RWA yields in defi aren't higher.

They're leveraged. $1.4B in positions backed by collateral that takes months to redeem in a system that liquidates in seconds.

We broke down what the yield is actually made of.

https://t.co/b1kxjoc3YO

the auction market in ethereum is working too well.

MEV market has become hyperefficient, pricing every block near its absolute marginal cost of production.

we are witnessing a perfect inverse correlation. as the profitability of building a block collapsed by 90%, the market share of the dominant builders locked in at >80%

with thousands of bots competing for every block, bid prices are pushed so high that the winner's profit margin is effectively zero.

only massive, vertically integrated builders with huge economies of scale can afford to operate on $20 revenue per block.

everyone else has been priced out.

Backed by Fearless

We have raised a $2.2M seed round to help fearless sovereign individuals take structured positions in Internet Capital Markets

Led by: @robotventures

Privacy has transitioned from a niche preference to a fiduciary requirement for smart money.

We are moving toward a 'Dark Forest' steady state where >60% of meaningful economic activity occurs in private order flow auctions (OFAs) rather than the open P2P network.

ethereum’s market structure is rotating.

the public mempool is losing its status as the default venue for price discovery, increasingly relegated to retail users who don't know any better.

smart money has systematically migrated to private channels because they can't afford to get picked off by bots in the open; hence privacy is a prerequisite for efficient execution.

Borrowing has a real cost again. There is now an active competition for capital.

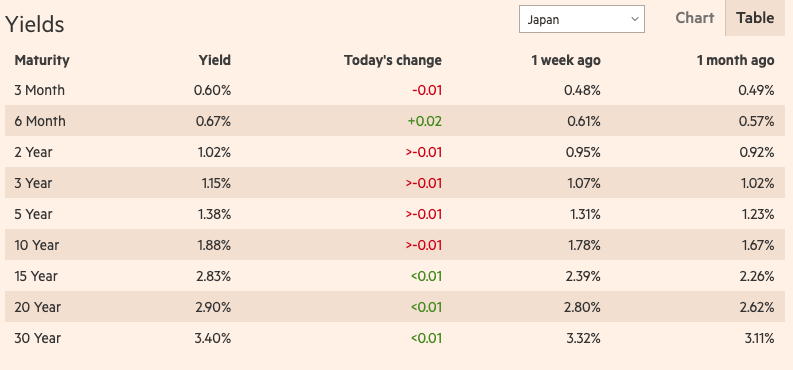

Japan used to anchor global carry. Three years ago the entire curve was pinned near zero. Today the 10y is around 1.88%. The 30y sits at 3.40%.

That matters because Japan was the marginal source of global leverage. When JGB yields normalize, the global cost of capital rises structurally. Cheap capital vanishes. The liquidity that powered the previous cycle no longer exists in the same form.

This is still not a crash but a systematic repricing event involving fundamental adjustment to new expected returns.

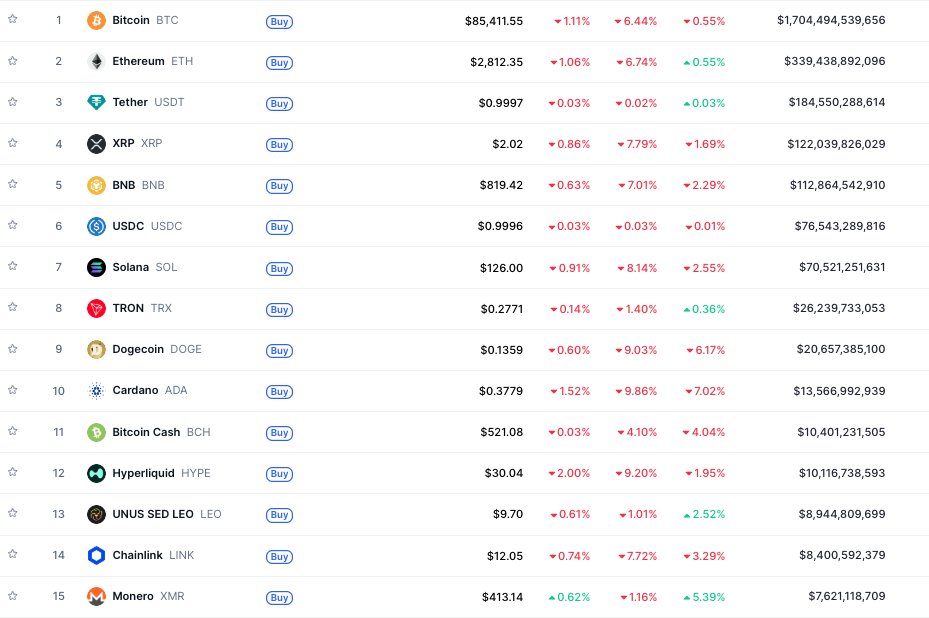

> Bitcoin is still over $1.7 trillion.

> Ethereum is still ~$340 billion.

> Solana is ~$70 billion.

That is not collapse. That is rotation out of risk exposure during rate repricing. The quick checks for a real “crisis” are:

> Are large exchanges facing solvency or credit events?

> Is there evidence of widespread forced selling from lenders or funds?

So far:

> USDT and USDC are still trading very close to 1 USD, despite S&P’s downgrade of Tether’s stability rating earlier in the week.

> There are no headlines about major exchange failures or big lenders blowing up.

> ETF outflows are large but orderly, and spreads in listed products remain tight.

This is exactly what a risk off repricing looks like when an asset class has migrated into mainstream markets. Prices adjust sharply, flows reverse, but pipes do not break.

> Rates are no longer rising violently

> Liquidity is not expanding yet

> The dollar is stable

> Credit spreads are contained

> Funding costs are manageable

The positive inflection only arrives when the rate path moves from restrictive to accommodative. That is when real liquidity waves return. At that point crypto tends to outperform everything else because it reprices faster.

We are not there yet, but the structural setup is much cleaner than in previous cycles. The floor is higher, the leverage is lower, and the demand base is broader. When accommodation finally returns, crypto will feel it first.

the fundamental macro constraint on risk assets including crypto and DeFi is easing.

overnight markets are softer & leverage isn’t as punishing on the margins. but this isn’t cheap money territory.

free money is still far from accessible.

Modern exchanges are no longer just venues where trades are executed; they’re monetization frameworks for liquidity.

GRVT continues to execute at the intersection of exchange architecture and structured liquidity.

Big step forward!

New piece of Grvt’s yield flywheel is now LIVE

Introducing Grvt Liquidity Provider (GLP) Strategy, our native protocol vault using delta-neutral, market-making strategy

☼ Managed with a LP and trading firm that’s been in the game for 40+ years

☼ Battle-tested for 6 months with ~48% APR and 7.6 Sharpe ratio

☼ Access to invest in GLP depends on your lifetime trading volume

☼ GLP investors also earn from a weekly 15% Grvt Points pool based on TVL

→ Info on investment cap: https://t.co/9DuX1phcJG

→ Get started: https://t.co/YzWhDy7Cwt

The U.S. Secured Overnight Financing Rate -- the daily cost of borrowing dollars against Treasuries -- jumped 18 bps to 4.22%, its biggest one-day rise in a year.

That was not random but a signal that liquidity just tightened at the core of the dollar system.

When SOFR rises, every leveraged dollar becomes more expensive -- from Wall Street repo desks to offshore stablecoin markets to CEX's perps. That ripple pushes funding costs higher, compresses carry, and drains speculative appetite.

Crypto felt it instantly. The same dollar liquidity that props up leverage and stablecoin liquidity just became scarcer and pricier.

The timing of this crash mirrors several prior episodes:

1. September 2019 Repo Crisis: funding rates spiked 300 bps intraday >> Bitcoin fell ~10%.

2. March 2020: repo panic during COVID >> broad deleveraging, Bitcoin crashed >40%.

3. April 2023: debt-ceiling collateral squeeze >> minor SOFR surge >> crypto correction.

It’s all always about liquidity transmission and the reflexivity of funding conditions.

A few basis points in repo turned into billions wiped from market cap -- a reminder that everything in crypto still syncs to the price of dollar funding.

We’re excited to deepen our partnership with Transak, joining @tether and IDG Capital in the newly announced $16 million strategic round.

Our investment rests on a simple thesis: as regulated stablecoins become the preferred medium for cross-border settlement, the winners will be the firms that pair a global compliance stack with friction-free API integration for wallets, exchanges, and fintechs.

We’re excited to support Sami, Yeshu and the entire team as they expand these rails worldwide.

Money is changing and we’re enabling it!

Thrilled to announce our $16M strategic round to scale stablecoin payments, led by @tether and @IDGCapital

Read more on our blog 👉 https://t.co/bcqavJZ99m

Traditional DeFi vaults solved one problem, trustless execution, but left three big issues unattended:

- professional managers have no incentive to reveal their edge when every trade is broadcast in real time;

- investors cannot easily check who is actually running the vault or whether that person has a track‑record;

- discovery is haphazard, so good strategies get buried and poor ones can still attract deposits.

GRVT tackles all three simultaneously.

- Manager identities are verified by the exchange team;

- trade disclosure is delayed by four hours so alpha is not front run; and

- strategy pages are ranked and surfaced algorithmically, much like a modern e‑commerce catalogue, so investors see credible options first.

Institutional controls, transparent onchain execution, and real liquidity; exactly the mix we look for in our portfolio.

It’s here: Finance that just flows

You deserve a real shot at building wealth

With just $1

On premium options

In one click

And so we start our mission with Grvt Strategies — now LIVE

Invest in elite traders and let them win for you

Plus, get early time-limited rewards:

1. Invite friends to invest & earn up to 500 USDT each

2. Invest & get guaranteed extra 20% APR

→ Time-limited incentives details: https://t.co/AHyVHG3awO

→ Base incentives details: https://t.co/Iv06rivXtM

→ Invest in our first lineup of traders now: https://t.co/LXiTV51KWJ

And spot our new look?

Vision, mission, roadmap, and our brand upgrade details coming soon. Stay tuned.

A year ago @AethirCloud launched their token and opened its GPU marketplace. Twelve months on, two data points tell the story:

1. First, Scale. Aethir now delivers more paid GPU hours than any other Web3 cloud. Checker and Scaler nodes stretch across five continents, and fresh operators are coming online every week under the licence model.

2. Second, Revenue. Fees booked in the last quarter annualize to about US $141 million. That money comes from real clients (AI labs running inference, game studios pushing renders, DeFi teams crunching risk models) who pay to execute on Aethir hardware. It’s cash in the door, not a forecast, and it already funds expansion and underwrites token economics.

These numbers matter:

1. Demand is genuine. Plenty of DePIN projects boast capacity first and hope workloads appear later. Aethir flipped that script: demand showed up early enough to fund supply expansion, not the other way around.

2. Token flywheel has traction. Restaking ATH through EigenLayer mints eATH, which now earns a slice of GPU fees. If workloads grow, yield climbs; if yield climbs, more tokens lock up, deepening liquidity and dampening sell pressure. Reflexive loops cut both ways, but right now it’s spinning in the right direction.

The objective for year two is unchanged: make high-performance GPU compute as open, reliable, and economically transparent as the best public clouds.

1 year since our TGE, Aethir has grown into the largest decentralized GPU Cloud network in Web3 and is leading the DePIN space with $141M+ ARR 🔥

Now, it's time to celebrate 🪂🎉

We’ve got exclusive surprises for our Aethirians, and spotlighting our biggest product drops 🧵👇

Our portfolio company @ChainSight_ has been quietly shipping something very smart: unbundling the oracle layer and turning it into a flexible, modular platform that feels like modern developer infrastructure.

This is the key conceptual shift: oracles not as a service, but as a platform.

@0xshumpei breaks this down perfectly, because as blockchains evolve toward application-specific use cases, developers need bespoke oracle logic, not just static price feeds.

-- Need to fetch data from a niche API? Done.

-- Want to process it through your own volatility model? Upload your custom logic.

-- Want it live on Ethereum, Solana, L2s, or all at once? It takes minutes.

And security isn’t an afterthought. With ChainSight, you're working with a fundamentally different type of oracle: one that’s verifiable, composable, and private by design.

i keep coming back to the idea time and again that POL collapses two markets:

1. blockspace security, and

2. application-level liquidity,

into a single, composite market priced in BGT.

1. security via staking (through validators) and

2. liquidity (through dapps)

now bid for the same scarce resource: delegated boost.

that may sound abstract, but its more clear with supply/demand curves.

supply side.

-- block time averages 2s (43.2k blocks/day), the base emission is 0.5 BGT/block (21.6k BGT/day), and reward-vault emission ranges from 1.5-4.5 BGT depending on boost.

-- with total emissions at 120k BGT/day, vault emissions average ~2.28 BGT/block (98.4k BGT/day; you can take 3 BGT/block as well), reflecting boost distribution (infrared’s 64% share likely earns more, others less).

-- at that pace, circulating BGT (14.13M) doubles roughly every 116 days.

-- that works out to ~0.85% inflation every 24 hours.

the block-level cap is fixed: extra dapps cannot raise aggregate emissions; they can only fight for a bigger slice.

demand side. BGT is non-transferable, but it isn’t frozen. we can undelegate, wait out a cooldown epoch, and re-delegate. that gives it episodic velocity: turnover happens in days or weeks, not blocks. though the exact epoch length isn’t clear. berachain defines an epoch as 192 blocks; with ~2s block time, that’s ~384s (6 min 24s), but practical delays (e.g., network load) might stretch this. redelegation likely takes 3 epochs (post-undelegation wait, redelegation, and confirmation), so ~19 min. because the right to delegate is what prints future BGT, demand for BGT delegation really is demand for a licence to dilute the rest of the holders. in equilibrium, the licence price (i.e., the real yield paid by vaults) must cover:

1. the opportunity cost of plain BERA staking, and

2. the time-to-redelegation friction (cooldown epochs plus gas fees).

if a vault’s net APR after optimizer gas can’t beat plain staking, its boost will drain out, and its liquidity will follow.

now, infrared manages about 40% of total stake yet 64% of boost, that’s a leverage ratio of 1.6x. consider a single infrared validator sitting at the 10M BERA cap: that’s ~2.5% of network stake and ~5% of total boost. over a 24-hour window it proposes ~1080 blocks, minting:

-- base reward: 0.5 BGT/block × 1080 = ~540 BGT

-- boost-driven reward: 5% of the network’s 98.4k

-- BGT daily vault stream ≈ 4920 BGT

-- total ~5460 BGT per day.

infrared channels roughly 60% of that flow (~3276 BGT) into reward vaults that, after slippage and gas, pay a blended 25% APR (illustrative, net of slippage and gas). the net result is:

-- iBERA stakers: ~3% incremental yield over plain staking

-- iBGT holders: 10–15% in wrapped-incentive form

(Note: APR and yields are illustrative)

because the yield pool is fixed while supply keeps growing, these rates fall with dilution; when circulating BGT hits ~25M (in ~90 days from today), yields will halve unless vault budgets grow proportionally. though dapps may increase budgets as they compete for liquidity.

also, governance is pure 1 BGT-1 vote with a 20% quorum and a two-day guardian timelock. because quorum is measured directly in BGT, the cheapest way to gain influence is to buy boost, emit fresh BGT into one’s own vault, farm it back, and recycle the voting power. the 5-of-9 guardians can veto sketchy payloads, so lightning-fast coups like curve-style gauge sniping are off the table; but a week-long bribery campaign remains perfectly feasible.

inevitably, whenever two protocols chase the same liquidity, they will keep out-bidding each other for boost until the marginal apr advantage shrinks to the point where it no longer justifies switching costs.

infrared’s 64% boost share gives them outsized influence here, and if their algorithm overly favors their own validators, centralization risks grow.

the next 116-day (assumptive) issuance cycle will reveal whether emissions diversify or re-centralize.

if you trade or hold BTC, knowing where the real liquidity lives is half the game.

bitcoin just printed $111k–$112k intraday highs and is flirting with a fresh ATH.

but the real story is what’s not trading:

- 31% of all BTC hasn’t moved in 5 yrs

- US spot ETFs now hold ≈1.19M BTC and added another 3000 BTC yesterday

- new mining adds only 450 BTC/day

we’re already 11 months of future supply in the hole.

unless a forced seller (miners, US marshals auction, or a big ETF redemption) dumps coins, every new dollar of demand has to bid higher to pry coins from cold storage.

i wrote the below article to map out this squeeze in plain numbers and show the four release valves that could still flood the market.