@badcharts1 That's because a higher yield environment is accompanied by higher INFLATION. Which nominally decreases the debt/gdp by virtue of increasing gdb and 'stagnating' debt.

It's over, Europe has officially given up on its digital sovereignty: they just signed up to Pax Silica, the US initiative to lock other countries in its AI stack.

In case you think I'm exaggerating, Jacob Helberg, the US Under-Secretary of State who architected Pax Silica, LITERALLY says so in the article (see screenshot 👇): he himself explicitly positions Pax Silica as designed to counter "digital sovereignty" - a concept he opposes because it would mean countries building their own tech stacks.

I wrote a long article 2 weeks ago titled "The Pax Silica Con," warning Europe that it was a "cage" to keep them "dependent on American tech and unable to build their own": https://t.co/yqq6uzhKnz

The cage door was wide open and clearly labeled. They walked in anyway.

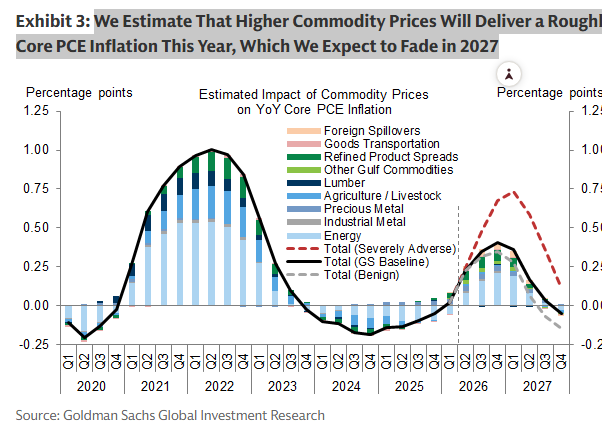

GS: We Estimate That Higher Commodity Prices Will Deliver a Roughly 0.4pp Boost to Year-over-Year Core PCE Inflation This Year, Which We Expect to Fade in 2027

Kind a perfect setup for the new Fed chair... he'll look like a hero

Dividend recaps are back, levering portfolio companies to 5x+ at the lowest spreads post-GFC.

The exit’s frozen, so PE is paying itself out of the credit market instead.

Source: Pitchbook

The latest Fed H.8 data appears broadly consistent with the thesis that the Iran conflict led to a temporary trapping of liquidity within the U.S. financial system🎯

Take a look at "Other Deposits" at foreign-related banking institutions in the United States. Deposits surged by nearly 30% from the start of the conflict to their peak at the end of May, before easing modestly in recent weeks. If the thesis is correct, this growth rate should continue to slow going forward.

Those deposits likely contributed to easier financial conditions across the wholesale funding system, supporting greater leverage, risk-taking, and ultimately fueling narratives around AI infrastructure, semiconductors, and other liquidity-sensitive assets.

In many respects, the mechanism resembles a form of private sector QE. Unlike traditional quantitative easing, no central bank BS expansion was required. Instead, reduced global trade activity and lower realeconomy demand for dollars may have concentrated liquidity inside the U.S. financial system. Arguably, the effect on financial conditions was even sharper than a conventional QE impulse.

The key question now is what happens next?

With the U.S. reportedly reaching an agreement with Iran - one that many would argue involved significant concessions on several previously non-negotiable issues -will those deposits begin to leave the U.S. banking system as global trade financing, inventory rebuilding, FX hedging?

#DXY #LIQUIDITY #REPO #LEVERAGE #AI #IranWar

Iran’s fundamental mistake is that it believes this war is not existential for the US.

This war is existential for the so called American pact aka Pax Americana. The pact in which the US provided investments, military protection, and a very sophisticated financial infrastructure. In return, the other participants focused on what they could do best. The division of labor, and comparative advantage: China: high quality labor, GCC Arabs: cheap and reliable energy, etc.

As part of the pact, any excess capital from these participants would get invested in US financial markets, primarily in the form US treasuries, but also venture capital (eg Saudi money in Softbank), and other instruments.

This did two things:

1-Lower the cost of capital in the US. This meant lower interest rates, higher stock market, more money available for startups, lower housing costs, and many other things.

2-The invested capital served as a hostage, a guarantee of good behavior by those in the system, which supplied some level of stability to the pact. The US could theoretically seize or freeze the assets of any misbehaving participants.

Parts of this pact have already been going away. China is not a US satellite state or even a partner. It is a competitor, building its own pact in the form of Belt and Road Initiative. It is also reducing its exposure to US treasuries and increasing its gold reserves.

If the US loses its dominance over the Persian gulf, another part of this pact will break. The GCC Arab states have lost their protection, while still having a hostage in the US. That’s an incentive to reduce their exposure and diversify their assets out of the US.

It will also send a signal to everyone else in US orbit that the military protection is not available anymore.

As these orbit states reduce their exposure to US assets, the cost of capital in the US will rise: higher interest rates, lower stock market, higher home financing costs, fewer startups, etc.

Furthermore, the US has $31T public debt, with average maturity of 5.9 years. As the interest rates rise, the cost of rolling over this debt is going to rise.

Last but not least, there’s about $1.6T in additional debt that gets added every year, which will be paying higher interest.

As the debt/GDP ratio rises, the feedback loop kicks in: the US has to pay a higher interest rate to keep the same investor.

This is why the loss of the Persian Gulf is so significant for the US.

I might write a later post about the effect of rates on debt financing.

The National Bank of Georgia has announced it has purchased an additional US$100 million of #gold for its international reserves. https://t.co/lM6pOf3p9W