Deeply grateful for today’s pardon and to President Trump for upholding America’s commitment to fairness, innovation, and justice.

🙏🙏🙏🙏

Will do everything we can to help make America the Capital of Crypto and advance web3 worldwide.

(Still in flight, more posts to come.)

Onwards. 💪

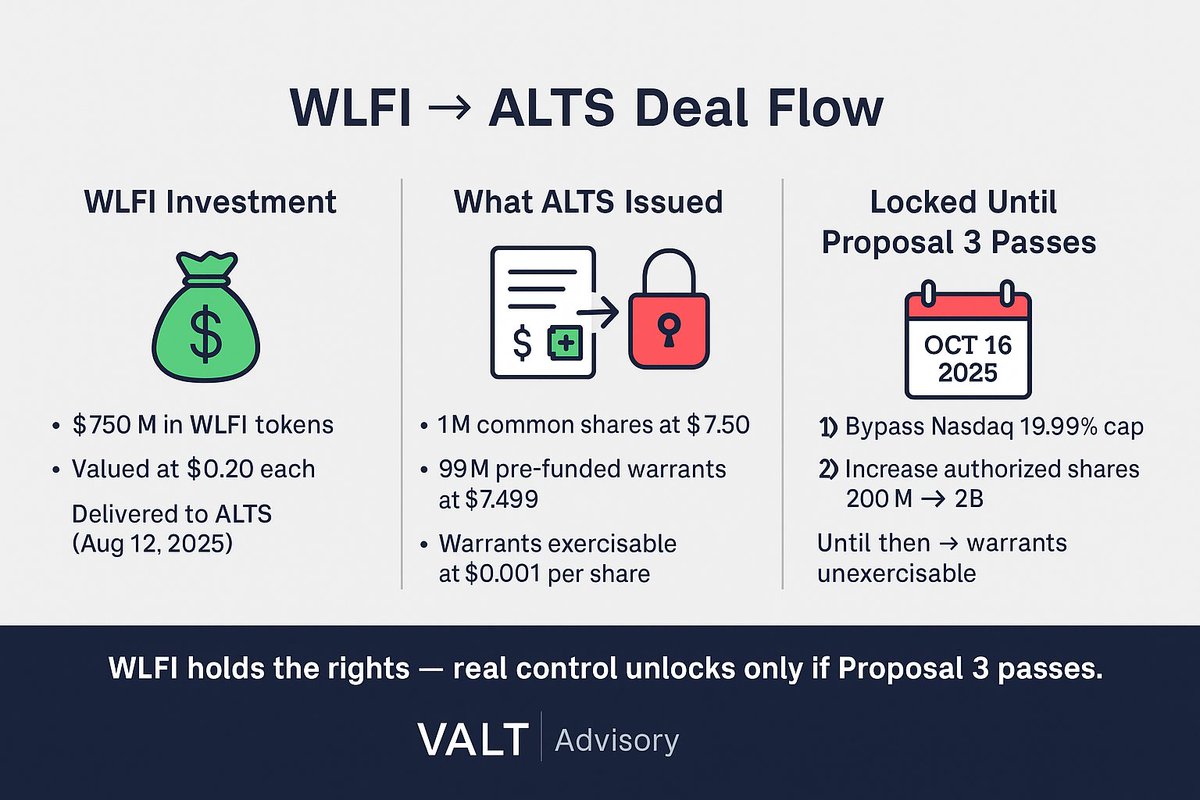

🚨 $ALTS Shareholder Vote Update

Alt5 Sigma’s Oct 10 Special Meeting delivered key approvals:

✅ Issuance of 119M shares to World Liberty Financial ($WLFI) - approved

✅ Appointment of WLFI’s second board director - approved

🕐 Proposal 3 to increase authorized shares to 2 B ➡ adjourned to Oct 16

This sets the stage for $WLFI to deepen control and for $ALTS to expand its capital structure ahead of the next phase of the treasury integration play.

#ALTS #WLFI #Tokenization #CryptoEquities

@benjoo7201 Short term: Bearish bias due to dilution risk and uncertainty.

Long term (if $WLFI executes): Potentially bullish if integration drives real utility and token-based revenue streams

🚨 $ALTS Shareholder Vote Update

Alt5 Sigma’s Oct 10 Special Meeting delivered key approvals:

✅ Issuance of 119M shares to World Liberty Financial ($WLFI) - approved

✅ Appointment of WLFI’s second board director - approved

🕐 Proposal 3 to increase authorized shares to 2 B ➡ adjourned to Oct 16

This sets the stage for $WLFI to deepen control and for $ALTS to expand its capital structure ahead of the next phase of the treasury integration play.

#ALTS #WLFI #Tokenization #CryptoEquities

@Dustin051917 $ALTS held its Oct 10 Special Meeting - $WLFI proposals were approved, but only by narrow margins, not overwhelming votes.

36.9M For vs 12.3M Against on share issuance

25M For vs 23.8M Against on WLFI’s 2nd board seat

That’s hardly a show of strong shareholder confidence.

1/

So it’s possible $WLFI got its shares + warrants approved but still can’t exercise those warrants yet because $ALTS hasn’t increased its authorized shares (Proposal 3 was adjourned to Oct 16).

Until that passes, there simply aren’t enough shares legally available.

2/

Even if the share increase passes, those warrants are priced $7.5–$9, while $ALTS trades near $2.40.

That makes them deep out of the money -no reason to exercise right now.

The leverage only matters if $ALTS re-rates higher post-vote or after a major WLFI catalyst.

3/

So for now, WLFI holds control on paper - not conversion power.

The real unlock happens after Oct 16, when share authorization could expand the capital structure for actual execution.

🚨 $ALTS Shareholder Vote Update

Alt5 Sigma’s Oct 10 Special Meeting delivered key approvals:

✅ Issuance of 119M shares to World Liberty Financial ($WLFI) - approved

✅ Appointment of WLFI’s second board director - approved

🕐 Proposal 3 to increase authorized shares to 2 B ➡ adjourned to Oct 16

This sets the stage for $WLFI to deepen control and for $ALTS to expand its capital structure ahead of the next phase of the treasury integration play.

#ALTS #WLFI #Tokenization #CryptoEquities

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

This week marks a pivotal inflection point for $ALTS.

Friday’s shareholder meeting concluded voting on the $WLFI takeover proposal - a deal that could transform @ALT5_Sigma into the first public-market proxy for the World Liberty Financial ecosystem.

Under SEC rules, the company has four business days to disclose results.

If approved, it unlocks $WLFI integration into a listed equity structure - a milestone for tokenized treasuries and crypto-linked balance sheets.

Outcome due this week. Watch closely.

This week marks a pivotal inflection point for $ALTS.

Friday’s shareholder meeting concluded voting on the $WLFI takeover proposal - a deal that could transform @ALT5_Sigma into the first public-market proxy for the World Liberty Financial ecosystem.

Under SEC rules, the company has four business days to disclose results.

If approved, it unlocks $WLFI integration into a listed equity structure - a milestone for tokenized treasuries and crypto-linked balance sheets.

Outcome due this week. Watch closely.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.

“When Liquidity Breaks Trust: $ASTER as the Natural Beneficiary of #Hyperliquid $10 B Meltdown”

The Catalyst - Structural Failure at Scale

The Trump-tariff crash triggered over $19 B in total market liquidations, with Hyperliquid alone responsible for ~$10 B - half the industry’s damage.

That number matters because it wasn’t just about leverage - it revealed thin internal liquidity and inadequate risk buffers.

Bloomberg’s post-mortem described Hyperliquid as having “the most amount of long liquidation, and the least liquidity to match,” meaning forced closes hit empty books.

Traders were wiped out not because they were wrong - but because the venue failed to absorb volatility.

The Sentiment Fracture - “We Got Liquidated by the Exchange”

Across X, sentiment turned decisively negative:

Screenshots of users losing entire accounts despite tight stops.

Accusations that Hyperliquid’s liquidation engine “front-ran” their orders.

Meme culture forming around “getting Hyper-liquidated.”

That’s not trivial - in DeFi, trust is liquidity. When traders feel betrayed, they migrate.

The Rotation - “From Forced to Fair”

Enter $ASTER.

With Hyperliquid’s credibility shaken, traders may rotating to platforms that promise:

Deeper LP vaults

Cross-chain execution

Hidden orders

Transparent liquidation logic

ASTER’s marketing as a “fair, transparent perp DEX” is perfectly timed - and its daily volume spiking past Hyperliquid’s confirms early inflow.

This is how narrative rotation begins: not with whitepapers, but with pain.

The Core View

Hyperliquid’s $10 B liquidation wasn’t just capital destruction - it was trust destruction.

$ASTER, positioned as the fair-execution alternative, now sits in the liquidity slipstream.

If traders rotate capital and volume proves real, this could be one of Q4’s best short-term rotation trades.