"Once it's over, things don't go back to normal."

The LNG facility in Qatar alone will take 3 to 5 years to rebuild

Fertilizer, helium, chip supply chains are all disrupted

The strait is a chokehold with no alternative route. This isn't transitory.

🎙️ @LizAnnSonders joined @GuyAdami on the latest RiskReversal podcast

【Monthly Dialogue with Julius Bär】In this April episode with Julius Bär, I discuss the implications of the Iran war for global markets and China, whether investors should chase the recent rebound or stay defensive, the outlook for oil, gold, and the US dollar, and why Chinese market has shown relative resilience.

The conversation also covers China’s economic momentum, sector preferences, and the role of defensive, value, and high‑dividend stocks -- particularly Chinese banks -- in navigating ongoing geopolitical and macro uncertainty.

Recorded on April 9.

https://t.co/rVVVOmXT5T

Shipping volume from China’s ports in the first half was 8.5% higher than 2023, with container freight rates surging by a factor of four, according to NCFI. Exports - from cars to steel to consumer goods - soared. - Bloomberg

This is what I wrote in my annual outlook published in December 2023:

“Beijing’s ideological commitment to preventing moral hazard and corruption is the other deflationary force that is

often underestimated.

Chinese policymakers have clearly adopted a different philosophy for managing financial risks. In the West – particularly the US – money printing and government balance sheet expansion have become the policy path of least resistance in responding to financial risks since the Global Financial Crisis. “Too big to fail” is essentially an acknowledgement that financial stability will be prioritized over the prevention of moral hazard.

In contrast, Beijing aims to solve financial risks by tightening regulations, launching anti-corruption campaigns, and inhibiting financial sector balance sheet expansion. From Beijing’s perspective, a systemic bailout in the form of QE and government balance sheet expansion will not only create systemic moral hazard, but it may also lead to rampant corruption in the state-dominated financial sector.

If there is one thing in common between Beijing and the US Main Street, it is that they both hate financial elites. As such, Beijing’s obsession with preventing moral hazard and corruption may continue to delay the necessary fiscal and monetary response that is needed to effectively reflate the economy.”

Labor demand has normalized, and even looks a bit weak in certain areas. Balance is returning to the labor market. The Fed can find a lot of comfort in the progress here.

This morning’s job openings data shows a labor market that has almost completely normalized from the pandemic shock. Measures of labor market tightness have completed their roundtrip as employers have found the right balance for their needs, all with very little job destruction. This is very positive data for the Fed’s mandate.

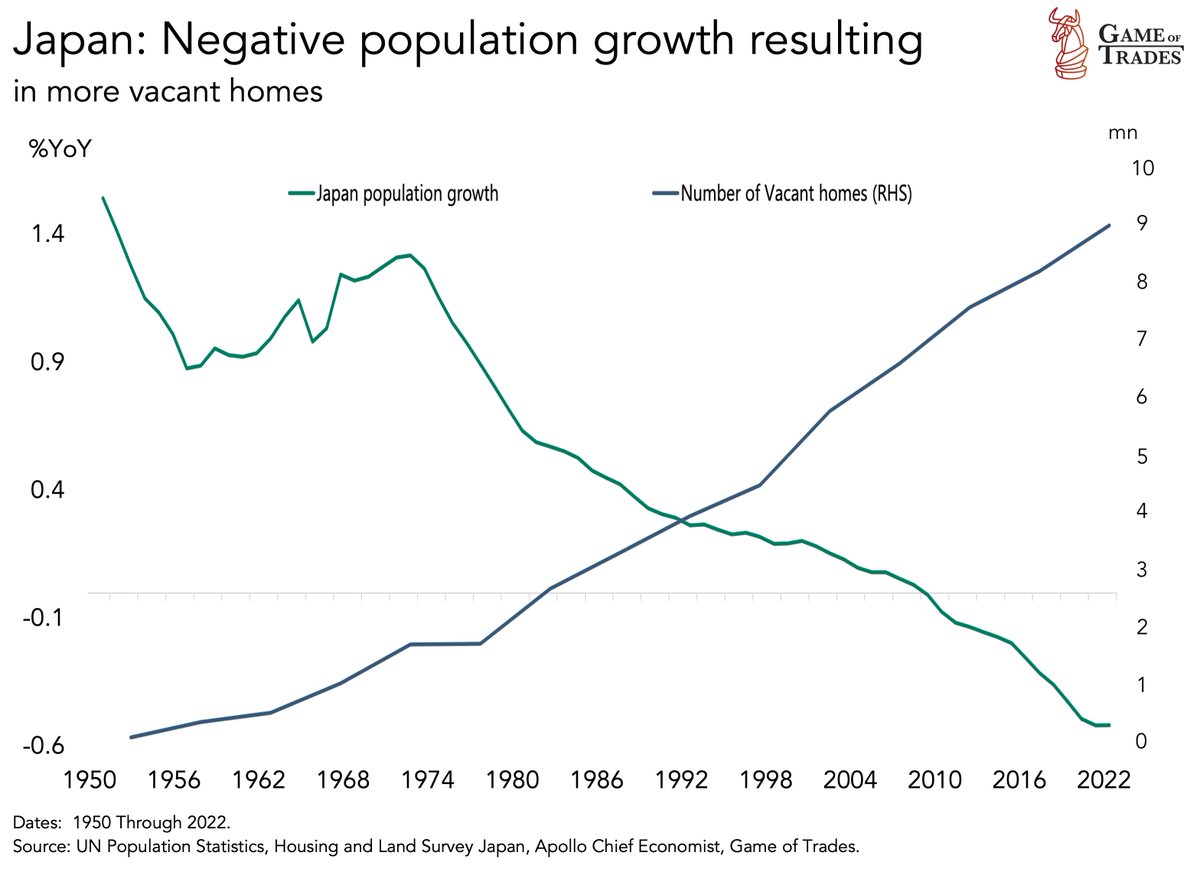

Japan’s population has now been contracting for almost 15 years

At the same time, number of vacant homes there has risen significantly

Now reaching the 9 million mark

At this rate, Japan’s demography poses long-term sustainability risks for their economy

😬

China Considers Government Buying of Unsold Homes to Save Property Market

China is considering a proposal to have local governments across the country buy millions of unsold homes, people familiar with the matter said, in what would be one of its most ambitious attempts yet to salvage the beleaguered property market.

The plan can “inject liquidity to developers directly and improve their financial situation, as well as immediately digesting excess inventory,” said Raymond Cheng, head of China property research at CGS International Securities HK. “This is all win situation. Of course, it needs a lot of funds - at least 1 trillion yuan to make the impact more meaningful.”

Shujin Chen, head of China financial and property research at Jefferies Financial Group, estimated at least 2 trillion yuan ($277 billion) of investments would be needed. https://t.co/AtP34RdMoC

Chinese market pausing at critical technical levels. Rapid sector rotation means the rebound will see plenty of Z-turns. Cook’s visit and Yellen in April will help defrosting the relation. In an election year, China holds one of the keys. https://t.co/JhCyr9Qh4g

Stocks look to continue to crash up as a synchronized global cutting cycle begins. The whole may be greater than the sum, and the potential for negative economic surprises amidst high policy rates skews the risk towards more cuts than expected.

https://t.co/GmPKzUJjmU

In the history of modern finance, no single indicator has done a better job of predicting when the next global recession will start than when the Bank of Japan starts raising rates. Foolproof!

Blue is the ETF $TQQQ, 3x leveraged QQQ

Orange is the price of Bitcoin.

The measure is the cumulative change in prices from January 1, 2018, to yesterday (6 1/4 years).

Effectively they are the same thing.

If BTC is "something different" (digital gold, hard money, a new financial system, the world computer, etc.), why has it traded like overleveraged tech stocks for well over half a decade now?

The ECB just doesn't have much compelling evidence to start a rate cutting cycle soon.

Recent inflation prints are still too high, unemployment is at secular lows, wage growth is too high for 2% target, and recent economic momentum is positive.

China is throwing a kink in the US Big Tech bonanza story. Apple is down today after a report that its China sales plunged 24% in the first six weeks of the year, and AMD is falling after the US blocked it from selling a tailor-made AI chip to China. https://t.co/MuPoxNaf24