A sharp divergence between near-term funding markets and the interest rate swap curve defined Australian fixed income through the week to 29 May 2026. Rather than moving in concert, BBSW rates held their ground or edged marginally higher while swap rates retreated across every tenor — most decisively in the belly of the curve — pointing to a meaningful reassessment of medium-term rate expectations in the wake of sustained upward pressure over recent months.

Read more - https://t.co/zmDIvbQHG8

#BankBillSwaps #InterestRates #FixedIncome #AustralianMarkets #YieldReport #BBSW #MonetaryPolicy #IncomeInvesting

The ASX hybrid market navigated the week ending 29 May 2026 with a mixed but measured tone across both the standard and non-standard segments, as investor focus on income generation kept underlying demand intact despite a somewhat more active price tape.

Yield hierarchy continued to define the landscape. In the non-standard space, Nufarm (NFNG) held its place as the top-yielding instrument at 10.53%, ahead of Ramsay Health Care (RHCPA) at 9.13%. The standard cohort was led once again by Judo Capital (JDOPA) at 9.69%, with Latitude (LFSPA) close at 9.18% and Macquarie Bank Capital Notes 2 (MBLPC) at 8.96% all commanding a meaningful premium over the tightly priced major bank names and continuing to appeal to yield-seeking allocators.

Price action across the standard segment was decidedly more dispersed than the prior week. The standout mover was Macquarie Group Capital Notes 4 (MQGPD), which surged +6.22% likely reflecting a technical or call-related re-pricing given its proximity to maturity. Elsewhere, CBA PERLS 12 (CBAPI) rose +0.73% and CBA PERLS 13 (CBAPJ) added +0.67%, while on the downside, Latitude (LFSPA) pulled back –1.14%, MBLPC slipped –0.97%, and Judo Capital (JDOPA) eased –0.91%. In the non-standard segment, NFNG retreated –0.30% while RHCPA was essentially flat at +0.01%.

Read more - https://t.co/b6Jby9KFxC

#WeeklyHybrids #ASXHybrids #FixedIncome #YieldSpreads #IncomeInvesting #AustralianMarkets #HybridSecurities #YieldReport

Weekly Cash Rate Update -

Australian interest rate market pricing has eased more decisively over the week to 29 May 2026, with the 29 May curve sitting visibly below both the 22-May and 15-May profiles across the forward horizon. The step-down is progressive and modest at the front end but increasingly pronounced through the middle and longer tenors, marking a clearer dovish shift compared to the consolidation observed in prior weeks. This repricing suggests markets are reassessing the likelihood of further tightening following the RBA’s May decision to lift the cash rate by 25 basis points to 4.35%.

Read more - https://t.co/8GHIKV7JHn

#WeeklyCashReport #RBACashRate #InterestRateOutlook #AustralianMarkets #SavingsAccounts #FixedIncome #MonetaryPolicy #YieldReport

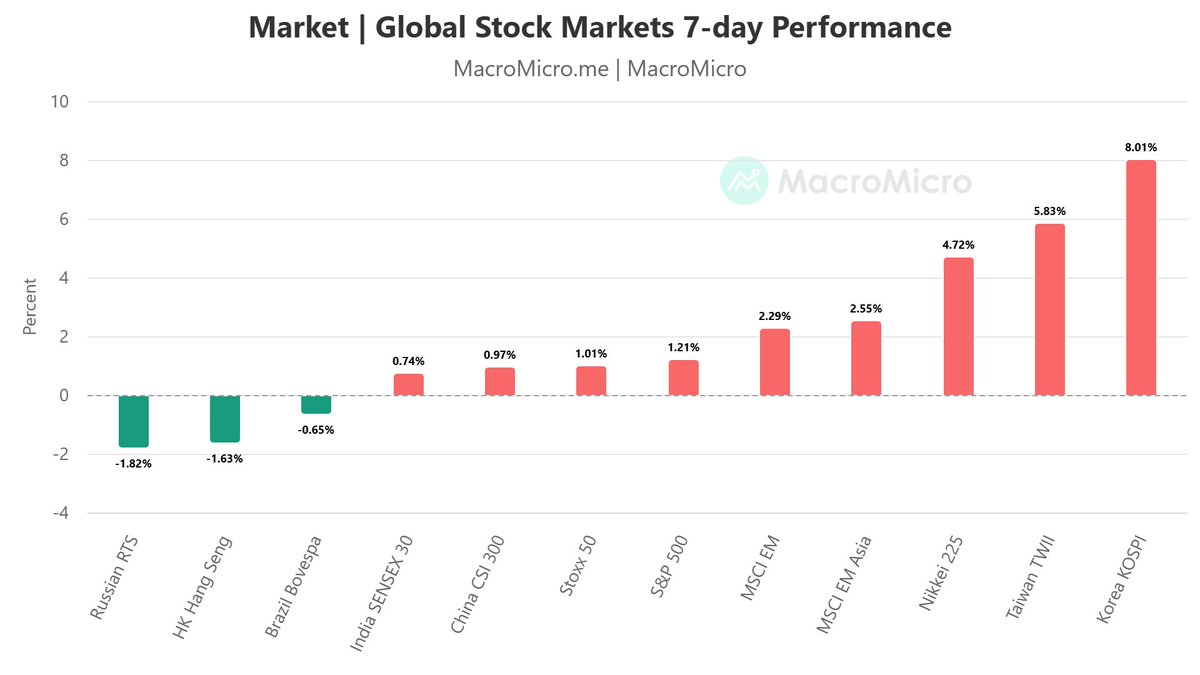

Chart of the Week –Cyclical Upswing – Global Earnings and Manufacturing Cycle

Despite heightened geopolitical tensions and market volatility, the outlook for equities remains constructive. While risks warrant close monitoring, periods of uncertainty often create investment opportunities. Two key factors support this view. First, economic and corporate fundamentals remain strong. Taiwan’s export growth and strong commentary from TSMC reinforce the view that the global manufacturing cycle continues to improve, driven largely by the accelerating adoption of AI technologies. Second, earnings expectations across global markets continue to be revised upward, particularly within technology and AI-related sectors. Although some valuation measures appear stretched, price-to-earnings ratios remain reasonable, with AI beneficiaries such as Taiwan, South Korea, Japan and the US experiencing justified structural re-ratings supported by robust earnings growth.

#EquityOutlook #GlobalMarkets #AIAdoption #TechEarnings #MarketOpportunities #TSMC #TaiwanExports #StructuralReRating #InvestingInsights #GeopoliticsAndMarkets

Markets rotated back toward energy and commodities, while tech momentum cooled. Energy ETFs led gains — BetaShares Crude Oil (OOO) surged 10.1%, with strong moves in space (RCKT +8.9%) and cybersecurity (HACK +6.2%). Clean energy and hydrogen exposures also rebounded. Tech themes stayed constructive — China Tech (DRGN +3.9%) and semiconductors (SEMI) held firm — but precious metals weakened, with gold ETFs down 4–6% and uranium (ATOM –8.2%) under pressure.

Read more: YieldReport Weekly ETFs https://t.co/xKjFJI85At

#ETFs #EnergyMarkets #TechnologyThemes #CleanEnergy #YieldReport

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

Australian government bond yields eased modestly at the shorter end of the curve on May 27, following April CPI data that printed below expectations. The 2-year yield fell two basis points to 4.57 percent and the 5-year declined two basis points to 4.57 percent, while the 10-year was little changed at 4.91 percent and the 15-year edged one basis point higher to 5.12 percent. The slight bull flattening at the front end reflects a repricing of near-term RBA rate hike risk, though the long end remains anchored at elevated levels given persistent underlying inflation and the global bond yield environment.

https://t.co/vIkqgA0h0W

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

https://t.co/BETV8CPY7w

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank#asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights#TermDeposits #InterestRates#BankingInsights #AustralianBanks #FinancialMarkets

Weekly overview of Bank Bill Swap Rates

A pronounced divergence characterised Australian short-term and fixed income markets through the week to 22 May 2026, with front-end bank bill rates continuing their measured ascent while the interest rate swap curve pulled back uniformly across all tenors. Rather than a synchronised directional impulse, the period was defined by a split: near-term funding rates grinding higher under the weight of a restrictive policy setting, while swap markets re-priced lower most sharply at the belly, pointing to a reassessment of medium-term rate expectations following recent upward momentum.

Read more - https://t.co/XTR45mpqWi

#YieldReport #BankBillSwaps #FixedIncome #AustralianMarkets #InterestRates

The Minutes Speak Louder: Fed’s Hawkish Undercurrent Runs Deeper Than the Votes

The Federal Reserve released the minutes of its April 28–29 FOMC meeting on 20 May, offering the most detailed window yet into deliberations behind a decision that was anything but routine.

Read more - https://t.co/ZZbUmImA3l

Weekly Term Deposit Rate -

Over the past week, ending May 22, 2026, the strongest opportunity across the deposit curve remains concentrated around 6 months to 1 year, where average rates are highest and competition is deepest. The standout tenor is 1 year, with an average rate of 4.89%, median 5.15%, and top rates of 5.45% from RACQ Bank. This suggests the 1-year segment continues to offer the best balance of yield, breadth and reliability.

For shorter terms, value remains uneven. 1–2-month deposits have low average rates of 1.53% and 1.78%, with wide ranges driven by a few high-rate outliers. Great Southern Bank and in1bank lead at 3.50%–4.00%, but most institutions are materially lower. These terms suit liquidity parking only.

Read more - https://t.co/muBTabEuJp

#TermDeposits #InterestRates #FixedIncome #SavingsStrategy #BankRates #AustralianFinance #DepositRates #WealthManagement #FinanceAustralia #IncomeInvesting

Chart of the Week -Tightening Financial and Borrowing Conditions

Global bond yields surged sharply, with the US 10-year Treasury yield rising to 4.6% while equivalent long-term yields in the UK, Japan and Germany climbed to multi-decade highs of 5.2%, 2.7% and 3.2% respectively. MM’s global 10-year government bond indicator reached 4.86%, its highest level since 2008, with more than 80% of countries experiencing rising yields. The move reflects persistent inflation pressures, stronger-than-expected economic data and increasingly hawkish central bank expectations. As markets reprice for a prolonged higher interest rate environment, investors are reassessing portfolio positioning, valuation assumptions and the implications for equities, fixed income and broader asset allocation strategies.

#yieldreport #financialmarkets #financial #bondmarket