Here is the 5th business of the 20 unique businesses. This one is from the world of pharma. It is a company which truly stands by the complete Integrated facility across the entirety of the CRDMO cycle , along with unique CDMO molecule pipeline which does not have a single molecule dependency unlike most others.

One of the only CRDMO companies in the country that is able to execute well and grow at a faster pace at the same time...

Most Indian companies do ONE of these. Sai Life Sciences does ALL THREE.

This is the story of India's most integrated CRDMO and why it could be a structural story.

Let's understand the why behind it!

The Toll Booth on the Digital Economy → The One Company Without Which AI Does Not Exist

One of the most unique companies in the entire global semiconductor value chain that checks our filter of unique businesses :-

→ High barriers to entry (might need at least 15 yrs to crack which is both R&D and cost heavy to build it)

→ Cannot be replicated even with a blank cheque (China has tried for a decade)

→ Exceptional return ratios

→ Zero direct competitors at the leading edge

→ Doing something that sits at the absolute frontier of human engineering

Let's discuss more on ASML Holding in 3 simple steps :-

→ Why this business is Unique → Financial Health → Growth Triggers

The third "unique" business we are discussing today rides on one of India's strongest structural trends. As our GDP expands, the nation gets wealthier, and the "Financialisation of Savings" gathers pace. We believe this company is perfectly positioned to capitalize on these massive tailwinds.

Let's dive into Nuvama - understanding on first that why this business we think is unique, Understanding Financial Health and Future growth triggers for the company

This is the second part of our "Finding Moated Business" series, following our previous discussion on INOX INDIA.

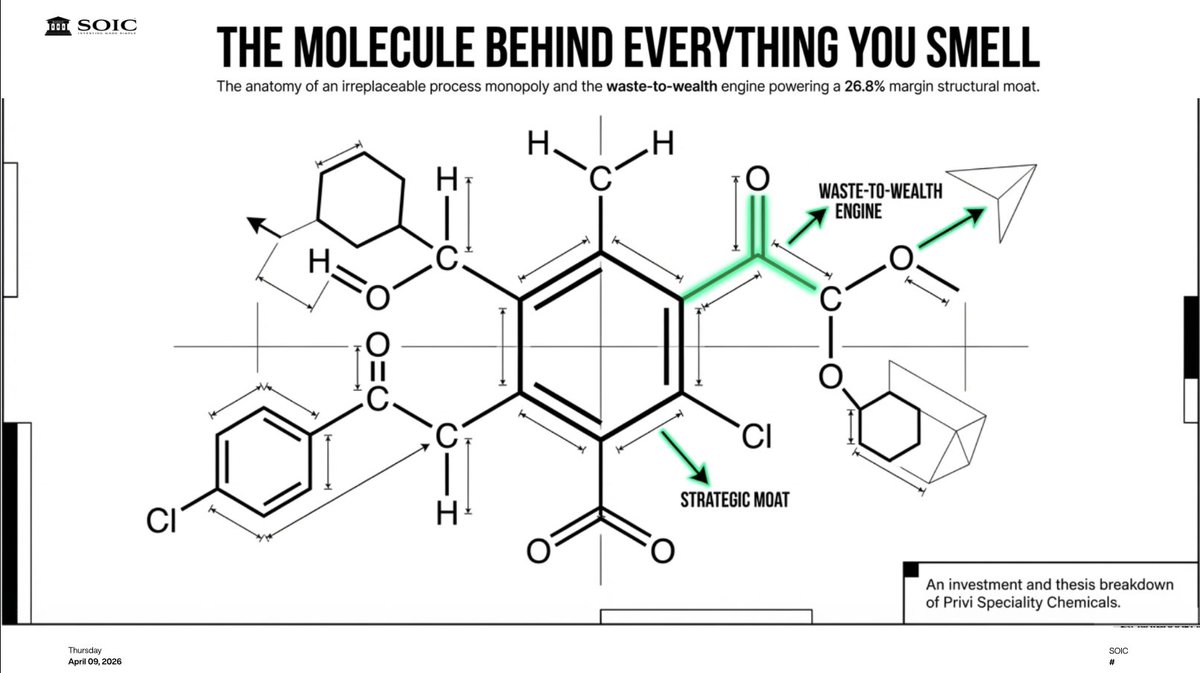

The focus this time is on another highly intriguing Indian chemical company. It's one of only four such companies globally, which strongly suggests the presence of a significant competitive advantage, or MOAT, in its business model.

In this thread, we will analyze this business in three key steps:

1) Understanding what makes this business MOAT-ed and how.

2) Assessing if this MOAT translates into robust financial performance for the company.

3) Determining if this MOAT's primary function is to simply accumulate cash on the balance sheet at a normalized growth rate, or if it provides the capacity for growth significantly faster than its industry peers.

One of the unique capital good companies that checks our filter of unique businesses -

→ High barriers to entry

→ Cannot be replicated just via blank cheque

→ Good return ratios

→ Limited competitors

→ Doing something cutting edge

Let’s discuss more on Inox India’s Business in 3 simple steps

→ Why this business is Unique

→ Financial Health

→ Growth Triggers

Feels like we might be closer to the bottom of the MFI cycle. The real story is how earnings shape up once credit costs start easing.

Explored this angle recently in detail here:

https://t.co/DXAV5jrcpk

My 2 cents on Arman -I would say that given the sector NPA% is coming down and so is Armans NPA coming down ,even if the price reaches median price to book value (3.9) from present 1.8 then Arman share price should more than double in less than 3 years time

Detailed deep dive on a classic distressed turnaround that’s showing signs of life

You will find inside :-

> A interesting turnaround case study

> + A 3 step framework for finding asymmetric plays in metal and mining businesses

https://t.co/hm62C9kN1v

Disclaimer - not a recommendation to buy/sell

A deep dive on a business in the Generic CMO space in Domestic Pharma

Blog covers the

1. Value chain

2. Difference between CMOs vs CDMOs

3. Generic Drugs

4. About the business model

5. Different business segments

6. Growth triggers

7. Valuations & Risks

https://t.co/KAhaQwUKLh

Disclaimer: no recommendation to buy or sell.

Dynamatic ties up with Dassault for complete rear fuselage manufacturing of Falcon 6x

Blog to understand the complete business:

https://t.co/gakOF2t6wd

What is the purpose of SOIC YouTube channel?

Entire purpose is to educate you on businesses and industries. There are very few in depth fundamental Yt channels in India.

Do we recommend stocks here?

Absolutely not. If we cover 5 businesses in an industry some might do well and some might not. Entire idea is to teach you on how to do it yourself or to make you more aware about these industries.

We covered Peb, bottlers, exchanges, hospitals, Cdmos etc etc. we are proud of the fact that people who are serious learner’s will use these videos as the starting point and not the ending point.

For those who come to channel for recommendations. You are not at right place. Given it’s an educative channel on industries and businesses.

Hope this is clear :)

Time to add far more value going forward!

Q2 FY26 was a big quarter for Indian hospitals.

Strong revenue growth almost across the board… but with very different stories on margins, payor mix and scalability.

Let’s walk through the peer set and then answer the core question: who actually delivered the standout Q2?

Here a while back we discussed Zomato (Eternal)

A webinar one can refer to understand how to analyse and value platform business

The valuation in this might not make sense now as a lot of facts changed for the company but a template one can use to understand on how to value platform businesses

Disclaimer - We had an active recommendation in the company in past and have exited a while back. This is not a recommendation to buy/sell and is only for education purpose

Is AI the next IT bubble?

Short answer “No”. AI is tracing the arc of Shales. Like the US oil boom, the narrative is shifting from scarcity to abundance. The early parallels—surging capital, stretched valuations—echo the dot-com era. But unlike 1999–00 (where productivity gains evaporated) or the 1980s AI Winter (rule-based systems failed), this is a profound, capital-intensive structural buildout.

Here in this thread I would not bore you with all the story of how AI was built and history of it rather would jump on straight to the discussion on how we view this as the multi year boom and where does the real value lies in the AI value chain out there

So let’s dive deep and understand what AI has brought in for us investors as an opportunity…

The Indian healthcare delivery industry is projected for robust growth at a Compound Annual Growth Rate (CAGR) of 9–11% between FY25 and FY27.

This expansion is supported by long-term structural drivers such as favourable demographics, rising incomes, increasing chronic diseases, and the growth of medical tourism. The overall healthcare delivery market is expected to reach ₹7.8 trillion by fiscal 2027.

Here's the deep dive on what's happening with the listed hospitals in India👇

In just 3 years, ~72 MTPA of capacity changed hands -almost the same as ~82 MTPA over the entire FY12–22 decade.

That’s not noise; that’s a structural reset that’s pushing the top-5 share toward ~62% by FY27 and hard-coding discipline into the sector’s DNA.

Lets' try and understand how this boring sector is suddenly in the lime light

A few months back at , we studied a unique auto ancillaries that has been consistently able to outperform the auto growth.

A business whose business model who thrives on the concept that, "Its much easier and cheaper for the OEMs to make the cars look innovative that them to be actually innovative"

SJS Enterprises is a quiet beneficiary of this shift sitting at the intersection of Good Products, Deep Pocket Penetration, and Rising Aesthetics.

If cars are turning into lifestyle statements, SJS is the ideal proxy to this :

> from decals, overlays & chrome plating → to 3D lux parts & hydrographics

> from low-ASP commoditised trims → to high-margin premium surfaces

This is a sustainable long term trend and just an one-off fad led by premiumisation - global & domestic.

Consumers want aspirational interiors & Deep pocket penetration - once inside an OEM platform, SJS expands wallet share model-by-model and by increasing ticket size and launching more products with similar synergies

This is not just a story but a reality which the company has been able to show even into the numbers by outperforming the Industry for 23 consecutive quarters.

Disclaimer - not a recommendation to buy/sell

https://t.co/TMWg0BpPnC

August export data for chemical companies in India

Companies that showed strong growth -

- Aarti Industries

- Balaji amines

- Neogen chemicals

- Tatva chintan

- Archean chemicals

Disclaimer - Not a recommendation to buy or sell