mostly global micro / small caps. experienced trader & PM, running my own capital. Valuations based on DCF and monte carlo, not hopes and dreams. Not advice!

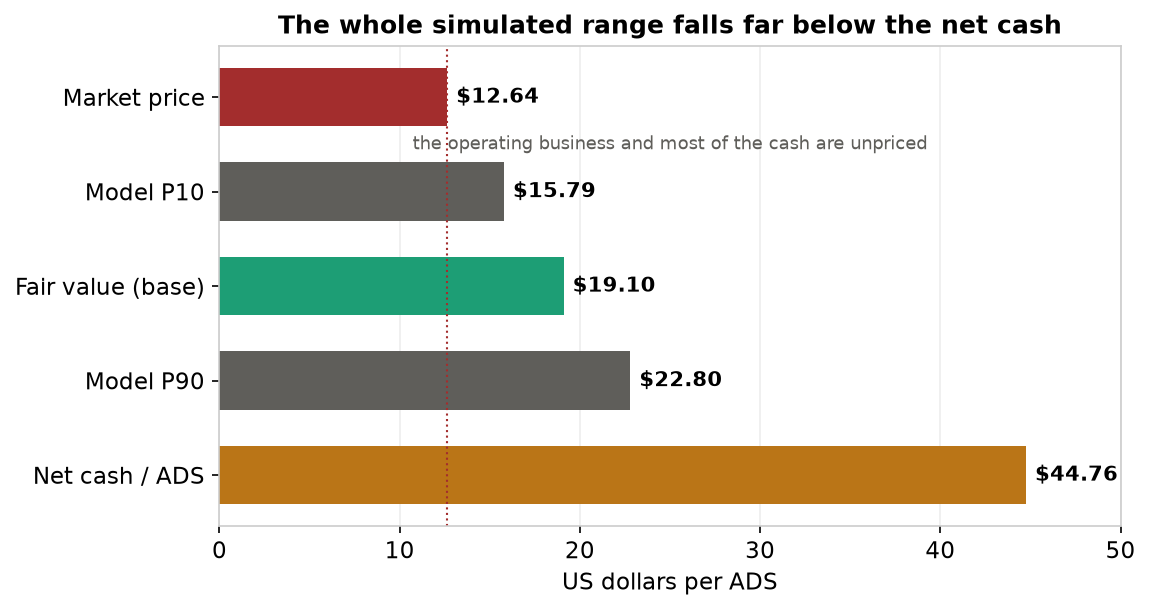

$SOHU trades at US$12.84 against about US$44.76 an ADS of net cash, zero debt, with the profitable Changyou games arm thrown in free. Our valuation opinion from earlier this week centres fair value near US$19.10 an ADS, about 49% above the current share price.

Full analysis with every assumption and source in the reply below.

I hold a position in https://t.co/73eN9oIhhM. Not investment advice, a valuation opinion. Do your own research.

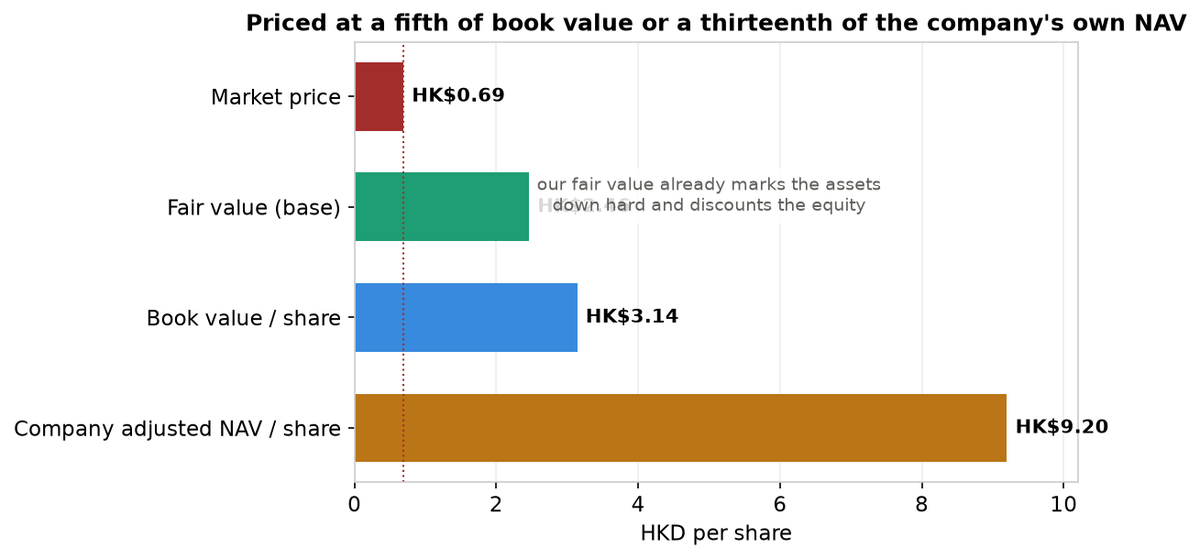

On its own valuation, Far East Consortium owns HK$9.20 a share of hotels, car parks and property. The shares trade at HK$0.70.

New valuation opinion: Far East Consortium, https://t.co/einJ6ZYFSq on the Hong Kong exchange. A property, hotels and car parks group controlled by the Chiu family, priced at about a fifth of book value.

What you get at the current share price of HK$0.70:

• Market value HK$2.1 billion on 3,059 million shares

• 0.22 times statutory book value of HK$3.14 a share

• Dorsett hotels, car parks and development land, carried in the accounts at cost, not market

• Net debt about HK$20 billion, roughly twice book equity, which is exactly why it is this cheap

Please not that this is a geared, distressed discount, not a free lunch. Three straight years of heavy losses, the dividend switched off entirely and Australian gaming exposure through the Queen's Wharf Brisbane complex alongside the troubled Star group.

So we take a harsh haircut to the company's own asset value before we value it. Even after that haircut, a seeded Monte Carlo simulation centres fair value at HK$2.46 a share, about 251% above the current share price, with every run landing above HK$0.70. Deeply cheap, with serious risks.

Full analysis with every assumption and source in the reply below.

I hold a position in Far East Consortium. Not investment advice, a valuation opinion. Do your own research.

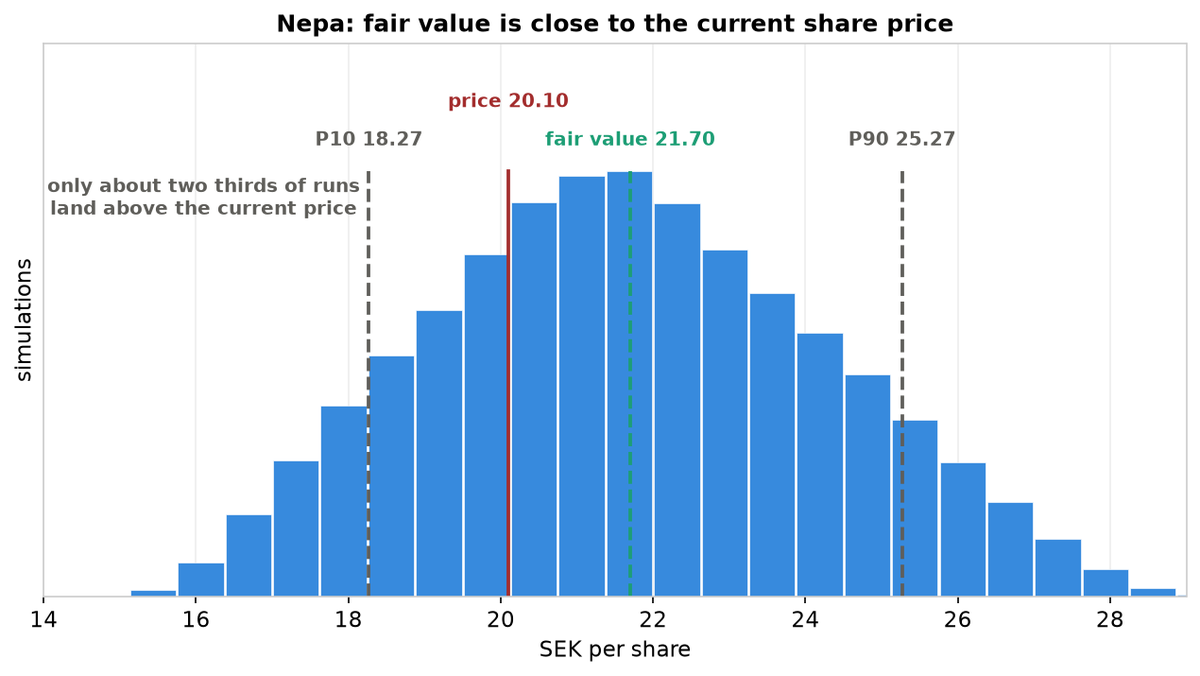

Three straight years of falling revenue and a SEK 34 million loss in 2025. Underneath that:

• zero debt,

• SEK 16.1 million of net cash, and

• a recurring revenue base that has started to turn up.

New valuation opinion: NEPA on Nasdaq First North Stockholm $NEPA, $NEPA.SS, the marketing analytics firm behind the brand tracking of some very large consumer names.

What you get at the current share price of SEK 20.10:

• Market value about SEK 158 million

• Enterprise value about SEK 142 million, roughly 0.64 times 2025 sales of SEK 222.6 million

• A gross margin near 75% on a majority subscription revenue base

• Annual recurring revenue bottomed at SEK 121 million in mid 2025, back to SEK 136 million

But the return to profit is cost driven, headcount is down about a quarter and reported revenue is still falling. The bull case needs the revenue turn to show up in the reported numbers. The next read is the Q2 report expected on 14 August.

Our seeded Monte Carlo simulation centres fair value at SEK 21.70 per share, about 8% above the current share price, with 72% of runs above it.

Modestly undervalued, not a bargain, yes we publish those verdicts too, not everything is cheap!

Full analysis with every assumptions and sources in the reply below.

I hold no position in Nepa. Not investment advice, just a valuation opinion. Do your own research.

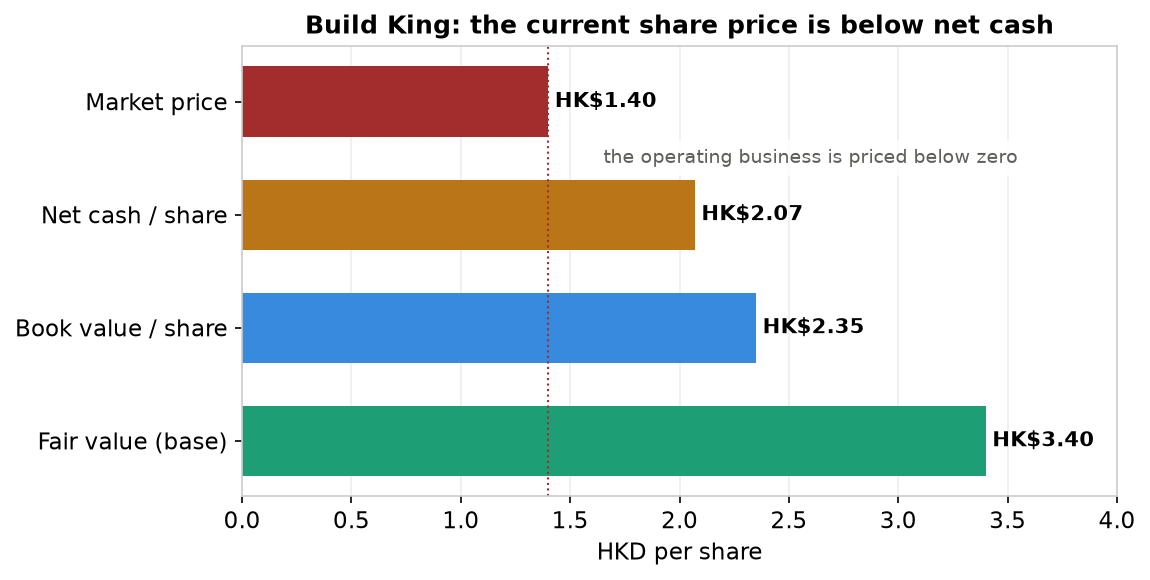

A reminder on the cheapest profitable contractor we have covered. Build King https://t.co/FQQoVcCHk9 builds Hong Kong's roads, housing and hospitals, earns money every year and holds about HK$2.07 a share of net cash against a HK$1.38 share price. The cash in its own bank account is worth about 50% more than the entire company, so the construction business, with a fully booked two year order book of HK$30.8 billion, is priced below zero.

It is cheap for reasons worth naming. Margins are thin, cyclical and still sliding, the 2025 profit growth was a cleanup of prior year charges and parent company Wai Kee controls about 58% of the shares. We price all three, normalise the earnings down and haircut the cash for the working capital a contractor genuinely needs. Fair value still comes out near HK$3.40, about 146% above the current share price.

While you wait, the company pays a dividend near 12% including this year's special, about 8% on the ordinary payments alone. A controlled contractor that actually pays out is a different proposition from one that hoards.

I hold a position. Not advice.

Growth was never the doubt with $NIO though, but profit is right? It is getting there, but still not fully.

Sales volume is up big every Q and the stock is red because every quarter still ends in a GAAP loss, so the market refuses to pay for growth it is still funding I think.

On a very positive note: the day a GAAP profit prints and holds, the re-rating can be fast, because the volume base will already be built.

Agreed, the math is absurd: at 0.4x EBITDA the market is calling the cash dead.

The main problem is that cash like this only moves when the controller (GungHo) decides or when they put in a lowball offer for the stock.. I do not think that anyone is questioning if cash is there though.

I do believe that the record date of 30th of June will be followed up by an actual dividend... first time they are doing this. But in good South Korean governance fashion they seem to execute the dividend in the worst way possible; without any communication to shareholders.

It still amazes me how this company seems to do everything right internally but with a total lack of respect to shareholders (minority shareholders at least).

So let's wait and see on that dividend $GRVY

as always; not advice!

Far East Consortium $35.HK is a Hong Kong property, hotels and gaming conglomerate that trades at about a fifth of its book value. Its hotels and car parks earn money, but a HK$20 billion debt load and a HK$835 million interest bill sink the group to a loss, on top of that it pays no dividend.

A shite company then? Our fair value is HK$2.46 against a HK$0.69 share price. A deep discount and a risky one.

As always, not advice. DYODD!

Link to substack post in the first reply.

Since quite a lot of you are clicking the links, please consider subscribing, liking or reposting if you like the article. Would be very much appreciated!

A reminder on one of the cheapest balance sheets we have written about so far.

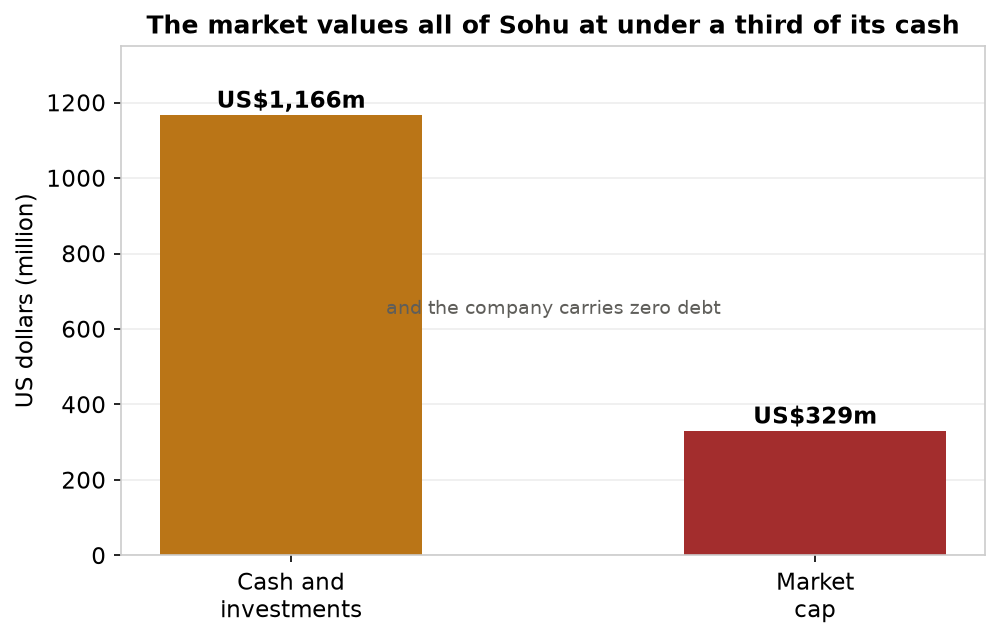

https://t.co/73eN9oIhhM $SOHU holds about US$1.2 billion of cash and investments, roughly US$44.76 an ADS, with zero debt, against a share price around US$13. So the market pays under 30 cents for every dollar of cash and it values the profitable games business, Changyou, at less than nothing (okay there are some other issues).

The catch is governance, not so much the location of the cash. A founder has controlled Sohu for 25 years and has never paid a dividend. Much of the cash is held offshore, the proceeds of the 2021 Sogou sale to Tencent, so it is accessible. It just never comes back to investors, al least not through dividends.

The one thing that does return cash is a buyback, which has retired about a quarter of the shares since 2023. That is the whole thesis: if it keeps going the discount will probably close, if it stops the cash stays whereever the founder wants it. We credit only 40% of the net cash for that governance risk and leave Changyou's ongoing profit as upside we do not even model.

Even then we reach a fair value near US$19 an ADS, well above the current share price.

Full write up is in the link below. and remember;

Not advice, ever! DYODD

@Reignots@ClarkSquareCap Is the signal function not just as important as the actual size of the div pay-out? It is a clear signal to the bear case level (at which the stock currently trades imo).

Build King $240.HK, a profitable Hong Kong contractor, trades at HK$1.40 while holding about HK$2.07 a share of net cash, more than its entire market value.

The construction business, with a fully booked two year order book, is priced below zero. On top of that, the company pays a dividend near 12%.

Our fair value is about HK$3.40.

Not advice, DYODD!