Forensic Analysis: SEC Filings & Tape,Decoding Options, Short data & Macro for Asymmetric plays. Learning one deep-dive at a time. Not Financial Advice

$HPE - Friday movement. It is not just because of DELL sympathy.. the fundamental backdrop kept the bids firm ahead of the mi day earnings :

Activists & Insiders: Elliott Management's newly expanded 27.4M share stake continues to fuel structural optimization hopes.

Balance Sheet De-leveraging: $HPE disclosed the monetization of its H3C stake for roughly $987M, giving them clean capital to pay down debt post-Juniper.

$HPE -Can it hit $50 after hours on Monday ?

If HPE drops a true beat after the close (EPS well above the $0.55 whisper, an expansion of the $5B AI backlog, and a major upward revision to full-year FY26 guidance), the 10.6% post-market implied volatility will unlock. A 12% to 15% gap up from a $44 baseline in late-theater trading is exactly where a squeeze to $50 would happen

$CRCL

-Speculation only.. bullish, specifically anticipating a high probability of a short squeeze that pushes the stock into the $130.00 to $134.00 range, or potentially higher. Here is the data-driven rationale for this bullish lean: 1-The CLARITY Act is a Massive De-Risking Event: The recent bipartisan compromise on the CLARITY Act explicitly protects the transaction-based rewards that Circle relies on for its business model. This fundamentally removes the existential regulatory overhang that was depressing the stock, paving the way for institutional adoption. 2-The "Powder Keg" Short Setup: Short sellers have aggressively targeted the stock due to fears of margin contraction, with short interest jumping 22.4% recently to cover 12.2% of the float. Even more telling, the daily short volume ratio surged to a staggering 48.11% of all trading volume just days before the earnings blackout. If Circle reports even mildly positive forward guidance regarding their high-margin software services, these short sellers will be forced to rapidly buy back shares to cover their positions, creating a violent upward price spike. 3-Historical Precedent: Circle has a history of massive post-earnings rallies. Following their last earnings report in February, the stock surged 35.5% in a single day after beating EPS estimates. While the high valuation and recent insider selling (which was largely pre-scheduled via 10b5-1 plans) provide ammunition for the bears, the structural setup in the options market and the heavily squeezed float suggest the path of least resistance is a violent move upward. If management executes a strong earnings call, expect the stock to hit the top of the options market's 15% expected move (around $130) and potentially challenge Wells Fargo's recent $142.00 price target.

$SHAZ- The $SHAZ "Sovereign AI" Inflection: A $1.25B Masterclass

1/ The Catalyst: SharonAI ($SHAZ) just dropped a nuclear-grade 8-K. A 5-year, $1.25 Billion Master Infrastructure Agreement with ESDS Software Solutions.

The Scale: For a ~$445M market cap company, this is a TCV-to-Cap ratio of 2.8x.

The Math: Amortized over 60 months, that’s ~$250M/year in high-margin recurring revenue.

2/ The Hardware Moat: This isn't a "pilot" program. It’s a deployment of 8,200 NVIDIA B300 (Blackwell Ultra) GPUs. The Performance: 14 PFLOPS dense FP4 compute 55% faster than the B200.

The Infrastructure: 1,400W TDP per GPU requires Direct Liquid Cooling (DLC).

The Edge: $SHAZ has 70MW of Tier IV capacity secured at @NEXTDC M3 in Melbourne. In a power-constrained world, Capacity = Alpha.

3/ Counterparty De-Risking: The bear case today was skepticism over ESDS’s ability to pay. The 8-K silenced this with cold data:

Security: ESDS is mandated to provide $140M in Letters of Credit/Bank Guarantees.

Lock-in: No "Termination for Convenience" in the first 36 months. This isn't "hope"; it's a collateralized asset.

4/ Financial Engineering: $SHAZ is scaling without the "Death Spiral" dilution common in tech micro-caps.

https://t.co/vvcMQcFgRS Facility: A $500M non-recourse, asset-backed debt engine.

The Tech: Financing via stablecoin liquidity against verified GPU hardware.

The Result: Massive scaling of the "AI Factory" while keeping the float tight (~10.8M share float).

5/ The Tape (The "Gap & Crap" Recovery): Today was a textbook technical shakeout.

The Open: Gapped to $25.80.

The Trap: Flushed to an intraday low of $22.54 to shake out "paper hands."

The Absorption: Heavy institutional accumulation drove a recovery to close at $27.62 (+21.5%).

6/ Valuation Framework: If $SHAZ executes on a $275M-$300M revenue run-rate:

Peer Multiples: Neocloud peers (CoreWeave/Lambda) trade at 8x-12x Revenue.

Conservative 6x Multiple: Implies a $1.8B Market Cap.

Target: With current share structure, "Fair Value" sits north of $75.00 as the market prices in the backlog.

7/ The Verdict: We are witnessing an Episodic Pivot (A+ Catalyst). Today was Day 1 of the structural re-rating. Once the market reclaims the $30.00 IPO price, we enter "Blue Sky" territory.

$RZLV -$RZLV 20-F ALERT: The "Audit" is In – Hypergrowth Validated-https://t.co/LET7KeXPdk wait is over. Rezolve AI has officially filed its Form 20-F Annual Report with the SEC. If you were looking for the "Green Light" that separates speculative AI rumors from production-grade reality, this is it. -The "Triple Crown" Metrics The 543% Growth Flip: 2025 revenue hit $46.8M, but the real story is the H2 acceleration. Revenue skyrocketed 543% in the second half vs. the first half as major deployments went live. The "Floor" is Set: The company exited the year with $19.4M in December MRR, establishing a $232M+ Annualized Run Rate (ARR). This provides a massive, high-conviction foundation for their raised $360M revenue guidance for 2026. Software-Elite Margins: Blended gross margins are at 66%, but the core software component is performing at 90%+. This is the structural profitability "Whales" look for in the SaaS/AI sector. -The "Fully Funded" Mandate The biggest "short" thesis on small-cap AI is always dilution. The 20-F just killed that narrative. Cash Position: $111.1M as of year-end. Capital Fortress: With over $750M in total funding secured (including the oversubscribed Jan raise), the Company explicitly stated they have "zero requirement for additional operational equity" to execute their 2026 mission. -Strategic Edge: Agentic Commerce This isn't just "Search." Rezolve has processed 112.7 billion API calls across 950+ enterprise customers. They are moving from the "Experimentation Phase" into Live Infrastructure. 📉 The Technical Setup (Tuesday Morning) The Gap: The stock is already showing relative strength, drifting green overnight as the "Compliance Risk" of the missing 20-F is removed. T Bottom Line: The 20-F proves the "Hockey Stick" is real. $RZLV is no longer a concept it’s an infrastructure leader trading at a massive discount to its Forward ARR. #RZLV #AI #AgenticCommerce #Squeeze #StockMarket

$RZLV -$RZLV 20-F ALERT: The "Audit" is In – Hypergrowth Validated-https://t.co/LET7KeXPdk wait is over. Rezolve AI has officially filed its Form 20-F Annual Report with the SEC. If you were looking for the "Green Light" that separates speculative AI rumors from production-grade reality, this is it. -The "Triple Crown" Metrics The 543% Growth Flip: 2025 revenue hit $46.8M, but the real story is the H2 acceleration. Revenue skyrocketed 543% in the second half vs. the first half as major deployments went live. The "Floor" is Set: The company exited the year with $19.4M in December MRR, establishing a $232M+ Annualized Run Rate (ARR). This provides a massive, high-conviction foundation for their raised $360M revenue guidance for 2026. Software-Elite Margins: Blended gross margins are at 66%, but the core software component is performing at 90%+. This is the structural profitability "Whales" look for in the SaaS/AI sector. -The "Fully Funded" Mandate The biggest "short" thesis on small-cap AI is always dilution. The 20-F just killed that narrative. Cash Position: $111.1M as of year-end. Capital Fortress: With over $750M in total funding secured (including the oversubscribed Jan raise), the Company explicitly stated they have "zero requirement for additional operational equity" to execute their 2026 mission. -Strategic Edge: Agentic Commerce This isn't just "Search." Rezolve has processed 112.7 billion API calls across 950+ enterprise customers. They are moving from the "Experimentation Phase" into Live Infrastructure. 📉 The Technical Setup (Tuesday Morning) The Gap: The stock is already showing relative strength, drifting green overnight as the "Compliance Risk" of the missing 20-F is removed. T Bottom Line: The 20-F proves the "Hockey Stick" is real. $RZLV is no longer a concept it’s an infrastructure leader trading at a massive discount to its Forward ARR. #RZLV #AI #AgenticCommerce #Squeeze #StockMarket

$RZLV -The $RZLV numbers this morning are essentially a masterclass in AI scaling. While the "Tape" is playing tug-of-war at the $2.60 level, the fundamental re-rating is hard to ignore: 🔹 The Growth: 543% H2 revenue surge vs. H1. 🔹 The Guide: 2026 revenue raised to $360M (well above previous $310M estimates). 🔹 The Floor: Exited 2025 with $232M in contracted ARR. That's a massive safety net for a ~$1B market cap. 🔹 The Cash: $750M+ total funding. The "dilution" bear case is officially dead. Why the stagnation? Look at the data: Shorts borrowed 2.5M+ shares today alone to hold this back, and there's a massive Call Wall at $3.00. The Setup: Historically, $RZLV is a "Day 2" mover (Avg +15% continuation). If this clears the $2.89 HOD, the shorts are trapped with near-zero availability to borrow more. Watching the 20-F filing today as the final "green light" for the Whales. 🐳 #AI #Stocks #Trading #RZLV $RZLV

$IBRX 48-Hour Forensic Update: The "Quiet" Battle for the Floor. It has been two days since the FDA Warning Letter triggered a -21% shock. While the narrative has been dominated by "Management Risk," the actual data from the last 48 hours tells a story of aggressive institutional defense and clinical validation.

1. The Clinical Counter-Punch (March 26)

While management is effectively "benched" from making promotional claims, they just dropped a massive clinical update this morning.

QUILT-2.005 Milestone: The Independent Data Monitoring Committee (IDMC) confirmed the pivotal trial for BCG-Naïve patients (first-line) is adequately powered to show statistical significance.

Why this matters: This isn't the "failed" monotherapy cohort. This is the primary expansion market. A supplemental BLA (sBLA) for this multi-billion dollar indication is now officially on track for Q4 2026. This effectively separates the "marketing noise" from the "clinical signal."

2. Technical Resilience: The $7.20 Floor

The "Flush" Reversal: On March 24, the stock hit a terrifying low of $6.54.

The Recovery: Since that low, the stock has battled back to hold the $7.30–$8.00 range. Today (March 26), it even tested $8.43 before the shorts attempted to cap it.

Volume Analysis: After the 86M share "liquidation" on Tuesday, volume has normalized, suggesting that the "Panic Sellers" have been flushed out and replaced by "Whale" accumulation.

3. Market Microstructure: The Short Squeeze Setup

The "Silence Trap" we anticipated is backfiring on the shorts:

Utilization remains at 100%: There is zero "legal" inventory left to borrow.

Cost to Borrow (CTB): Has surged to 17% today. Shorts are paying a heavy premium to bet against a company that just confirmed its trial is powered for success.

Put-Call Ratio: The 1.32 ratio for the March 27 weekly expiration shows high bearish positioning the exact fuel needed for a "gamma squeeze" if the stock reclaims $8.50.

4. Regulatory Reality Check

SEC EDGAR Audit: Still no 8-K responding to the FDA or new equity offerings. Management is following the 15-day compliance window to the letter.

The May 8 "Ace": The market is waiting for the sBLA Acceptance for the Papillary indication. If that drops during this high-CTB/Low-inventory environment, the recovery to $10.00+ could be instantaneous.

Final Verdict

The "Management Silence" is a legal requirement, not a sign of failure. The clinical data (QUILT-2.005) is the true north. We are currently watching the shorts pay 17% interest to defend a "marketing" headline while the clinical value continues to compound.

Capital preservation was the play on Tuesday. Strategic observation is the play today.

#IBRX #ANKTIVA #BiotechIntel #StockMarket

$DNLI-AVLAYAH is widely considered the most significant biotech catalyst of 2026:

1. It Solves the "Holy Grail" of Biology

For 30 years, the biggest "graveyard" in medicine has been the Blood-Brain Barrier (BBB). Thousands of drugs have failed because they simply couldn't get into the brain.

• The Significance: AVLAYAH is the first-ever medicine to use a "Transport Vehicle" (TV) to trick the brain into letting it pass.

• The Impact: By approving this, the FDA didn't just approve one drug; they validated a delivery platform that can now be used for Alzheimer’s, Parkinson’s, and ALS. This is the "Intel Inside" moment for brain medicine.

2. The "Competitive Vacuum"

In February 2026, the FDA rejected REGENXBIO’s gene therapy for Hunter syndrome.

• The Reality: That rejection left the entire market wide open. Denali now has a monopoly on treating the neurological symptoms of this disease. In the world of rare diseases (Orphan Drugs), a monopoly usually leads to massive, high-margin revenue and a multi-billion dollar valuation "re-rating."

3. The "Royalty Pharma" Stamp of Approval

Royalty Pharma (the "Whale of Whales" in biotech funding) didn't just bet on Denali they put $275 million on the line specifically for this approval.

• The Significance: These guys are the smartest math-minds in the sector. They don't gamble. Their $275M investment was a "pre-approval" bet that the TV platform was worth billions.

$DNLI- WHY WAS IT REMOVED? (THE "GHOST" LISTING)

1.Administrative "Fat Finger" or Early Sync: The FDA’s digital databases (Drugs@FDA, Orange Book, etc.) often sync data from internal review servers to public servers in "batches." It is highly common for a drug to be populated onto the public site hours or even days before the official announcement, and then pulled down once the agency realizes the public has spotted it before the formal 8-K filing or press release.

2.Staging for the News: This is a strong signal that the Approval Letter has likely been signed, and the FDA web team was simply "staging" the page. The removal is a "clean-up" to ensure the official announcement follows the proper regulatory protocol.

3.Historical Precedent: We saw this exact behavior with several high-profile approvals (e.g., Biogen’s Leqembi). The "leak" through the database leads to a pre-market spike, the removal causes a temporary "dip" of uncertainty, and the official press release finally triggers the real squeeze.

$DNLI- $DNLI: Technical & Regulatory Synthesis — April 5 PDUFA

As Denali Therapeutics approaches the FDA decision for tividenofusp alfa (DNL310), the equity exhibits a rare convergence of institutional accumulation and mechanical supply constraints.

1. Institutional Activity at Current Levels Level 2 tape captured a ~237k share print (~$5M+) at $20.97 during the March 24 session suggesting meaningful institutional participation at this price zone ahead of the catalyst window.

2. Clinical De-risking Phase 1/2 data demonstrated a 91% reduction in CSF heparan sulfate the key CNS biomarker of disease published in the NEJM. CMC review is complete, materially reducing the probability of a technical rejection.

3. Mechanical Gamma Trap The April 17 option chain shows concentrated Open Interest at the $22.50 strike (832 contracts). A sustained move through $22.50 triggers a Gamma Flip forcing market makers into a pro-cyclical delta-hedging cycle that mechanically accelerates price discovery higher.

4. Liquidity Bottleneck 9.63 Days to Cover. NYSE closed Good Friday April 3. Short sellers have a compressed 7-trading-day window to de-risk ahead of the binary. This creates a structural time-decay trap for the bearish thesis.

5. Platform Optionality 3,050 June $30 calls represent the largest single OI block in the entire chain. The market isn't just pricing tividenofusp alfa — it's beginning to re-rate Denali's broader Blood-Brain Barrier Transport Vehicle platform across Sanfilippo, Pompe, and Alzheimer's programs.

6. The Terminal Exit Risk/reward remains optimal for a Pre-PDUFA Drift strategy. The terminal liquidity point is Thursday April 2. The path of least resistance points toward the 52-week high of $23.77 and the secondary liquidity zone of $25.00.

Not financial advice. Do your own work.

$966M cash. Breakthrough Therapy designation. No AdCom. Cleared competition.

Clock is ticking. ⏱️

#DNLI #Biotech #MarketMechanics #InstitutionalFlow

$IBRX- Tough end of day report - March 24th 2026. Part of investing.

$IBRX Forensic Recap: March 24, 2026

Today was a masterclass in how regulatory news collides with extreme market microstructure. The long-term Anktiva thesis hasn't changed but today's -21% crash was driven by a specific information shock.

---

1/ THE CATALYST: FDA Warning Letter

FDA Warning Letter MARCS-CMS 725468 was issued March 13 but not publicly disclosed until the FDA posted it on their website today, March 24. During that window, the company announced major wins the NCCN Guideline update (Mar 17) and Macau Approval (Mar 20).

IMPORTANT: Companies are not always required to file an 8-K for warning letters materiality is a judgment call. We are not alleging deliberate concealment. What we are saying is the timing created an information asymmetry that the market repriced violently today.

---

2/ THE "SLAP"

The FDA cited "false or misleading" claims in:

• A direct-to-consumer TV ad featuring CEO Adcock & Dr. Soon-Shiong

• A Jan 19 podcast on The Sean Spicer Show

Key violations:

• Implied Anktiva could "treat all cancers"

• Described it as a "cancer vaccine" not an approved label

• Showed arm injections (it's delivered intravesically into the bladder)

• Zero risk disclosures in the podcast

This is their THIRD FDA enforcement action in 6 months. That pattern matters.

---

3/ STATUS

This is a marketing/compliance issue NOT a clinical one.Anktiva's 700% revenue growth is real. The FDA is not questioning the science or the approval. They're questioning how management is talking about it publicly.

The company has 15 *working* days to respond (~April 15). Expect relative quiet from management during this period as they coordinate their response.

---

4/ PRICE ACTION

• Open: $9.07

• Intraday low: $6.54 (-30% peak-to-trough)

• Close: ~$7.42 (showed real resilience off lows)

• Volume: ~86.9M shares roughly 4x avg daily volume

That closing bounce matters. It suggests some buyers stepped in at the lows. But the structure is damaged short-term.

---

5/ SHORT INTEREST & THE SILENCE TRAP

Short interest remains ~35.41% of float (~132M+ shares short). Borrow utilization is pinned near 100%.

With management now in a regulatory response period (~15 working days), expect a relative news vacuum. Shorts will likely use this silence to test the $6.00–$6.50 support zone.

Note: High "Short Exempt" volume seen today reflects legal market-maker exemptions to the uptick rule NOT naked short selling. Important distinction.

---

6/ THE BOTTOM LINE

The science hasn't changed.

The revenue trajectory hasn't changed.

But management credibility has taken a hit both from the content of the letter AND the timing of its disclosure.

We are now in a high-volatility "wait and see" period.

Two catalysts that can reset the narrative:

📍 ~April 20 — Saudi Arabia commercial launch

📍 ~May 8 — FDA sBLA filing decision (papillary bladder cancer)

Not financial advice. Do your own due diligence.

Patience and capital preservation are the only plays here.

#IBRX #ANKTIVA #TradingIntel #Biotech

$IBRX- $IBRX INTEL: MARKETING VS. MEDICINE ($6.54 SHAKEOUT)

The market just underwent a -30% "liquidity raid" based on a headline that requires a deep forensic read. If you sold the $6.54 bottom, you traded on fear. If you bought the $7.50+ recovery, you traded on data.

1. THE "SLAP": AD COPY, NOT CLINICALS

The FDA Warning Letter is a marketing compliance issue. The FDA’s OPDP office is penalizing PSS for aggressive podcast/TV ad claims.

Crucial: This is NOT a product recall. The drug’s safety, efficacy, and current FDA approval for bladder cancer remain 100% intact.

2. THE $6.54 LIQUIDITY VACUUM

We saw a complete failure of the $9.30 floor as stop-losses were hunted down to a flash-crash low of $6.54.

The Read: The gap between $6.54 and the 7.50 recovery was fueled by institutional "Whales" recognizing a sentiment overreaction. They filled their bags while retail panicked over a marketing dispute.

3. THE SEPARATION OF CHURCH & STATE

The FDA office reviewing the Papillary sBLA (Day 15 window) is separate from the office policing TV ads. A "Marketing Warning" does not legally stop a "Clinical Filing Acceptance."

THE BOTTOM LINE: PSS pushed the envelope on marketing and got a public slap on the wrist.

Status: V-Recovery in Progress. Support: $7.50.

#IBRX #ANKTIVA #TradingIntel #Biotech

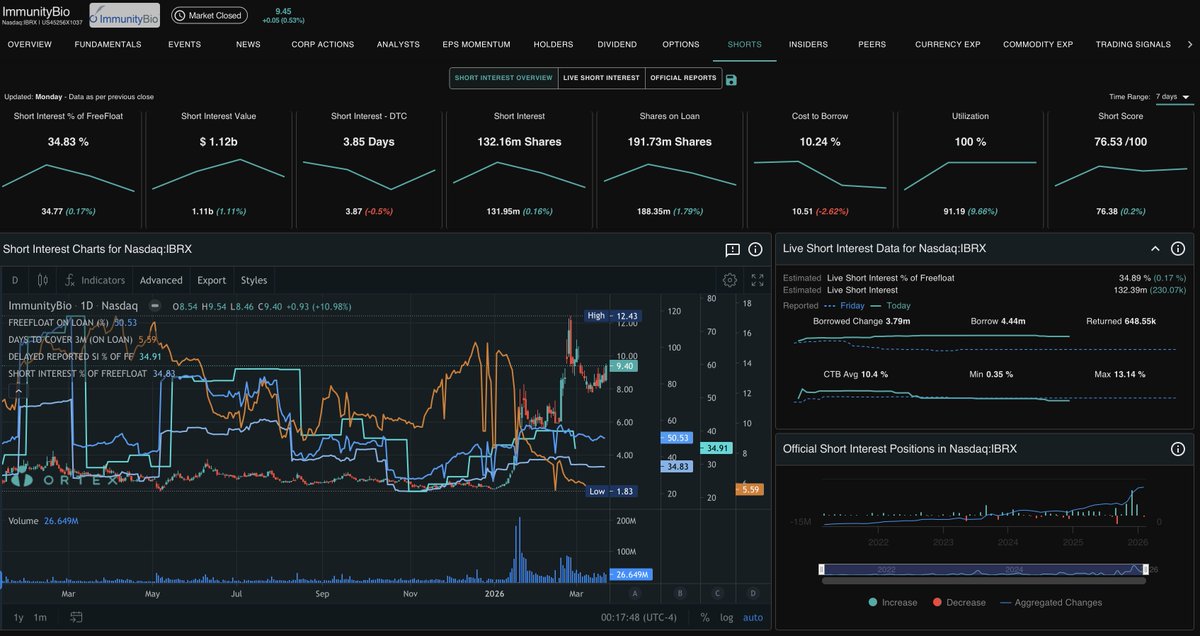

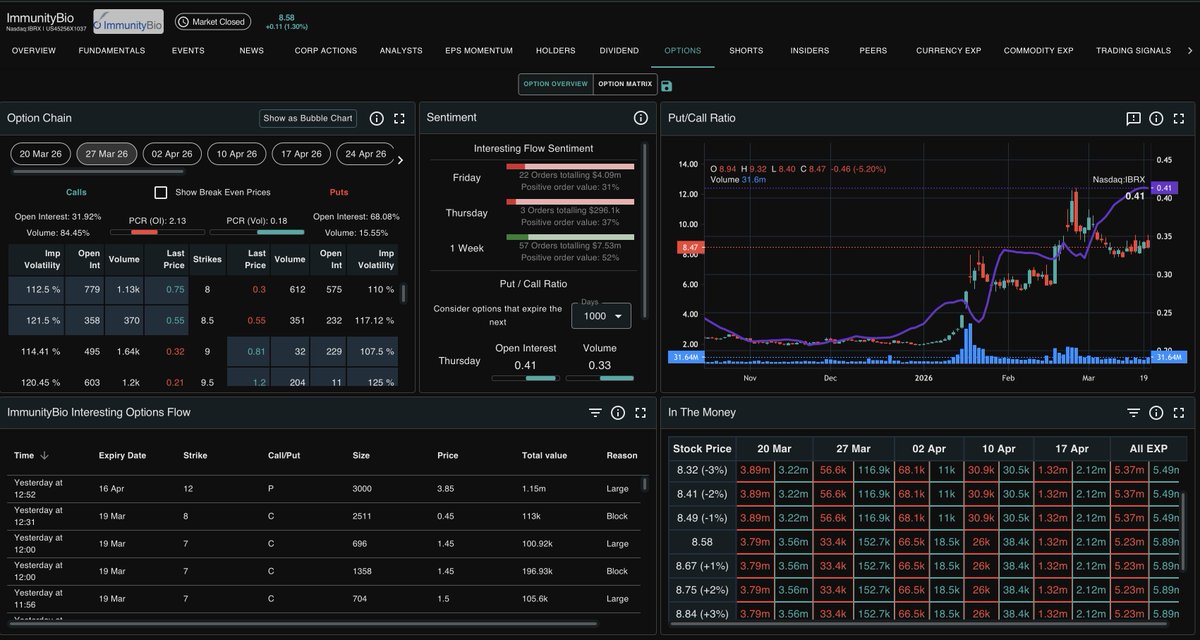

$IBRX- $IBRX Short INTELLIGENCE REPORT: MARCH 23, 2026. As always data attached ( short interest data)

Today was not just a green day; it was a structural shift in $IBRX market mechanics. The "Short Trap" has moved from theory to reality.

1. THE TAPE: BREAKOUT & ABSORPTION

The Breach: $IBRX decisively cleared the $9.30 resistance, hitting an intraday high of $9.54.

The Whale Signature: A massive 695,962-share block hit at the $9.40 close ($6.5M+). This signals institutional "buy-in," not retail flipping.

Volume: 26.7M shares extreme conviction fueled by a "Wall of Analysts" (BTIG $13 target / D. Boral $23 target).

2. MECHANICAL FAILURE: SHORT EXHAUSTION

Utilization: Pinned at 100%. There is zero remaining "legal" inventory to borrow.

Inventory Crisis: IBKR availability dropped to a staggering 200 shares tonight. Shorts are out of ammo to defend the $10.00 magnet.

Borrow Fees: Averaging 11.25% (Max 13.14%). Shorts are paying predatory interest to stay underwater.

3. THE CATALYST CLOCK

FDA Window: Today is Day 14 since the sBLA resubmission. The market is betting on a Class 1 (60-day) designation, moving the finish line to May.

THE BOTTOM LINE: We closed at $9.40 (+11%) on massive volume. $9.30 is now the floor. With zero borrow and a Gamma Trap set, the path of least resistance is UP.

#IBRX #ANKTIVA #ShortSqueeze #Biotech

$IBRX- Marc 23rd UPDATE: THE $9.30 BATTLE IS HERE

$IBRX Family, listen up. We are at a structural "Breaking Point" today. While the broader market is distracted, the tape is revealing a massive tug-of-war for the soul of this stock.

The Situation: Shorts are Cornered

This morning, $IBRX gapped up and touched $9.38, officially blowing past Friday’s "options pin." Since then, we have seen aggressive "Short-Exempt" selling hitting the bid to keep us under the $9.30 mark.

Why are they so desperate?

100% Utilization: There are officially ZERO shares left to borrow (Ortex confirms only ~15k available). They are literally recycling the same "ghost shares" to suppress the price.

The $9.32 Wall: This was Friday's manipulation high. Breaking and holding above this level triggers a massive wave of mechanical stop-losses for the shorts.

The Catalyst: The "Wall of Analysts"

BTIG: Initiated with a BUY ($13 Target) this morning.

D. Boral (Jason Kolbert): Reaffirmed his $23.00 Target today.

The Message: The "Smart Money" is pricing this for a $10B+ valuation while the shorts are fighting over pennies at $9.15.

The Game Plan

The shorts are "leaning" on the $9.17–$9.30 wall. They are hoping you get bored and sell. Don't.

Watch $9.00: This has become a massive institutional support floor.

Watch the Break: If we clear $9.40 on high volume this afternoon, the "Squeeze" moves from a theory to a reality.

Bottom Line: We have the science, the revenue (Saudi/Macau), and the analyst upgrades. The shorts only have a 14,000-share wall at $9.17. That wall is made of paper.

Patience is the only thing they can’t beat.

#IBRX #ANKTIVA #ShortSqueeze

$IBRX- $IBRX Forensic Catalyst Calendar: March 22–28

As always not financial advise .. but presenting facts based on publicly available data.

1/ Sunday–Tuesday (March 22–24): The ROTH Conference 🎤

The Event: 38th Annual ROTH Conference in Dana Point, CA.

The Data: ImmunityBio management is confirmed to participate in 1-on-1 institutional meetings and a presentation.

The Analysis: This is the first time management will speak publicly since the Macau approval (Friday) and the NCCN Guideline expansion (Tuesday). Watch for updates on international launch timelines and the sBLA review status. Institutional "Smart Money" often accumulates following these private fireside chats.

2/ Monday (March 23): The "Pin Release" & Gap-Up Potential

The Mechanical Event: First trading day following the March monthly options expiration.

The Analysis: On Friday, the stock was pinned at $8.47 to save Market Makers from delivering 3M+ shares for the $9.00 calls. That financial incentive is now zero. Without the artificial "Operational Shorting" pressure, $IBRX is free to react to the Macau Asia-entry news.

Watch Level: A break of $9.32 (Friday's high) would signal a complete shift in control from shorts to bulls.

3/ Tuesday–Thursday (March 24–26): The "Saudi 30-Day" Window 🇸🇦

The Commercial Event: Mid-point of the 60-day launch window established on February 20, 2026.

The Analysis: We are officially entering the "Pre-Launch" phase for Saudi Arabia.

The Catalyst: Any news regarding the first shipment of ANKTIVA to Cigalah Healthcare or the registration of the first KSA patient would be a massive "Proof of Concept" for international revenue. Remember: Saudi is the only place approved for Lung Cancer (NSCLC) right now a market much larger than bladder cancer.

4/ All Week: FDA sBLA Acceptance Notification.The Regulatory Event: The 14–30 day window for the FDA to formally "Accept for Filing" the papillary-only sBLA resubmitted on March 9, 2026.

The Analysis: The FDA has already acknowledged receipt. A formal "Acceptance" PR next week would include the PDUFA date (the final decision deadline). This is a massive de-risking event that shorts are dreading.

5/ All Week: The NCCN "Silent Revenue" Build 🩺

The Guideline Event: First full week of clinical availability under the March 17 NCCN update.

The Analysis: Urologists across the US now have the green light (Category 2A) to prescribe ANKTIVA for papillary-only patients with high-confidence insurance reimbursement. This is "off-label" revenue starting immediately, effectively tripling the drug's US market size before the FDA even finishes its review.

Summary for Next Week:

The Situation: Shorts doubled down on Friday to pin the price, but they are now facing a week with zero options protection and four massive fundamental catalysts.

Monday is a new game. The Asia gateway is open, the Saudi launch is weeks away, and the US market just tripled in size. Data > Emotion. 🚀🚀

#IBRX #ANKTIVA #ShortSqueeze #BiotechInvesting #DrPSS #SaudiArabia

$IBRX- $IBRX Short Intelligence report- March 21st . Data attached. $IBRX is currently one of the most structurally over-leveraged shorts in the entire market.

1/ Numbers don’t lie, but they do tell a story. While we were all distracted by the Friday "pin" at $8.47, the short data was recording a catastrophic structural trap. Here is the forensic deep-dive into the current $IBRX Short Interest. #IBRX #ShortSqueeze #Ortex

2/ The "Supply Lock" (Utilization: 100%) -The Ortex data confirms we are at 100% Utilization.

What it means: Every single share available to be lent out has already been borrowed.

The Reality: There is zero legal borrow left. Any "selling" we saw at the $9.30 wall on Friday was almost certainly "Operational Shorting" (IOUs) by Market Makers. They are digging a hole they can't fill.

3/ The Magnitude: 132 Million Shares Trapped

Estimated Short Interest: 132.32 Million shares.

% of Freefloat on Loan: A massive 51.22%.

Short % of Freefloat: 34.87%.

Comparison: Anything over 20% is a powder keg. At 51% of the float on loan, $IBRX is currently one of the most structurally over-leveraged shorts in the entire market.

4/ Days to Cover (DTC): The "Week-Long Stampede"

DTC: 3.84 to 5.64 days (based on 3-month volume).

Translation: If every short seller tried to exit on Monday, it would take nearly 6 full days of 100% of the trading volume just to close their positions. There is no "Emergency Exit." In a squeeze, it becomes a literal stampede.

5/ Cost to Borrow (CTB) & Availability

CTB Average: 10.64%.

Availability: Interactive Brokers (IBKR) shows only 650k shares available at an 8.16% rate.

This is the "calm before the storm." With 100% utilization, the moment the price crosses $9.15, the CTB is mathematically primed to explode as lenders recall shares.

6/ The Verdict: The Friday "Pin" was a desperate defensive move. The shorts spent millions on Friday to force an $8.47 close and kill the $9.00 calls. But look at the Ortex charts—they didn't cover. They doubled down.

They are now "Naked" against: ✅ Macau/Asia Approval (New Revenue) ✅ NCI Science Validation (Govt Backing) ✅ 100% Supply Lock (No Exit)

The spring is coiled. The exit is blocked. Monday is a new game.

#ImmunityBio #ANKTIVA #ShortSqueeze #TradingData #Fintel

$IBRX- Another tough day on Friday ( March 20th). Second time in a week we tried to breach $9.30.. but could not hold on. Begs the question why.?. Here is a data driven explanation:

$IBRX Forensic Audit – The Friday "Pin" Exposed

1/ The "Friday Flush" wasn't a sell-off. It was a surgical strike. If you’re shaken by $IBRX dropping from $9.32 to $8.47, you’re looking at the wrong data. We have spent the morning digging through various platforms to understand the underlying data. Here is the "Smoking Gun" evidence of what really happened. #IBRX #ShortSqueeze

2/ The $9.00 "Call Wall" . There were 27,672 Call contracts sitting at the $9.00 strike for Friday's expiration.

The Math: If $IBRX closed at $9.01, Market Makers (MMs) would have been forced to buy/deliver 2.76 Million shares.

The Conclusion: Dropping the price to $8.47 saved the MMs millions. This wasn't a lack of buyers; it was a "Pin" to protect the house.

3/ Visible Manipulation. The Heatmap doesn't lie. Every time we touched $9.32, a massive "Orange Wall" appeared.

The 885K Block: Data confirms MMs dumped 885,000 shares at $9.26.

At 100% Utilization, these aren't real shares being sold—this is "Operational Shorting" used as a fire extinguisher to put out a fundamental rally.

4/ The Inst.itutional Floor. While retail was "shook" by the red candles,Thick bands of liquidity (buying) held the $8.40 - $8.50 line all afternoon.

Hidden Accumulation: While MMs were flushing the price to kill the options, "Whales" were sitting at the bid, vacuuming up every share being dumped.

5/ The "Bear" Trap .Don't be fooled by technical models calling for "Zero Probability" of upside.

The Flaw: Models using RSI and CMF are Lagging Indicators. They tell you what happened yesterday.

The Reality: They cannot calculate for Macau FDA Approval or NCI Science Validation. The news was suppressed by the options pin. The move is DELAYED, not canceled.

6/ The Verdict .We are looking at the literal friction between a company moving toward its true value and a financial system trying to settle its debts.

Short Interest: 132M+ shares.

Utilization: 100%.

Catalysts: Global.

The $9.00 "Options Anchor" is now gone. Monday is a new game. Data > Emotion.

#ImmunityBio #ANKTIVA #Biotech #ShortSqueeze