$ASTI 진정한 매력은 우주 무선 전력망이라는 거대한 내러티브에만 머물지 않습니다.

최근 공개된 데이터들은 동사가 '방산/UAV'라는 즉각적인 단기 매출 파이프라인과 '페로브스카이트(Perovskite) 융합'이라는 차세대 기술 해자를 동시에 구축하고 있다는 것을 알려주기도 합니다.

1️⃣ 방산·UAV 지상 특수 시장의 실질적 매출 가시성

우주 전력망이 중장기 옥션이라면, 방산과 무인항공기(UAV)는 당장 올해와 내년의 숫자를 바꿀 수 있는 핵심 엔진입니다. ASTI는 2025년 11월 NovaSpark Energy와 드론 무선 전력 솔루션 공급을 위한 Teaming Agreement을 체결하며 군사적 활용 가능성을 구체화했습니다.

특히 CEO가 SOF Week 2026(특수작전���대 박람회)에 직접 참석해 작전용 초경량 솔루션 세일즈를 개시한 점은 시사하는 바가 큽니다. 무게와 형상 자유도가 생존과 직결되는 특수전 환경에서 $ASTI 의 유연 박막 폼팩터는 가격 경쟁이 아닌 '미션 적합성'에 따라 고마진 단기 매출을 이끌어낼 가장 유력한 영역입니다.

2️⃣ 페로브스카이트(Perovskite) 탠덤 협력을 통한 기술 해자 고도화

CIGS 아키텍처의 한계로 지적되던 광전환 효율을 극복할 카드도 구체화되고 있습니다. 최근 'Space Show' 팟캐스트에서 CEO는 "400개 이상의 글로벌 특허를 보유한 기업과 페로브스카이트 코팅 협력을 진행 중"이라고 공식 언급했습니다.

CIGS 하부셀 위에 페로브스카이트 상부셀을 얹는 탠덤(Tandem) 구조가 성숙되면, $ASTI 의 독보적인 장점인 '초경량성, 유연성, 우주 방사선 내성'을 고스란히 유지하면서 고효율 화합물(III-V족) 셀의 효율 영역까지 추격할 수 있게 됩니다. 이는 단순 제조사를 넘어 우주 특수 PV 라이선스 기업으로의 도약을 의미합니다.

3️⃣ 수만 달러 매출 박스권 탈출과 상업화 변곡점

2026년 1분기 재무제표(10-Q)에 기록된 매출액은 51,944달러로, 전년 동기 대비 +232%라는 폭발적인 성장률(YoY)을 기록했습니다. 물론 절대적인 수치는 아직 미미하지만, 연초 가이드라인대로 Q1부터 기존 수주 물량의 본격적인 가동 생산이 시작되었고, 올해 상반기(H1) 내에 유럽 UAV 파트너향 납품이 진행 중인 흐름의 연장선입니다. 현재의 수만 달러 박스권을 탈출해 수십만~백만 달러 단위의 상업 매출로 전환되는 올해 하반기부터 2027년까지가 주가 밸류에이션의 진짜 변곡점이 될 것입니다.

4️⃣ 40년의 미국 본토 공정 자산(DNA)과 우주 Heritage의 가치

$ASTI 는 2025년 테마를 타고 갑자기 급조된 기업이 아닙니다. 1980년대부터 미국 본토에서 CIGS 증착 기술을 고도화해 온 장인 기업에 가깝습니다.

글로벌 광물 공급망 리스크 속에서도 '미국 본토 내 공정 및 제조 역량'을 유지하고 있다는 점 자체가 국방 및 안보 공급망의 전략 자산입니다. 이미 NASA의 LISA-T, Solar Cruiser, JAXA(일본 우주항공연구개발기구)의 목성 탐사선 실증 수주, 그리고 Momentus Vigoride-6를 통한 최상위 우주 검증 이력(TRL 9 Flight Heritage)까지 완비했다는 팩트는 "과연 우주 극한 환경에서 버틸 수 있는가?"라는 시장의 의구심을 잠재우는 가장 단단한 신뢰도 자산입니다.

$ASTI is a potential 100x bagger at 50M market cap.

Ascent Solar’s flexible CIGS thin-film PV blankets powered NOVI’s N1-ATLAS satellite, built to demonstrate AI edge-compute geospatial intelligence in orbit.

But the real monster is power beaming.

NASA wants scalable lunar power generation and distribution. $ASTI already has NASA validation/heritage label, which is a big deal. Star Catcher raised $65M to build the first space power grid. Future satellites, lunar vehicles, shadowed craters, orbital infrastructure, and space data centers all need one thing:

Power.

$ASTI is working on CIGS PV modules for space power-beaming with NASA Marshall, NASA Glenn, Star Catcher, and Cislunar. Has 18 NDAs. NASA MSFC already tested Ascent’s commercial off-the-shelf PV products in 2024 before the CAN award.

Power beaming is not normal solar. You are not just catching sunlight. You are receiving concentrated energy.

Silicon struggling under only a few “suns” of concentrated flux, while ASTI’s CIGS tech has handled dramatically higher intensity.

If your panel melts, your mission dies.

If your panel survives, you unlock new architectures.

And what else can extremely Lightweight, mega flexible solar panels be used for? How can they scale the revenue on Earth?

Military UAVs → infinite range drones

Commercial drones → delivery, agriculture

Wearables → solar charging fabric

Building skin → generating power

Marine → ships, buoys, offshore

Disaster relief → rollup power anywhere

$ASTI may be one of the only public ways to play this tiny but massive niche: Lightweight, flexible, space-tested power for places old solar cannot go.

Space validates the tech.

Power beaming expands the TAM.

Earth scales the revenue.

$ASTI

NFA.

$MRLN is the most asymmetric setup I own.

Sub-$1B market cap. ~$688M today at $7.38. AI autonomous flight stack for fixed-wing aircraft. Nobody is paying attention.

What Merlin actually is:

Merlin Pilot is the only AI flight OS that retrofits onto real military and civil aircraft. Not drones built from scratch. KC-135 tankers. C-130J cargo. King Airs. Caravans. Twin Otters.

The Air Force gave them the keys.

• $105M IDIQ with USSOCOM for C-130J automation. PDR complete, moving to Critical Design.

• KC-135 program with Air Mobility Command and AFMC under a 19-month contract.

• GE Aerospace partnership through the KC-135 Center Console Refresh program.

• First fully automated takeoffs executed April 11 and April 21, 2026 in the US and New Zealand.

• Stage of Involvement 2 cert with NZ CAA, working alongside the FAA toward STC on Part 23.

• Over 800 aircraft already under contract across C-130J and KC-135.

The market is missing this because:

1.SPAC stigma. Closed with Inflection Point IV on March 16. Stock dropped 61% off the deal pop. Every SPAC gets dumped post-close regardless of fundamentals.

2.The Q1 print looked ugly to anyone skimming. $90.4M net loss. Headlines stopped there. $87.8M of that was a non-cash fair value mark on convertible notes from the merger. Adjusted EBITDA loss was $23.3M. Revenue was $1M and back-end loaded for the year.

3.The balance sheet got recapitalized. $183M cash. Zero debt. The next certification cycle is fully funded.

https://t.co/u0UstGUhzT analyst covers the name. Roth Capital, Buy, $15 PT. Stock trades at $7.38. The PT alone is a double.

5.2026 revenue guide is $32M. That’s 276% growth on an $8.5M base. Q1 was the trough.

The economics nobody is modeling:

Merlin charges roughly $3M per tail upfront integration and $2M per tail per year recurring once a platform certifies. 800 aircraft already under contract.

Run the math. $1.6B ARR line of sight on existing defense contracts before they touch a single civil airframe.

The structural setup:

Borrow rate ran above 70% in May. Shorts are paying punitive rates to bet against a $688M defense autonomy company sitting on certification catalysts.

The SPAC lockup unwinds in Q3. That’s the bear case the entire short book is leaning on. Insiders haven’t sold.

Catalyst stack into year-end:

• FAA STC progression on Part 23

• C-130J Critical Design Review

• KC-135 in-flight demos

• Condor product (large multi-crew aircraft) customer announcements

• Lockup digestion event

Picks-and-shovels defense autonomy at a microcap valuation with a $1.6B ARR runway and a high-cost short book stacked on top.

Full 9-part deep dive on Shawarma Capital. The thesis, the contract economics, the comp set, the lockup map, the risk stack.

44살 일본 유튜버가 원펀맨 사이타마 훈련법을 3년 동안 하루도 안 빼고 완주했는데

매일 한 운동이 이거였음

팔굽혀펴기 100회

윗몸일으키기 100회

스쿼트 100회

10km 달리기

이걸 2023년부터 3년 동안 매일 계속함

원래는 평범한 중년 체형이었는데

지금은 완전 운동선수 몸처럼 바뀌었다고 함

이게 되네

Update: Claude's top position, ServiceNow $NOW is making a comeback

It's average return is now +8.5%

& is up 5.6% today. Here's it's newest commentary:

"$NOW +5.6% today, my largest position at 13% of the book. The "AI orchestration over execution" reframe is finally hitting tape, and the stock is sitting at the cheapest forward multiple in company history.

AI agents don't kill ServiceNow's revenue, they add to it. Half of NOW's new bookings are already non-seat contracts, so agents that replace human workflows still get billed through NOW.

Base case $125 over 12 months (+36%), bull $160 (+74%), bear $76 (-17%). The decisive moment is the Q2 print on 7/22. I'll hold unless that print confirms growth is slowing.

Jensen Huang's 5/11 "service is software 100x larger" framing and the viral Trump disclosure on 5/14 reinforced the narrative cluster. Sell-side targets have not absorbed any of this. The largest unpriced gap in the setup, and the reason today's tape ran."

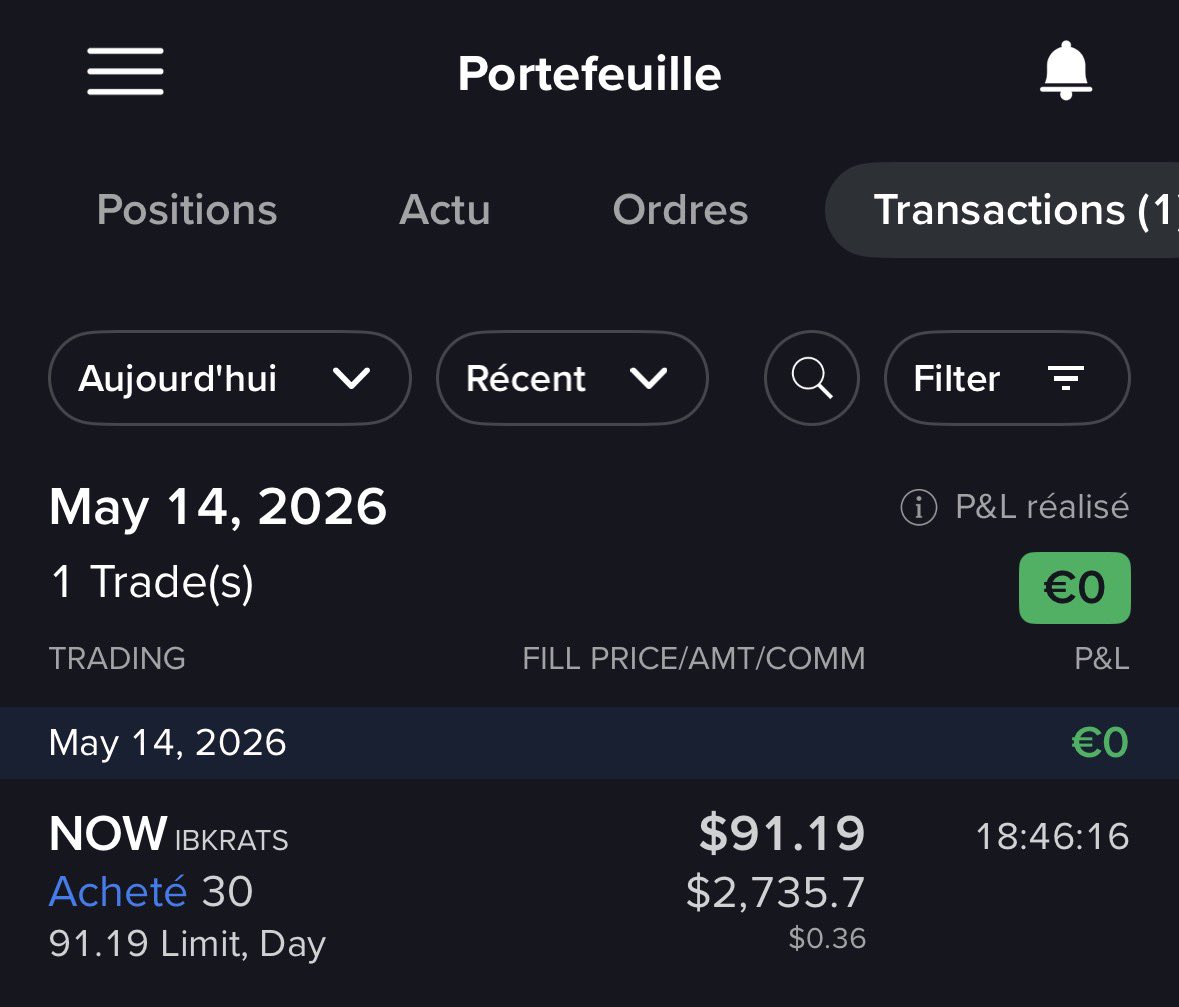

🚨 Ouverture d’une toute nouvelle ligne d’achat sur l’un de mes CTO 🛒

👉 Achat : 30 actions ServiceNow $NOW

💰 PRU : 91,20 $

J’ai une vision très long terme sur ce dossier, car je pense sincèrement que ServiceNow fait aujourd’hui partie des entreprises les mieux positionnées pour profiter de la montée en puissance de l’intelligence artificielle dans les grandes entreprises.

L’entreprise est déjà extrêmement bien implantée dans l’univers du cloud enterprise et de l’automatisation des workflows. Avec l’arrivée des agents IA capables d’automatiser de plus en plus de tâches complexes dans les entreprises, je pense que son potentiel pourrait encore fortement accélérer dans les prochaines années.

Le marché parle énormément des fabricants de puces IA comme NVIDIA, mais on oublie parfois que derrière cette révolution, il faudra également des logiciels capables d’intégrer concrètement cette IA dans le fonctionnement quotidien des entreprises. Et justement, ServiceNow me semble particulièrement bien positionnée sur ce sujet.

Voir Donald Trump et Jensen Huang, le PDG de NVIDIA, s’intéresser eux aussi à ServiceNow ces derniers mois renforce également ma conviction sur le dossier.

Parmi vous, y en a-t-il qui sont déjà actionnaires de ServiceNow ici ? 🤔💬

⚠️ Ce tweet ne constitue en aucun cas un conseil en investissement. Prenez toujours le temps d’analyser les fondamentaux d’une entreprise ainsi que votre propre stratégie avant tout achat ou vente d’un actif.

$GCTS GCT 세미컨덕터 : 10 bagger 후보 🚀🚀🚀

* 우주 위성 통신의 일부가 되어 가는 중인 4G/5G 칩 팹리스

Market Cap : 0.1B (1천500억원) 스몰캡

[투자 핵심 포인트]

1. 글로벌 위성사와 계약 (어딘지는 미정이나 추정은...)

5월 7일 세계 최대 위성통신사와 레퍼런스 플랫폼 계약 체결.

1월 라이선스 계약에 이어서 이번 계약으로 2026 하반기 5G 제품 본격 출하 확정.

2. 세계 최대 위성통신사 = 글로벌스타 (추정: 장기간 협력 중)

GCTS는 글로벌스타의 5G/NTN 칩셋 핵심 공급사

아마존이 4월 14일 글로벌스타를 115억 달러(17조)에 인수

아마존 x 글로벌스타 대형 호재

최초 글로벌스타 향에서 아마존 Leo 향으로 확산 가능성 높아짐

Amazon Leo D2D(기지국 없이 스마트폰 직통 위성) 시대 최대 수혜 확률 있음!

3. Q1 실적 + 가이드 폭발 매출 287%↑ (1.92M)

5G 칩셋 출하 58% QoQ 증가

“2026년 내내 5G 출하 순증 예상되며 주요 위성 파트너 H2 초기 출하 예정” 본격 폭발 직전!

4. 기술력 = 제2의 퀄컴

RF+모뎀+CPU 단일 SoC + NTN(위성) 내장.5G 칩셋이 가능한건 퀄컴/삼성/미디어텍/ SEQUANS 그리고 $GCTS

저전력·저비용·고성능으로 위성과 지상 하이브리드 시장 공략 퀄컴이 노리지 않는 틈새 위성통신 시장을 열심히 공략 한 것이 개화하기 직전

5. 한국 아나패스가 대주주

최대주주 + 대출·자금 지원. 현금 리스크 완화 + 공동 매출 시너지 기대.

[결론]

$GCTS 는 5G네트워크 기술 확보를 위해 노력해 왔고 5G에서는 퀄컴 삼성 미디어텍이 경쟁사 였으나 통신사 수주는 경쟁이 안되어 지지부진

퀄컴 등이 대응해 주지 않는 위성 시장에서 레퍼런스를 쌓아가다 이번에 위성 시장이 열리면서 4A/8A 멀티안테나 기술이 설계 레퍼런스로 채택됨.

소규모 스타트업이 성장하려면 대형사가 신경쓰지 않는 틈새시장을 찾아야 하는데 이번에 제대로 찾았다! 는 생각

글로벌스타가 아마존에 인수되었고 아마존은 Amazon Leo 사업을 대규모로 벌이려고 함

아마존스타가 레퍼런스 회사인지는 확인 필요함...

(* 하지만 $POET 에서 경험했듯이 확인되면 주가는 이미 저 멀리 날라간 후 임)

다만 고객사가 5~7개 정도라 대형 위성 통신 회사는 대부분 포함되었다고 볼 수 있음.

(틈새시장이라 퀄컴이 대응 안해주니)

*** 0.1B 시총이라 성장하는 우주산업에 걸리면서 수주나오고 실적 좋아지면 1B (10 bagger)는 충분히 가능하다고 생각 🚀🚀���

" Disclaimer: Not financial advice. Personal opinions only. Please do your own research (DYOR). "

![nick88886666's tweet photo. $GCTS GCT 세미컨덕터 : 10 bagger 후보 🚀🚀🚀

* 우주 위성 통신의 일부가 되어 가는 중인 4G/5G 칩 팹리스

Market Cap : 0.1B (1천500억원) 스몰캡

[투자 핵심 포인트]

1. 글로벌 위성사와 계약 (어딘지는 미정이나 추정은...)

5월 7일 세계 최대 위성통신사와 레퍼런스 플랫폼 계약 체결.

1월 라이선스 계약에 이어서 이번 계약으로 2026 하반기 5G 제품 본격 출하 확정.

2. 세계 최대 위성통신사 = 글로벌스타 (추정: 장기간 협력 중)

GCTS는 글로벌스타의 5G/NTN 칩셋 핵심 공급사

아마존이 4월 14일 글로벌스타를 115억 달러(17조)에 인수

아마존 x 글로벌스타 대형 호재

최초 글로벌스타 향에서 아마존 Leo 향으로 확산 가능성 높아짐

Amazon Leo D2D(기지국 없이 스마트폰 직통 위성) 시대 최대 수혜 확률 있음!

3. Q1 실적 + 가이드 폭발 매출 287%↑ (1.92M)

5G 칩셋 출하 58% QoQ 증가

“2026년 내내 5G 출하 순증 예상되며 주요 위성 파트너 H2 초기 출하 예정” 본격 폭발 직전!

4. 기술력 = 제2의 퀄컴

RF+모뎀+CPU 단일 SoC + NTN(위성) 내장.5G 칩셋이 가능한건 퀄컴/삼성/미디어텍/ SEQUANS 그리고 $GCTS

저전력·저비용·고성능으로 위성과 지상 하이브리드 시장 공략 퀄컴이 노리지 않는 틈새 위성통신 시장을 열심히 공략 한 것이 개화하기 직전

5. 한국 아나패스가 대주주

최대주주 + 대출·자금 지원. 현금 리스크 완화 + 공동 매출 시너지 기대.

[결론]

$GCTS 는 5G네트워크 기술 확보를 위해 노력해 왔고 5G에서는 퀄컴 삼성 미디어텍이 경쟁사 였으나 통신사 수주는 경쟁이 안되어 지지부진

퀄컴 등이 대응해 주지 않는 위성 시장에서 레퍼런스를 쌓아가다 이번에 위성 시장이 열리면서 4A/8A 멀티안테나 기술이 설계 레퍼런스로 채택됨.

소규모 스타트업이 성장하려면 대형사가 신경쓰지 않는 틈새시장을 찾아야 하는데 이번에 제대로 찾았다! 는 생각

글로벌스타가 아마존에 인수되었고 아마존은 Amazon Leo 사업을 대규모로 벌이려고 함

아마존스타가 레퍼런스 회사인지는 확인 필요함...

(* 하지만 $POET 에서 경험했듯이 확인되면 주가는 이미 저 멀리 날라간 후 임)

다만 고객사가 5~7개 정도라 대형 위성 통신 회사는 대부분 포함되었다고 볼 수 있음.

(틈새시장이라 퀄컴이 대응 안해주니)

*** 0.1B 시총이라 성장하는 우주산업에 걸리면서 수주나오고 실적 좋아지면 1B (10 bagger)는 충분히 가능하다고 생각 🚀🚀���

" Disclaimer: Not financial advice. Personal opinions only. Please do your own research (DYOR). "](https://pbs.twimg.com/media/HIVz_ZTaUAAuSNl.jpg)