In Defense of Exponentials

I used to tell founders, the reaction you are going to get to your launch is not hate, it’s indifference. By default, nobody cares about your new chain.

I have to stop telling them that now. Monad just launched this week, and I’ve never seen so much hate about a blockchain that just launched. I’ve been investing into crypto professionally for 7+ years now. Before 2023, almost every chain I’ve ever seen that launched was mostly met with enthusiasm or indifference.

But now, new chains are born into a chorus of hate. The amount of haters I’ve seen for projects like Monad, Tempo, MegaETH—before they even hit mainnet—is a genuinely new phenomenon.

I’ve been trying to diagnose: why is this happening now, and what does it mean about the psychology of this market?

The Cure is Worse than the Disease

Forewarning: this is going to be the vaguest blockchain valuation post you ever read. I don’t have any fancy metrics or charts to sell you on. Instead, I’ll be arguing against the zeitgeist of Crypto Twitter, which for the last couple of years, I’ve been constantly on the opposite side of.

In 2024, I felt like what I was arguing against was financial nihilism. Financial nihilism is the belief that none of these assets matter, it’s all memes at the end of the day, and everything we’ve built is inherently worthless.

Thankfully, that’s no longer the vibe. We have broken out of that spell.

But the zeitgeist now is what I’d call financial cynicism: OK, maybe some of this stuff has value, maybe it’s not all memes, but it’s grossly overvalued and it’s only a matter of time before Wall Street finds that out. Not that all chains are worthless. But these things are all maybe worth 1/5th-1/10th of what they’re currently trading at (have you seen these PE ratios?), and so you’d better pray like hell Wall Street doesn’t call us on our bluff, because once they do it’s all getting wiped out.

You’ve got many bullish analysts now trying to conjure up optimistic L1 valuation models, inflating PE ratios, gross margins, DCFs, trying to fight against this mood.

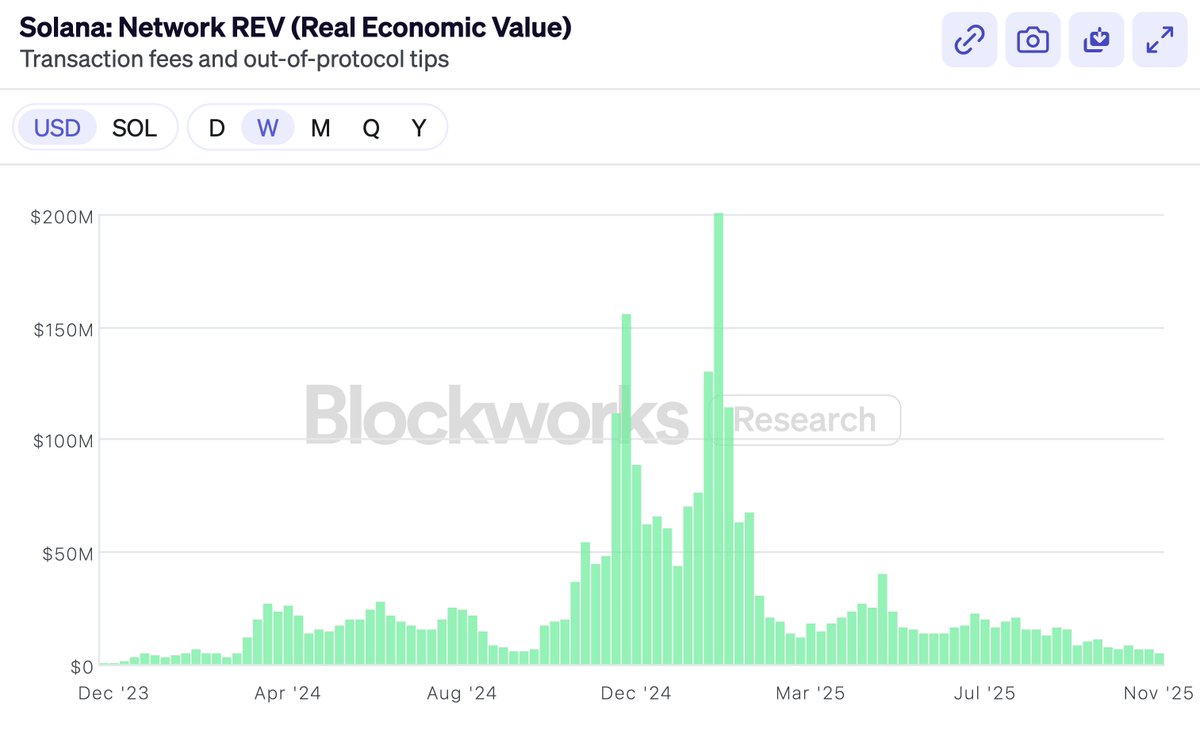

Late last year, Solana very proudly embraced REV as a metric that could finally justify their valuation. They proudly announced: we—and only we—are no longer bluffing to Wall Street!

And, of course, almost immediately after REV was embraced, it fell off a cliff (though $SOL, tellingly, did better than REV did).

Not that there’s anything wrong with REV. REV is a very clever metric. But the point of this post is not metric selection.

Then came the launch of Hyperliquid. A DEX that had real revenue and buybacks and PE multiples. And the chorus said—look, look I told you! Finally, for the first time ever, a token that has some real profits and a proper PE multiple. (Nevermind BNB, we don’t talk about that.) Hyperliquid will eat everything because obviously Ethereum and Solana don’t make any real money, we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these buyback-heavy tokens are all great. But the market always had the ability to invest into exchanges. You could always buy Coinbase, or BNB, or whatever. We own $HYPE, and I agree that it’s a fantastic product.

But that’s not why people were investing in ETH and SOL. The fact that L1s don't have exchange-like profit margins is not why people were buying them—if they wanted that, they could’ve bought Coinbase stock.

So if I’m not critiquing blockchain financial metrics, maybe you think this post is going to be chiding the sinfulness of the token-industrial complex.

Obviously, everyone has lost money on tokens in the last year, VCs included. Alts are down bad this year. And so the other half of the zeitgeist on CT is arguing about who's to blame. Who’s become greedy? Are the VCs greedy? Is Wintermute greedy? Is Binance greedy? Are the farmers greedy? Are the founders greedy?

The answer, of course, is the same as it’s ever been.

Everyone is greedy. Everyone. The VCs, Wintermute, the farmers, Binance, the KOLs, they're all greedy, and you are greedy too. But it doesn't matter. Because no functioning market has ever required anyone to act against their self-interest. If we're right about crypto, we can all be greedy and the investments will still work out. Trying to analyze a market that has gone down by figuring out “who’s greedy” is going to be about as fruitful as commissioning witch trials. I guarantee you, nobody just started being greedy in 2025.

So this, too, is not what I’m going to be writing about.

Many people want me to write a post about why $MON should be valued at X or $MEGA at Y. I’m not interested in writing this post, or advocating that you buy anything in particular. In fact, you probably shouldn’t buy any of them if you don’t already believe in them.

Will any new challenger chain win? Who knows. But if it has a material chance of winning, it's going to be priced on that basis. If Ethereum is worth $300B or Solana is worth $80B, a project that has a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow CT is scandalized by this, but it’s no different than Biotech. A drug that has less than a 10% chance of curing Alzheimer's is priced by the market as worth billions of dollars, even if 90% chance it won’t pass stage 3 trials and will go to 0. That's how the math works—and turns out, markets are pretty good at doing math. Binary outcomes are priced on probabilities, not on run rates or moral turpitude. It’s the “shut up and calculate” school of valuation.

I really don’t think that’s an interesting question to write about. “5% chance to win? No way, that’s clearly a 10% chance!” Markets, not articles, are the best way to assess that for any individual token.

So here’s what I am going to write about: CT doesn't seem to believe anymore that chains are valuable.

I don’t think this is because they don’t believe new chains can win market share. We just saw Solana dominate market share after emerging from the ashes less than 2 years ago. It’s not easy, but of course it’s possible.

It’s more that people have come to believe that even if a new chain wins, there’s no prize worth winning. If $ETH is just a meme, if it’ll never generate real revenue, then even if you win, you won’t be worth $300B. The contest is not worth winning, because these valuations are all bunk and it’ll all come crashing down before you go to claim your prize.

Being optimistic about chain valuations has become passé. Not that nobody is optimistic—obviously there must be optimists out there. For every seller there’s a buyer, and as much as CT cool kids love to drag L1s, people are comfortable buying SOL at $140, ETH at $3000.

But there’s a perception now that all the smartest people are over buying smart contract chains. Smart people know the jig is up. If not now, then soon. The only people buying here are suckers—Uber drivers, Tom Lee, and KOLs who say stuff like “trillions.” And maybe the US Treasury. But not the smart money.

This is bullshit. I don’t believe it, and you shouldn’t either.

So I felt like I had to write a smart person’s manifesto on why general purpose chains are valuable. This post is not about Monad or MegaETH. It’s really in defense of ETH and SOL. Because if you believe ETH and SOL are valuable, the rest is straight downstream.

Defending ETH and SOL valuations is generally not my job as a VC, but fuck it, if nobody else is willing to do it, then I’ll write it.

Feeling the Exponential

My partner Bo experienced the Chinese Internet boom first-hand as a VC. I’ve heard how “crypto is like the Internet” so many times now that it doesn’t even register for me anymore. But when I hear his stories, it always reminds me how costly it is to be wrong about these things.

A story he often tells is about when all the early e-commerce VCs (it was a small group back then) got together for coffee in the early 2000s. They debated: how big is the market for e-commerce going to be?

Is it going to be mostly electronics (maybe only techies will use PCs)? Could it ever work for women (perhaps they’re too tactile)? What about food (maybe impossible to manage perishables)? These were deeply important questions for early VCs to decide what to invest in and what prices to pay.

The answer, of course, was that literally every single one of them was devastatingly wrong. E-commerce would sell everything, and the target audience was the whole fucking world. But nobody at the time actually believed it. And even if they did, it would be too absurd to say out loud.

You just had to wait long enough for the exponential to show you. Even among the believers, very few thought e-commerce would become as big as it became. And those few who did, almost all of them became billionaires from just not selling. Every other VC—as Bo tells me, since he was one of them—sold too early.

It has become passé in crypto to believe in the exponential.

I believe in the crypto exponential. Because I’ve lived it.

When I started in crypto, nobody used this stuff. It was tiny and broken and awful. TVL on-chain was in the millions. We invested into the first generation of DeFi, MakerDAO, Compound, 1inch, back when they were science projects. I remember playing around on EtherDelta back when DEXes traded single digit millions a day, and that was considered to be a huge success. It was complete dogshit. Now we routinely trade in the tens of billions on-chain every day. I remember believing it was crazy that Tether hit a billion dollars in issuance and was being written up in the NYT as a ponzi scheme on the brink of shutdown. Now stablecoins are over $300B and regulated by the Federal Reserve.

I believe in the exponential because I’ve lived it. I’ve seen it over and over again.

But you might respond—well, stablecoin growth might be exponential, maybe DeFi volumes are exponential, but they don’t accrue to ETH or SOL. The value doesn’t get captured by the chains.

To which I answer: you still don’t believe in the exponential.

Because the exponential’s answer is always the same: it doesn’t matter. This stuff is going to be so much bigger than it is today. And when it’s absolutely enormous, you’ll make it up on scale.

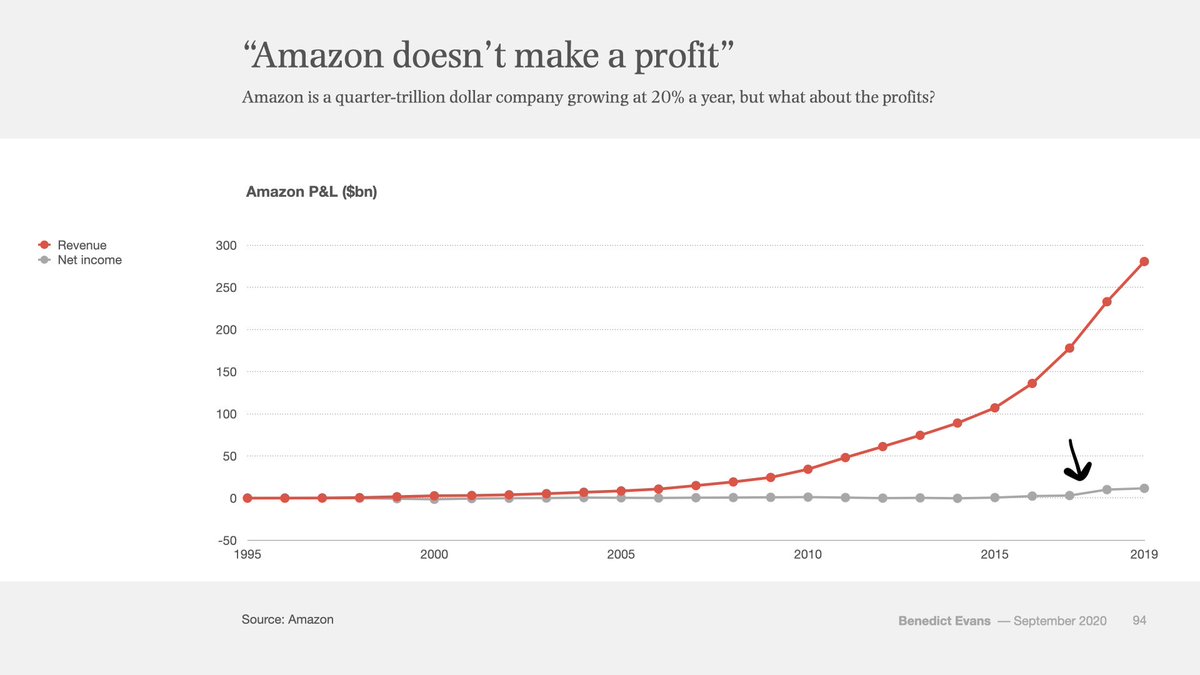

Study this chart.

This is Amazon’s P&L from 1995 to 2019. That’s 24 years. Red is revenue, gray is profit. You see that little blip on the end where the gray line goes up? That’s when, 22 years in, Amazon started actually making a profit.

Amazon was 22 years old when this little gray line of net income first peeled off of 0. Every single year before then, there were op eds and critics and short sellers claiming that Amazon was a ponzi scheme that would never make any money.

Ethereum just turned 10 years old. This is what the first 10 years of Amazon stock looked like:

10 years of chop. All along the way, Amazon was beset with doubters and non-believers. Is e-commerce a VC-subsidized charity? They’re selling underpriced cheap low-quality knick-knacks to bargain hunters, who cares? How are they ever going to make actual money, like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong regime. That’s the regime of linear growth. But e-commerce was not a linear trend, and so every single person for 22 years arguing about P/E ratios was devastatingly wrong. No matter what you paid, no matter when you bought, you were not bullish enough.

Because that’s what exponentials do. When it comes to truly exponential technologies, no matter how big you think it’s going to get, it just keeps getting even bigger.

This is the thing that Silicon Valley has always understood better than Wall Street. Silicon Valley was raised on exponentials, while Wall Street was raised on linearity. And over the last few years, crypto’s center of gravity has migrated from Silicon Valley to Wall Street. You can feel it.

Granted, crypto growth doesn’t look as smooth as e-commerce’s growth. It’s burstier, it goes in fits and starts. This is because crypto, being about money, is deeply tied to macro forces, and it also has more violent regulatory push and pull than e-commerce. Crypto strikes at the heart of the state—money—and so it’s more unnerving to governments than e-commerce ever was.

But the exponential is no less inevitable. It's a crude argument. But if crypto is exponential, then the crude argument is correct.

Zoom out.

Financial assets want to be free. They want to be open. They want to be interconnected. Crypto turns financial assets into file formats, makes it as easy to send a dollar or a stock as to send a PDF. Crypto makes it possible for everything to talk to everything. It makes it all 24/7, global, interconnected, and open.

That will win. Open always wins.

If there’s no other lesson I've learned from the Internet, it’s that. Incumbents will fight against it, governments will huff and puff, but eventually they will give up against the adoption, the generativeness, the sheer efficiency that this technology enables. It’s what the Internet did to every other industry. Blockchains are how that same trend will gobble up all of finance and money.

Yes—with enough time—all of it.

An old saying goes: people overestimate what can happen in two years, but they underestimate what can happen in ten.

If you believe in the exponential, if you zoom out enough, then it’s all still cheap. And it should humble you that every day, the holders outlast the sellers and naysayers. Big capital has a longer time horizon than CT swing traders might lead you to believe. Big capital has been trained through history not to fade big technologies. You know, the big gushy story that originally got you to buy $ETH or $SOL? Big capital believes that story and hasn't stopped.

So what exactly am I arguing?

I am arguing that applying P/E ratios to smart contract chains (the “revenue meta,” as it’s now called), is giving up on the exponential. It means you have consigned this industry to the regime of linear growth. It means you believe 30 million DAUs on-chain and <1% of M2 is it. Crypto is just one of the things in the world. A sideshow. It did not win. It was not inevitable.

More than anything, I’m arguing to be a believer. Not just a believer, but a long-term believer.

I’m arguing that this exponential will be bigger than anything else you’ve been a part of in your life. That this is your e-commerce. That you will look back when you’re old and tell your kids—I was there when it all happened. Not everyone believed it was possible, that whole societies could change, that all of money and finance would be transformed by programs running on decentralized computers that we collectively owned.

But it actually happened. It changed the world.

And you were a part of it.

Disclosure: These are my own views. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY among many other tokens. Dragonfly believes in the exponential. This is not investment advice, but is advice of another kind.

Nicely proposed framework to verify whether a token should exist

>Blockchain test: If you replaced the blockchain with a regular trusted database, would the app lose its core value?

>Token test: If you swapped this token for ETH or USDC, would the app lose its core value?

And four categories of token design:

>Asset: The token is the asset being secured (Bitcoin)

>Blockspace: The token prices a unique scarce resource that the chain produces (ETH)

>Bond: The token is staked at risk, like a performance or consensus bond where using an external asset would introduce trust assumptions (LINK)

>Allocator: The token allocates capital across competing producers in a verifiable way (TAO?)

I am not a fan of TAO, and based on my impression from casual conversations with TAO builders, the current design favors mundane output rather than excellence. It is more profitable to generate multiple outputs that sit in an average range than a superior one that sits on top, while the reality in business is winner takes all.

@Aryonchain has theorized and captured that failure effectively:

>emission based on stake hype, not actual outside demand

>gaming the evaluator is often more profitable

>colluding validators can capture outsized rewards

The paper arguing against token existence for governance is the tricky part. TBH, it is somewhat a red flag for me if a token's only utility is governance, and whether the current form of DAO governance is effective is another topic worth discussion. For projects that want to have a DAO, I don't think it makes sense to use existing tokens, as existing token holders might not have real incentive to vote for the best outcome rather than native token holders, where a bad vote can hurt their own interest. Governance tokens may sit with performance bond, all Interest at risk.

@kenzieyangxz Great writing Kenzie. Curious to hear forward looking thoughts from you and Galaxy. Also what does Galaxy lending team think about Morpho midnight

Thank you Derrick @zeebradoom and Sam @0xCryptoSam for organizing the event. Fun time together.

I want to organize an event for the club too once our office is ready.

Whitepaper Reading @ethconf 2026: Morpho Midnight

Thank you to @zeebradoom (@BigBrainVC) for the pizza and @0xCryptoSam (@recvcx) for the space!

And of course @Morpho for an incredible paper!

The conversations were deep and very insightful so thank you everyone that attended! The room was packed with experts, with members from @anza_xyz , @paxoslabs, @Quantstamp, @polychain, just to name a few.

Some unique insights/questions discussed through the evening included:

1. What are the reasons for seemingly arbitrary numbers, like the 15 minute overdue position linear liquidation incentive factor growth, the max 50 bps annualized settlement fee, or the 1% continuous fee cap?

2. Why use "units" rather than ERC20 tokens? Our discussion thought that it may be to capture value through the settlement fee (forcing all trading to happen through Midnight), and to reduce on-chain computation overhead of using ERC standards.

3. Why are there just 2 optional gate contracts? We thought that it was just that one gate was to specify the restrictions on credit positions and one gate for debt positions.

4. What does footnote 5 mean? We discussed what it meant that Morpho Blue only realized bad debt after collateral was "fully seized" and the expectation for liquidators to act promptly. We discussed how frontrunning may still be an issue.

5. We discucsed the possibility to tokenize positions to create secondary markets, and the possibility for Midnight to internalize these products.

6. Is there the possibility for two identical markets to launch 2 different markets (thereby fragmenting liquidity)? We concluded that it was probably up to the Router to match markets that were structurally identical.

7. Are seperate "markets" created based on fee structure, duration, and collateral? We believed this may cause liquidity fragmentation issues.

8. What is the difference between Midnight and peer to peer lending? We thought the ability for Midnight to do "batch" liquidations rather than pair wise liquidations was a huge efficiency unlock. We also talked about how the fact that both lenders and borrows can act first and "bid" was a huge unlock, as previous lending protocols depended on either a borrower or lender to always act first.

9. Does a hand picked liquidator introduce new risk if the liquidator doesn't act? Yes, but institutional liquidators may be paid to help manage markets, which reduces the risk of this occuring.

10. Is it possible to sell your position to a particular individual? Through gates, it may be possible to control who you sell/buy your position to without only selling to the best market price.

Thank you for attending, and reach out if you would like to attend the next ny whitepaper reading circle!

Link to whitepaper: https://t.co/4fKnZYqlPi

Link to summary: https://t.co/ho2MpHPEo7

A note on the SPCX pre-IPO (IPOP) contract:

TradeXYZ IPOP contracts are price-based perpetual contracts that track the market-implied expected price of one share of Class A or common stock. Neither share count nor market cap are an input to the market specification, oracle methodology, or conversion treatment.

Our documentation had previously featured educational examples showing how a user might derive their own fair price in a scenario where they started with a view on both market cap and share count. Although these examples were included for context, we received feedback that they caused confusion, so we have removed them from the documentation.

TradeXYZ does not use, publish, or rely on a share-count or market-cap denominator for SPCX or any other XYZ market. When SpaceX completes their IPO and sufficient external market data becomes available, SPCX is expected to transition to standard external oracle pricing, and the contract is expected to converge toward the public trading price.

Bro, with this much money moving on chain nowadays, we seriously need a SOP for counting.

Two dashboards. One protocol. $188m apart.

Entropy advisors(Protocol Audit): $203m. Protocol website: $391m.

Entropy advisors quoting DefiLlama counts unique capital once. Website quoting raw on chain data counts every layer the same dollar passes through.

Same money. Counted differently. Nearly 2x gap. Adding extra hours to my work....

Reading Archetype Privacy 2.0 Thesis by @oddhash

Early crypto privacy tools forced a tradeoff: be private, or be usable cross ecosystem. Not both. Mixers and dark pools siloed your data. Nothing else could touch it, price it, or build on top of it. We are at the bottom left. The goal is the top right: private and usable across the ecosystem at the same time. They call this private shared state.

>Currently three technologies are competing to get there. Each has real tradeoffs. The future belongs to hybrid stacks with ZK.

>I've been looking at private credit RWA recently. The opportunity is massive and privacy tech is indispensable infrastructure for it. How do you keep borrower identity and loan details private while maintaining on-chain transparency and records?

>Privacy 2.0 is built to solve.

Good read. My takeaway from speaking with folks from Wall Street is that large corporates already have access to sophisticated hedging and risk-transfer tools, while many SMB risks can be addressed through existing insurers. The opportunity for PMs may be less about replacing these systems and more about covering risks that are currently too niche, expensive, or operationally burdensome to insure.

>The challenge is that SMB risks are often highly localized and idiosyncratic. Traditional underwriters solve this through scale, proprietary datasets, and customized pricing. PMs face a tradeoff: the more standardized a contract becomes, the more liquidity it can attract but the greater the basis risk; the more tailored it becomes, the better the hedge but the harder it is to attract market makers and sustain liquidity.

>An underappreciated constraint is data availability. SMBs often lack the historical data needed to quantify how sensitive their business is to a given risk factor. Traditional insurers address this through risk pooling, actuarial models, and underwriting data across large books of business. On PMs, even if a contract is liquid, businesses may still struggle to size the hedge correctly. A local ice cream shop may know intuitively that cold weather hurts sales, but without data linking daily revenue to temperature, they can't know whether a 10°F drop means a 5% or 30% decline, making any hedge largely a guess.

>In that sense, the key constraint may not be the trading mechanism itself, but whether localized risk can be translated into contracts that are simultaneously measurable, liquid, and economically meaningful.

Hearing lots of recent discussions focusing on how prediction markets can become an insurance-like mech for SMBs (eg. NYC bar Kalshi hedge). A few rough thoughts on the pros/cons here:

> Prediction markets offer fine-grained event hedging, easy/legible payout options, and less admin paperwork compared to trad insurance mechanisms. Prediction markets can also offer niche, parameterized markets that no traditional insurer would create for a single SMB.

> Eg. a logistics company for example could hedge delivery risks by using on weather markets or Strait of Hormuz markets rather than going for costly custom-built insurance policies

> For market makers, this "hedging" behavior by SMBs provides a really great source of nontoxic flow - the SMBs trade on exposure rather than on information, making these markets more attractive for MMs to provide liquidity and underwrite

> One structural problem though, is that there could be a "basis risk" - the outcome of the market (esp. large liquid markets) might not be tied to the cost-centers of the business. For example, a PM has "will temps in New Jersey be under X" as a liquid market, but the real risk I as a business care about is will XYZ road to my NJ warehouse be frozen/filled with snow. This will probably result in some sort of tradeoff - either I accept a more liquid market that carries basis risk, or I attempt to bootstrap some bespoke market.

> Another question is on the privacy side - by default, SMB's insurance policies are private. However, PM orderbooks are public - this could be how something like the NYC bar's hedge is surfaced and doxxed. This might be resolved through some pooling mech.

> Finally, one interesting angle is regulatory. SMBs and other companies may be legally obligated to buy certain forms of insurance (eg. workers' insurance, auto insurance). So even if on a mechanism level PMs can fulfill some insurance functionality, SMBs are still legally required to retain insurance.

Overall, using PMs to fulfill insurance criteria is a super super interesting evolutionary direction + research focus, but we're still super early and the idea still needs to be proven at scale. Excited to see more experiments by @lzminsky and others in this area!

Lovely Implementation of Tauric research. I have personally backtested their framework and yielded a better than buy and hold result. This version provide a zero cost pipeline when implement locally with Claudecode

I built an AI stock analysis pipeline that costs $0 in API fees. This work is an extention on TauricResearch/TradingAgents. It use your claude code subscribtion and using CLI to run the analysis.

Main function:

Deploys 12 specialized agents — analysts, researchers, a trader, risk team & portfolio manager — all debating before issuing a BUY / HOLD / SELL verdict.Runs entirely through your local Claude Code session. No API key needed.🧵👇

How it works: Analyst Team → Research Debate → Trader → Risk Debate → Portfolio ManagerEach agent has one job and argues with the others. The Portfolio Manager makes the final call with a full written rationale.

🔗 https://t.co/tByO6sCW20

Up for discussion. Love your qualitative part, but I feel like the data supported doesn't tell me whether buyback sucks or works. It is apparent that there are many factors influencing token prices as u listed and having buyback doesn't guarantee the token price urge. Do you think there will be a better and a more statistically significant way of reaching your conclusion? Trailing 12 months is flawed as the entire altcoin market is down. Is there a way of doing A|B testing across different time frames or having some regression model showing buyback is either an insignificant factor or giving negative return

Have studied Circle few months ago. I don’t doubt its ability to grow and make revenue. Q3 shows a %580 YoY increase in USDC Transaction Volume. Current price is $76. Bullish in long run.

My first quick recap of Circle’s recent earnings report is now up on my personal site:

My Take: Short-term bear momentum and long-term structured bull.

Great Disconnect: Market Panic vs. Circle’s Q3 Fundamentals | by MoonLake | Nov, 2025 | Medium https://t.co/BETEHQQhSS