TA - @iitrpr & @iitm_bs | Charpak Lab Fellow'24 @psl_univ 🇫🇷 | MitacsGRI'23 @UMontreal 🇨🇦 | Siemens Scholar'24 | Data Science Major with Minor in Economics

Jane Street made $4.3 billion with a single strategy in India, it worked so well that regulators launched an investigation

it only got exposed because Jane Street sued their own employees and accidentally leaked the strategy

India's options market is 422 times larger than its stock market

every morning they bought $500 million in stocks

once puts were cheap enough they loaded up, sold all their stocks in the afternoon

$85 million in a single day, they ran this for two years straight, regulators ordered $570 million forfeited

Bookmark & Watch the full story today ↓

ever been here?

open overleaf → write a paragraph → "hmm...this needs a citation" → open 15 different tabs → skim 8 abstracts → find the 1 actually relevant paper → format bibtex → paste it back on overleaf

if so, i built a plugin just for you. meet openleaf:

→ reads your paper paragraph by paragraph

→ searches major academic databases

→ filters out irrelevant papers using ai

→ one click to add BibTeX to your .bib

you'll also find the 🤝 friendly and 🔥 fire reviewers there. i don't think i need to tell you what they do :)

free. open source. no account. no data collection.

works with ollama, openrouter, openai api and more.

https://t.co/XvX03iem38

dear algorithm, please show this to my fellow researchers in need 🙏

#overleaf #latex #opensource #academictwitter

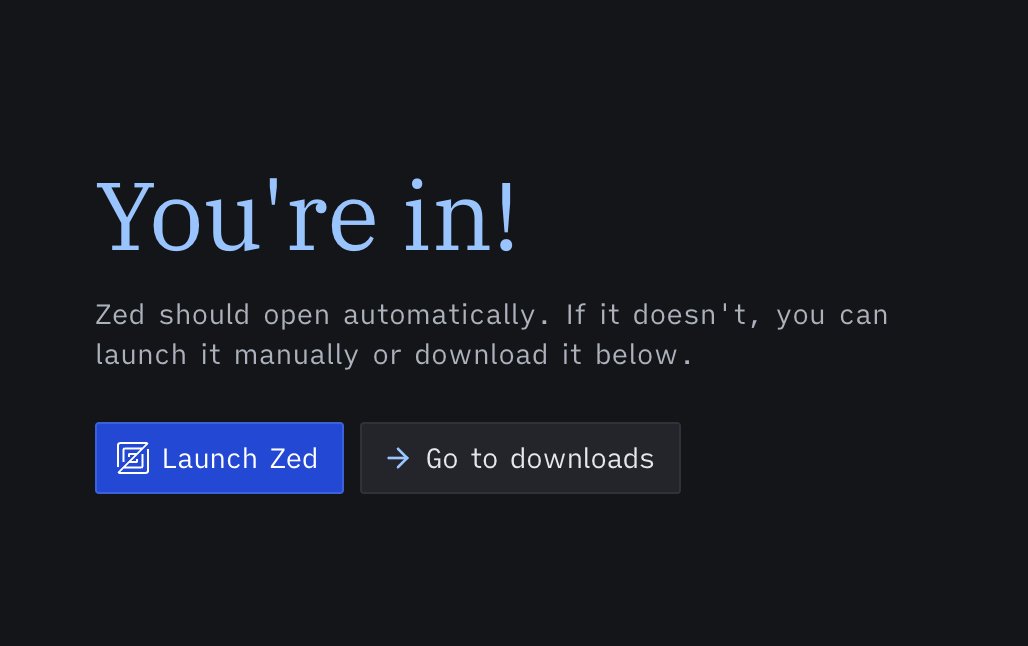

Introducing: Zed for Students! 🎓

Enjoy Zed's Pro plan free, for a year, if you're a current university student (or teacher!)

- Zed Pro features for 12 months

- $10/month in token credits

- Unlimited edit predictions

Apply today: https://t.co/YE6suEkB2U

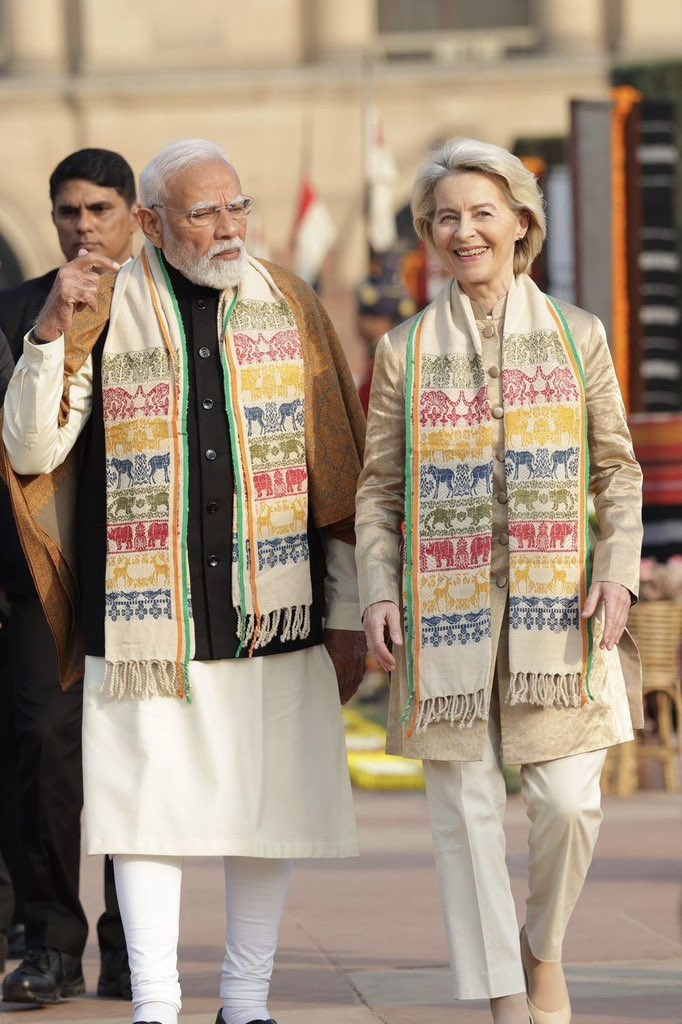

Europe and India are making history today.

We have concluded the mother of all deals.

We have created a free trade zone of two billion people, with both sides set to benefit.

This is only the beginning.

We will grow our strategic relationship to be even stronger.

Fresh from #WEFDavos:

"we are on the cusp of a historic trade agreement. Some call it the mother of all deals. One that would create a market of 2 billion people.." President @vonderleyen

President @antoniocostapm & @vonderleyen will visit India Jan 25-27. 🇪🇺🤝🇮🇳

#EUIndia

Europe is ready to deliver on a powerful new agenda with India.

Today, the EU agreed to move forward with the signature of a new Security and Defence Partnership.

It will expand our cooperation in areas such as maritime security, counterterrorism and cyber-defence.

I look forward to signing it next week during the EU-India Summit in New Delhi.

My intervention in #EPlenary ↓

This paper from Stanford University tackles a question that’s been debated for decades in quantitative finance: can raw market data alone meaningfully predict stock price direction, without handcrafted indicators or heavy financial feature engineering?

The author proposes a Convolutional Neural Network–based approach to predict the directional movement (bullish vs bearish) of individual S&P 500 stocks using pure multivariate price data.

Instead of technical indicators, the model consumes raw daily OHLCV data plus adjusted prices that explicitly encode dividends and stock splits, which are usually smoothed away or ignored in most academic work.

The core idea is subtle but important. Multivariate time series are treated as spatial objects, not just sequences. Each rolling window of historical prices is reshaped into a matrix that behaves like a 1D “image,” allowing CNN filters to detect local patterns such as short-term momentum, volatility shifts, and structural breaks caused by corporate actions.

This reframing borrows intuition from computer vision rather than traditional econometrics.

The dataset spans up to two decades of daily data per stock, sourced from an institutional-grade provider. Ten channels are used: open, high, low, close, volume, and their adjusted counterparts.

Sliding windows generate thousands of training samples per stock, dramatically increasing data density without synthetic augmentation. A normalization step ensures scale invariance across features.

Architecturally, the model uses a deep 1D CNN with eight convolutional layers, followed by fully connected layers and a Softmax classifier optimized with cross-entropy loss. Early layers focus on short-term price structure, while deeper layers capture longer-term trends.

Unlike LSTMs, which struggle with noisy gradients and statefulness in finance, the CNN’s localized receptive fields make it naturally robust to volatility spikes and event-driven price jumps.

The training objective is framed as a probabilistic classification task: predicting bullish or bearish movement over future horizons ranging from 2 to 30 days.

Extensive hyperparameter tuning reveals that performance depends heavily on window size, batch size, and learning rate, with Adam optimization and larger batch sizes producing the most stable convergence.

Results are where the paper becomes provocative. On several large-cap stocks, reported validation accuracies reach high-80s to low-90s percent, significantly outperforming earlier deep learning baselines trained on raw data.

JP Morgan stock, in particular, shows accuracy touching ~91% for longer forecast horizons. Loss curves and accuracy plots suggest genuine learning rather than overfitting, aided by careful train–validation splits and shuffling.

The author is careful not to overclaim. The model predicts direction, not returns, and does not directly incorporate transaction costs, slippage, or execution constraints. Still, the findings suggest that CNNs can internalize complex market mechanics directly from raw price tensors, including the non-linear distortions introduced by dividends and splits.

The broader implication is that feature engineering may be less critical than representation choice. By letting the model learn spatial relationships inside time-series windows, the approach sidesteps many subjective assumptions baked into technical indicators. The paper also hints at natural extensions: hybrid CNN–LSTM architectures, portfolio-level predictions, and integration of textual sentiment for fundamentals-aware forecasting.

In short, this work argues that treating financial time series as structured, image-like data is not a gimmick. It is a viable inductive bias that unlocks predictive signal from raw market data, challenging the long-held belief that markets are too noisy for deep learning without heavy human intervention.

Paper: S&P 500 Stock’s Movement Prediction using CNN

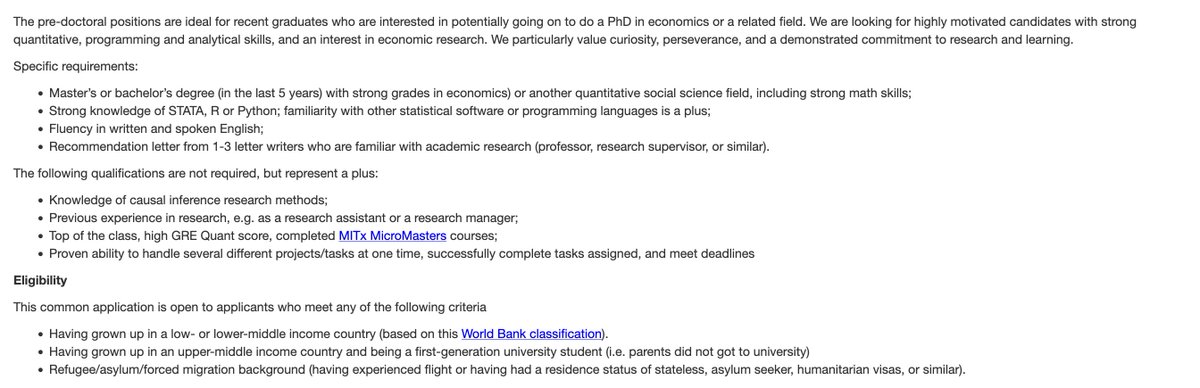

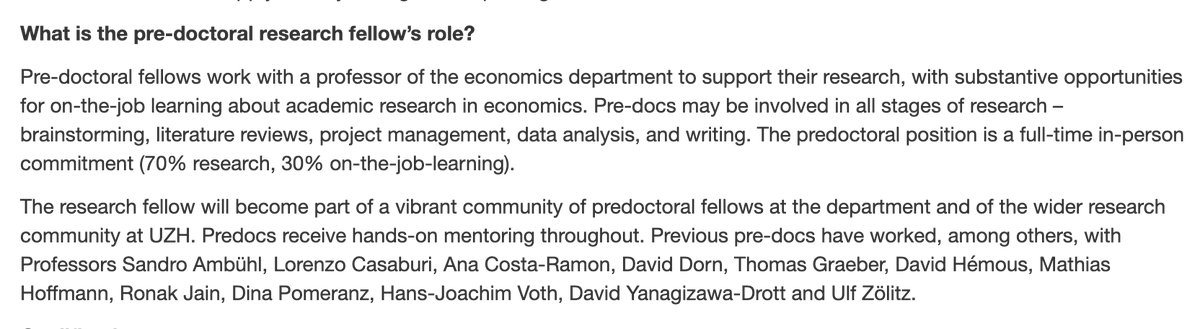

Great pre-doc opportunities at @econ_uzh in Zurich for aspiring PhD candidates from low- & middle income countries or with a refugee/asylum seeker background.

Predoctoral Program Global Talent Common Application: https://t.co/StEks06fZr Please share widely in your networks!

Karush–Kuhn–Tucker (KKT) conditions characterize optimal solutions of constrained optimization problems by linking gradients, constraints, and multipliers. In probability, they guide maximum-likelihood estimation under constraints. In machine learning, they shape SVMs, regularized models, and many training objectives. In real life, KKT principles support resource allocation, pricing, scheduling, and engineering design where optimal constrained decisions are essential.

When GoI starts citing violation of laws from 1937, you know it's a matter of time before the state comes down on you like a ton of bricks. Indigo deserves it.

⚓ Navy Day 2025

Celebrating the courage, commitment and professional excellence of the #IndianNavy — a force that protects us at sea and catalyses India’s maritime rise.

We present the curtain raiser of “Forged by the Sea”, the Indian Navy’s 2025 Special Feature —

a tribute to our sailors, our spirit, and our sea power.

🗓️ Stay tuned on 04 December 2025 for the full feature.

#NavyDay2025 #NauSenaDiwas2025 #IFR2026_India #OpDemo2025

@IndianNavy@IN_WNC@IN_HQENC@IN_HQSNC

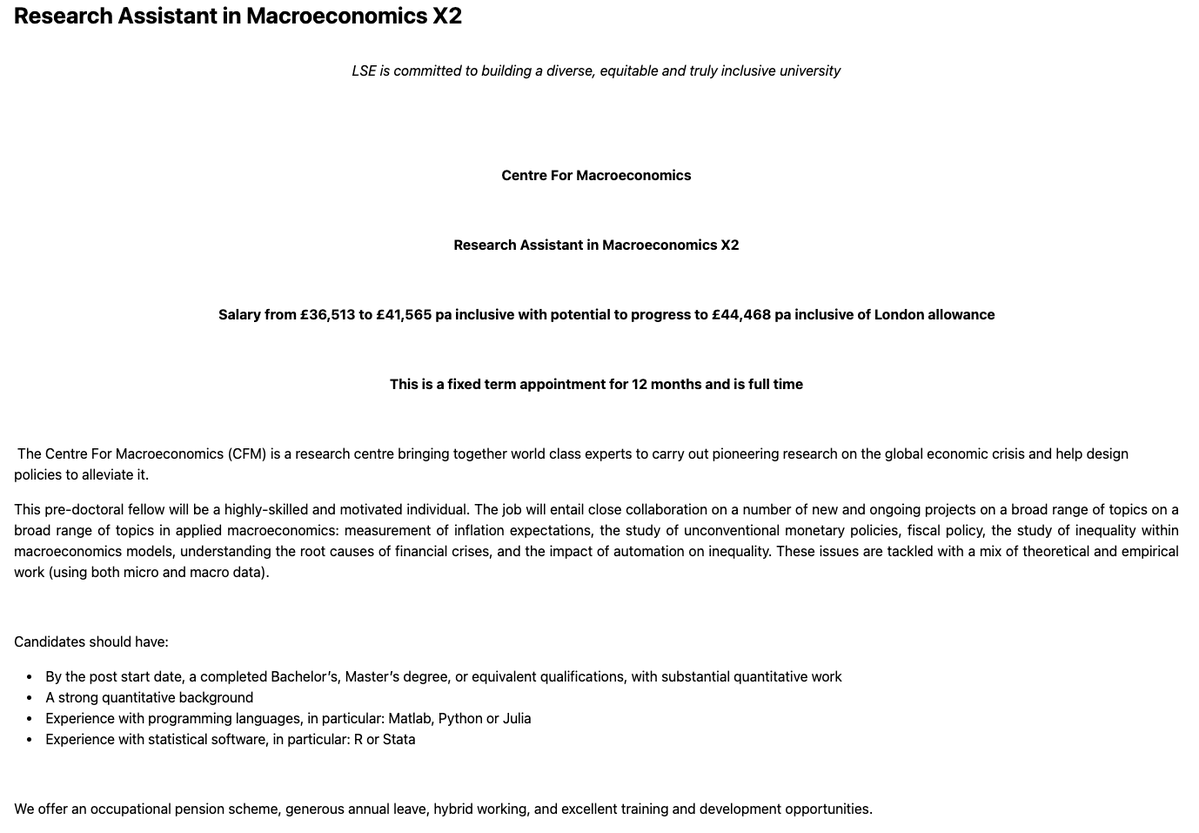

Macro at LSE is hiring pre docs for September 2025!

Come and work in the best city in the world, on cutting edge macro with me, Ethan @ilzetzki, Ricardo @R2Rsquared, Matthias (@mdoepke) and Ben @ben_moll!

Past predocs have gone to places like Harvard, LSE and Northwestern.