Passionate father of 3, deeply in love with my 1st crush. Retired from the corporate world Working 365 days/yr, On vacation just as much! #DYOR no advice

I'm not FI (I'm rich of time, but don't have millions).

Never going to be RE (I love working).

No interest in reaching FIRE (requires too much saving and not enough fun).

Yet, I found a way to enjoy freedom and have all the time in the world. Find your way, it's possible!

You can afford the trip. So why does booking it feel wrong? 😬

For 40 years, saving was the goal and spending the enemy. That built your retirement, but now the habit holds you back.

The saving muscle is strong. The spending muscle needs training too.

#RetirementSpending

Dividend investors love to misuse one number: the payout ratio.

Under 80% safe, over 80% unsafe, done. That shortcut tosses out great companies and keeps bad ones. How to read it properly 📊

https://t.co/2UBpBdGxAr

#payoutratio

You spent 40 years learning to save. Nobody taught you to spend. 💸

That switch is the hardest part of retirement.

This week: why savers freeze, why spending is the plan working, and how to enjoy what you built.

Harder to spend than you expected?

#RetirementSpending

The shift that changes how you invest:

Stop judging a holding by yield alone. Ask the bigger question: what's my total return, income plus growth, over the years I hold it? Buy the whole return. Not just the cheque. 🧭

#DividendGrowth

Before you sell the house and chase the sun: live there first. 🌅

Visit in different seasons. Rent before you buy. Talk to a cross-border planner 12-18 months ahead.

The happy expats went in with eyes open.

Where would you retire if you could go anywhere?

#RetireAbroad

Want total return on overdrive? Reinvest the dividends. 🔁

Each one buys more shares, which pay their own dividends, which buy more shares. The snowball builds on itself. Over decades, that compounding does the heavy lifting.

#DividendGrowth

Think your Canadian accounts just follow you abroad? Many do not. 🏦

As a non-resident, some brokerages freeze accounts, and your TFSA loses its tax-free magic outside Canada.

Line up where your money will live before you move.

#RetireAbroad

Leaving Canada for good can trigger a "departure tax." 💸

Become a non-resident and Canada can tax some investments as if you sold them on the way out.

CPP, OAS and pensions still reach you, often with tax withheld first.

Plan with a cross-border pro.

#RetireAbroad

The trap with chasing income alone:

A stock can pay a steady cheque while its price slowly sinks. You feel paid, but your capital is shrinking underneath you. That's not income. It's your own money, minus the loss. 🪤

#DividendGrowth

Something the market does reliably over time:

When a company raises its dividend year after year, the share price tends to climb with it. A growing payout signals a healthy business, and buyers pay up. Income and growth feed each other. 📈

#DividendGrowth

The one that catches people: your provincial health coverage can lapse if you are away too long. 🏥

Care abroad, or flying home for an emergency, can cost a fortune without a plan.

Get solid international health insurance. First, not last.

#RetireAbroad

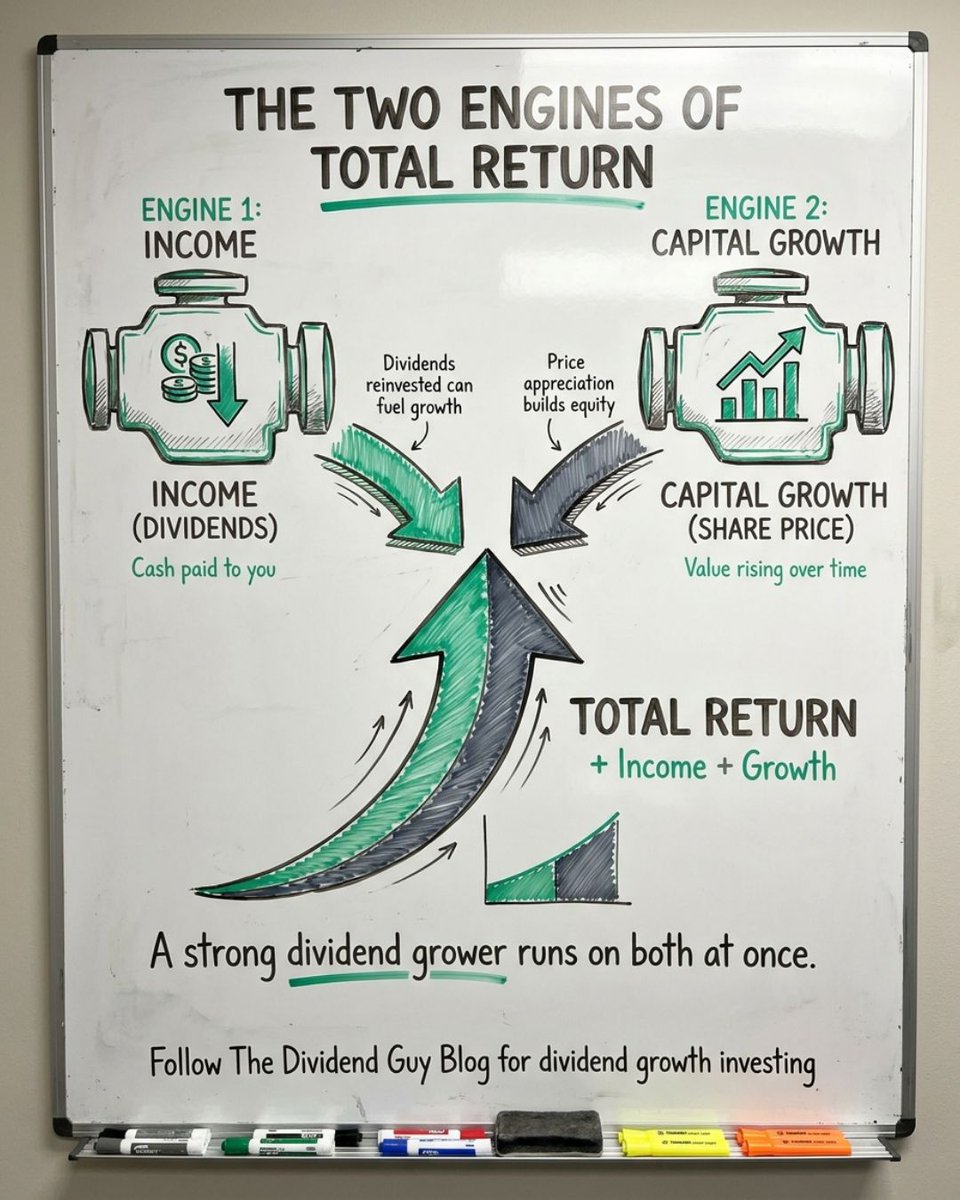

Total return runs on two engines:

1. Income, the dividends in your account.

2. Capital growth, the rising value of your shares.

A strong dividend grower fires both. One engine glides. Two flies. ⚙️

#DividendGrowth

Wintering abroad and moving abroad are not the same thing. ✈️

Stay part-year, keep your home and ties in Canada: you usually stay a resident.

Move for good: you become a non-resident, and taxes change.

Know which you are before you book.

#RetireAbroad

Most dividend investors watch one number: the income. They're missing half the story.

Total return = the dividends you collect + the growth in the share price underneath them. This week: why the cheque is only half the picture. 📊

#DividendGrowth

Retiring abroad is the dream: sun, lower costs, adventure. 🌍

But the fine print is where it gets expensive.

This week: residency, the health-coverage trap, tax surprises, and how to test it first.

Ever thought about retiring in another country?

#RetireAbroad

How to tell a healthy high yield from a trap? Run it through the Triangle.

Revenue and earnings still growing? Dividend still rising? Payout ratio reasonable? A high yield with cracks underneath is a value trap in costume. 🔺

#DividendGrowth

The number that beats today's yield: yield on cost.

Buy at 3%, let the dividend grow a decade, and you can be earning 7-8% on what you originally paid. You don't chase a high yield. You grow one. 🌱

#DividendGrowth

Run this retirement stress test once a year:

1. Cash wedge of 24 to 36 months?

2. No holding over 10% of income.

3. 80%+ in core holdings.

4. Survive a 30% drop in year one without selling?

5. How did you act in 2020 and 2022?

📋

https://t.co/WYcFgvit8F