Post earnings, how major PSU Banks stand on earnings ratio

Relative valuation should account for their falling NPAs and robust credit growth - No reco.

#NIFTYBANK#NIFTY50

A look at which sectors experienced strong growth from earnings

Metals, pharma and Manufacturing are robust but haven't translated into outperformance- No reco

#NIFTY#Sensex

$ONGC with an interesting snippet in their concall on sales from new well gas, showcasing premium over market prices

Be mindful natural gas prices have almost doubled- No reco

#Energyindex#NIFTY#Sensex

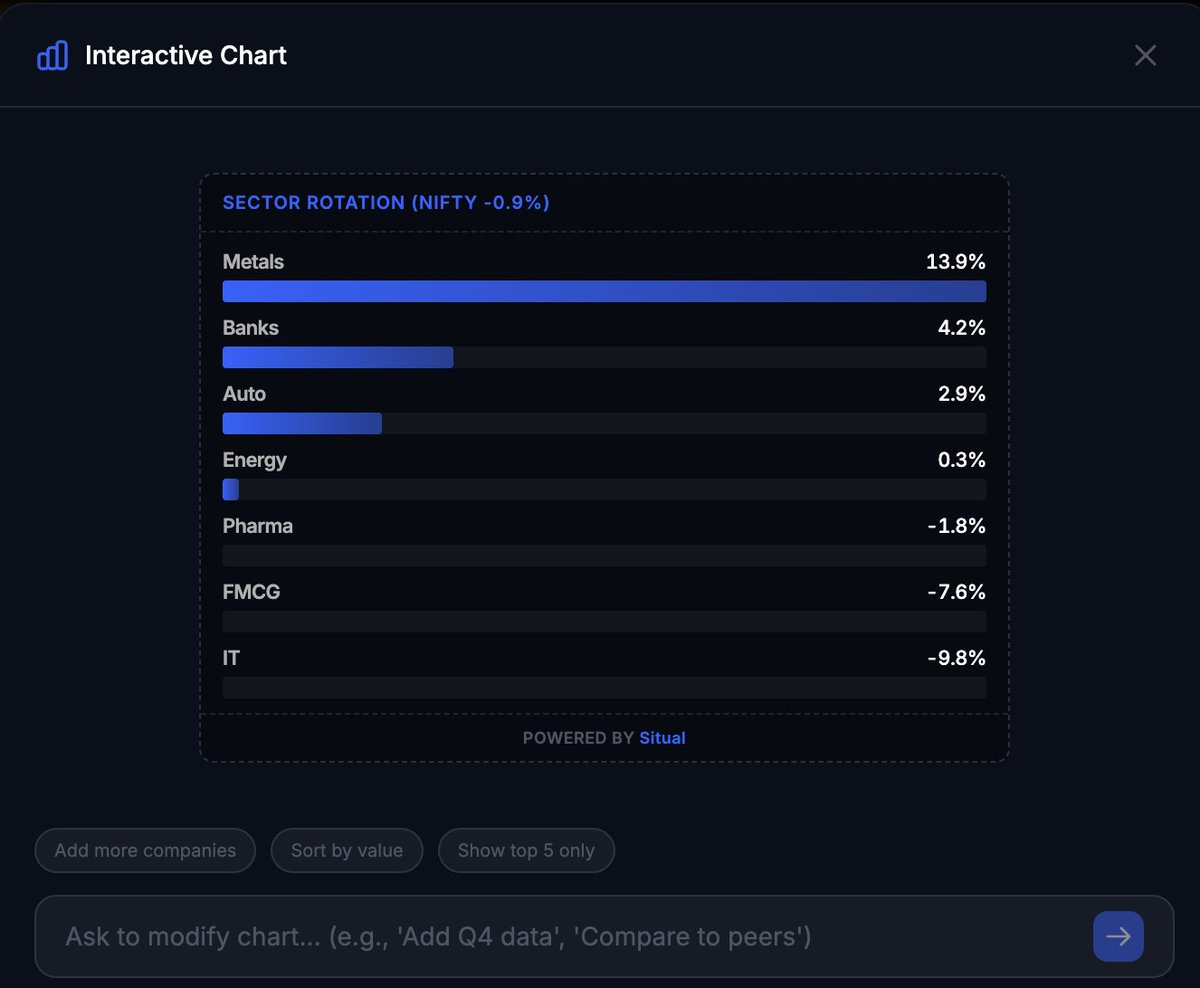

The big story has been on the sectoral rotation as FII flows have dictated liquidity in the stock markets

IT getting hammered most with rotation towards Capital goods, telecom and banking- No reco

#NIFTY50#SENSEX#Investing

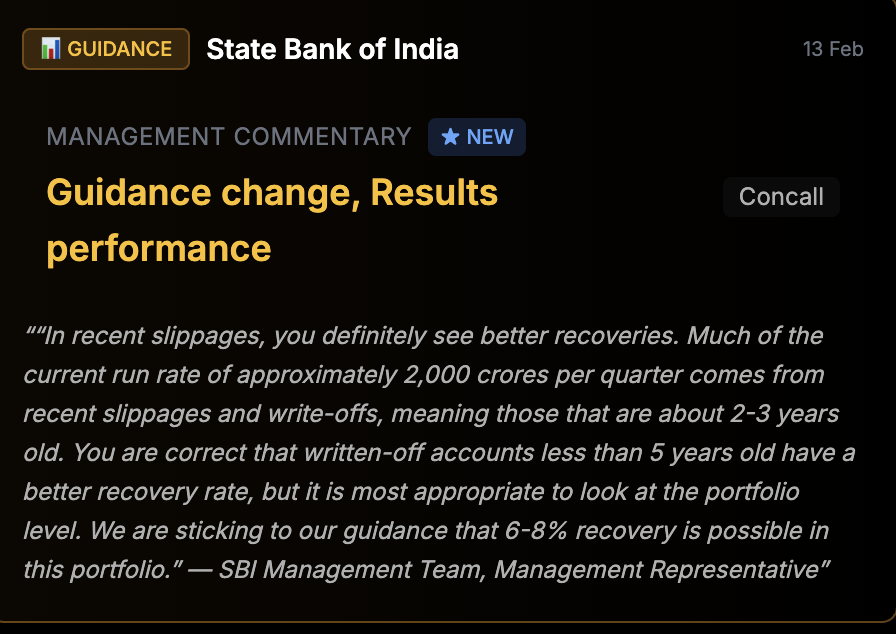

SBI has largely delivered and led the pack of strong results from PSU Banks

Here they are on recoveries going forward in the coming quarters

#Nifty50#StockMarket#Sensex

$HDFC coming out with some big claims, confident of their deposit growth outpacing credit growth going forward.

They also expect top line growth to be faster. No reco.

What you missed behind Indus Tower results. The media sold you declining revenue and estimates miss.

But no one tells you why. Read this. No reco. #Nifty50

Interesting data from our AI on Infra order book/Revenue multiple for the larger infra companies as announced by management. No reco. #Nifty50#Sensex#niftyoptions

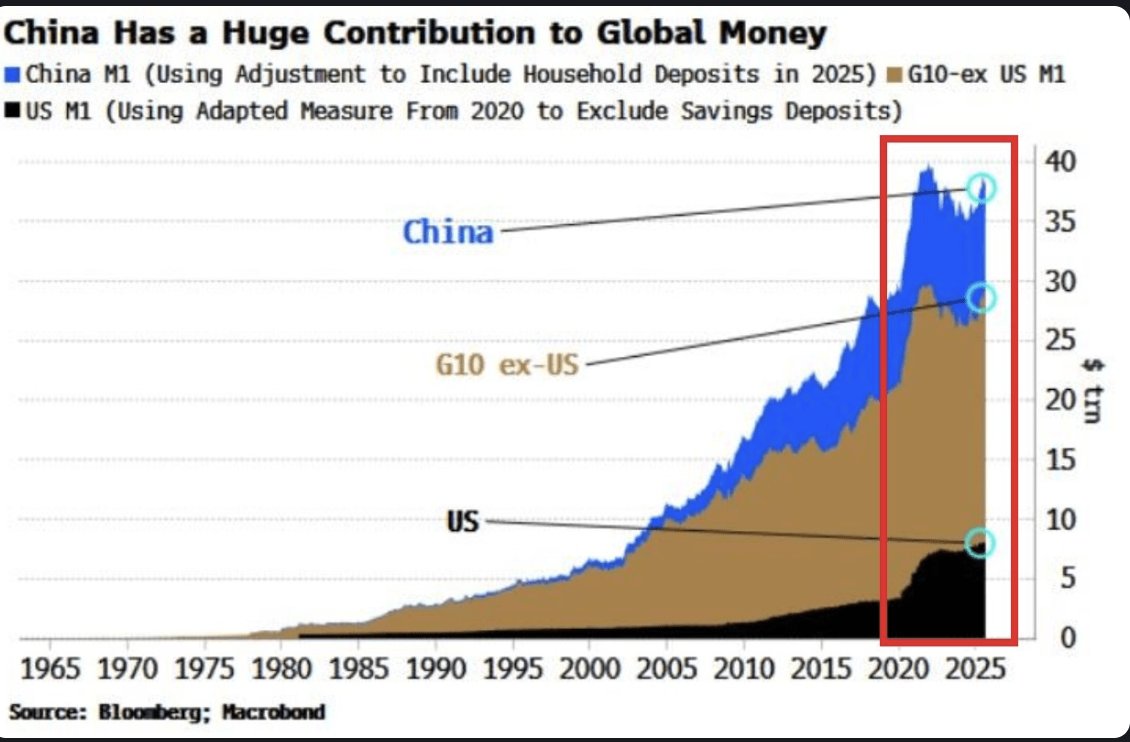

One of the key triggers for increased inflow and liquidity into metals and critical infra has been Chinese M1 supply. Over the last month, this has increased by the most at 4.9%. No reco.

Across Indian financials, increased liquidity seems to be the name of the game, which will persist over the next 4-5 months as a combination of CRR cuts + rate cuts + OMOs.

No reco. #Nifty50#SBI

Across the equity markets, for both FIIs and DIIs, here is where capital has flowed, represented as growth across various sectors.

You can generate your own personalised charts by just prompting or customizing our AI. #Nifty50

China M1 has come in higher at 4.9% YoY for January. Data from Bloomberg here on China now at 25% of global M1 supply. This has been largely fuelled by government bonds - not private lending.

No reco.

Interesting snippet on credit growth which has moderated with deposit ration being sticky at 10.2%. Also, PSU banks coming in at 9.1x PE vs Bank NIFTY's 16.4x, suggesting for room for re-rating.

No reco.