Palantir $PLTR may be one of the most difficult stocks in the market to analyse because both sides have a point.

The business performance is exceptional. In Q1 2026, revenue grew 85% to $1.633B, U.S. revenue grew 104%, adjusted operating margin reached 60%, and adjusted free cash flow came in at $925M. Management also raised full-year revenue guidance to roughly $7.65B–$7.66B, implying about 71% growth for FY2026.

Those are not normal software numbers.

The U.S. commercial business is the part that stands out most. Revenue there grew 133% year-on-year, suggesting Palantir is no longer just a government contractor with a good story. It is increasingly being adopted by companies trying to turn AI from demos into actual operating systems for decision-making, logistics, manufacturing, defence, healthcare and finance.

The balance sheet is also strong. This is not a speculative cash-burning AI name. Palantir is generating very high free cash flow, raising guidance, and operating with software-like margins. Institutional ownership has also become meaningful, with major holders including BlackRock, Vanguard and State Street.

But valuation is the problem.

At around $132 per share, Palantir is valued at roughly $340B. That puts it on an extremely demanding multiple. Analysts are divided: some targets sit far above the current price, while the lowest targets remain dramatically below it. That tells you the market is not debating whether Palantir is a quality business. It is debating how much future dominance investors should pay for today.

For me, Palantir is not a simple “overvalued AI stock” and it is not a simple “buy at any price” compounder either.

It is a rare company with extraordinary growth, margins and strategic relevance, but the current valuation leaves very little room for disappointment.

The key question is whether Palantir becomes a normal enterprise software company, or whether it becomes one of the core operating layers for AI across governments and large businesses.

If it becomes the latter, the valuation may eventually make more sense.

If growth slows before that dominance is obvious, the stock could be punished hard.

That is what makes $PLTR so interesting.

It may be expensive for a software company.

But possibly not expensive enough if it really becomes infrastructure.

#Palantir #PLTR #AI #Stocks #WeeStocks

A lot of people are asking why markets suddenly became nervous.

The answer is probably not one thing. It’s several things hitting at the same time.

For months, AI optimism helped push valuations higher and higher. Then a stronger-than-expected jobs report arrived, Treasury yields jumped, and investors started questioning whether interest rates might stay higher for longer. (Reuters)

At the same time, oil prices have been reacting to Middle East tensions, adding another layer of inflation risk. Higher oil prices make it harder for central banks to cut rates and harder for investors to justify paying extreme multiples for growth stocks. (The Guardian)

What we’re seeing now looks less like a financial crisis and more like a market asking an uncomfortable question:

“How much future growth has already been priced in?”

That’s why many of the stocks that led the rally are also leading the pullback. When positioning becomes crowded, the exit door suddenly feels very small.

The interesting thing is that the long-term AI thesis hasn’t changed much in a week.

What changed is the price investors were willing to pay for it.

Sometimes markets don’t correct because the story changes.

They correct because expectations got ahead of reality.

If you’ve been investing for a while, you’ve probably seen this pattern before. Excitement pushes prices higher, confidence builds, and eventually investors pause to reassess what they’re actually paying for future growth. That doesn’t mean the opportunity disappears—it just means the market is recalibrating.

The bigger question now is whether this is just a healthy reset or the start of a deeper repricing. What do you think?

#Stocks #Investing #AI #Nasdaq #WeeStocks

Something I’ve always found strange in investing is that people can spend weeks researching a company, reading quarterly reports, studying the competition, listening to earnings calls and building a thesis… and then sell simply because the position is showing a large profit.

Imagine buying a stock because you believe revenue can double over the next five years, margins will expand, analyst targets are rising and management is executing well.

Six months later you’re up $20,000.

What has actually changed?

Has revenue growth slowed?

Have future earnings estimates been cut?

Has management reduced guidance?

Has a competitor emerged with a better product?

Have analysts started lowering targets?

Or are you simply looking at a larger number on the screen than you’ve ever seen before?

The stock doesn’t know whether you’re up $2,000 or $200,000. The business is still doing exactly what it was doing yesterday.

Some of the greatest investments in history looked expensive after a 100% gain. Many looked even more expensive after a 300% gain. Investors who sold purely because the profit felt large often watched from the sidelines as the company continued executing and the valuation continued climbing.

Of course there are times to sell. Valuations become stretched. Growth slows. Management disappoints. Better opportunities appear elsewhere.

But I suspect many investors spend too much time watching their profit and not enough time monitoring the variables that actually determine future value.

So it isn’t how much money you’ve made.

BUT whether the reasons you bought the company still exist.

#Stocks #Investing #Compounding #Wealth #WeeStocks

Imagine you could travel back to 2010 and buy Amazon.

Would you?

Most people instantly say yes.

I’m not so sure.

To earn the life-changing returns, you wouldn’t just need to buy Amazon.

You’d need to sit through years of volatility, analyst criticism, market crashes, recessions, missed expectations and endless headlines claiming the stock was overvalued.

The hardest part of investing… it is not just finding great companies….

It’s having the conviction to hold them when everybody else is telling you that you’re wrong.

Looking backwards, great investments look obvious.

Living through them and experiencing all the fun is a completely different experience.

$AMZN $NVDA $MSFT $AAPL

#Stocks #Investing #WeeStocks

The AI trade finally stumbled.

Chip stocks sold off. AI names were hit hard. Investors suddenly started worrying about valuations, interest rates and whether AI spending has gone too far.

What fascinates me is that the companies themselves seem to be sending the exact opposite message.

Alphabet just raised around $80 billion.

Meta is reportedly considering a huge capital raise of its own.

Anthropic has filed for an IPO.

SpaceX is about to come to market.

If the people building AI thought the opportunity was peaking, this would be a very strange time to be raising record amounts of capital.

Instead, it looks like they’re doing the opposite.

They’re trying to secure as much money as possible while they still can.

The market appears to be asking whether AI spending has gone too far.

The companies spending the money appear to be asking whether they’re spending enough.

One of those groups is going to be very wrong.

$NVDA $META $GOOGL $MSFT $AMZN

#Stocks #Investing #AI

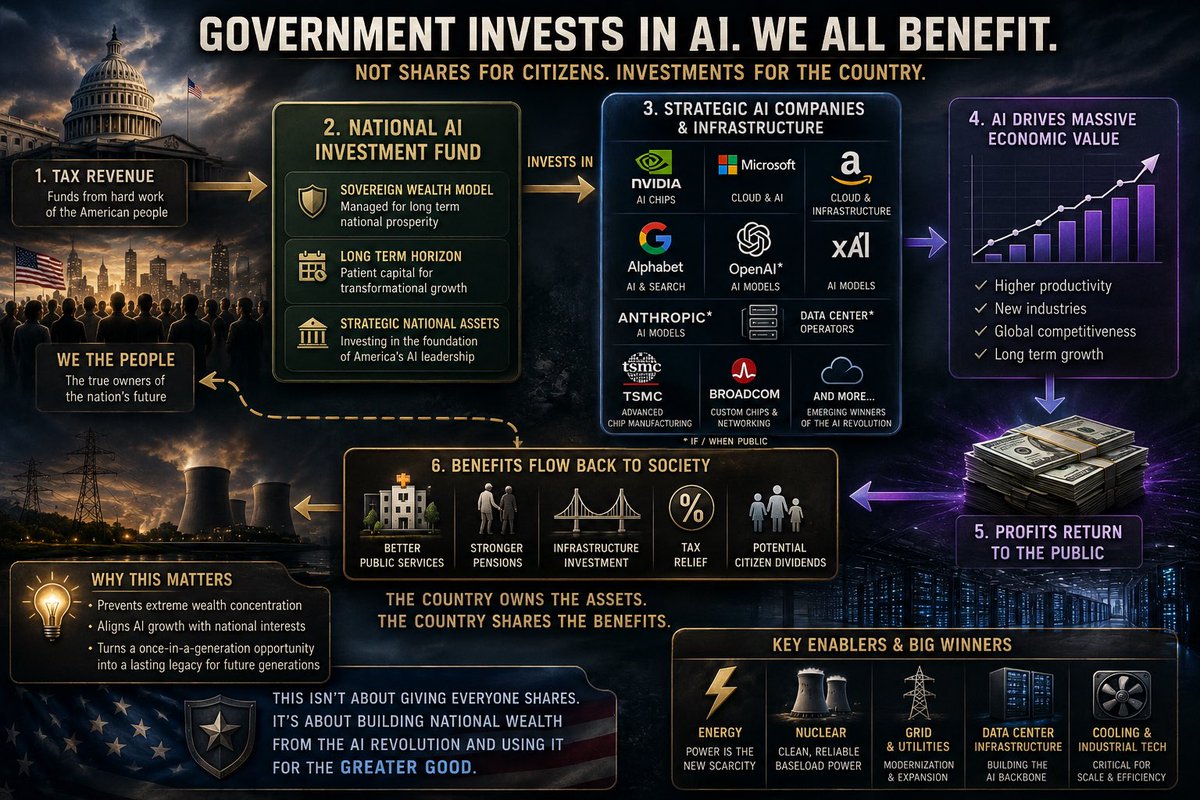

President Trump’s reported comments about exploring AI ownership for Americans sparked a lot of discussion, but I suspect many people are interpreting it the wrong way.

The first assumption is that citizens would somehow receive shares in AI companies directly. That sounds attractive politically, but it would be extremely difficult to implement in practice. A far more realistic outcome would be governments investing in strategic AI assets on behalf of the public, much like sovereign wealth funds have invested in oil, gas, infrastructure, and other national resources.

The comparison that immediately comes to mind is Norway. Norwegians don’t individually own pieces of oil fields, yet the country’s oil wealth has been accumulated through public investment and ultimately benefits society through government spending, pensions, and long-term financial stability. If AI becomes as economically important as many expect, policymakers may begin viewing it in a similar way.

That possibility raises an interesting question for investors. If governments decide that certain AI companies are strategically important to national competitiveness, which businesses would be viewed as essential infrastructure rather than simply private technology firms? NVIDIA would likely be near the top of the list because it supplies the chips powering much of today’s AI boom. Microsoft, Amazon, Alphabet and perhaps future public companies such as OpenAI or Anthropic could also find themselves in that category because they control the cloud and computing platforms on which AI increasingly depends.

What’s even more interesting is that the biggest beneficiaries might not be AI companies at all. Every major AI announcement seems to be followed by another discussion about power shortages, data-centre construction, and electricity demand. If governments begin investing around AI as a national priority, energy producers, grid operators, nuclear developers, and data-centre infrastructure companies could become just as important as the model builders themselves.

The broader debate is really about where AI-generated wealth ends up. If a small number of corporations capture most of the value, wealth concentration accelerates. If governments own meaningful stakes in the infrastructure underpinning AI, some of those gains could potentially flow back into public services, pensions, lower taxes, or entirely new forms of citizen benefit. We may be watching the early stages of a discussion that has less to do with technology and more to do with how societies choose to distribute the economic value created by increasingly intelligent machines.

SpaceX has reportedly set its IPO price at $135 per share, implying a valuation of roughly $1.75 trillion.

So here’s what I don’t understand.

IG’s spread betting market has recently been trading around a $2.2 trillion implied valuation.

If you can potentially buy the actual IPO at a $1.75 trillion valuation, why would you pay up for a $2.2 trillion valuation today?

The only answer is that traders believe the stock will surge immediately after listing.

In other words, they’re not betting on the IPO.

They’re betting on the pop.

That might happen. Demand appears extremely strong.

But it also means you’re no longer asking whether SpaceX is a great company.

You’re asking whether it’s worth hundreds of billions more than the IPO valuation before public investors have even seen a full quarter of trading.

That’s a very different question.

For me, that’s where the speculation starts to outweigh the investment case.

At a $1.75 trillion valuation, investors can at least anchor their expectations to the IPO pricing.

At $2.2 trillion, you’re effectively assuming that the market has already underpriced one of the most anticipated listings in history.

That’s possible.

But it’s a much tougher bet than simply believing SpaceX will be a successful public company.

Maybe the real takeaway isn’t whether SpaceX is overpriced or underpriced.

It’s that investors are already pricing in a near-perfect debut.

And when expectations get that high, the biggest risk isn’t the company.

It’s the gap between what everyone expects and what actually happens.

#SpaceX #IPO #Stocks #Investing

@RoundtableSpace As they say, the market is never wrong. But this is small volume, so don’t panic. Let’s watch next week and let the pullback develop. Then we can judge it more fairly.

Don’t panic!

Probably quantum computing.

AI is already running into limits around compute, energy and cost. Quantum won’t replace AI, but it could become the technology that unlocks the next major leap forward.

Many Wall Street analysts remain bullish on the space despite the risks. Some analyst price targets imply 50% to 200%+ upside for select quantum computing stocks over the next few years, driven by expectations of increasing commercial adoption, government contracts, and continued advances in quantum hardware and software.

That’s why investors are watching names like $IONQ, $RGTI, $QBTS and $QUBT so closely. The sector is still highly speculative, but analysts continue to publish targets that suggest significant upside if the technology delivers.

The biggest winners of the AI boom were often the companies supplying the tools. NVIDIA sold the picks and shovels.

Quantum could end up being the next set of picks and shovels.