We’ve officially hit the #3 New Bestseller on Substack! 🏆

Knowing that these deep dives into backtesting, RealTest, AI and quant workflows are helpful to you is what keeps me going.

A Monte Carlo test is useful for one reason:

> Your future trade sequence will not match your backtest trade sequence.

Risk comes from the paths capital can take, not just the endpoint.

From $10k to $3.96M

As someone who tests RealTest strategies for traders who care about costs, this Dow Award paper is worth studying for one reason: “when leverage earns its place”.

The full checklist, results, and RealTest code are in the article:

I tested Gemini on a RealTest portfolio build.

In this test, it combined 5 strategies, added one Risk Percent control, avoided duplicate symbol exposure, then upgraded weights with rolling 50-day return correlation.

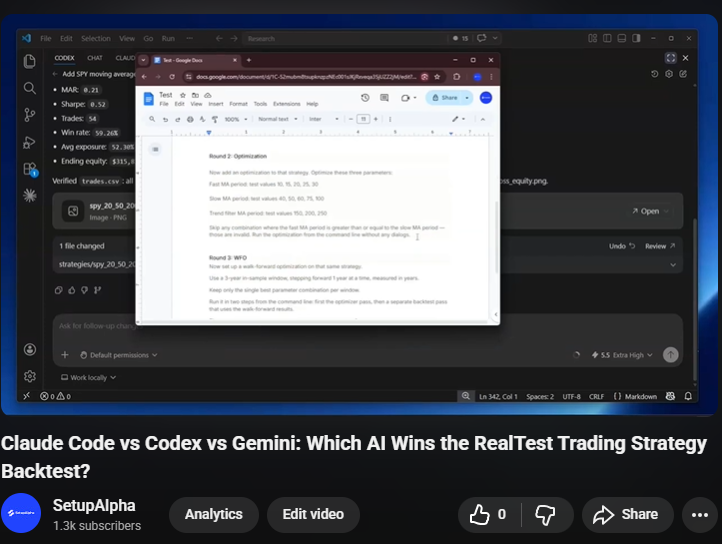

I gave Codex, Gemini, and Claude Code the same RealTest job:

build SPY strategy

run base test

optimize MAs

run walk-forward

make charts

All 3 finished.

But there was one catch.

This trading strategy a very simple.

> Gaps below yesterday's low.

> Buy.

> Wait for a green day.

> Sell.

The backtest had 953 trades and a 64.01% win rate.

In theory AI can write a trading strategy in seconds.

I tested OpenAI Codex, Gemini, and Claude Code on the same SPY moving-average strategy.

My goal was to see which one could move through the actual RealTest research workflow with the fewest fixes.

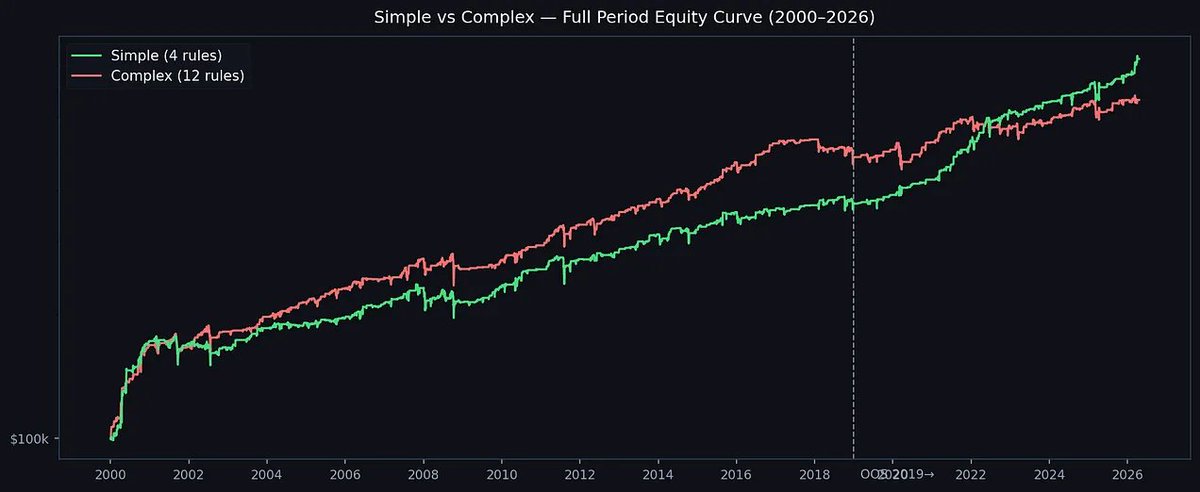

The useful test is not trend following vs mean reversion.

It is whether they fail differently.

In this RealTest run, the 50/50 book had lower MaxDD than either standalone system and the best MAR.

The best standalone strategy was not the best portfolio ingredient.

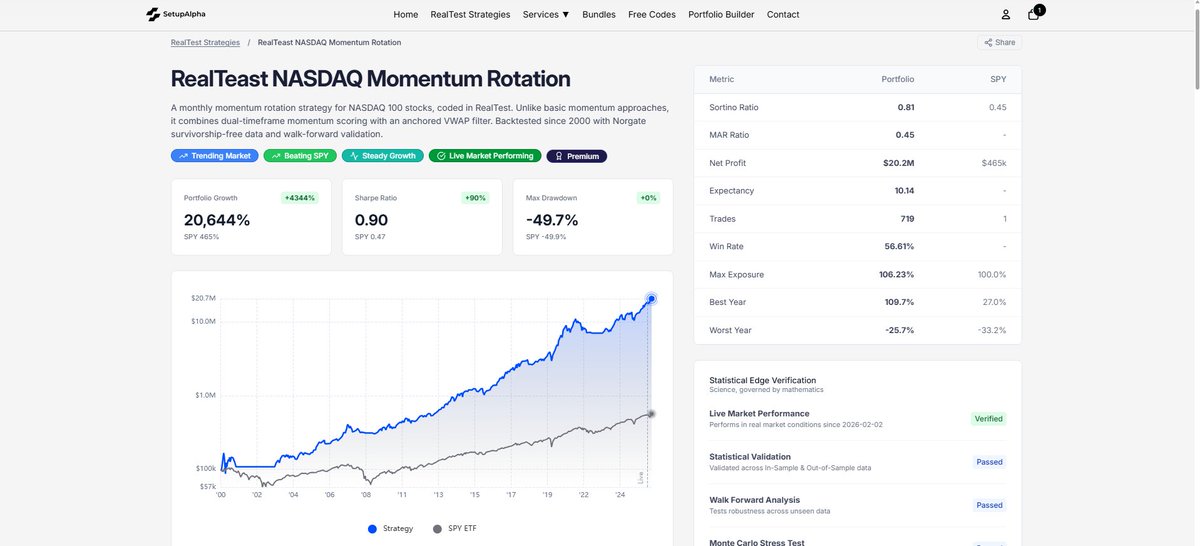

Last week, I published the Nasdaq momentum strategy.

Right now is one of the best periods for momentum this year.

Conditions like this usually appear only once or twice a year.

You can download the RealTest script and strategy rules here:

YTD Results.