@Malone_Wealth Ryan could have just owned up better to the dilution. Clearly there would be dilution, and it’s not necessarily bad for shareholders if the deal works. But avoiding going into any further detail than half cash have shares, it’s on the website seemed a little avoidant.

@ryancohen@ryancohen …you probably don’t want to hear this, but maybe…

Turn GME into a Physical Asset Trust.

Buy silver, all the silver. Break the paper trade. Issue more GME ATM, buy more silver.

Repeat.

Then when you’ve bought all the silver, buy platinum, then companies.

$GRCE I initiated a position in Grace Therapeutics ahead of its near-term FDA PDUFA target date of April, 23 for GTx-104, an IV formulation of nimodipine for aneurysmal subarachnoid hemorrhage (aSAH).

The core of the thesis is that this is being misclassified as a high-risk biotech binary when, in reality, it is closer to a delivery optimization of an already-proven therapy. Nimodipine has been the standard of care for decades, but oral administration in ICU settings is inconsistent and often interrupted. GTx-104 addresses this directly through controlled IV delivery, improving pharmacokinetics and dosing reliability.

The mechanism of action is already validated; GTx-104 is reformulation accompanied by a new delivery method, where safety, consistency of exposure, and clinical practicality are the primary drivers of approval. The Phase 3 data demonstrated improved dose consistency and a reduction in hypotension events, which are directly relevant in this patient population.

$BMEA

Biomea Fusion has a Phase 1 obesity trial running for its oral GLP-1 candidate BMF-650. We have a near term readout of 28-day weight loss data expected in Q2 2026.

But what makes Biomea even more interesting is their other asset.

Icovamenib (their menin inhibitor) has shown in preclinical work that when paired with GLP-1 therapy it may enhance metabolic efficiency while preserving lean muscle mass vs GLP-1 alone.

If that concept translates clinically, it opens the door to a metabolic stack:

GLP-1 for appetite suppression + menin inhibition for improved metabolic function.

So the near-term catalyst is the BMF-650 Phase 1 readout, but the longer-term thesis could be the combination approach.

Worth keeping on the radar, this company is still very small, and BMF-650 is only in Phase 1, and Icovamenib Phase 2 but if I’m watching these results I can only assume Lilly, Merck and Novo are too.

$LLY $MRK $NVO

#PerplexityComputer

Worked some more this morning; I thought additional prompting might help. While Computer is proficient in some tasks, sometimes it has the reasoning skills of an ADHD child. I went through three iterations, and after $30 in token burn I gave up.

This model, at least, is not going to replace traditional coverage anytime soon. Maybe if I build out the processes and framework from scratch, but continued iterations are just token burn, so back to square one.

MoonLake

Specific prompting for all projections to be fully data‑driven, and to look beyond top‑line readouts to surrounding data points as well. I specified not to give weighting to opinions or research speculating on the probabilities of approval (trying to filter for garbage‑in/garbage‑out groupthink) and instead to focus on safety, efficacy, and data, and to attempt to form an independent opinion based on what the FDA would be reviewing. Market penetration modeling should be based on TAM as well as competitive positioning on potential labeling, safety, and efficacy.

First iteration:

Errors everywhere. Despite my request, it went back to analyst consensus to form an opinion, BLA timing was wrong, cash runway was wrong, indications were missing, it even got the company website wrong, and it falsely suggested SLK had no oral candidiasis instances.

Second iteration:

Computer fixed some probability weightings and added back in the oral candidiasis data, but then refit the DCF to match the prior price target, which is completely backwards. Computer noted that the DCF did not match the price target but, since I did not specifically ask it to adjust, it moved on.

Third iteration:

It jumped from a low‑$30s price target straight to almost $200. It was missing the PsO indication completely and still missing additional rheum or derm indications beyond the current pipeline. The terminal value in the DCF was far too high for a biotech. Probabilities of approval still seem wrong.

At this point I was over $30 into this report, but I believe that if I attempted to fix everything that was wrong, it might take another $100. There is still too much to fix. I quit; back to scratch.

Failed experiment?

No. We learned something.

The takeaway:

Computer is a better model than most, but we should not be relying on output from AI at all for investment valuation at this point. It might look professional, but the gaps and errors are pervasive. Maybe a ground‑up, process‑based framework will fix this; maybe not.

Back to work.

https://t.co/antL2lG7TC "Computer"

I got a chance to test it out tonight, first prompt took way too long; it was a simple "Hi! What can you do?"

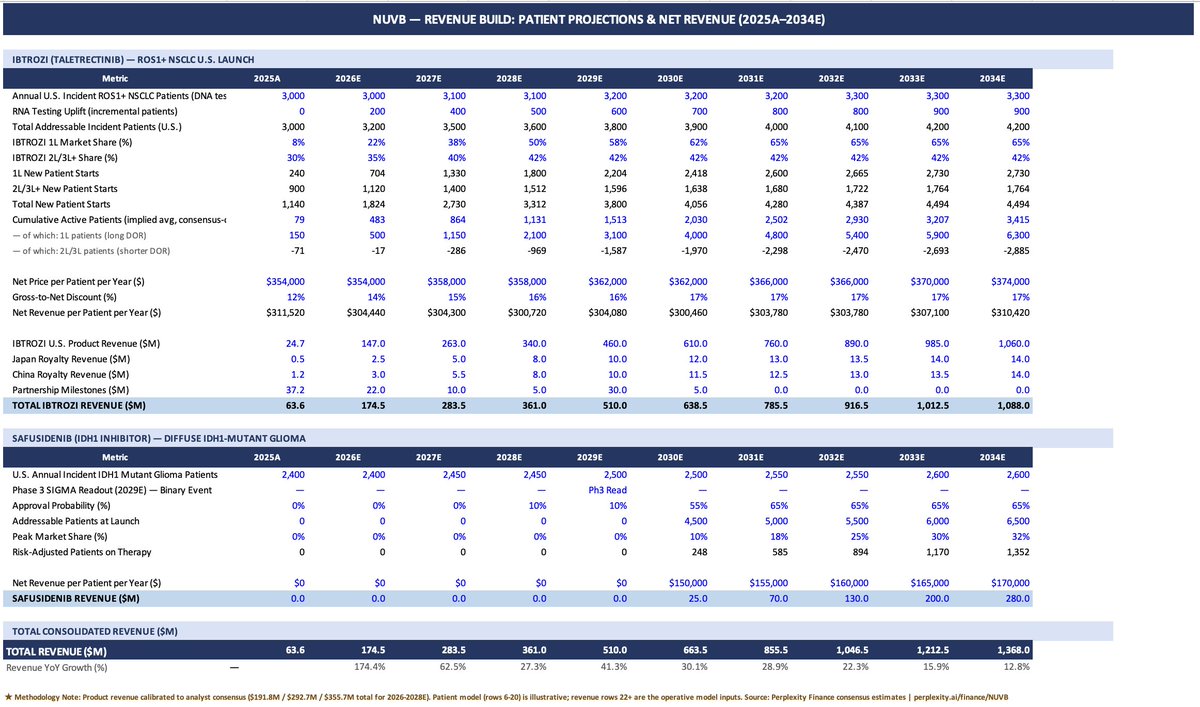

Second prompt, something on my list to build out and actually look at on excel: a DCF model for $NUVB.

Took a while and burned about $2 in token costs... I asked a simple question on a number that seemed off to me, just asking to explain. It reworked the spreadsheets, I'll say it did seem more reasonable on the second iteration. Another $1+ in tokens.

Expensive? I thought so... this should have been optimized much better, I thought the token burn was excessive.

Biggest issue I have is the lack of conviction. Just simply asking to explain a number caused it to completely rework a DCF model, and swung all the valuation figures wildly.

That is concerning.

I was surprised by the time it took. The 3 prompts took almost 14 minutes of working time.

The Computer model was much more robust than a standard response from an LLM. Night and day differences. And my prompt was very simple.

I don't think it's quite ready to replace me, but with some additional prompting it might not be that far off...

I've got a dedicated Mac on the way tomorrow to setup a custom Open Claw model. I'll be interested to see the differences after some customization.

Just to burn some extra tokens, (almost $4 worth) I had it take a look at the silver markets... response was much worse, material errors throughout.

Most of the problems seemed to stem from the sources.

Computer pulled references from Substack that were flat out misinformation, but also sources like Bank of America or J.P. Morgan, which while the information was not wrong, at this point, the information was stale.

Stale information is just as good as wrong information in a situation like this.

Worth the token burn... not even close.

Some screenshots of the $NUVB output... I think some of the penetration I would have modeled differently, but here it is for anyone interested. Consider this more research on AI capabilities than on Nuvation Bio.

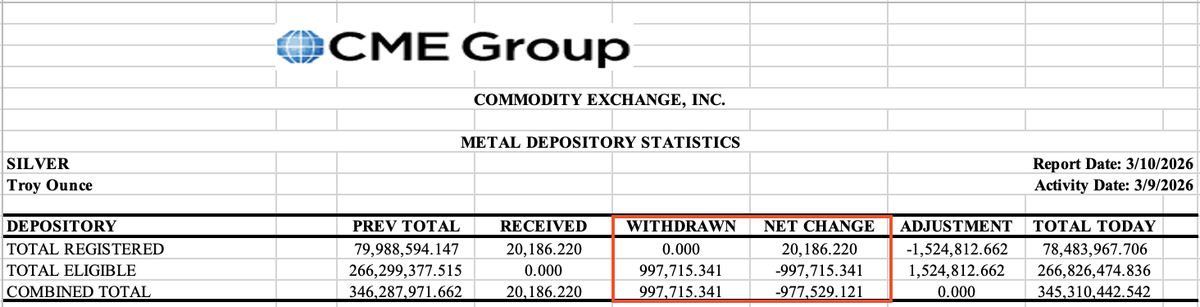

COMEX. Another light day yesterday. Less than a million ounces of #Silver withdrawn.

Trend continues, but it will be interesting to see if there is sustained deceleration.

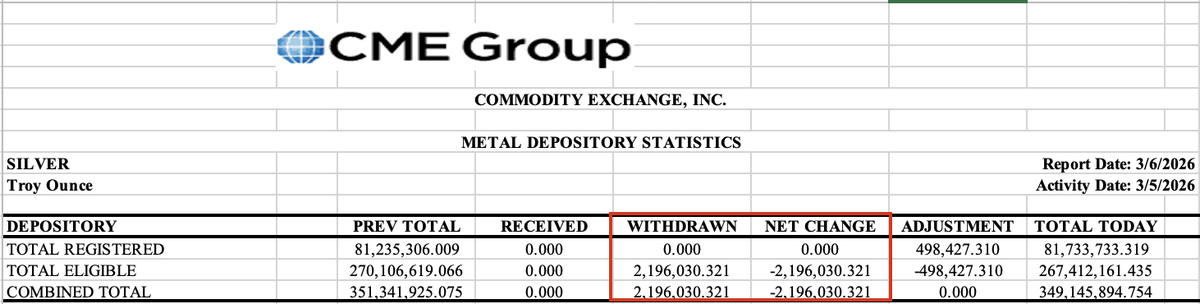

COMEX. A fairly normal day... just a little over 2 million ounces of silver withdrawn.

The problem is that this has become normalized, and outflows are persistent...

CME does not have unlimited silver stock to support millions of ounces being withdrawn daily.

#SILVER $SLV $PSLV $SIVR

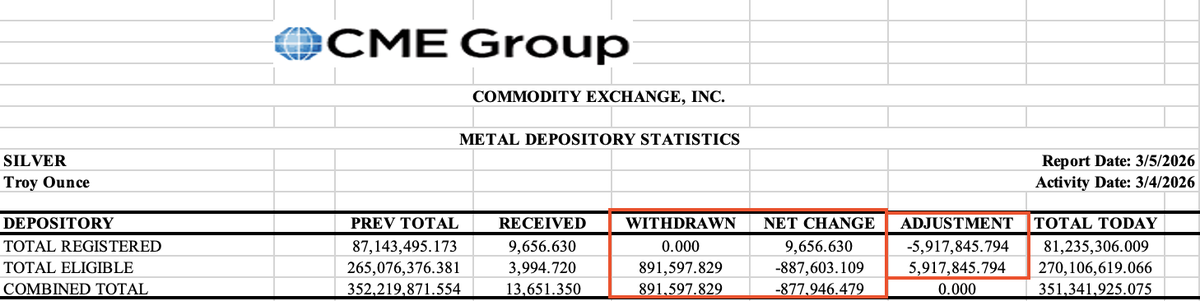

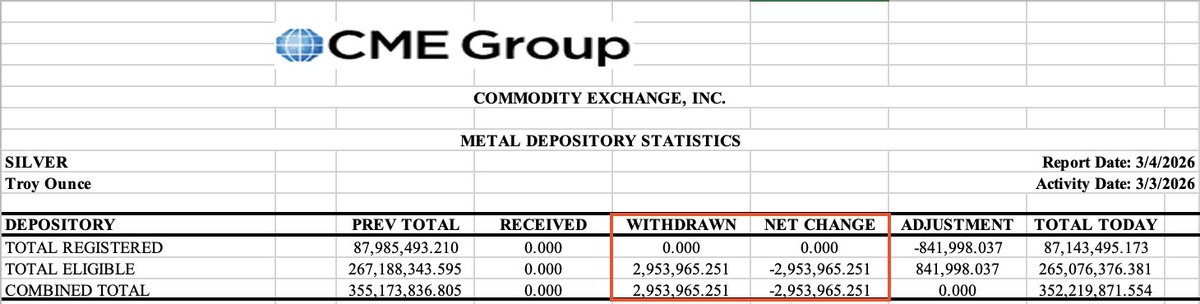

COMEX Silver!

Wednesday's activity report, March 4th.

Registered silver fell almost 6 million ounces! In addition we had nearly 1 million ounces withdrawn.

For a refresher - registered silver is available for immediate settlement of futures contracts.

February 9th, 2026 we had over 101 Million ounces registered, less than a month later we have lost approximately 20% of the collateral backing immediate settlement of futures contracts.

This trend has been ongoing.

Demand exceeds supply.

$SLV $SIVR $PSLV #Silver