply is near all-time lows

2) Consumer credit is still very tight

3) Floorplan costs are through the roof (aka, inventory financing costs for dealers)

4) And used car prices are still high by all historical standards.

The result: dealers are (wisely) running on extremely lean inventories.

This means less risk and lower costs... But there's one problem:

Lean inventories don't leave dealers with good cushions. Meaning, if (and when) business picks up, you're panicking to resupply your lot...

This, my friends, is the USED CAR CYCLE:

1) Consumer demand speeds up

2) Dealers fight for inventory and pay more

3) Prices increase

4) Consumer demand slows down

5) Dealers cherry-pick inventory and pay less

6) Prices decline

7) Consumer demand speeds back up

And on and on and on...

So while it may seem like we know where prices are headed and that volatility in market is cooling — things are really just manifesting in new ways.

Here's the bottom line:

Whether you're a dealer or an in-market car buyer, I wouldn't try to time the market.

Regardless of where prices go next, it seems like volatility is going to keep accelerating in both directions.

Good luck my friends. Stay winning.

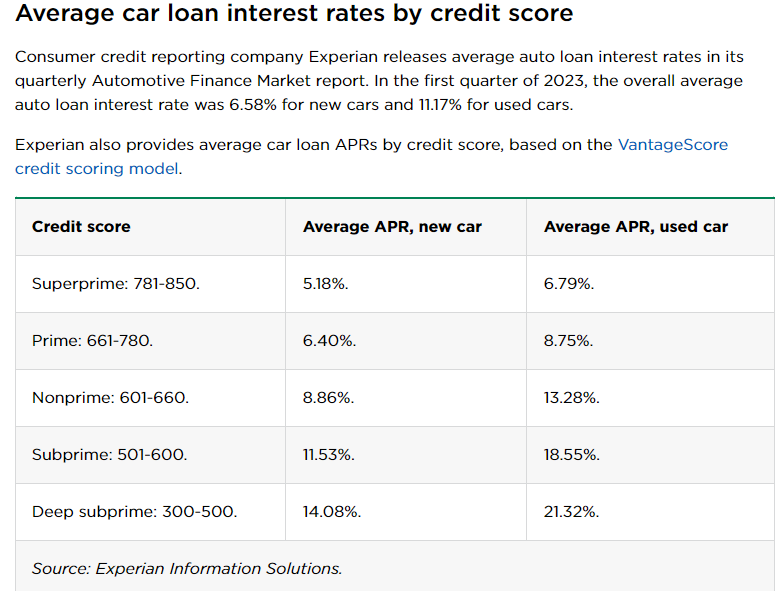

Auto loan and credit card interest rates just hit a new record high.

Average interest rates:

- Credit Card: 25%

- Used Cars: 14%

- New Cars: 9%

Meanwhile, we have record levels of debt:

- Total Household Debt: $17.1 trillion

- Auto Loans: $1.6 trillion

- Credit Card Debt: $1.0 trillion

The worst part?

Student loans just hit a record $1.6 trillion.

Interest on student loans has been suspended since 2020, but it set to resume next month.

The debt crisis is real.

U.S. auto loan rejections have surged 📈

Basically, unlike the past couple of years, it’s a rough time to be a car shopper if you don’t have decent credit and/or some money down.

Have good credit and/or some money down? You’re fine.

I’m closely watching what happens next.

Past 60 days have been a rollercoaster:

— Capital One shut off all dealer floorplans (aka inventory lines of credit)

— US Auto Sales shut down 39 dealerships

— Wells fargo laid-off all its junior Auto loan underwriters and capped future loans

— PenFed Credit Union started cutting dealers from indirect auto lending

— Citizens Financial Group exited indirect auto lending space

According to Automotive News:

Loan officers representing 17 of 46 large and "other" banks (less than $50 billion in assets) in April expected their institutions to tighten auto loans "somewhat" by the end of the year.