This is a thread of tweets that have sentences so wild that not even infinite monkeys randomly typing on a typewriter can come up with

This will be an ever growing thread.

Legit entertaining to see Hermes try to control your browser and then you see the weirdest bugs on the front end

In Jumper the AI typed USDC first, then the chain but in doing so, the USDC token doesnt refresh, and its just stuck there not nowing which usdc to select

I'm not clear on Hermes Desktop's "interrupt" feature. It seems queued by default, but you have a /queue and no /interrupt.

I must click to expand the queue tab to find the queued prompt to force an interrupt, which feels clunky. 🙁

@NousResearch

Vaults cannot come fast enough. So many ETF databases paywall the ETF holdings. It's ridiculous, given that this is basic 101 information for investors to know what they are investing in.

Y'all forgot about table selection in trading (not shading the QT, just a passing comment). You can literally not trade something if it's fucky and you don't understand it. It's ok. Find other opportunities to swing at. Drop the ego

I traded SKYY because I believed SaaS was oversold. Then it ATH. I knew it was not sustainable, as bagholders were either getting out and UBER news had spooked them. I got out near the top.

I wouldn't say this is an edge or whatever. But it's a lot easier to have a vibe read of the market if you are focused

Now, for the next magic trick: Understand that companies cannot keep paying Claude/OpenAI forever, and eventually self-hosted OS models will be good enough. This means companies hosting their own models will be the future (as always), so invest there. Leading indicators will be the quality of OS models, more tools to build out harnesses, commitments to host etc

The counter-thesis to this is that some large tech firms are even considering building their own shit (long live semicons again?) like Bytedance. Remember that AWS was born not because they wanted to build out servers for no reason; it was because it was needed to support Amazon itself. This parallels Bytedance using Oracle. Why would they do that? They have some of the most PvP internal swe culture in there.

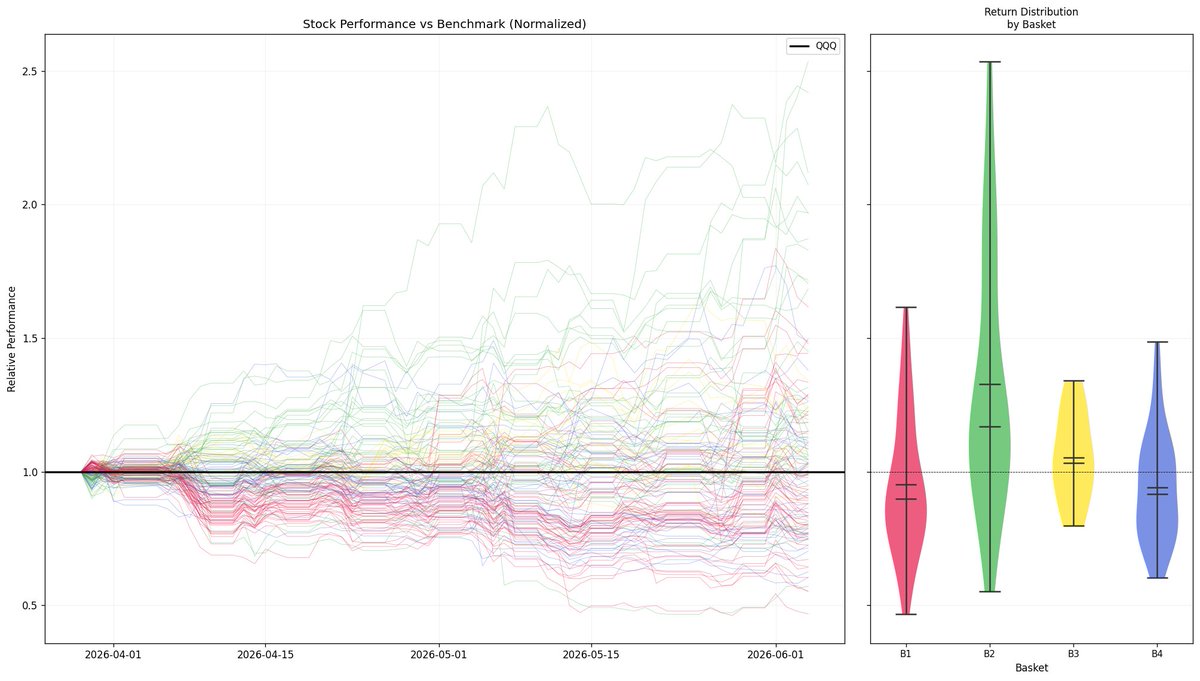

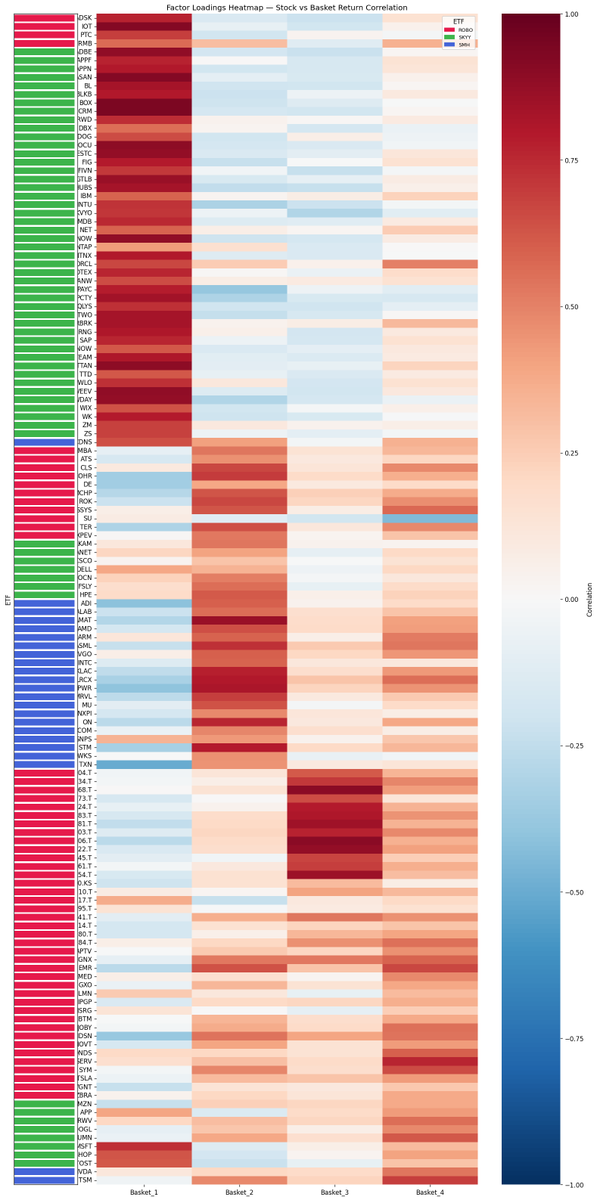

I am finding a cluster of stocks that reflects this view via factor analysis.

We just fucking wrote about this, but let me give you my thoughts as a trader as to why this is batshit insane and you're smoking more crack than @HunterBiden was if you're doing this trade (at least he appears to be just straight up long $HYPE).

Saylor has the following problem:

1 - His asset is BTC.

2 - BTC is the rationale for the price of his common stock.

3 - He has ~15Bish of preferred stock at about 10% outstanding coupons, using round numbers.

So this means we're looking at $1.5B of annual cash needs against a current cash pile of $900mm.

The market has correctly figured out Saylor has to do one of the following:

Start selling BTC to pay dividends

or

Stop paying the dividends

The former is awful for MSTR holders, the latter is awful for preferred holders, especially because once they stop, they should remain stopped until either BTC goes way back up or the company blows apart.

That means the thing marketed as reliable income is going to turn into indefinitely trapped capital with no cash flows.

Why would Saylor do this? Well, he probably assumed BTC would go up forever, faster than 10% per year. If you do that, it all makes sense. But if you don't believe that, the whole thing is batshit insane.

Right now, it's either that prefs eventually eat the value of the equity and likely create an inescapable snowball of death, but on a very long timeline, or that he's going to have to sell a shitload of BTC to redeem it all, or he's going to do neither and just pray it goes back up, which itself is the market overhang for a 4% holder, which means we're going to get the worst of both worlds.

That means if you buy STRC you could be waiting many years for a court to work this out and praying BTC holds up during that time so you get cashed out (and Saylor doesn't find other creative ways to incinerate money before that point).

There's a price at which I like STRC, as a former distressed guy. It's not in the 90s. Hint: it's not even in the 80s.

We just fucking wrote about this, but let me give you my thoughts as a trader as to why this is batshit insane and you're smoking more crack than @HunterBiden was if you're doing this trade (at least he appears to be just straight up long $HYPE).

Saylor has the following problem:

1 - His asset is BTC.

2 - BTC is the rationale for the price of his common stock.

3 - He has ~15Bish of preferred stock at about 10% outstanding coupons, using round numbers.

So this means we're looking at $1.5B of annual cash needs against a current cash pile of $900mm.

The market has correctly figured out Saylor has to do one of the following:

Start selling BTC to pay dividends

or

Stop paying the dividends

The former is awful for MSTR holders, the latter is awful for preferred holders, especially because once they stop, they should remain stopped until either BTC goes way back up or the company blows apart.

That means the thing marketed as reliable income is going to turn into indefinitely trapped capital with no cash flows.

Why would Saylor do this? Well, he probably assumed BTC would go up forever, faster than 10% per year. If you do that, it all makes sense. But if you don't believe that, the whole thing is batshit insane.

Right now, it's either that prefs eventually eat the value of the equity and likely create an inescapable snowball of death, but on a very long timeline, or that he's going to have to sell a shitload of BTC to redeem it all, or he's going to do neither and just pray it goes back up, which itself is the market overhang for a 4% holder, which means we're going to get the worst of both worlds.

That means if you buy STRC you could be waiting many years for a court to work this out and praying BTC holds up during that time so you get cashed out (and Saylor doesn't find other creative ways to incinerate money before that point).

There's a price at which I like STRC, as a former distressed guy. It's not in the 90s. Hint: it's not even in the 80s.

To what extent, is this sliver of users that DON’T use a dex aggregator (feature) simply because they want to have a consistent, deterministic pool of dexs?

As in price discovery is less important to them than knowing who’s consistently called

Not sure if skill issue on my end but the command should be:

curl -fsSL https://t.co/UCUFCsWuL1 | bash -s -- --include-desktop

I was failing install using the command in the pic

@NousResearch@Teknium

@0xQuit Smart contract risk is going to be so much higher. Using AI is one thing; having the talent to use AI and build scaffolding tools is another. And this is on top of having to hire regular security researchers too. It feels like audits are going to be very expensive.

Cheaper tokens mean you can spend more on APIs downstream.

Tech spend is zero-sum because you have to allocate budgets.

For example, we tout X402 so much, but gas fees on ARB/Base are more expensive than a single DeepSeek Flash call. It's even worse for frontier models.

Not the prettiest chart in the world, but some stocks, despite being in different ETFs, correlate with other stocks in other ETFs.

SKYY is a fairly messy ETF because it includes at least 3 factors (enterprise SaaS, consumer tech, hyperscalers)

@TECleveland @cremieuxrecueil Despite some bogus grants, a lot of government is like this cartoon. I bet this "small team" would find a line item for "screwworm sterilization" and delete it, not knowing that they just devastated American farming: https://t.co/OAnAkxDSEK