Low agency critics who don’t build things love saying that every “chat with PDF company is now dead” due to ChatGPT launching PDF uploads

They need to justify their lack of action to themselves: “aha! I knew I was right to sit on my butt and not build anything on top of GPT!”

Meanwhile the creator of ChatWithPDF has already created 6 other apps since ChatWithPDF

Who will win in the long run?

Every researcher's path is a rollercoaster filled with numerous lows. With unspeakable joy, today I want to share a high point: our paper, “Improving Wikipedia Verifiability with AI,” has been published in the prestigious @NaturePortfolio. Dive in https://t.co/fMJ4dXPuDp [1/4]

My prediction: in 2024, most companies will realize that smaller, cheaper, more specialized models make more sense for 99% of AI use-cases. The current market & usage is fooled by companies sponsoring the cost of training and running big models (especially with cloud incentives).

Lastly, they have the right partnerships in place to unlock $USD millions in crypto settlement volume overnight - 29 million merchants and thousands of cross-border payments - one of the few platforms that can begin to solve global payments at scale

Consumer AI apps are all chasing the most obvious ideas. Breakout apps don’t work that way. The technology should be invisible in the background.

The smart builders aren’t making AI girlfriends. They’re using AI bots to seed a dating app until they reach a critical mass of users

App Chains are not new. The difference in 2023 is that they are coming to EVM, where the majority of users + integrations (wallet, validator, bridge, node) support. Optimism’s OP Stack @optimismFND is open-source and allows any project/team to launch their own roll-up chain. In 2023 alone, adopters include:

> Coinbase’s Base @BuildOnBase

> Zora’s Network @ourZORA

> Worldcoin’s ID @worldcoin

If you ask a project the reason behind a roll-up strategy, they will give you some flavor of the following:

> Scaling: “ETH L1 is too slow”

> Flexibility: “Contracts are not optimized” or “I want to support an EIP that hasn’t hit mainnet yet”

> Value Capture: “Token launch does not make sense but I want to monetize on-chain”

The first two are pretty familiar arguments. The last is the most pertinent. The holy grail for a crypto project is able to monetize on-chain — you get global access at basically zero marginal cost (all forms of “traditional” marginal cost is outsourced to the chain). The headwinds are unknown regulatory risk on a case-by-case basis.

Today’s versions of these are:

> NFTs (@opensea) — secondary fees of on-chain NFTs

> DeFi (@0xProject) — routing fees of on-chain swaps

> Staking (@BlockdaemonHQ) — validator income of inflation + chain fees

The conversation of roll-ups have mostly been around tech optimization, but the goal is really value capture optimization in the absence of a token launch. Factors like:

> Sequencer PnL — company can monetize like a validator on block activity.

> Flexibility — company can loss-lead on a contract-level (zero cost for NFT minting) to optimize for user growth but still capture downstream sequencer fees

> BD — company gives a % of fees to partners that come to chain

The long-term payoff will come down to the project’s ability to lean on their user network effects. It’s not purely a tech game, it’s a BD/Strategy game. 2023 App Chains are about value capture as much as it is about tech.

Oh so you think crypto hasn’t found product market fit because you dislike digital art, finance, or meme coins? How’s that any different than all the “crappy” consumer goods you also don’t like but someone, somewhere does and buys online? Does that make Amazon or PayPal a crappy product without PMF? Wrong.

Like legacy e-commerce, crypto is expanding consumer preference. Anywhere, anytime, all the time. Key enhancement is crypto created digital property rights. Creators understand and value it. That’s the point. If you don’t find something you like on-chain today, don’t worry, you’ll come back later. Many didn’t buy books when Amazon started but eventually they bought something. Seen this movie before🍿

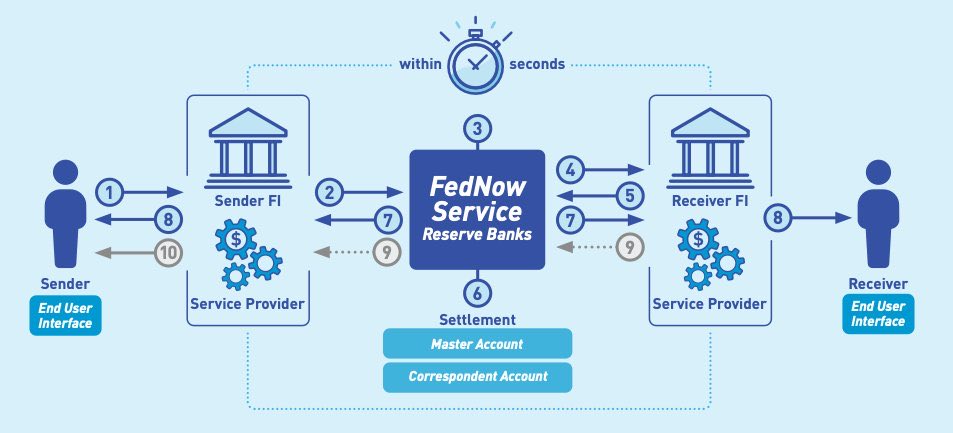

FIRST JPMC, THEN CBDC

Whether it’s intentional or emergent, this is indeed what’s happening: a backdoor nationalization of the banking system.

Blue tribe is killing gray tribe banks (SVB, FRC) and red tribe banks (regionals) to consolidate all the assets at the too-big-to-fail banks, especially JPMC.

Then they roll out FedNow. Even if it’s not a CBDC, it’s central bank digital *control* with every transaction chokepointed through them.

First JPMC, then CBDC.

Do we expect a massive sustainability campaign against AI as we’ve experienced with PoW? Or the real-world use cases coming out on a daily basis will be enough to justify it?

@taxes_crypto This is what we enable at @DiagonalFinance 👀

We bring the convenience of pull payments on-chain, while removing critical trust assumptions at the payment layer.

Shopping use cases for ChatGPT are about to explode.

@Shopify and @Klarna are in the first batch of ChatGPT Plugins offered

New paradigm: Prompt -> Answer -> Purchase

🤯🤯

![Fabio_Petroni's tweet photo. Every researcher's path is a rollercoaster filled with numerous lows. With unspeakable joy, today I want to share a high point: our paper, “Improving Wikipedia Verifiability with AI,” has been published in the prestigious @NaturePortfolio. Dive in https://t.co/fMJ4dXPuDp [1/4] https://t.co/UG2gRJKKuH](https://pbs.twimg.com/media/F8z9QxzWwAA4PvK.jpg)