A ~25% fall that recovers in 8 months and a ~25% fall that's still deepening after 18 months are NOT the same bear market

One tests your nerve, the other tests your conviction

In this post we cover the two types of bear markets, why the current one is nothing like 2022, and what it means for your portfolio

Link: https://t.co/GVbAXDLLU6

One of the unique capital good companies that checks our filter of unique businesses -

→ High barriers to entry

→ Cannot be replicated just via blank cheque

→ Good return ratios

→ Limited competitors

→ Doing something cutting edge

Let’s discuss more on Inox India’s Business in 3 simple steps

→ Why this business is Unique

→ Financial Health

→ Growth Triggers

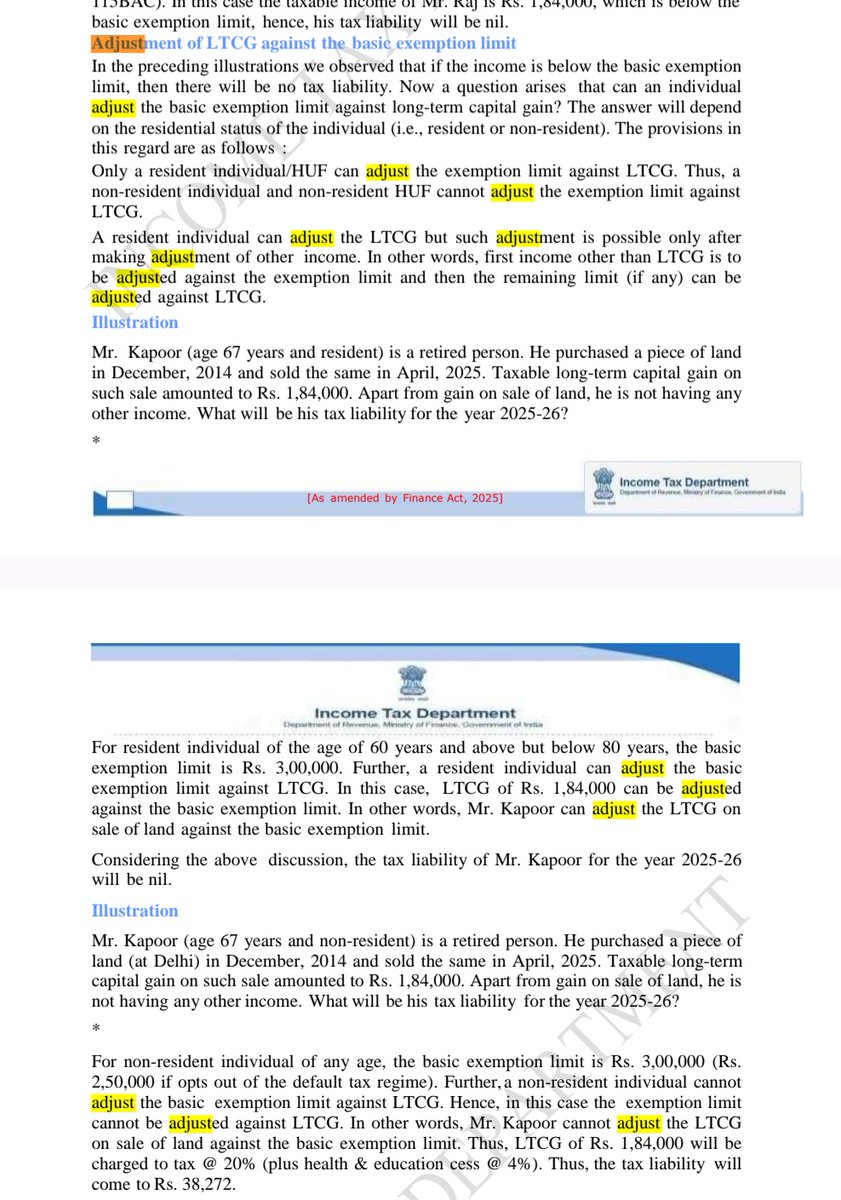

Don't book ₹1.25 lakhs of LTCG before reading this

You may have to pay ₹62,400 in taxes

Applicable for those making around ₹12L from salary/OI

Those making ~₹50L/₹1 Cr may also fall in higher surcharge slabs

Infographic by @RupeetoolByFGM Retweet to spread awareness🔁

I ran some of my writing through an AI checker. 29.7% robot-generated! Thing is, it obviously wasn't. Ethical and creative reasons aside, the book in question is nearly a decade old - well before technology could do this. 1/3

Median drawdown in stocks with MarketCap below 3,000 Cr from their 2017-18 peaks had reached around ~65% pre covid

Currently, median drawdown is ~63%

This gives a good insight into where we stand currently

We are likely around the phase of maximum pain

With an additional 5-10% of downside, the worst of the correction would probably be over

Exciting times ahead✅

@CalmInvestor@CalmInvestor can you update this post and tell what is current median drawdown now? Suspect it maybe approaching 40%

Also is there a way to incorporate time correction as a metric to get more holistic picture?

Anthropic has triggered four separate stock market selloffs in less than four weeks. Today makes five.

It started February 3 with Cowork legal plugins. Thomson Reuters dropped 16% in one session, its worst day on record. LegalZoom cratered 20%. FactSet fell 10.5%. Jefferies traders called it the “SaaSpocalypse.” Then Opus 4.6 launched on Feb 6, and financial data stocks bled again. Feb 20, Claude Code Security hit cybersecurity: CrowdStrike down 8%, Cloudflare 8.1%, JFrog 25%, the Global X Cybersecurity ETF at its lowest since November 2023. Yesterday, a blog post about COBOL modernization sent IBM down 13%, its worst day since October 2000, erasing $31 billion in market cap. The Dow dropped 820 points.

Today: enterprise connectors for FactSet, S&P Global, LSEG, DocuSign. Private plugin marketplaces. Industry plugins across finance, HR, engineering, and wealth management.

The iShares Software ETF has fallen 35% from its September peak. Software is having its worst month since the 2008 financial crisis. The sector’s 21% underperformance versus the S&P is the worst relative drawdown ever recorded, exceeding the dot-com bust. Hedge funds made $24 billion shorting the space in the first week of February and are increasing their positions. Price-to-sales ratios across SaaS compressed from 9x to 6x.

All of this from product announcements by a company that didn’t exist four years ago and now runs $14 billion in annualized revenue, growing 10x year-over-year for three consecutive years. Claude Code alone generates $2.5 billion annually nine months after public launch. 500+ customers spend over $1 million a year. $380 billion valuation after a $30 billion Series G two weeks ago.

But today’s partner list is the real signal. FactSet, S&P Global, LSEG, DocuSign. These are the companies whose stocks got destroyed three weeks ago. FactSet doesn’t build a connector to the platform that just torched its market cap unless its internal models show that fighting Claude costs more than joining it. DocuSign and Intuit rallied on their partnership announcements.

Three weeks from existential threat to distribution partner. IBM didn’t partner. IBM lost $31 billion yesterday.

Anthropic is running the AWS playbook at 10x speed. The companies that survived cloud built on it and accepted thinner margins for broader distribution. That compression is now hitting every knowledge-work SaaS vertical at once, and the companies lining up to build connectors already did the math on what happens if they don’t.

The software ETF is down 15% in February. Anthropic shipped something on four separate occasions this month. Each time, billions evaporated. Today they’re hosting an enterprise briefing. Salesforce reports earnings tonight.

There is no precedent for AI as a technology

No technology has ever improved at a double exponential rate with new capability unlocks every few months

Electricity, planes, auto etc ? Low single digit improvement and no major change in the core function

Internet ? Yes it’s faster by 1000x but has the core capabilities changed as much ? Same for mobile

AI is very different that the double exponential is leading to new capabilities every few months

It’s like your car is able to fly within a year and then evolves into a rocket after that. Not just faster, but a very different form of transportation

The implication is that every time a new capability unlocks we will get another round of technology shock, similar to what we saw with the software and IT services companies

These and other industries will not go extinct but the business model will change. As this churn happens, there will be a lot of losers and with that terminal values crash till we uncover the new winners

Strap your seatbelts - we are in for a wild ride