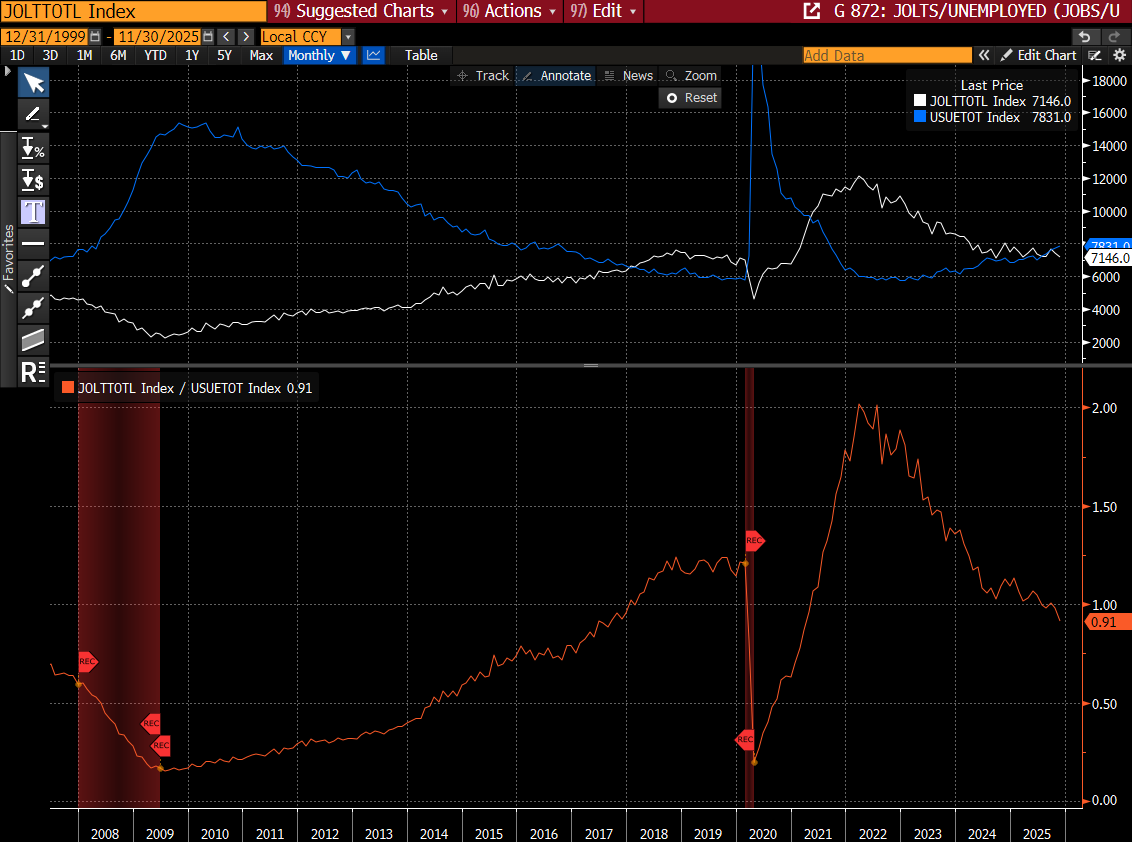

JOLTS - While the low firing rate got +ve attention, the so called "Powell ratio", which is job openings/jobseekers declined to 0.91, the lowest since early 2021, which keeps the “downside risks” to the jobs market intact for policy makers

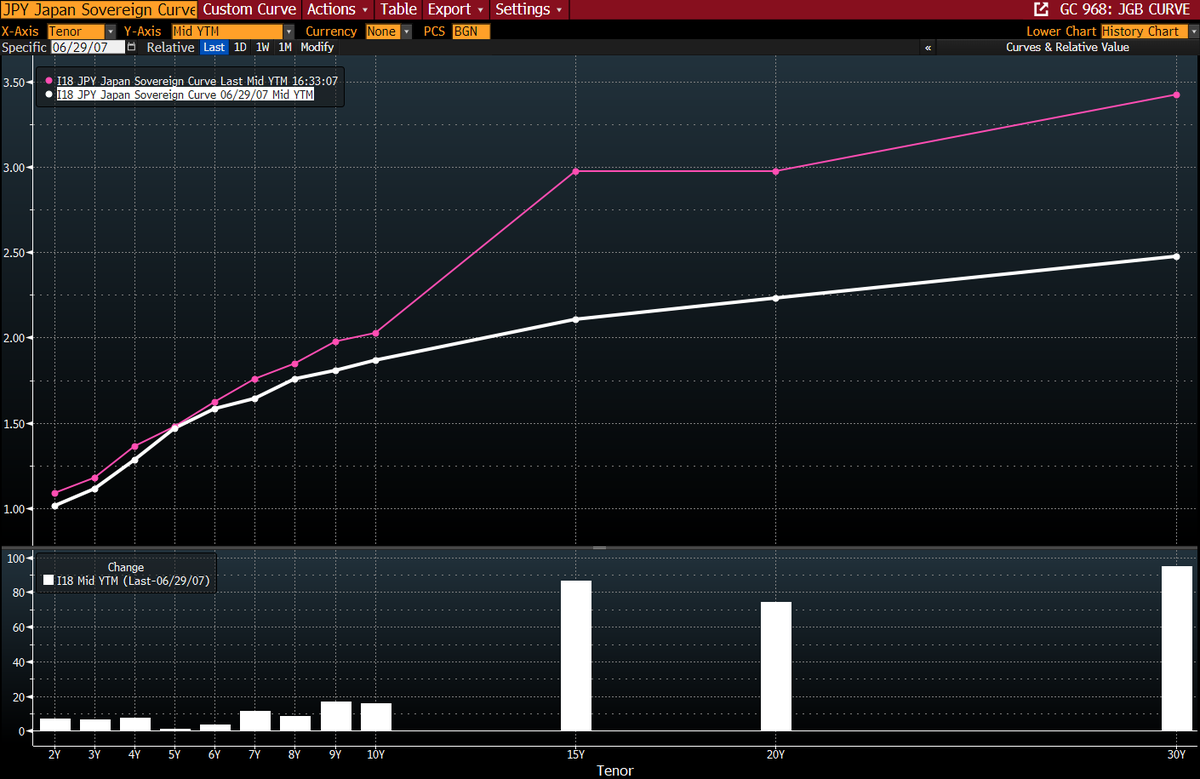

After the latest belly led selloff, the JGB curve up to 10y is now almost identical to June 2007, after two hikes had been delivered.

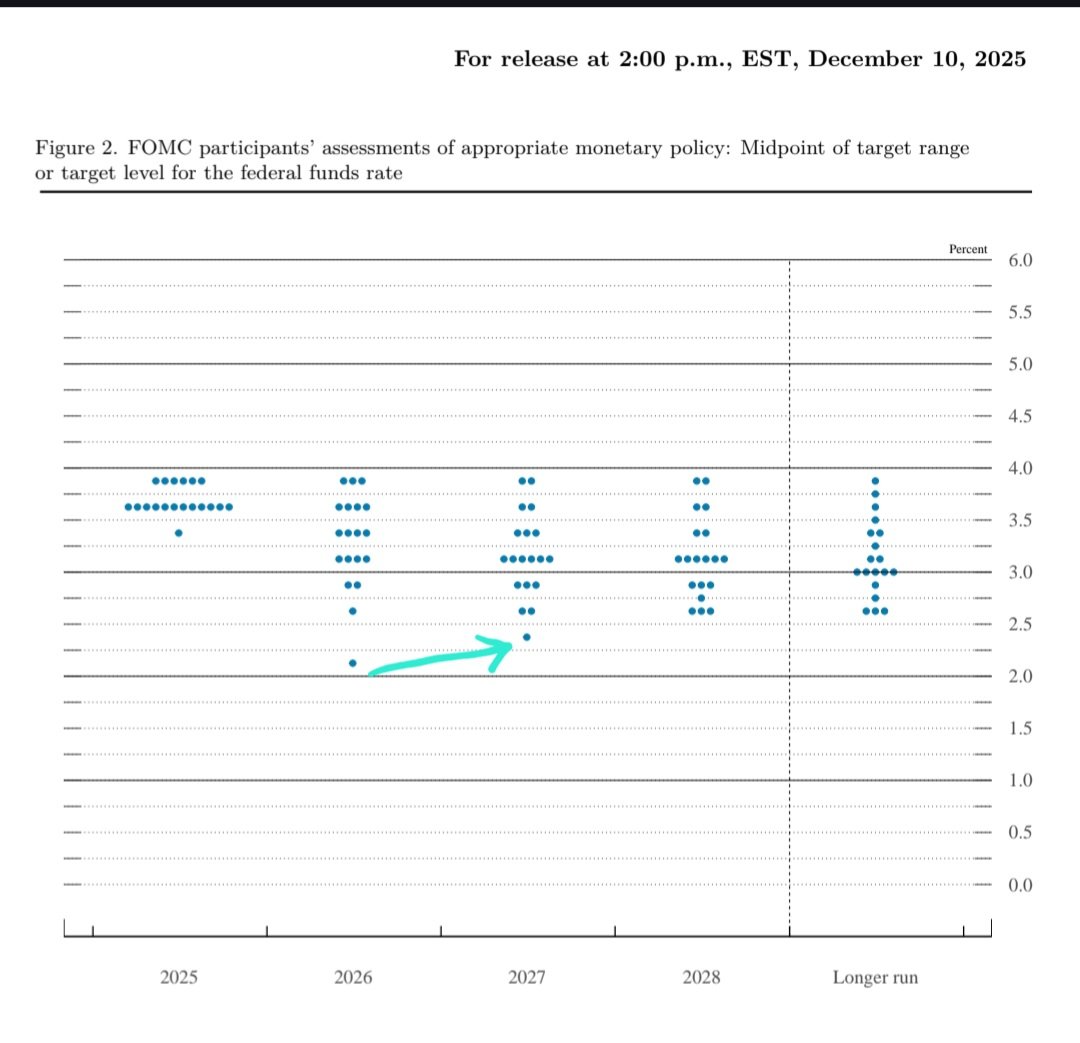

(Fwiw US unemployment was also 4.5% at this time).

Ken Tropin, a macro legend and founder of Graham Capital Mgmt on Macro Hive pod, asked on best macro opportunity/most likely to work... "I think term premia is underpriced, so I like the steepener as a general statement ... "

Insightful interview >>> https://t.co/gxUsCgqqrY

Most of the new EUR hike premia is coming in the 1y vs 2y gaps (whites/reds), 2y vs 3y (reds/greens) has barely moved. Probably due to the higher starting point.

In some places, reds/greens has flattened = market saying any hikes will be limited. V interesting cycle set-up.

If you're trading rates/macro, it's important to think about global policy cycles. The transition between easing/pause/tightening is vicious. We're seeing this right now in APAC markets... Since mid‑October, 2‑year yields: KRW +51 bp, AUD +48 bp, NZD +34 bp.

If you're trading rates/macro, it's important to think about global policy cycles. The transition between easing/pause/tightening is vicious. We're seeing this right now in APAC markets... Since mid‑October, 2‑year yields: KRW +51 bp, AUD +48 bp, NZD +34 bp.

ECB's Schnabel introducing a new term and acronym... "Quantitative normalisation". QE > QT > QN > ?

Also says ECB b/s will end with structure tilted "towards shorter-dated assets" (I read: term premia keep rising).

https://t.co/mA3EYiMSmF

Bessent tells Maria Bartiromo that the Fed's caution on further rate cuts isn't warranted because inflation isn't going to be a problem:

"The decision to cut rates by 25 basis points, I applaud. But the language that went with it tells me that this Fed is stuck in the past. Their inflation estimates have been terrible so far this year. They keep coming down, inflation keeps coming down and their models are broken. And I'm just not sure what they're thinking here in terms of signaling that they may not want to cut rates at the December meeting. They've got a lot to answer for not only for this year but for many years past, both in their GDP estimates and their inflation estimates, which are consistently wrong. And we're going to find a leader who is going to revamp the entire institution in terms of process and inner workings."