2/ This post argues that an unbundled system of separately traded, tokenized carbon attributes would provide a missing economic incentive for suppliers to reduce their emissions.

1/ New post reflecting research over the past year or so with one of the largest spec traders in voluntary carbon credits.

The argues in favor of unbundling raw materials with their carbon attributes as a new approach to reducing supply chain emissions.

https://t.co/dFSX1Z1HLh

What if the unique value prop of memecoins is that they perfectly thread the needle between the Howie test and state gambling laws?

It could be a multibillion $ industry tbh

(another visualization of the same data)

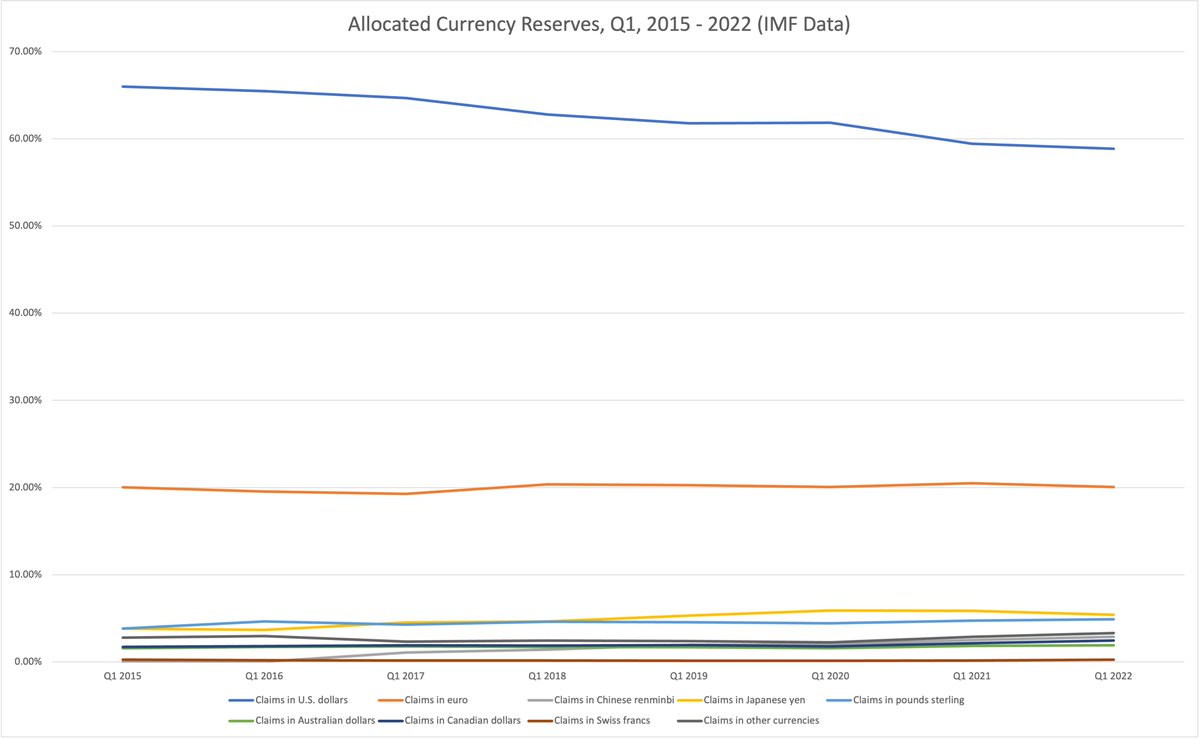

USD dominance persists, but it's waning

I haven't heard a credible theory of what reverses this

have heard some credible theories of what *might* accelerate it, based on hypothetical fact patterns that seem more likely to play out today

@balajis ringing the alarm bell on the banking system / fed / USD in the short term

On a longer time horizon, it's interesting to see the trends in what central banks themselves hold

USD claims falling noticeably as a % of allocated currency reserves since 2015

.@silvergatebank must be run by the biggest bunch of muppets ever.

Step 1: Take USD deposits from crypto firms and pay no interest

Step 2: Buy 3mth US treasury bonds yielding 4.78%

Step 3: Assume $10 billion of deposits, make $478mio a year

That's all you have to do. Muppets

1/ The recent $USDC depeg raises a critical question: what would happen to USDC holders if @Circle the company were to fail?

In this post, I argue that USDC isn't actually backed by a ringfenced pool of USD collateral, it's backed by the balance sheet of Circle the company.

👇

@sherlockdefi I think there's a decent chance that pooling risk across DeFi protocols via on-chain subordinated credit markets would provide more scalable protection for defi users against catastrophic exploit risk.

This is how tradfi banks meet Basel III capital sufficiency requirements.

Hate to see this. Users mistakenly assume security audits mean protocols are safu and coverage from @sherlockdefi etc can make them whole following an exploit.

@sherlockdefi paid a ~$4m claim on a ~$195m loss. DeFi insurance isn't going to scale imo.

I am working tirelessly right now to help people investigate the attack on Euler. But this misinformation is helping fuel threats against me and my family and I have to ask for it to stop please. Sherlock audited the code. Yesterday they paid a claim.

https://t.co/1rI6Sccm7z

For defi to reach millions of users, we must find another way to protect users against exploit losses.

Defi's enjoys elevated capital efficiency from native tokens. If there is a way to trade some of that capital efficiency for meaningful protection, seems like a good trade.

This is a commendable approach to life.

But, if one of defi's goals is to onboard millions of users, amor fati cannot be a foundational philosophy.

The risk-adjusted returns in defi are unappealing to many because exploit risk, however small, is catastrophic risk.

For starters this is my fault. Not the Euler teams. Not the hackers.

I put my money somewhere knowing there were risks involved so I have to take complete ownership of all consequences resulting from it.

One clear takeaway from the @eulerfinance hack is that security audits are not guarantees against exploits.

Another is that current protocol-level exploit coverage products like @sherlockdefi aren't scaling to provide meaningful protection for users affected by exploits.

Very sorry to hear about the @eulerfinance hack.

I continue to believe protocols can do more than audits (they had 6 audits?) to protect against user losses in exploits.

Idk if on-chain subordinated credit markets would work in practice but it feels like a worthy experiment.

2/ TLDR: DeFi capital efficiency comes at a cost. Users transact with smart contracts at their own risk, sometimes losing funds in exploits. Protocols could use lending markets to cushion user losses in the same way banks use subordinated credit markets to protect depositors.

Circle was probably banking with SVB for the same reason it did a SPAC and has “Circle Ventures”: it sees itself as a growth company and is selling a growth story. The SPAC obv makes the growth story even more important

You’re a stablecoin issuer. Stay in your lane bro

@BTCVIX It looks like they're going to get the peg back (great short term win), but at the cost of basically commingling the reserve account with the rest of the circle balance sheet.

welp I guess they did it

bankruptcy experts, pretty please explain how @circle creditors wouldn't have recourse to the reserve account if Circle fails

USDC reserve account now = Circle balance sheet