I know there are questions you're thinking through, decisions you're trying to make and outcomes you're trying to understand. So ask the right question first.

𝗗𝗲𝗰𝗶𝘀𝗶𝗼𝗻.

𝗪𝗵𝗮𝘁 𝗺𝗮𝗸𝗲𝘀 𝘆𝗼𝘂 𝘀𝗼 𝘀𝘂𝗿𝗲 𝘁𝗵𝗲 𝗱𝗲𝗰𝗶𝘀𝗶𝗼𝗻 𝘆𝗼𝘂 𝗺𝗮𝗱𝗲 𝗶𝘀 𝗮𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝘁𝗵𝗲 𝗿𝗶𝗴𝗵𝘁 𝗼𝗻𝗲?

The confusion usually starts when the outcome begins changing and the situation no longer feels as obvious as it once did.

The numbers/situation may still look strong but something feels different.

Sometimes expectations move ahead of reality before most people notice it.

Sometimes the visible outcome is actually being driven by something most people are not paying attention to yet.

And sometimes two situations that once looked almost identical slowly begin leading to completely different outcomes because the assumptions, incentives, timing, execution or starting conditions were different from the beginning.

That’s usually where the confusion starts.

Not because information is missing. Most information is already available.

𝗕𝘂𝘁 𝗺𝗮𝘆𝗯𝗲 𝘁𝗵𝗲 𝗯𝗶𝗴𝗴𝗲𝗿 𝗽𝗿𝗼𝗯𝗹𝗲𝗺 𝗶𝘀 𝘁𝗵𝗮𝘁 𝗽𝗲𝗼𝗽𝗹𝗲 𝗼𝗳𝘁𝗲𝗻 𝘀𝘁𝗮𝗿𝘁 𝘀𝗲𝗮𝗿𝗰𝗵𝗶𝗻𝗴 𝗳𝗼𝗿 𝗮𝗻𝘀𝘄𝗲𝗿𝘀 𝗯𝗲𝗳𝗼𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴 𝘁𝗵𝗲 𝗿𝗶𝗴𝗵𝘁 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀.

Because sometimes the answer is visible. The real question is what’s still missing.

So why does the same situation still look completely different to different people?

The difficult part is understanding:

➖what is actually driving the outcome,

➖what patterns or signals already exist,

➖what assumptions people are making,

➖what is just noise,

➖and what could become important long before the outcome becomes obvious in hindsight.

I think a lot of complex situations start making more sense once you stop looking at them as isolated events.

Usually there are multiple forces interacting together:

+ expectations,

+ incentives,

+ money flow,

+ execution,

+ constraints,

+ timing,

+ pressure points,

+ second-order effects,

+ and small decisions compounding over time.

Which is also why reacting to the visible outcome is usually the easy part.

The harder part is identifying the root cause, thinking through cause & effect, and seeing how small changes in one variable can slowly change the entire outcome later.

A lot of important decisions are also made before the full picture becomes clear.

Which means you rarely get perfect information, perfect timing, or complete certainty.

Sometimes you are working with patterns.

Sometimes probabilities.

Sometimes incomplete signals.

And sometimes the only real edge is seeing the situation a little more clearly before everyone else does.

𝗢𝗿 𝗺𝗮𝘆𝗯𝗲 𝘁𝗵𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻 𝗶𝘀:

𝗔𝗿𝗲 𝘄𝗲 𝗲𝘃𝗲𝗻 𝘀𝗼𝗹𝘃𝗶𝗻𝗴 𝘁𝗵𝗲 𝗿𝗶𝗴𝗵𝘁 𝗽𝗿𝗼𝗯𝗹𝗲𝗺,

𝗼𝗿 𝗷𝘂𝘀𝘁 𝘀𝗼𝗹𝘃𝗶𝗻𝗴 𝗶𝘁 𝗮𝘁 𝘁𝗵𝗲 𝘄𝗿𝗼𝗻𝗴 𝗹𝗲𝘃𝗲𝗹?

That’s mostly what I try to think through and break down here. Whether it’s a stock, sector, business, market behavior, life decision, or any other complex situation.

If you read all of this carefully, you probably already understand the kind of thinking I’m interested in.

So if there’s a stock, business, life decision, or any complex question you’ve been thinking through but never really discussed properly, feel free to comment with a little context around it.

Would genuinely like to think through it together.

Okay listen. You want to take a decision about battery chemicals stocks, right?

And yes, the market is down. If you can't take the opportunity now, then when will you?

But what I'm saying is, before taking any decision, understand the value chain carefully, not just what you see or read. Try to think differently.

Think like this:

- Where could the market actually create value first, and what evidence would prove it?

- What is the market already assuming will happen, and what is still uncertain?

- Which event could change the entire narrative, not just the next quarter?

- If the business works, what must happen next, and then what?

- If you could track only a few things for the next two years, what would they be?

See, the goal is to move from what is the company doing? to what is the market waiting to see, what changes if it happens, and how do I know if I'm right?

Information is rarely the problem, the challenge is knowing which signals matter and which are just noise.

You already know the revenue, EBITDA, margins, capacity, guidance and orders. But some questions still remain and sometimes those questions matter more than the numbers.

So for that, read this PDF.

Long PDF? Who reads that much?

You will, because you want to take good decisions, right?

It covers GFL, Himadri, PCBL, Neogen, HEG, Acutaas, and Tatva. Basically, cathodes, anodes, electrolytes, salts, additives, and binders.

From signals to triggers, timelines to bottlenecks, everything is there and at the end, there are a few tables mapping the ecosystem with companies like Ola, Exide, and Amara Raja to help you get more clarity.

- What is the one event that changes all these stories from potential to reality?

https://t.co/5DyRKU0C3a

Ram Nikesh Ji, yes, Sudeep is also connected. They have created a dedicated subsidiary called "SAM" for the EV and energy storage.

The reason I did not include it in the post is that I was more focused on cathodes, anodes, electrolytes and recycling.

But if you look at the full chain, Sudeep sits one step before the cathode material.

They are working on Precursor Cathode Active Materials, mainly battery-grade iron phosphate and manganese-based materials used in LFP batteries.

Think of it like this. A battery cell company cannot directly jump to making the cathode. There are multiple material-processing steps before that and Sudeep is trying to participate in one of those steps.

Right now, their Customer Qualification Plant is active, samples are going to customers.

Phase 1 is planned at 25,000 MT, with a long-term target of 100,000 MT. If execution stays on track, commissioning is expected around April 2027 and battery-material revenues can start becoming visible from FY28.

In battery chemicals, don't just ask who is building capacity.

Ask where the bottleneck is, because capacity can be copied. The bottleneck usually can't.

And once you find the bottleneck, you start seeing which company may have something others don't.

If you forget the stock price for a moment,

then which side do you believe in more - dry coating or wet coating in cell manufacturing?

Because that one answer may tell you more about you than the stock itself.

If you want something proven and already working, then wet coating, but if you can take some risk and give it a few years, then dry coating.

@brainwaverrr

Yeah, the SBI weight was wrong, that's on me.

But don't look at that number alone. The point I was making was about the impact of weights on the index move.

If that was wrong too, I would have genuinely liked to see the math rather than getting blocked.

That's how we all learn.

Bro, my bad on the exact % – SBI is around 10%, but it moves with price.

Still the point holds: HDFC, ICICI, Axis, Kotak are up good, but SBI is flat + PNB, IndusInd and other heavy ones are red 2-4%. Their drag keeps the index only +16 pts.

Weight game bro, big stocks rule the index move. Not missing much.

Exactly 🙂

That's why I am not looking too much at whether it was bullish, sideways or adjusted later bocz he is specifically pointing to that illiquid PE.

If it was only about the payoff, then combining all legs and looking at expiry would be enough.

But he keeps coming back to that one strike.

So maybe the catch is somewhere there only...

Not necessarily about the direction of the trade, but about how you can get out of the risk when one leg itself is not really tradable.

And as you said, he could have adjusted for sure. So maybe the answer is not in the original position, but in what can be done around it.

Hitachi Energy is down 3.5% today. It's down 8% in the last 5 days. Yet it's still up around 75% in the last 6 months.

So can it go down from here?

Of course it can.

But can it still go up 50% over the next 6–12 months?

Maybe.

Most people will look at the ₹33,265 price and 140+ PE and stop there.

But FY26 revenue was around ₹8,148 crore, while the order book has reached nearly ₹29,555 crore, roughly 3.6x annual revenue.

Now think about the problem India is trying to solve.

The challenge is no longer just generating power. The challenge is moving that power efficiently across the country, integrating renewables, upgrading transmission networks, expanding substations and dealing with transformer shortages.

This is not a one- or two-quarter story. It's a multi-year cycle and that's where the pattern starts showing up.

The biggest winners are often the companies sitting at a bottleneck or choke point that the system cannot easily bypass.

Hitachi sits right in the middle of one of those choke points, that's why I think looking only at the PE misses part of the story.

The market may be valuing not just current earnings, but the role the company could play if this grid upgrade cycle lasts for the next decade.

Now another question comes up.

Is there any other stock like Hitachi?

Yes.

Maybe not at the same scale or position today.

But that's usually how cycles work.

The market finds the obvious winner first, then starts looking for the next company helping solve the same bottleneck.

Hitachi Energy..

They are getting large orders, strong visibility and everything seems aligned with the theme. So it feels like the opportunity is already understood.

But if you look deeper, the role of the company is not that simple. They are not just part of grid expansion, they are solving the problems the grid will face next and that difference changes how you should look at it.

The company is focused on three key areas.

Moving power over long distances through HVDC, managing voltage instability through STATCOM, and controlling the grid through automation.

These are not basic products, these are stress-driven systems.

That is why their position in the value chain is different.

They are present across transmission, power electronics, and control layers together and that is where higher value and better margins usually come from.

Even now, a large part of revenue is still coming from transformers and GIS. That is mid-cycle demand, where execution and earnings are already visible.

But the shift is happening in the order book, a big portion of new orders is now coming from advanced segments like HVDC.

These are long-cycle projects where orders come first and earnings come much later. So visibility is high, but actual performance is still ahead.

Management is also guiding in the same direction.

A lot of these projects will start reflecting properly in earnings around 2027–2028.

Right now, it is still early execution.

So the picture you see today is only partial. Margins have started improving, but the real expansion depends on how this order book gets executed.

That phase has not fully played out yet.

And this is where one question becomes important.

If most of the earnings are still 2–3 years away, what exactly is getting priced today?

Because demand here does not come evenly.

It comes when renewable energy increases, when instability shows up, and when transmission becomes a bottleneck and at that point, spending becomes necessary, not optional.

That is when pricing power changes. Because these systems are not easy to replace, and very few players can deliver them.

This is where margin expansion actually builds.

But even if all of this is correct, timing still decides outcomes. Orders are already visible, but earnings are still catching up and markets usually move in between these two.

So the gap is not in understanding the company.

It is in understanding when this shift shows up in numbers and when the market fully reacts.

That is where positioning actually matters.

And maybe the better way to look at it is this.

Is this a company benefiting from what is visible today…

or from what has not fully shown up yet?

https://t.co/Rd8ofgENd8

Okay, Inox India is up 12% today.

Can it go down from here? Yes, of course.

Can it go up again after that? Of course.

The moment you start understanding the pattern, you'll stop looking at the move and start looking at what is creating the move.

In life and in the stock market, one thing matters a lot — pattern recognition. You see the move, but most of the time you don't see the pattern behind it.

If you look at the energy sector, you can see the same thing in Green H2 as well.

- Over the last month, John Cockerill India moved from around ₹5,200 to ₹9,800, almost 2x. INOX India moved from around ₹1,400 to ₹1,700, roughly 21%.

- That is the signal. Something changed, and the question is what.

- And more importantly, if there is a pattern here, can we apply the same thinking to other parts of the energy sector?

- John Cockerill India is still a steel-processing equipment EPC and technology business. It is not a green steel business yet.

- The big change is the acquisition of John Cockerill Metals International and the consolidation of the group's metals business into the listed entity.

- CY25 revenue was around ₹358 crore. The consolidated order book is already around ₹3,300 crore, while the India order book is around ₹1,321 crore.

- The company also announced a JSW Vijayanagar Metallics order worth around ₹1,250–1,300 crore. That shows how the combined JCIL and JCMI platform can participate in larger projects.

- One thing the market may be looking at is management's increasing focus on green steel, hydrogen steelmaking, EAF and decarbonization.

- At the same time, the parent company already has electrolyzer technology and plans to scale India electrolyzer capacity to 2 GW by 2029.

- Management is also targeting EBITDA margins of more than 10% over the next three years. They believe upstream steelmaking is a much larger opportunity than traditional downstream processing.

- Yet there is no electrolyzer business inside JCIL today. That is where people start looking for the next trigger.

- Maybe the market is already seeing the metals consolidation and the ₹3,300 crore order book. Maybe it is also looking at the possibility of moving closer to green steel and hydrogen steelmaking over time.

- But for the next re-rating, the market will probably want to see something real. Not presentations. Not possibilities. But actual commercial traction.

- Whether that comes through larger green steel orders, upstream steelmaking opportunities or hydrogen-related projects remains to be seen. That is probably what people are waiting for.

Now look at INOX India. INOX India is still primarily an Industrial Gas and LNG business.

- FY26 revenue was around ₹1,632 crore with an order book of around ₹1,514 crore. The current drivers are LNG, aerospace and Cryo Scientific.

- LNG revenue reached around ₹457 crore in FY26. Management believes LNG can grow faster than the standard products business.

- They already have around 60%–65% market share in India but only around 6%–8% globally. That itself shows how much room is still left.

- Management also highlighted a ₹200 crore aerospace order. They expect more orders of a similar nature going forward.

- They also expect strong growth in Cryo Scientific. ITER alone could contribute around ₹50–60 crore annually.

- At the same time, management is increasingly talking about hydrogen infrastructure, liquid hydrogen, energy storage and fusion. Yet most of the revenue still comes from Industrial Gas and LNG.

- Unlike many capital goods stories, INOX already operates with EBITDA margins of around 24%. ROCE is around 37% and the balance sheet remains net cash.

- The stock moved from around ₹1,400 to ₹1,700 in a month, roughly 21%. Again, the signal is visible.

- Maybe the market is already pricing LNG growth and aerospace opportunities. It may also be pricing INOX's position in future hydrogen infrastructure.

- But for the next leg, the market will likely want to see hydrogen infrastructure and Cryo Scientific become a larger part of the business. That is when it starts becoming a real business.

If you think about it, both companies sit on different parts of the same theme. JCIL is closer to the electrolyzer, green steel and hydrogen steelmaking side.

INOX India is closer to the storage and hydrogen infrastructure side. Different parts of the value chain, but connected to the same long-term opportunity.

So maybe the question is not whether Green Hydrogen grows. The question is which layer of the value chain starts showing commercial traction first.

The signal is visible. The drivers are visible.

The market is already showing what it is expecting. The question is what still needs to be proven.

Because the market does not wait for everything to show up in revenue.

First the business changes. Then revenue follows. Then profits follow.

But expectations can change much earlier and many times, that is where the stock moves first.

If you think about it, Green Hydrogen is just one part of the bigger picture.

First comes the grid. Then BESS. Then EVs and cell manufacturing.

Then battery chemicals. Then battery recycling. Then Green Hydrogen.

Then data centers. Then semiconductors. Different themes, but all connected.

The market does not focus on all of them at the same time. It moves from one cycle to the next.

That is why pattern recognition matters.

First comes the signal. Then the driver. Then the expectation gap. Then the trigger.

Sometimes the opportunity appears where the bottleneck is building. Sometimes it appears where the chokepoint is forming.

The market moves from one layer to the next. You just have to understand which cycle it is focusing on right now.

Because if you do not understand which timeline you are looking at, you can be right on the business and still be wrong on the stock.

https://t.co/uztz0ligFY

$Nokia is definitely part of the value chain, but in a slightly different layer than $SIVE or $SOI.

$SIVE and $SOI are closer to specific optical components and materials. Nokia sits further up the stack through optical networking, data center interconnects, IP routing, and AI network infrastructure.

What makes Nokia interesting is the Infinera acquisition. That gave them stronger capabilities in coherent optics, photonic integration, InP-based technology, and data center optical networking.

So when people talk about AI, they usually focus on GPUs. But as clusters become larger, another challenge starts showing up.

How do you move massive amounts of data between GPUs, racks, and data centers without creating bottlenecks?

That's where Nokia starts fitting into the story.

I don't see it as a pure bottleneck play like SIVE or SOI.

I see it more as a company helping build the networking layer that allows those bottlenecks to communicate with each other.

The interesting part for me is that the market still largely remembers Nokia as a telecom company, while more of the growth discussion is starting to revolve around optical networking and AI infrastructure.

If AI and cloud continue becoming a larger share of revenue over the next few years, then the way investors value Nokia could look very different from the way they valued it as a traditional telecom equipment vendor.

I think most people are still looking at AI the wrong way. They see companies like $GOOGL, $META, $MSFT, and $AMZN spending hundreds of billions on AI infrastructure and immediately focus on the hyperscalers.

But the more interesting question is where that money goes after it leaves them. Because that is where the real bottlenecks start showing up.

Goldman now expects the four largest hyperscalers to spend a combined $5.3 trillion between 2025 and 2030. That estimate was revised higher after Q1 earnings.

Even more interesting, total capex between 2026 and 2031 is now expected to reach around $7.6 trillion. That is an enormous amount of money moving through the system.

Now think about what that actually means. Hyperscalers do not keep that money sitting on their balance sheets forever.

The money moves through the supply chain and as it moves, it eventually reaches very small bottlenecks that most investors are not paying attention to today.

That is why companies like $SIVE in CPO lasers and $SOI in silicon photonics substrates become interesting. They sit much lower in the stack where fewer people are looking.

Because when trillions of dollars start flowing through a supply chain, the biggest winners are not always the companies spending the money.

Sometimes they are the companies sitting at the bottlenecks. The ones that become difficult to replace when demand starts accelerating.

And that is the part I think the market is still trying to understand. AI stocks will not move in a straight line, and they never do.

But if this really is the beginning of the next industrial cycle, then the question becomes much more interesting. Which bottlenecks are still being underestimated today?

For me, $SIVE was probably one of the more visible examples recently. The company seems to be showing up across multiple $NVDA NVLink CPO ecosystems and merchant CPO supply chains.

The market has already started rerating it. Which tells you investors are beginning to notice where some of the pressure points are forming.

But that also creates another question. If the market has already discovered one bottleneck, then what is the next one?

Because these cycles usually follow the same pattern. The market finds one constraint, then starts digging underneath it looking for the next layer.

Maybe passive optical components become the next bottleneck. Maybe another part of the optical stack starts becoming the limiting factor.

I do not know yet. But that is where I find myself spending more time looking these days.

The other thing I keep thinking about is the shift from copper to optical technologies. At what point does the conversation start moving toward Micro LEDs?

I saw the recent developments around $MRVL. But honestly, I am more curious about $KOPN and where it fits if this transition plays out.

Most industry discussions still suggest it is too early. If we are talking about large-scale CPO adoption, commercialization probably sits somewhere around H2 2028.

Companies like AMS, MediaTek, and others are still working on solutions. A lot of the technology is still being developed rather than widely deployed.

That is why H1 to H2 2027 feels like a more interesting period to revisit this theme. By then we should have a much clearer picture of what is actually working.

What I find interesting right now is the gap between research reports and media attention. A lot of reports still talk about low readiness levels.

At the same time, media coverage around these technologies keeps getting louder. And whenever I see that kind of gap, I start paying attention.

Sometimes the hype arrives years before reality. But sometimes the market starts spotting a bottleneck before the reports fully catch up.

Couldn't agree more.

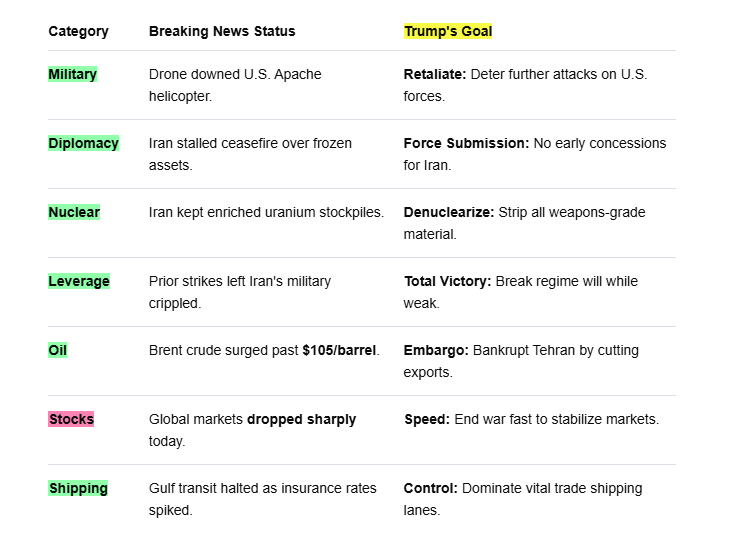

I think one reason people keep getting surprised is that they assume every conflict has one clear objective and one predictable path.

But when you look closely, there are usually many things happening at the same time. Security concerns, military strategy, oil prices, shipping routes, regional influence, domestic politics, economic pressure, and negotiations that most of us never get to see.

That's probably why every new headline seems to completely change the mood. One day people are convinced things are getting worse. The next day they are convinced a deal is around the corner.

And when someone like Trump is involved, it becomes even harder because his approach has often been to keep opponents, allies, and even markets guessing about what comes next.

Maybe that's why I find it difficult to become too optimistic or too pessimistic based on any single update.

The reality is that we can see the events. What we can't see are the discussions, trade-offs, and priorities shaping those events behind closed doors.

Sometimes people become very certain about an outcome when the people making the decisions may still be changing their own plans.

And while everyone is busy trying to predict how it ends, the economic and humanitarian costs keep building in real time.

Agree, but I think the real benefit comes from having surplus cash, not from the OD account itself.

The OD structure is powerful because your money remains accessible while reducing the interest calculation.

But if someone doesn't regularly maintain a meaningful balance in the account, then the advantage can be much smaller than it looks in examples.

Also, many people compare a regular loan and an OD loan without asking a simple question,

Where would that surplus money have gone otherwise?

If it was sitting idle in a savings account, OD can make a lot of sense.

But if that money was never going to sit idle in the first place, then the comparison becomes more interesting.

The interesting part is that OD works best when the alternative is idle cash. Once the alternative becomes a productive asset earning a reasonable return, the decision becomes much more personal and depends on risk, liquidity needs, and financial goals.

I think that's the part many people miss.

The product is useful.

But the question is whether you consistently have excess cash that can actually make the product work.

Look, I’m not saying all this because you need to know everything or track every single thing, that’s not what I’m trying to say.

I’m saying it because whatever decision you take, take it after thinking about it properly.

Don’t just look at what has happened or what is happening right now, think once about what may be coming next in the grid ecosystem.

Because sometimes the answer is not where most people are looking.

Take 4 companies — GE Vernova, Hitachi Energy, Siemens Energy and ABB.

Now see where most of their revenue comes from today and what type of revenue it is.

Then look at what is sitting inside the order book. Is it the same as the current business or does it look different?

Then look at what management is planning for the next few years. Is it the same business you see today or are they preparing for something else?

Then think about what problem or demand management is trying to solve and where in the grid ecosystem it sees the biggest opportunity.

Now connect all of that. What pattern do you see?

What has already been discovered and priced in by the market?

And what may still not be fully discovered or reflected in expectations?

Because sometimes the signal is not in one company, it is hidden in what multiple companies are preparing for at the same time.

Once you see that pattern, you stop looking at the company and start looking at where the demand is going.

Now all you have to understand is where the chokepoint is building and where the bottleneck may appear next.

That's it. There is your next decision.

See, you already know the stock names, the price, the backlog and the orders, but what is missing is clarity on where the demand is building, where the grid can break, and which parts of the ecosystem could matter the most over the next few years.

This PDF can give you that clarity and help you make a better decision.

https://t.co/B13BHvu6kv

@REDBOXINDIA Basically, Trump is using the threat of new strikes to force Iran into a quick deal, but escalating further risks pushing oil prices even higher and destabilizing global markets.

This post contains a PDF on the defence ecosystem value chain. Read it for better clarity and understanding.

https://t.co/QAfE4uFZRu

For example -

- Where exactly does the company sit in the defence and aerospace value chain?

- Is the company's role linked to initial platform induction, or to ongoing upgrades, readiness, and operational continuity?

- What specific operational challenge, threat evolution, or capability gap creates demand for the company's offerings?

- Once this challenge exists, is adoption of the company's solution operationally necessary or operationally optional?

- Who uses the company's products or systems, and who controls their adoption or deployment?

- As warfare complexity increases, does the company's functional importance increase directly, or is its role mediated by larger integrators?

- Can the company's offerings be substituted without redesigning systems, retraining personnel, or altering operational doctrine?

- Is the company's role isolated to a specific platform, or does it extend across multiple platforms and domains?

- At what stage of the defence and aerospace modernisation cycle does the company typically become relevant?

- How does management describe the evolving defence and aerospace ecosystem?

You will find companies like - Astra Microwave, Data Patterns, Avantel, Zen Technologies, C2C Advanced Systems, Solar Industries, Premier Explosives, Bharat Dynamics (BDL), Paras Defence, Apollo Micro Systems & others

Look, many of you have messaged me about defence stocks Astra Microwave, Avantel, Data Patterns, Zen Technologies, C2C Advanced and others.

First thing you need to understand is the cycle.

I can understand many of you have already invested and now prices are not moving as per your expectations or you see other sectors performing better. That is where the confusion starts.

This is exactly why I keep saying understand the cycle first, then think about valuation.

🤔Think where will the actual work happen from 2025 to 2035?

Look at what kind of activity will dominate, how work will be distributed, what components and subsystems will be needed, which segments will drive demand, what is common across systems, and how often replacement or maintenance happens.

Only after this, you will start seeing which part of the ecosystem actually matters. Then you choose companies that fit into that cycle.

Once you understand the cycle, the next step is to test the company against it.

Because answers are already available.

The gap is in asking the right questions.

🤨Where exactly does the company sit in the defence and aerospace value chain?

🤨Is the company linked to initial platform induction… or ongoing upgrades and operational continuity?

🤨What specific threat, capability gap, or operational need creates demand for its products?

🤨Once that need exists, is the solution necessary… or optional?

🤨Who actually uses the product, and who decides its deployment?

🤨Can it be substituted without redesigning systems or retraining personnel?

🤨Is the company tied to one platform… or spread across multiple platforms and domains?

After that, you can think about valuation and margins. That matters, I agree. But before that, choosing the right part of the cycle matters more.

Because in defence, not every company benefits equally. Only those sitting at the right layer of the cycle actually see sustained demand.

Here is the PDF on these defense stocks. Understand the questions first, then look for the answers.

https://t.co/XlAcPPpMjv

You can read this pdf also for better clarity, for example

- Where exactly does the company sit in the defence and aerospace value chain?

- Is the company's role linked to initial platform induction, or to ongoing upgrades, readiness, and operational continuity?

- What specific operational challenge, threat evolution, or capability gap creates demand for the company's offerings?

and others

https://t.co/QAfE4uFZRu

Look, many of you have messaged me about defence stocks Astra Microwave, Avantel, Data Patterns, Zen Technologies, C2C Advanced and others.

First thing you need to understand is the cycle.

I can understand many of you have already invested and now prices are not moving as per your expectations or you see other sectors performing better. That is where the confusion starts.

This is exactly why I keep saying understand the cycle first, then think about valuation.

🤔Think where will the actual work happen from 2025 to 2035?

Look at what kind of activity will dominate, how work will be distributed, what components and subsystems will be needed, which segments will drive demand, what is common across systems, and how often replacement or maintenance happens.

Only after this, you will start seeing which part of the ecosystem actually matters. Then you choose companies that fit into that cycle.

Once you understand the cycle, the next step is to test the company against it.

Because answers are already available.

The gap is in asking the right questions.

🤨Where exactly does the company sit in the defence and aerospace value chain?

🤨Is the company linked to initial platform induction… or ongoing upgrades and operational continuity?

🤨What specific threat, capability gap, or operational need creates demand for its products?

🤨Once that need exists, is the solution necessary… or optional?

🤨Who actually uses the product, and who decides its deployment?

🤨Can it be substituted without redesigning systems or retraining personnel?

🤨Is the company tied to one platform… or spread across multiple platforms and domains?

After that, you can think about valuation and margins. That matters, I agree. But before that, choosing the right part of the cycle matters more.

Because in defence, not every company benefits equally. Only those sitting at the right layer of the cycle actually see sustained demand.

Here is the PDF on these defense stocks. Understand the questions first, then look for the answers.

https://t.co/XlAcPPpMjv

Yes, it's 5 years from 2021 to 2026 now. Back then, after COVID, these stocks traded at crazy highs like 100-250x earnings due to too much hype.

Today: Route Mobile 10-14x, IRCTC 28-30x, IndiaMart 25x, IEX 22x, Happiest Minds 24-25x. Many are down a lot over 5 years.

Market doesn't care what we want. It prices real growth, risks and future earnings. 2021 was peak excitement. Now it's normal after the cycle.

Simple lesson: Buy at fair prices, not dream prices. Cycles always change.