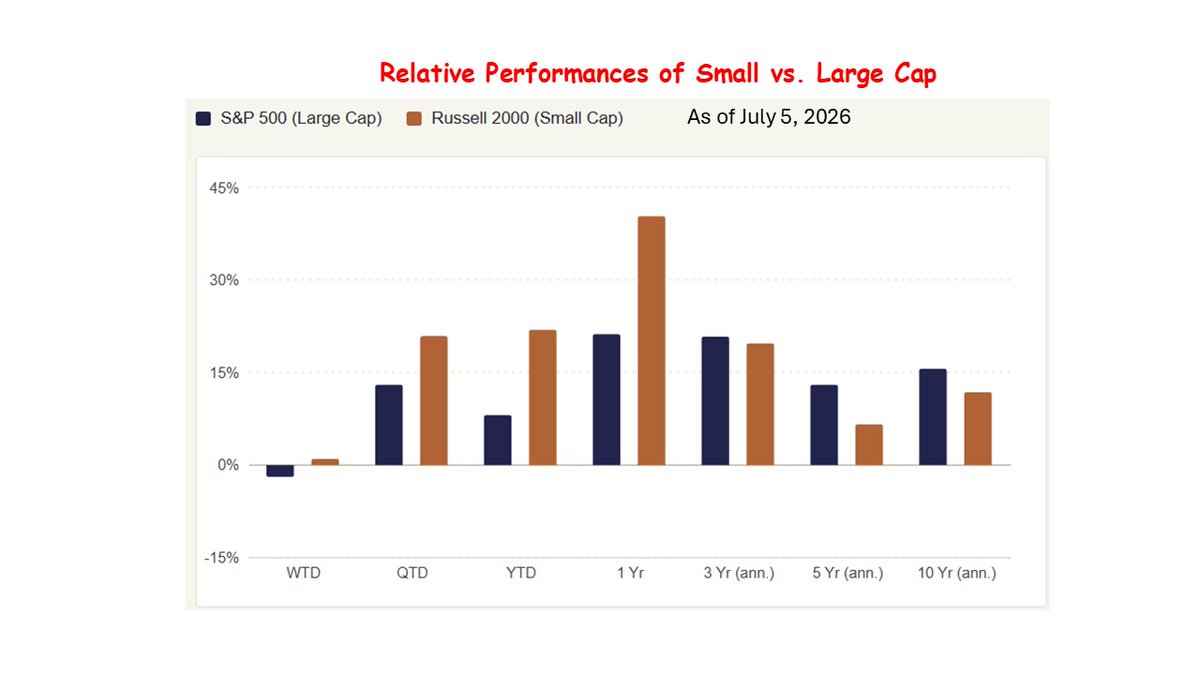

Why Small-Cap Stocks Are Finally Beating the Giants

Small-cap stocks are having a rare moment in the sun. After years of lagging behind the S&P 500 and the giant technology companies that dominated the market, Russell 2000 has become one of this year’s strongest performers. Through July 6, the Russell 2000 was up 21.3% year to date, compared with 10.1% for the S&P 500. In the first half of 2026, small caps had their best start to a year since 1991.

The June report changes the labor-market story. The economy is not shedding jobs in a recessionary way, but the hiring engine is sputtering. Payroll growth is slower, revisions are negative, labor-force participation has fallen, leisure and hospitality is weakening, and job gains remain heavily dependent on health care and social assistance.

This is no longer a booming labor market. It is a “low-hire, low-fire” economy with less margin for error. The Fed is now less likely to hike soon, the dollar has weakened on that expectation, and investors will increasingly ask if the cooling trend will continue.

Is the Stock Market Overvalued? What P/E Ratios Are Telling Us

Valuation metrics are among the most powerful tools investors have for assessing whether stocks are cheap or expensive — and right now, several of them are flashing warning signs.

The market may well continue rising — AI-driven earnings growth, resilient consumer spending, or falling interest rates could justify today's multiples. But the data spanning 140 years is consistent: buying expensive markets produces disappointing long-term returns. Right now, by virtually every measure, the market is expensive.

CA Jobs Struggling in May

California’s May jobs report offered a small sigh of relief, but not a strong vote of confidence. The state added jobs again after a weak April, but the gain was tiny. Employers added only 3,100 nonfarm payroll jobs in May, while the unemployment rate stayed stuck at 5.3%.

That means California’s labor market is not collapsing. But it is not taking off either.

California still has the assets to lead the next economy. But for now, the Golden State remains an economy where many workers are still waiting.

A Peace Dividend, but Not Yet a Return to Normal

Oil prices have already voted in favor of the expected U.S.-Iran agreement. Brent crude fell more than 5 percent after news of the deal, dropping to about $80 a barrel. Financial markets welcomed the possibility that the Strait of Hormuz, which normally carries roughly one-fifth of the world’s oil, could reopen.

The agreement is clearly positive for the world economy. It reduces the danger of an immediate energy crisis, lowers inflation pressure and improves the outlook for consumers and financial markets. But the peace dividend will arrive slowly and could disappear quickly. Oil may be flowing again, but confidence will take much longer to rebuild.

Inflation Flared Up, But the Fire Did Not Spread Like Wildfire

Inflation rose again in May, but the damage was not as bad as feared. The Consumer Price Index increased 0.5% from April and 4.2% from a year earlier. That is still too hot for comfort. But the more important news was that the increase was concentrated mainly in energy, especially gasoline, rather than spreading widely across the economy.

That is why investors appeared relieved. The headline number was unpleasant, but the core number was calmer. Core CPI, which excludes food and energy, rose only 0.2% in May after a 0.4% increase in April. From a year ago, core inflation was up 2.9%. In plain English, inflation is still above the Federal Reserve’s 2% target, but the report did not scream “second inflation wave.”

Pope Leo XIV’s first encyclical, Magnifica Humanitas, on AI

The pope is treating AI as the new industrial revolution. The question is not whether AI is good or bad. The question is whether business, government, and society will use it to lift people up or to reduce them to costs, data points, and replaceable parts.

The pope’s message for business is practical: AI should make the economy more productive, but also more humane. The real test is not whether AI raises profits next quarter. The test is whether it creates better jobs, better services, fairer competition, more truthful information, and broader opportunity. If AI makes companies richer but workers more insecure, customers more manipulated, and society more unequal, then we have gained efficiency but lost wisdom.

The Job Market Refuses to Quit

The labor market was supposed to limp. Instead, it jogged. It was supposed to whisper “slowdown.” Instead, it shouted, “Not so fast.” The May jobs report was not a fireworks show, but it was a lot stronger than the gloomy expectations many had at the end of 2025.

The U.S. economy added 172,000 jobs in May, while the unemployment rate held steady at 4.3%. That is a solid report by almost any reasonable standard. It shows that the economy is slowing from the red-hot post-pandemic pace, but it is not cracking. Consumers are still spending, businesses are still hiring, and the job market remains one of the strongest pillars holding up the economy.

Gallup’s latest results show an unusual and troubling split in the American labor market. In 2025, only 43% of Americans ages 15 to 34 said it was a good time to find a job in their local area. By contrast, 64% of Americans ages 55 and older said it was a good time to find a job. That 21-percentage-point gap was the largest generational divide among 141 countries surveyed. In most countries, the pattern is the opposite: young adults are usually more optimistic about job opportunities than older adults.

The economic implications are serious. Older workers staying active is good for the economy. It increases labor supply, supports household income, raises tax revenue, and helps offset the effects of an aging population. Older consumers with jobs, pensions, homes, and financial assets can continue to spend on travel, healthcare, leisure, housing services, and financial products.

But a weak youth labor market is dangerous for long-term growth. Young workers build skills by working. If they cannot get first jobs or early-career training, the economy loses human-capital formation. Poor early labor-market experiences can leave lasting scars: lower wages, slower promotions, delayed household formation, weaker confidence, and reduced lifetime earnings. The result could be lower productivity growth in the future.

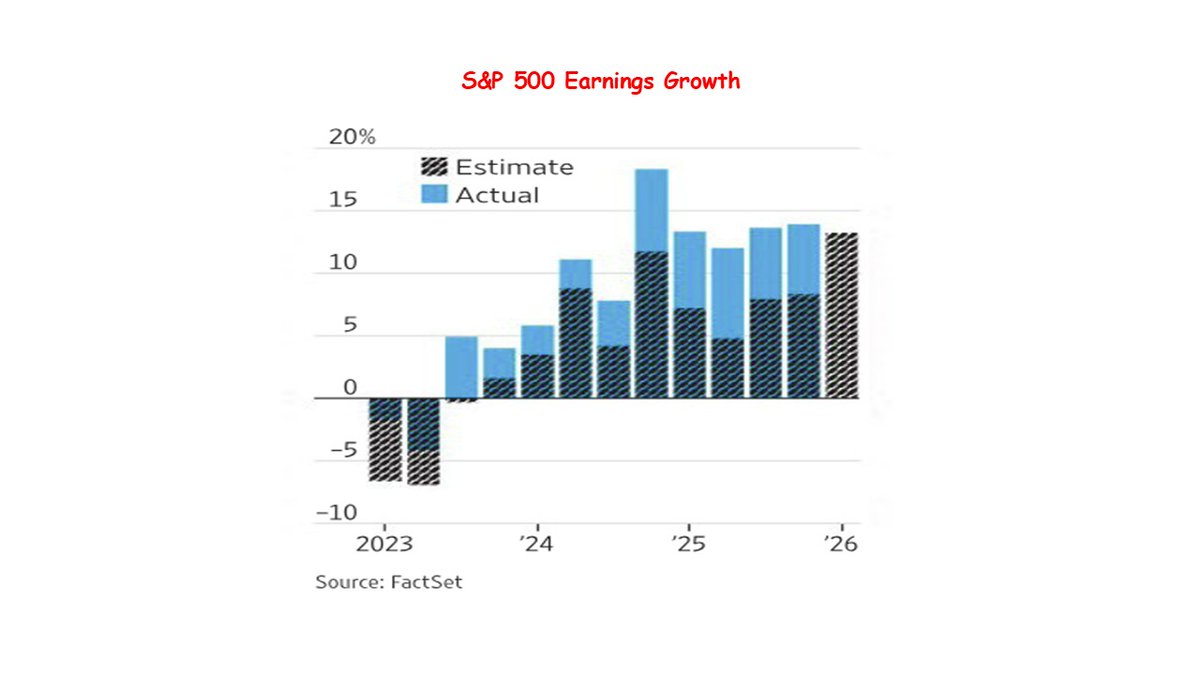

Why Has the Stock Market Been So Resilient?

The stock market has been climbing a wall of worry. Investors have had plenty to worry about: the Iran conflict, oil prices above $100, sticky inflation, high interest rates, tariff uncertainty, weak consumer confidence, and expensive stock valuations. Yet the S&P 500 has remained close to record highs. The reason is simple: investors believe the earnings engine is still powerful enough to outrun the risks.

The best conclusion is this: the market’s engine is strong, but the price of admission is high. Stocks have been resilient because earnings, AI, and productivity are still winning the argument. But with valuations stretched and geopolitical risks elevated, the market has little room for disappointment.

The April Consumer Price Index report was a setback for hopes that inflation was steadily moving back toward the Federal Reserve’s 2% target. Consumer prices rose 0.6% in April, following a sharp 0.9% increase in March. Over the past 12 months, the CPI rose 3.8%, up from 3.3% in March. That is not a minor fluctuation. It shows that inflation pressures have reaccelerated at a time when the Fed was looking for more evidence that price increases were cooling.

The bottom line is that inflation has not disappeared. It has changed form. Energy is the biggest visible problem, but the more important issue is that inflation pressure has broadened into food, shelter, and services. For consumers, that means the cost of living remains uncomfortable. For the Federal Reserve, it means rate cuts are likely to be pushed further into the future.

April Jobs Report: Better Than Expected, Not All Good

The April employment report was better than expected. Payrolls rose by 115,000, stronger than many economists had anticipated.

But the details were less reassuring. The unemployment rate rose on an unrounded basis to 4.34% from 4.26%, the number of unemployed workers increased, the labor force declined, and nearly half of the job gains came from health care and social assistance.

The labor market is clearly losing breadth and momentum. The Federal Reserve is likely to hold interest rates steady while waiting to see how the Iran war, higher energy prices, and inflation pressures plays out in the future.

The Economy Rebounded, but Inflation and Tariffs Complicate the Outlook

The first-quarter GDP report shows that the U.S. economy regained momentum after a weak end to 2025, but the details are not entirely reassuring. Real GDP grew at a 2.0% annual rate in the first quarter of 2026, a clear improvement from the 0.5% growth rate in the fourth quarter of 2025.

On the surface, this suggests that the economy has moved past the temporary weakness caused by the government shutdown and other distortions late last year. But underneath the headline number, the economy is sending a more complicated message.

Growth improved, but inflation accelerated, consumer spending slowed, imports jumped, and the future path of the economy remains clouded by tariffs, energy risks, and uncertainty about Federal Reserve policy.

The Stock Market after the Iran War

Despite the war, higher oil prices, and concerns about global shipping and energy supplies, the U.S. stock market has continued to move higher and set new records. That may seem surprising, but history suggests it should not be shocking.

The conclusion is simple: long-term investing has paid because America’s economy has repeatedly survived shocks that once seemed unbearable. Wars, recessions, terrorist attacks, financial crises, inflation scares, and pandemics have all tested investors. Yet over the long run, the stock market has recovered and moved higher.

The Iran war is serious. But history shows that investors who stay focused on the long term, rather than reacting to every crisis, have usually been rewarded. Short-term fear can dominate the headlines. Long-term earnings, innovation, and economic growth have dominated the market.

Long-term Economic Consequences of the Iran War

The recent Iran conflict has triggered more than a temporary spike in energy prices—it has created a structural shift in the global economy that will unfold over years rather than months.

While the initial market reaction has focused on the sharp rise in oil and gasoline prices, the deeper story is the emergence of a higher-cost energy environment that will shape growth, inflation, and global competitiveness well beyond the end of hostilities.

This is not simply a short-term disruption tied to a geopolitical event. It represents a reconfiguration of the global energy landscape and, by extension, the global economy.

The defining feature of the post-conflict period will not be the volatility of energy prices, but their higher floor. In that environment, the central economic challenge is no longer waiting for conditions to normalize but learning to operate efficiently in a world where energy is more expensive and the margin for error is considerably smaller.

Possible Economic Consequences of a Prolonged War

The failure of the U.S.-Iran talks has raised the risk of a stagflation shock. That means the world could face weaker economic growth and at the same time higher inflation.

This is no longer just a theoretical risk. Oil prices have already moved back above $100 a barrel, and the U.S. is blocking traffic to and from Iranian ports. Because of that, the main economic question is no longer whether renewed conflict would matter. The real question is how long the disruption lasts and whether it spreads beyond Iranian oil flows.

A rule of thumb is that every persistent 10% increase in oil prices lifts global headline inflation by about 0.4 percentage point and lowers global output by 0.1% to 0.2%.

Inflation is the clearest and fastest channel through which this shock would spread. First, energy prices rise directly: gasoline, diesel, jet fuel, electricity, and heating costs move up. Then indirect effects follow. Higher energy costs feed into freight, airfare, plastics, chemicals, agriculture, food processing, and many services that depend on transportation.

Over time, a prolonged shock can spread beyond energy and make inflation broader and more stubborn.

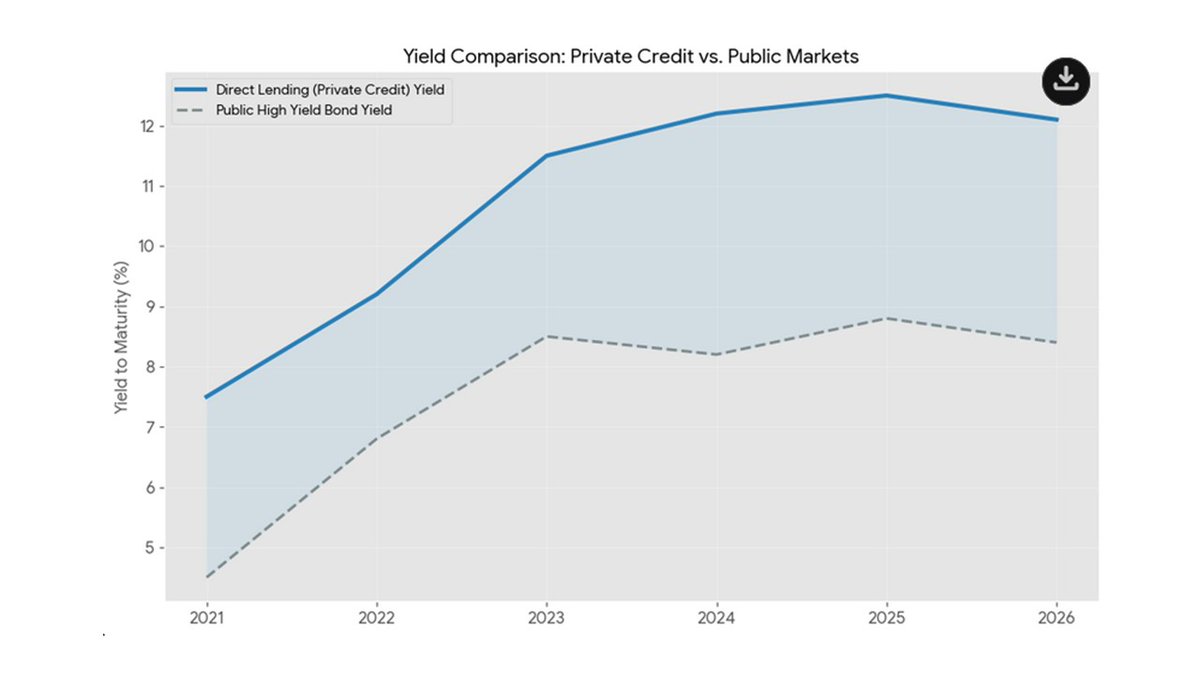

Private Credit: Canary in the Coalmine?

Private credit has grown into a major part of global finance. What began after the 2008 financial crisis as a replacement for bank lending has expanded into a roughly $2 trillion market, providing financing mainly to middle-market companies and private equity portfolio firms.

Strong investor demand fueled its rapid expansion. Institutional investors such as pension funds and insurance companies, along with wealthy individuals, were attracted by relatively high yields—often between 8 and 14 percent—and the protection offered by floating interest rates.

The market operates largely outside traditional banking regulation. Because loans are negotiated privately and do not trade in public markets, there is less transparency in pricing and oversight compared with bank loans or publicly traded bonds.

Several vulnerabilities are beginning to emerge. These include uncertain valuations of loans that do not trade regularly, liquidity pressures in funds that promise redemptions while holding illiquid assets, and the growing use of payment-in-kind interest that can mask financial stress among borrowers.

The industry is entering a more mature phase. While weaker lenders may face problems as credit conditions tighten, stronger firms with restructuring expertise and a shift toward asset-backed lending are likely to remain an important and permanent part of the financial system.

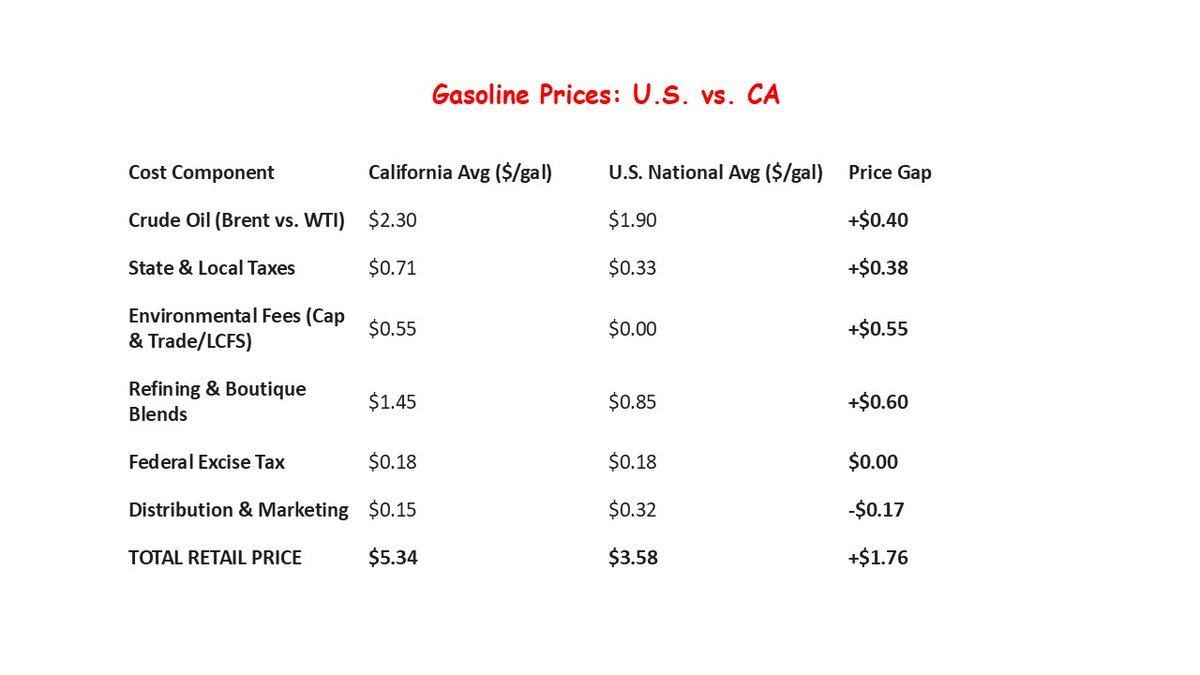

Why California Gas Prices Are Higher and More Volatile

· The conflict involving Iran illustrates how global geopolitical events can affect regional markets in very different ways. While the United States has become more energy independent due to the shale revolution, California remains structurally isolated from the nation’s energy infrastructure.

· As long as the state continues to function as a “fuel island” with limited pipelines, specialized fuel requirements, and shrinking refinery capacity, gasoline prices will remain higher and more volatile than in most other parts of the country—especially when global tensions disrupt oil supply routes.

Gasoline prices often rise quickly and fall slowly, a pattern known as the Rockets and Feathers effect.

• Retailers raise prices quickly when oil prices increase because they expect higher replacement costs for future fuel supplies.

• Oil markets respond to expectations of future disruptions, not just current supply levels.

• Geopolitical tensions create a risk premium in oil prices even when oil continues to flow normally.

• Financial investors buying oil futures during crises can push prices higher in the short run.

• Higher shipping costs and war-risk insurance during conflicts also raise oil prices.

• When oil prices fall, gasoline prices decline more slowly because retailers still hold higher-cost inventory.

• Regional factors such as limited refinery capacity, special fuel regulations, and geographic isolation can cause even larger gasoline price swings, as seen in California.

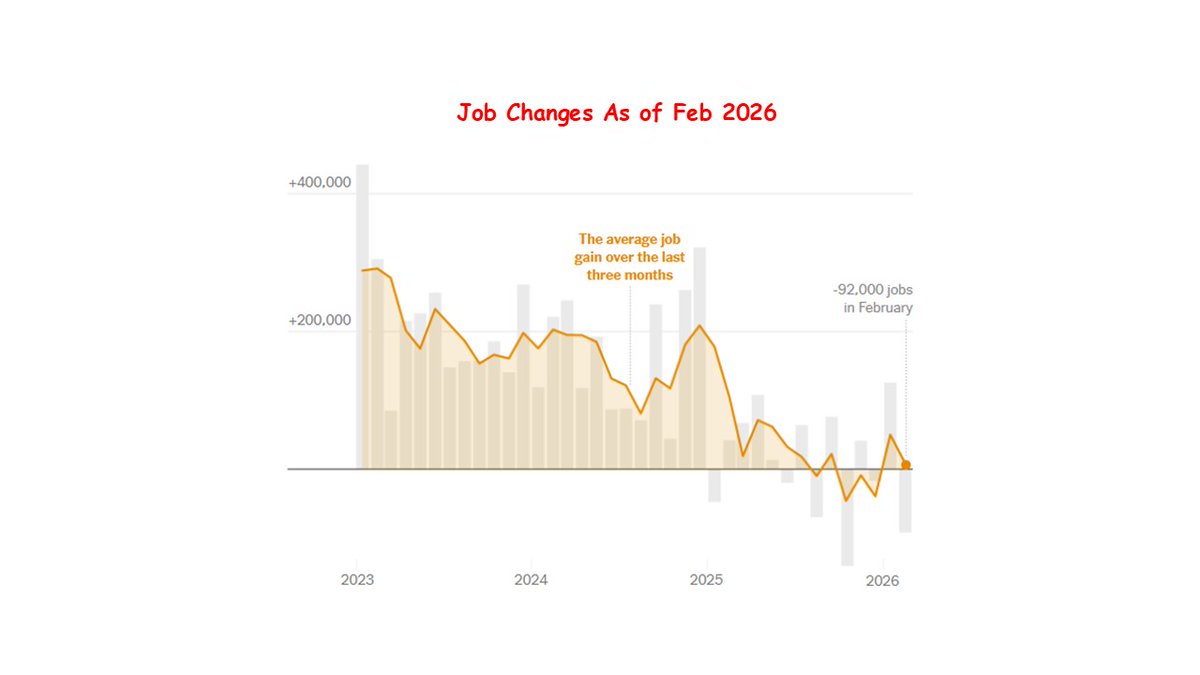

Cooling Labor Market

The labor market softened more than economists expected. Total nonfarm payroll employment declined by 92,000 jobs, while the unemployment rate edged up slightly to 4.4 percent.

The decline in payroll employment came as a surprise. We had expected modest job growth. However, some of the weaknesses reflected temporary factors, including strike activity in the healthcare sector and continued declines in several industries that have been experiencing structural adjustments.

Overall, the report suggests that the U.S. labor market is cooling gradually after several years of unusually strong employment growth.