While many DePIN projects compete on hardware specs, @theblessnetwork takes a different approach leveraging the devices you already own.

Idle time becomes earning time.

A truly decentralized compute network where every node is equal and sovereign. Simple, efficient, powerful.

32 Bitcoin. $2.47 million. 0.003% of the total position.

MSTR dropped 6%. BTC dropped 4%. $766 million in liquidations.

A $2.47 million sale moved a multi-trillion dollar narrative. That's the first thing worth understanding.

The symbolism mattered. The most famous "never sell" advocate selling anything handed a nervous market a reason to panic, right as the selling accelerated.

Saylor's explanation was immediate. He described the act as economic arbitrage proving Bitcoin's liquidity to lenders and credit agencies.

The proceeds met dividend obligations. He called it a "nothing burger."

He's technically right. 32 BTC against 843,706 BTC is mathematically irrelevant.

But here's what the market is actually reacting to.

The "never sell" narrative wasn't just philosophy. It was a financial instrument.

Strategy's ability to raise billions at favorable rates depended on institutional confidence that the Bitcoin position would never be touched.

That confidence underwrote the capital structure.

Throughout much of the year, markets could count on two major buyers: ETF demand and Strategy accumulation.

Both appear considerably weaker today than they did just a few months ago.

That sentence is the real story. Not 32 BTC.

Strategy has moved from accumulation mode to management mode.

➝ Phase 1 (2020-2025): raise capital

→ buy Bitcoin

→ repeat

➝ Phase 2 (2026): manage capital structure → meet obligations

→ maintain position

The loop has conditions now.

That's the phase change the market is pricing.

The number to actually watch isn't how many BTC Strategy sells.

It's whether the STRC preferred share program keeps raising capital at scale. That program funds new BTC purchases.

If raises stay strong

→ Strategy resumes buying

→ narrative heals. If raises slow

→ $1.5B annual obligation gets met from Bitcoin sales → it doesn't.

32 BTC wasn't the news. The question it opens is.

$MEGA launched with one of the lowest circulating supplies we've seen

most of the supply is supposedly locked

team locked

VCs locked

foundation locked

yet every bounce gets sold into immediately

either someone's got access earlier than they should

or the market is learning something before the rest of us

Bitcoin closed May at $73,000. Worst monthly close of 2026.

And June might be the most important month in crypto history. Not because of hype because of what's actually scheduled.

Three catalysts. Same 30-day window. Never happened simultaneously before.

CLARITY Act floor vote

"If the Senate fails to pass the bill before the August recess, the bill's prospects would deteriorate materially."

That's Stifel's chief Washington policy strategist not a crypto analyst. The window is June, or it's 2027.

Seven Democratic votes needed. Gallego said if ethics isn't resolved, "I am not afraid to vote no."

Alsobrooks said the same. The White House won't accept language targeting Trump.

Democrats won't vote yes without it. Someone has to move this month.

Warsh FOMC June 16

He can't cut rates. CPI 3.8%, PPI 6%, oil $100+, yields 4.6% the math doesn't allow it.

But he can signal. Tone, language, H2 forward guidance. Same data, different framing, completely different market reaction.

If he sounds hawkish, six more months of headwind. If he signals patience the setup changes.

Strait of Hormuz

Progress in ceasefire talks reduces the geopolitical risk premium on energy, easing inflation fears, making investors more willing to allocate to risk assets.

Oil from $100 to $85 changes the CPI calculation. Which changes Warsh's options.

Which changes ETF flows. Which changes BTC's price. These catalysts aren't independent they're chained.

➝ All three positive: $80K resistance breaks, H2 recovery sets up

➝ One disappointment: range-bound through summer

➝ All three negative: $70K retest

The structural case survived May intact. Exchange reserves 7-year low.

$58.72B in ETF infrastructure. Regulatory framework closer than ever.

But structure doesn't move price in the short term. Catalysts do.

June has three of them. That's the whole story.

RWA market is sitting at $17 billion right now.

by 2030? $5.5 trillion.

aggressive scenario? $8.2 trillion.

we're talking 300x to 500x growth.

this is one of the biggest "real money" narratives crypto has ever seen.

Two weeks ago, ICE went to the CFTC.

The message: Hyperliquid threatens global oil benchmark integrity. Shut it down or regulate it hard.

This week, at the Bernstein conference, Jeffrey Sprecher the CEO of ICE, the company that owns NYSE said something completely different.

Hyperliquid is "bigger than Nasdaq" in trading activity. The team is "very, very smart people."

$HYPE jumped 8% within the hour.

So what actually happened?

Three ways to read this.

➝ Genuine recalibration. The CFTC complaint went nowhere. Hyperliquid hit an ATH.

The regulatory attack failed. Sprecher acknowledged a competitor's strength rather than continuing to look threatened by it.

➝ Acquisition signaling. ICE acquired NYSE for $8.2B. Interactive Data for $5.2B. Ellie Mae for $11B.

Their entire growth strategy is buying the infrastructure layer of financial markets.

"Very smart people" running a platform "bigger than Nasdaq" that you can't regulate away that's historically been a term sheet, not a press release.

➝ Both simultaneously. The CFTC complaint creates regulatory pressure that forces Hyperliquid to spend resources on compliance.

The public praise signals willingness to deal. Create friction, then offer partnership. This is how large incumbents handle threats they can't eliminate.

Here's what actually matters though.

Sprecher said this at a Bernstein conference not on crypto Twitter. The audience is institutional investors and large allocators.

When the owner of NYSE calls a DeFi platform "bigger than Nasdaq" in that room, those people update their models.

Everything was down this week.

HYPE went up 8% on a single quote from a CEO who two weeks ago was trying to get it regulated out of existence.

The incumbents spent years ignoring DeFi.

Then attacking it. Now the CEO of NYSE's parent company is praising it at institutional conferences.

That's not the end of the conflict. It might be the beginning of something more interesting.

When your biggest enemy starts complimenting you in rooms full of their investors, you're either about to be acquired or about to be taken seriously as a permanent part of market structure.

For $HYPE holders, both outcomes are bullish.

Been watching @Outcomexyz quietly and the traction is real.

#1 front end on Hyperliquid's HIP-4, 10x the volume of second place. Self-funded, built by traders who were early $HYPE market makers.

500K $HYPE staked for permissionless deployment, only team on the board with that stack.

What makes this interesting to me is the team profile. No VC money, no hype cycle, just people who actually traded the thing building infrastructure around it.

That tends to produce better products than the alternative.

First badges dropping now, retroactive for Hyperliquid OGs and testnet participants. More rounds coming.

If you're in that group, worth checking eligibility sooner rather than later.

This week gave you two completely different signals at the same time.

Signal one: Someone sold $1.29 billion worth of BlackRock's IBIT in a single dark pool transaction.

Strategy paused Bitcoin buying for the first time in its multi-year accumulation program.

Spot ETFs posted seven consecutive days of outflows the longest streak since February.

BTC got pulled to $74K, exactly where max pain predicted it would go. ETH hit $2,003, sitting just above its own max pain of $2,200.

Signal two: Bitcoin exchange reserves have dropped to their lowest level since 2018 a seven-year low as continued withdrawals from trading platforms suggest long-term holders are moving coins into cold storage rather than preparing to sell.

Those two signals are pointing in opposite directions. And both are real.

Here's the honest read.

The $1.29B dark pool IBIT sale is the most discussed number this week. But context matters.

Dark pool transactions of this size typically represent institutional portfolio rebalancing rather than a directional bet against Bitcoin large funds managing multi-asset portfolios routinely rotate positions without it reflecting a fundamental view change on the underlying asset.

IBIT has $60B+ in AUM.

A $1.29B rebalance is 2.1% of the fund. That's noise at institutional scale, not a conviction exit.

Strategy's pause is more interesting.

Strategy completed the repurchase of $1.5 billion in convertible notes at an 8% discount to face value the first significant pause in its multi-year Bitcoin acquisition program.

The move reflects a new phase in capital management, with balance sheet quality now sitting alongside Bitcoin exposure as a key part of the story.

Read that carefully. Strategy didn't sell Bitcoin. They stopped buying new Bitcoin and used that capital to retire debt at a discount.

That's not bearish on Bitcoin. That's a CFO doing their job when the cost of capital exceeds the expected short-term return.

Strategy's year-to-date Bitcoin yield for 2026 climbed to 13.3% despite the pause, with holdings steady at 843,738 BTC acquired at an average price of $75,700.

Average cost basis $75,700.

Current price $74,000. The total stack is marginally underwater for the first time.

That number matters not because Strategy is in trouble, but because the psychological anchor has shifted.

When you're above your cost basis, every dip is a buying opportunity. When you're below it, the calculation changes.

Now the ETF outflow streak.

Seven consecutive days of outflows is the kind of data point that gets amplified into a narrative. The reality is more nuanced.

Deribit's chief commercial officer noted that sentiment has shifted noticeably since Bitcoin briefly climbed above $82,000 in early May, with traders now focused on inflation concerns, weakness in global bond markets and escalating tensions involving Iran.

That's macro, not structural.

The same macro that pushed oil above $100 and 10-year yields to 4.6% is creating headwinds for every risk asset simultaneously.

ETF outflows in this environment are expected they're the same institutional allocators doing the same 4.5% Treasury vs volatile BTC math we've talked about for weeks.

Here's the signal that cuts through all of it.

Bitcoin has spent much of 2026 trading like a high-risk tech asset, with its correlation to the Nasdaq hitting a record 0.96 in April meaning a Nasdaq selloff could drag crypto down with it, regardless of its digital gold narrative.

That 0.96 correlation is the most important data point of the week and nobody's really sitting with it properly.

If Burry is right about the AI bubble if the Nasdaq is in its 1999 final stage then Bitcoin's 0.96 Nasdaq correlation means it falls with the market regardless of exchange reserves, regardless of institutional infrastructure, regardless of CLARITY Act passage.

The "digital gold" thesis only works if Bitcoin decouples from risk assets. At 0.96 correlation, it hasn't.

But here's the counterargument.

The last time Bitcoin had high Nasdaq correlation was 2022. When the Nasdaq fell 33%, BTC fell 65%.

The correlation was real. But the crash also flushed out the leverage, reset the market structure, and set up the 2023-2024 recovery.

Bitcoin enters May-end with nearly $15 billion in combined Deribit options and CME Bitcoin futures open interest the pressure point being the May 29 expiry, where roughly $6.25 billion in contracts settled.

That makes May-end less about spot price and more about positioning, with Bitcoin's next major move depending on how quickly traders unwind, roll, or defend positions after the expiry.

The expiry just cleared. $8 billion in options settled. The leverage has been flushed.

Strategy cleaned up its balance sheet. The dark pool sale happened and the market absorbed it.

So which signal wins?

The honest answer depends on one thing Burry can't tell you and the on-chain data can't tell you either.

Does the AI narrative hold or does it crack?

If Nasdaq stays elevated through June and Warsh signals a more accommodative path on June 16 BTC's 0.96 correlation works in its favor.

Rising Nasdaq + crypto-friendly Fed = post-expiry bid materializes.

If Burry's right and the AI bubble starts deflating in June the same 0.96 correlation that hurt BTC this week becomes a weight.

Exchange reserves at 7-year lows won't matter if the broad selloff forces institutional rebalancing across every risk asset simultaneously.

The structural case is intact. The correlation risk is real.

Both things are true. The next 30 days will tell you which one matters more.

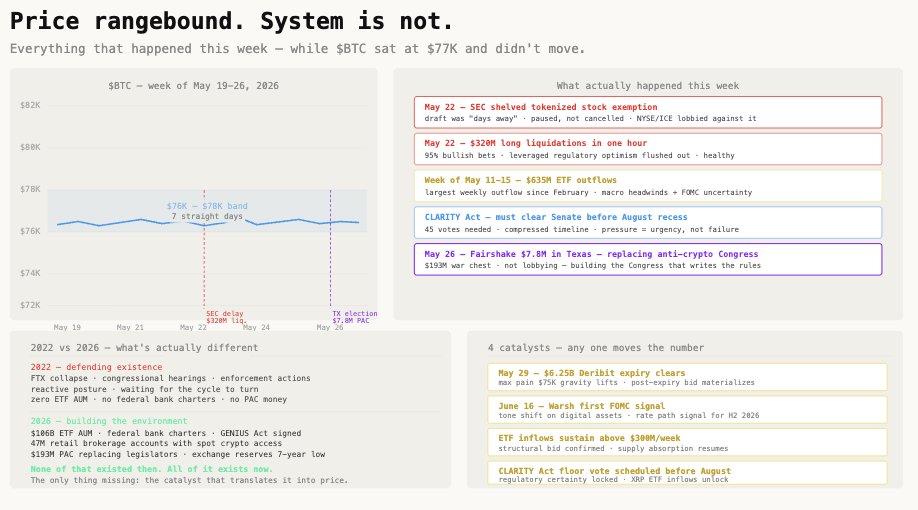

Everyone's watching the chart. The chart isn't the story this week.

BTC is at $77K. Exactly where it was Monday. And this is what happened in between.

SEC shelved the tokenized stock exemption. $320M in longs got liquidated in one hour.

ETF weekly outflows hit $635M. CLARITY Act floor vote confirmed as must-happen before August.

Fairshake spent $7.8M in a single Texas congressional race to replace an anti-crypto Democrat with a pro-crypto one.

Price didn't move. Everything else did.

Here's the thing about the $320M liquidation and the SEC delay.

Neither of those is what it looks like. The SEC didn't kill tokenized stocks it paused a draft that was days from release.

The liquidation wasn't a crash it was over-leveraged regulatory optimism getting flushed out. Both are healthy.

The Fairshake story is the one worth actually paying attention to.

➝ $7.8M in one Texas House race

➝ $193M total 2026 war chest

➝ Already deployed in Georgia, Kentucky, Alabama, now Texas

➝ The goal isn't lobbying it's replacing the legislators who write the rules.

In 2022 this industry was defending its existence in congressional hearings.

In 2026 it's buying the Congress that writes the rules. That's not a subtle shift.

Now look at what's actually sitting underneath the price.

$106B in US spot ETF AUM. $34B in tokenized RWAs. Federal bank charters for Coinbase, Kraken, Ripple, Circle.

47 million retail brokerage accounts with spot crypto access. GENIUS Act signed.

Warsh at the Fed.

Exchange reserves at a 7-year low. Whale accumulation at its highest since 2013.

None of that existed in the last cycle. All of it exists now.

The market is waiting for one catalyst to translate all of it into price. CLARITY Act floor vote. May 29 Deribit expiry clearing.

June 16 Warsh FOMC signal. ETF inflows resuming above $300M weekly. Any one of those moves the number.

The price is rangebound. The system is not.

That's not a contradiction. That's a setup.

Paul Atkins stood at the Economic Club of Washington and said the SEC was

"on the cusp" of releasing an innovation exemption for tokenized stocks.

That was May 8.

On May 22, the SEC shelved it indefinitely.

Two weeks. From "on the cusp" to "indefinitely delayed."

And $320 million in long positions got liquidated in the same hour the news broke.

Here's what actually happened and why it's more interesting than a simple regulatory delay.

The SEC was preparing to release its so-called innovation exemption for tokenized stocks as soon as the week of May 18, according to people familiar with the matter.

A draft had been prepared and reviewed by staff. The framework would have created a regulatory sandbox allowing crypto firms to offer on-chain versions of US equities.

Then NYSE and traditional stock exchange officials pushed back. Hard.

Several crypto industry executives argued that the SEC should avoid rushing a framework for tokenized securities.

Carlos Domingo, CEO of Securitize, wrote that regulators should ensure the exemption "applies to the right instruments," adding that delaying would be preferable to introducing rules that create operational or legal problems.

The official reason is shareholder rights. Who actually owns the underlying stock when a token represents it?

The SEC has continued drawing a distinction between "custodial" tokenized securities issuer-backed shares held through regulated intermediaries that provide investors with shareholder rights.

"synthetic" tokenized securities that only offer price exposure without transferring ownership.

That's a legitimate regulatory question. But notice who raised it loudest.

NYSE. ICE. The same institutions that own the existing equity trading infrastructure.

The same institutions that went to the CFTC two weeks ago to complain about Hyperliquid manipulating oil markets.

This is the same playbook. Different venue. Different asset class. Same incumbents.

➝ Week 1: CME and ICE go to CFTC "Hyperliquid's perp markets threaten benchmark integrity"

➝ Week 2: NYSE and exchanges go to SEC "tokenized stock exemption threatens shareholder rights"

Both arguments have legitimate regulatory substance.

And both are being made by the parties who have the most to lose from these markets existing.

The SEC's decision halted a framework that would have allowed crypto platforms to offer on-chain versions of traditional equities under a regulatory sandbox.

The delay leaves blockchain-based equities in regulatory limbo and triggered immediate selloffs across crypto markets and related equities.

Here's the part that makes this genuinely complicated.

The SEC had already approved Nasdaq's tokenized equity trading rules in March 2026 and NYSE's in April 2026, both allowing tokenized versions of select equities to trade alongside traditional shares via a DTCC tokenization pilot.

Those approvals now exist without the broader innovation exemption that was meant to accompany them.

So the SEC approved Nasdaq and NYSE to do tokenized equities.

Then delayed the broader exemption that would let crypto-native platforms do the same thing.

Nasdaq and NYSE can tokenize. Hyperliquid and Ondo cannot at least not under a formal regulatory framework.

Who benefits from that asymmetry?

Nasdaq and NYSE.

And here's the kicker. While the SEC deliberates, the market keeps moving.

Hyperliquid's HIP-3 framework has become the dominant perp venue trade.

xyz runs 24/7 perpetual markets for Tesla, Apple, Nvidia, Amazon and a synthetic Nasdaq index, with HIP-3 now driving over 35% of all Hyperliquid trading volume.

SpaceX perps launched on Hyperliquid this week. Cerebras pre-IPO did $230M volume vs Nasdaq's $30M premarket.

The regulatory framework being debated in Washington is meant to govern a market that already exists and is already growing with or without the exemption.

Tokenized stocks today are where stablecoins were in 2020 around 0.001% of their underlying market, growing exponentially.

with the regulatory framework just being drawn and institutional infrastructure being built in real time.

That comparison is the most useful frame here.

In 2020, stablecoins were growing without regulatory clarity. Banks and exchanges pushed back.

The regulatory debate took three more years.

By the time GENIUS Act passed in 2025, Tether and Circle had already built $310B in market infrastructure that regulators were now formalizing rather than creating.

Tokenized equities are following the same path.

There are currently over $34 billion in value represented by tokenized real-world assets, with approximately $1.55 billion of that consisting of tokenized equities significantly lower than the multi-trillion-dollar forecasts for tokenized asset adoption in 2030.

$1.55B today. $134T total equity market available.

The gap between those two numbers is either the opportunity or the ceiling, depending on what regulators do next.

The SEC delay isn't the end of tokenized stocks. It's the incumbents buying time while the infrastructure gets built around them.

CME and ICE tried that with Hyperliquid. Hyperliquid's at an ATH.

The playbook keeps running. The outcomes keep surprising.

https://t.co/CvjnGFLR1m just filed confidentially for a US IPO.

May 21, 2026. Draft S-1 submitted to the SEC. No share count. No price range. No timeline confirmed beyond "2026."

On paper, this should be an easy story. One of the oldest crypto companies alive. Founded in 2011.

95 million wallets. 43 million verified users across 100+ countries. $1.1 trillion in lifetime transaction volume. Adjusted profitable.

A regulatory environment in the US that's the most crypto-friendly it's ever been.

The timing should be perfect.

Except the crypto IPO class of 2026 has a problem.

BitGo went public on the NYSE in January 2026. First major crypto company to list this year. Raised $213 million.

Then dropped 36% below its IPO price within months. Still trading below where it opened.

That number 36% below IPO is what every institutional investor considering the https://t.co/CvjnGFLR1m roadshow is going to think about first.

Here's what's actually happening in the crypto IPO pipeline right now.

➝ Circle listed on NYSE. Performing. The benchmark everyone points to.

➝ Bullish (CoinDesk's parent) listed. Functioning.

➝ BitGo listed January 2026. Down 36% from IPO. The warning sign.

➝ Gemini listed. Mixed performance.

➝ https://t.co/CvjnGFLR1m confidential filing May 21. Waiting for SEC review.

➝ Kraken confidentially filed November 2025. Then paused in March when markets weakened. Still waiting.

➝ Grayscale filed for IPO. Hasn't moved forward.

➝ Consensys delayed.

➝ Ledger paused.

The pattern is clear. The window opened in late 2025 when regulatory clarity improved and BTC was pushing toward its highs.

Circle got through. Bullish got through. Then BitGo's post-IPO performance spooked the queue.

Now there are four or five companies lined up watching each other, waiting for someone else to go first and prove the market is ready.

https://t.co/CvjnGFLR1m is the most credible company in that queue.

But credible doesn't mean the window is open.

Here's the honest read on what https://t.co/CvjnGFLR1m actually is as a public company candidate.

The strengths are real. 95 million wallets is a distribution network. $1.1T in lifetime volume proves product-market fit.

Founded in 2011 means they survived the 2014 crash, the 2018 crash, the 2022 crash. That operational durability is something most crypto companies can't claim.

They run wallets, exchange, institutional trading, lending, and explorer tools a full-stack crypto infrastructure play, not just a trading venue.

The risks are also real.

➝ Last public valuation was $14 billion in 2022 at the peak. The market has repriced everything since.

The gap between that $14B mark and what institutional investors will pay in 2026 is the question nobody has answered yet publicly.

➝ Revenue transparency the confidential filing keeps financials private. Investors won't see the full picture until closer to the roadshow. If the numbers disappoint, the window closes again.

➝ Competitive pressure Coinbase is public, well-capitalized, and has COIN as a benchmark. Every institutional investor comparing https://t.co/CvjnGFLR1m will run it against Coinbase first.

➝ The BitGo effect a 36% post-IPO drop from a crypto company just months ago leaves institutional allocators cautious about how aggressively they price the next one.

Here's what the confidential filing actually means strategically.

A confidential S-1 gives https://t.co/CvjnGFLR1m the ability to go through the SEC review process which takes at minimum 2-3 months without publicly disclosing their financials until they're ready to launch a roadshow.

They can test market appetite quietly. They can adjust the timing based on what BTC does between now and Q4.

They can pull the filing entirely if conditions deteriorate without any public embarrassment.

This is the smart move. It's not a commitment. It's an option.

➝ If BTC breaks $85K-$90K in Q3, the macro backdrop for a crypto IPO improves significantly

➝ If CLARITY Act passes the Senate, regulatory clarity is locked in for a full product suite

➝ If BitGo starts recovering, the post-IPO performance narrative heals

➝ If all three happen: https://t.co/CvjnGFLR1m launches in Q4 2026 at a valuation that makes sense

If any of them don't the filing sits quietly in SEC review while the team waits for a better window.

The company isn't answering whether the IPO window is open.

It's filing the paperwork so it can answer quickly when it is.

Everyone's crediting the ETF launch for HYPE's rally.

That's not wrong. But it's not the full story.

HYPE hit $64.24 on May 24. New all-time high. Up 46% in a week. FDV briefly passed Solana's.

The narrative that landed everywhere was: "institutional ETF money arrived, HYPE mooned."

Bitwise and 21Shares launched US spot HYPE ETFs on May 12. Combined inflows hit $54M in seven days.

Eric Balchunas called it "rare to build in the first week like this." $25.5M in a single day.

Grayscale accumulated $35M in HYPE via OTC desks. The ETF story is real.

But here's what's actually driving the price mechanically.

Hyperliquid spends almost everything it earns buying HYPE back.

This isn't a discretionary decision by a team. It's written into the protocol.

The Assistance Fund Hyperliquid's treasury mechanism takes a portion of protocol revenue and continuously buys HYPE on the open market. No votes.

No board approval. No quarterly earnings call. Just continuous, automated, protocol-level buying.

➝ Hyperliquid's fee revenue in the last 7 days: higher than Solana

➝ HYPE now leads all L1 and L2 chains in weekly fee generation

➝ Every dollar of that fee revenue feeds back into HYPE demand

This means HYPE's price appreciation is partially self-referential. Higher price

→ higher FDV

→ more attention

→ more users

→ more fees

→ more buybacks

→ higher price.

That's a powerful loop when it's going up.

Here's the part worth sitting with though.

HYPE is climbing in large part because Hyperliquid spends almost everything it earns buying HYPE.

The buyback is written into the protocol, it runs continuously, and it has very little to do with whether outside investors believe in the asset.

That sentence cuts both ways.

On the way up, the buyback creates structural demand that absorbs selling pressure and amplifies any positive catalyst like an ETF launch.

The ETF inflows didn't cause the rally. They ignited a rally that the buyback mechanism then turbocharged.

On the way down, the same loop reverses. Lower price

→ lower fee revenue in dollar terms

→ smaller buybacks

→ less support

→ more selling pressure

→ lower price. The motor runs in both directions.

And here's the other thing nobody's pricing in clearly.

Hyperliquid's vertically integrated blockchain allows the platform to curate and offer products that no other decentralized exchange exists for.

Through HIP-3 markets it's offering pre-IPO perps SpaceX at $1.78T reference valuation just launched this week. Cerebras pre-IPO did $230M volume vs Nasdaq's $30M premarket.

This is a platform expanding into territory traditional exchanges have never touched.

That expansion is what Bitwise CIO Matt Hougan means when he compares Hyperliquid to Robinhood and CME rather than other DeFi tokens.

Not the price. The product category.

➝ Robinhood: democratized access to financial markets for retail

➝ CME: the infrastructure layer for institutional derivatives

➝ Hyperliquid: both, on-chain, 24/7, permissionless, with a buyback engine underneath

Van de Poppe said European traders have increasingly moved to Hyperliquid because perpetual futures trading remains difficult to access on many regulated venues in Europe.

That's not a crypto narrative. That's a regulatory arbitrage play with real user behavior behind it.

So what's the honest read at $63?

The fundamental case is genuinely strong. $1B+ projected revenue.

Leading fee generation across all chains. Pre-IPO and tokenized asset markets nobody else is offering.

Protocol-level buyback creating structural demand. CME and ICE scared enough to lobby regulators against it.

The risk is equally real.

At $15B FDV having just passed Solana the buyback loop that built this rally is the same mechanism that amplifies a drawdown.

If fee revenue drops 20%, buyback support drops 20%, and the institutional ETF money that arrived in week one is also the most likely to exit in week one of a reversal.

The ETF launch gave HYPE legitimacy. The buyback gave it momentum. The product roadmap gives it a thesis.

All three need to keep compounding for $100 to make sense.

Right now, they are. That's why it's at $63.