Let's run some numbers on $POD, and address why the FDV is truly a 'meme' in this case:

At its last datagen peak the network processed 3.5B output tokens/day across a 600-GPU fleet. With V2 unlocking meaningful per-GPU efficiency gains, 10B output tokens/day is a reasonable conservative target to anchor against. Below is what both look like at OpenRouter-rate pricing ($0.80 per 1M output, $0.15 per 1M input) and the historical 20:1 input:output ratio that real agent workloads tend to land on.

Note: this is a single-model exercise (Qwen 3.6 35B economics). In practice the network will serve a basket including Gemma 31B and 26B, which are faster and cheaper, broadening the addressable demand pool. So the math here is conservative on the revenue side.

Current 3.5B output/day:

Output revenue: $2,800/day

Input revenue: $10,500/day

Gross revenue: $13,300/day, all of which routes to POD buybacks

Node emissions ($0.50 per 1M output): $1,750/day

Buyback-to-emissions ratio: 7.6x (!)

For every $1 of POD paid out as emissions, $7.60 of POD is being bought back off the market. Most of those emissions are paid bonded, with a 20% fee on liquid claims routing back to stakers, so even the share that does hit the float gets partially absorbed by the same flywheel.

Against ~$10M in circulating market cap, that means current-rate buybacks already represent roughly 4% of the float being bought back annually. Post-V2 scenario, closer to 13%. On the float that's actually tradeable, the bid is structurally large.

Annualised current: ~$4.85M gross to buyback against a $100M FDV. About 21x.

Post-V2 conservative 10B output/day, same prices and mix:

Gross revenue: $38,000/day → ~$13.9M/year to buyback

Node emissions: $5,000/day

Buyback-to-emissions ratio: 7.6x (constant, the design scales linearly)

For benchmark, HYPE currently generates around $2.54M/day in fee-driven buybacks, $927M annualised, against a $58B FDV. The market values that buyback flow at roughly 63x.

Apply the same multiple to POD's current 3.5B-per-day economics and the implied FDV is roughly $300M, about 3x current. Apply it to the post-V2 10B scenario and you land closer to $880M, around 8.8x current.

The 10B figure is a working assumption of what V2 should unlock; the real number could be lower or higher and needs to be seen once V2 ships and the API is live. But the 7.6x buyback-to-emissions ratio is what makes the FDV stop mattering the way most people assume it does. It is not a token waiting to dump on you. It is a token the protocol is mechanically buying back faster than it is being issued.

2/ Train yourself to go from 10 to 40 to 100 hours of focused work a week. I did this for months building an automated trading system from scratch. 5am-10pm 7days/week

99% of people need #WorkLifeBalance or whatever, and that's great. But I'm talking to the people on a mission.

Introducing USVC - a single basket of high-growth venture capital, for everyone.

No accreditation required, SEC-registered, and a very low $500 minimum.

Includes OpenAI, Anthropic, xAI, Sierra, Crusoe, Legora, and Vercel. As USVC adds more companies, investors will own a piece of that too.

Liquidity typically comes when companies exit, but we’re aiming to let investors redeem up to 5% of the fund every quarter. This isn’t guaranteed, but if we can make it work, you won’t be locked up like in a traditional venture fund.

It runs on AngelList, which already supports $125 billion of investor capital.

And I’ve joined USVC as the Chairman of its Investment Committee.

—

Go back to the 1500s, you set sail for the new world to find tons of gold - that was adventure capital.

Early-stage technology is the modern version. It says we are going to create something new, and it’s risky. It’s daring.

But ordinary people can’t invest until it’s old, until it’s no longer interesting, until everybody has access to it. By the time a stock IPOs, most of the alpha is gone. The adventure is gone. Public market investors are literally last in line.

This problem has become farcical in the last decade. Startups are reaching trillion dollar valuations in the private markets while ordinary investors have their noses up to the glass, wondering when they’ll be let in.

Investing in private markets isn’t easy. You need feet on the ground. You need judgment built over years. Most people don’t have the patience to wait ten or twenty years for an investment to come to fruition.

But there is no more productive, harder-working way to deploy a dollar than in true venture capital.

USVC enables you to invest in venture capital in a broad, accessible, professionally-managed way, through a single basket of innovation, focused on high-growth startups, at all stages.

It is how you bet on the future of tech: the smartest young people in the world, working insane hours, leveraged to the max, with code, hardware, capital, media, and community. Your dollar doesn’t work harder anywhere.

There is an old line - in the future, either you are telling a computer what to do, or a computer is telling you what to do. You don’t want to be on the wrong side of that transaction.

USVC lets you buy the future, but you buy it now. Then you wait, and if you are right, you get paid.

Get access here:

https://t.co/pAj1sqUsG0

On OKX, we can see a large buyer stepping in during the sell-off. Someone was either arbitraging the price difference between OKX and other exchanges or accumulating a huge amount of ETH.

It's inspiring to see tens of thousands of community members secure life-changing wealth as part of the Hyperliquid genesis event. Importantly, none of these people were insiders. They:

1) believed in the vision for a better financial system when no one else would

2) acted on that conviction by using and building upon the nascent technology, bootstrapping an unstoppable financial network

The Hyperliquid genesis pays homage to the original ethos of Bitcoin: ownership goes to the believers and doers, not rent-seeking insiders.

For all you early believers, thank you for the unwavering faith and support. Hyperliquid would be nowhere without you all. I'm grateful and honored to be building alongside you.

--

Looking back, we've come a long way. But looking ahead, there's so much further to go.

Finance is humanity's greatest invention. It is the only effective way to coordinate human effort across time and space. Yet, the legacy financial system contradicts its underlying goal of empowering individuals:

- it is opaque and centralized

- it is owned and operated by privileged insiders

- it doesn't embrace technological innovation to better serve users

Hyperliquid is the evolution of finance. And Hyperliquid has not succeeded until it houses all of finance. If you're reading this now, you're still early. The new financial system welcomes you with open arms.

once upon a time @cobie raided the stream of @melabeeofficial, then taught her how to make a wallet while she was singing.

this is her live reaction as people donated $250K, including $100K from a single person.

enjoy this thread of crypto’s most wholesome moments… (continued)

1/

The Ethereum ETFs are set to go live on July 23rd. There are a number of dynamics present with the ETH ETF that have been overlooked by the market & which were not present with the BTC ETF. We take a look at flow predictions, ETHE unwinds & the relative liquidity of ETH:

The fee structure of the ETF ETFs is similar to that of the BTC ETFs. Most providers are waving their fee for a specified period, to help accumulate AUM. As was the case with the BTC ETFs, Grayscale has the maintained their ETHE fee at 2.5%, an order of magnitude larger than other providers. The key difference this time around is the introduction of the Grayscale mini ETH ETF, which previously wasn’t approved for the BTC ETF.

The mini trust is a new ETF product by Grayscale that originally disclosed at 0.25% fee, similar to the other ETF providers. Grayscale’s idea here is to capture a 2.5% fees on lazy ETHE holders, whilst funneling more active and fee sensitive ETHE holders to their new product, instead of having funds siphoned to low fee products such as Blackrock’s ETHA ETF. After the other providers undercut Grayscale’s 25bps fee, Grayscale came back and reduced the mini trust fee to only 15bps, making it the most competitive product. On top of this, they moved 10% of ETHE AUM to the mini trust and gifted ETHE holders this new ETF. This transition was completed at the same basis, meaning it was not a taxable event.

The resultant effect is ETHE outflows will be more muted as compared to GBTC as holders simply transition to the mini trust.

Now we look into flows:

There have been many estimates for the ETF flows, some of which we have highlighted below. Taking the estimates and standardizing them yields an average estimate in the $1bn/month region. Standard Chartered Bank offers the highest estimate with $2bn/month, while JP Morgan is on the low end at $500m/month.

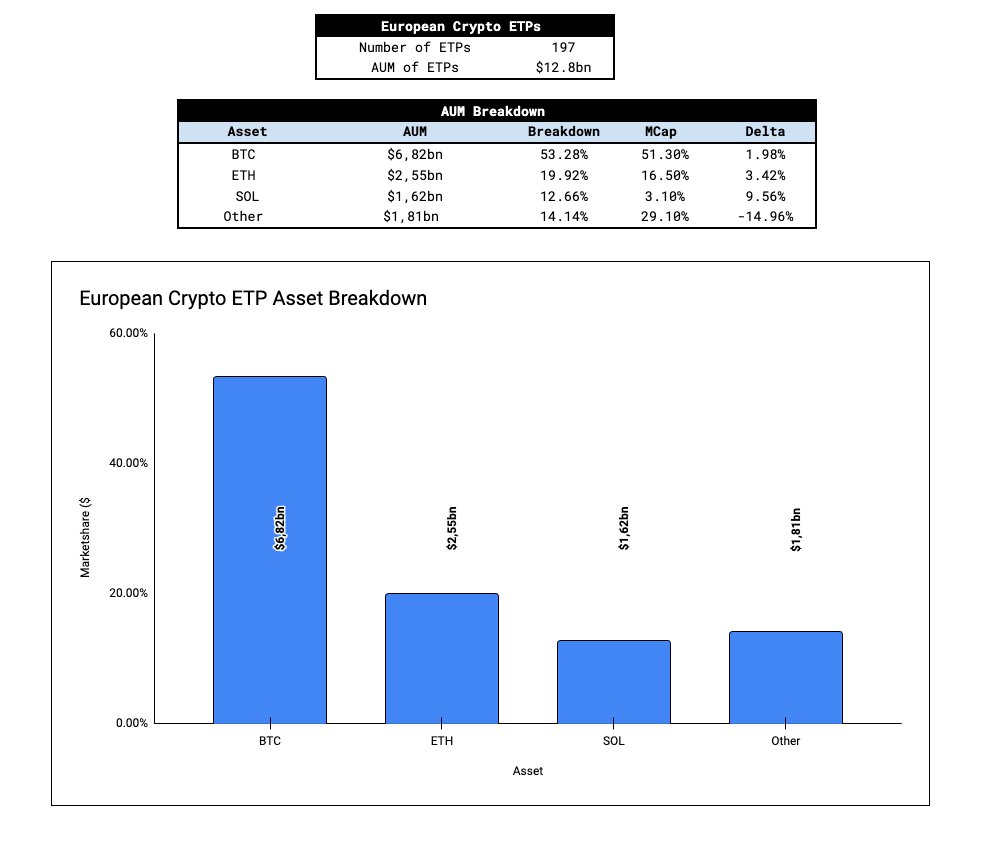

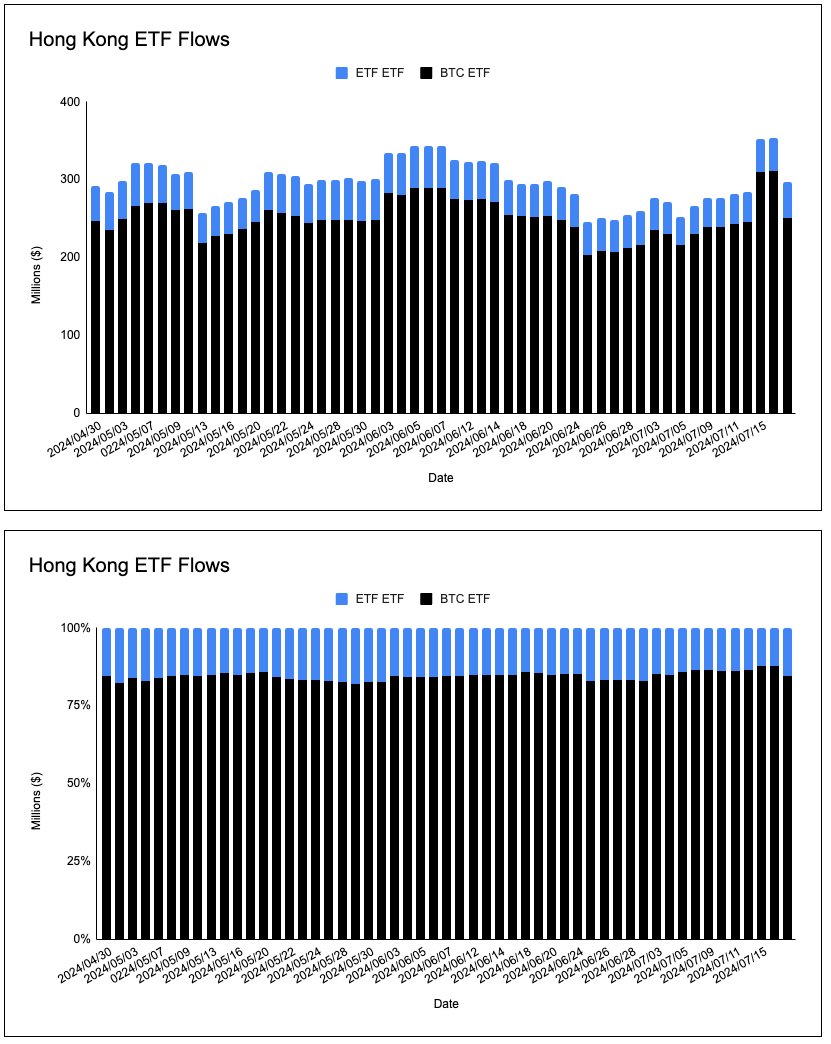

Fortunately, we have the help of Hong Kong and European ETPs as well as the closing of the ETHE discount in order to help estimate flows. If we take a look at the breakdown of AUM in HK ETPs, we arrive at two conclusions:

1. The relative AUM BTC and ETH ETPs are overweight BTC vs. ETH, the relative market cap sits at 75:25, while the AUM sits at a ratio of 85:15.

2. The ratio of BTC v ETH in these ETPs is reasonably constant and in-line with the ratio of BTC market cap to ETH market cap.

Looking at Europe, we have a larger sample size to look at – 197 crypto ETPs with a cumulative AUM of $12bn. After we boil down the data, we find that breakdown of AUM in European ETPs is broadly in line with the market cap for Bitcoin and Ethereum. Solana is over allocated relative to its market cap, this comes at the expense of ‘Other crypto ETPs’ (Anything not BTC, ETH, or SOL). Setting Solana aside, a pattern is beginning to emerge – the breakdown of AUM globally between BTC and ETH broadly reflects a market cap weighted basket.

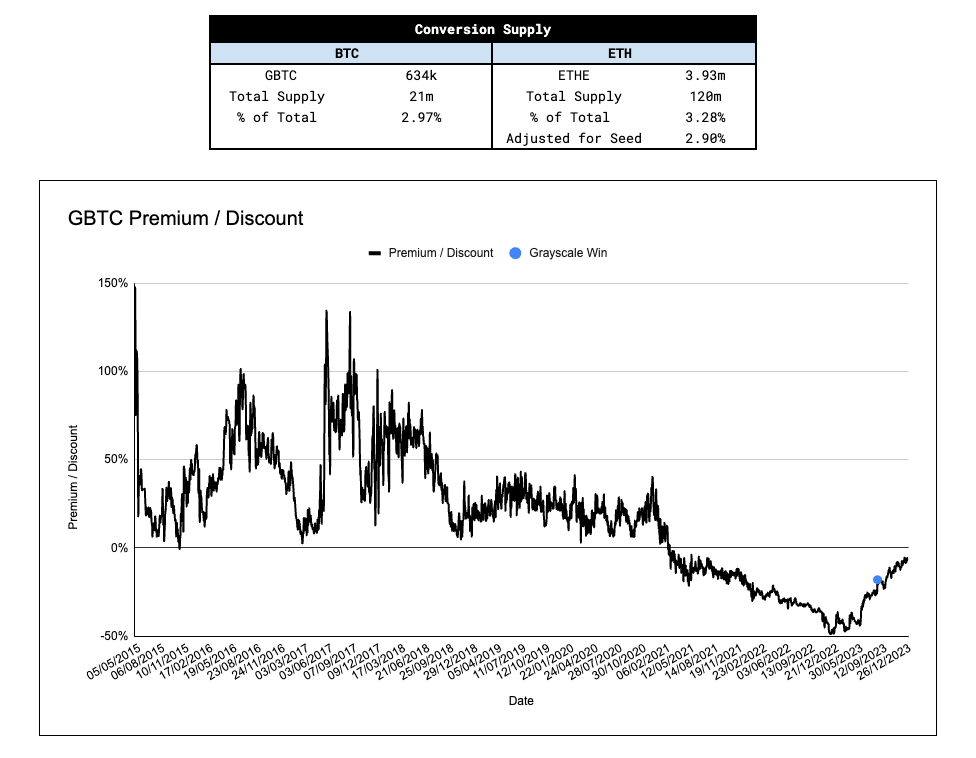

It’s important to consider the potential for ETHE outflows considering the GBTC outflows were the genesis of the ‘sell the news’ narrative. In order to model potential ETHE outflows and its affect on price, it’s useful to look at % of ETH supply in the ETHE vehicle.

Once adjusted for Grayscale mini seed capital (10% of ETHE AUM), the proportions of ETH supply as a function of total supply existing in the ETHE vehicle is similar to that of GBTC at launch. It’s unclear what proportion of GBTC outflows were rotational vs. exit, however if we assume the proportion of rotational flows to exit flows is similar, ETHE outflows have a similar impact on price to GBTC outflows.

Another key piece of information that most are overlooking is the ETHE premium/discount to NAV. ETHE has been trading within 2% of par since May 24th – whereas GBTC first traded within 2% of NAV on Jan 22nd, only 11 days after GBTC converted to an ETF. The approval of the spot BTC ETFs and their effect on GBTC was slowly priced into the market, whereas the ETHE discount to NAV trade has been far more telegraphed with the story already written with GBTC. By the time the ETH ETFs go live, ETHE holders will have had all of 2 months to exit ETHE around par. This is a key variable that will help stem the ETHE outflows, specifically the exit flows.

Continued in the next tweet >

I'm hopelessly optimistic.

But if I were to steelman the bear case:

- BTC ETF flows are slowing and reversing. The institutional sales machine is ramping up slower than expected

- ETH ETF flows could be minimal (initially). Plus there will be outflows from ETHE redemptions.

- The market has already frontrun the ETH ETF Flows (up 15% since ETF news). S1 approval is widely telegraphed. Who else is left to buy?

- No increase in CME OI on ETH after the announcement suggests a lack of TradFi interest

- An ETH ETF without staking is an inferior product

- BTC double top at $69K?

- Stock markets are at ATH while the economy is sluggish: Nasdaq could reasonably correct 10 - 20%.

- Smart, respectable VCs are writing thought pieces to express bearishness, which could influence others.

It’s easy to get spooked by all these factors, sell everything, and walk away. I’ve considered it too. Sentiment on CT is at its lowest, and top influencers are divided. This is probably the most challenging time in the markets this year.

In times like this, I keep all the risks in mind, extend my timeframes (zoom out), and stay ready to adjust quickly when needed.

I always look ahead towards the future, and it's going to be a bright one for crypto.

I’m on Team Bull — I believe we will slowly climb a wall of worry in the coming weeks.

At the end of the day, I ask myself:

“Can I risk being underexposed to the industry I’ve dedicated so much of my life to over these years?”

For me, the answer is clear.