A PM that I work with found an article on Diamond Quanta's commercialization approach in the emerging diamond semiconductor industry. Below, I synthesize the article with the recent $SOTK / Diamond Quanta collaboration announcement.

In a January 19, 2026, feature for Power Electronics News, interim editor-in-chief Aalyia Shaukat surveyed the emerging diamond semiconductor industry and its potential to push beyond today's wide-bandgap (WBG) materials. The article situates diamond among a new class of ultra-wide bandgap (UWBG) semiconductors whose bandgap exceeds 4 eV, offering theoretical advantages over both GaN and SiC in thermal conductivity, critical electric field strength, and high-temperature operation. While GaN-on-Si is scaling toward 300 mm wafers and SiC dominates at voltages up to 3.3 kV, diamond remains largely in the R&D phase, with the industry still working to reliably produce 4-inch single-crystal wafers, the threshold widely seen as necessary for mass production.

Shaukat profiles the growth techniques of the major players, ranging from mosaic homoepitaxy to heteroepitaxial step-flow processes. The piece then focuses on Diamond Quanta, founded in 2024 by Adam Khan (previously of Akhan Semiconductor), which takes a different approach entirely: growing polycrystalline diamond on silicon at low temperatures compatible with standard CMOS processing. In an interview at CES 2026, Khan described how the company's partnership with Japan's ExtenD Corporation and equipment integration by Heller Industries enabled the production of 300 mm diamond-on-silicon wafers, and how a laser densification process developed with Lawrence Livermore National Labs smooths the rough diamond surface for direct bonding. Diamond Quanta's near-term launch product is Adamantine Optics, a scratch-resistant diamond glass for AR displays and smartphones, while thermal interface materials and diamond interposers represent the next commercial steps. Active-doped diamond power devices, which Khan says have already demonstrated stable PIN diode operation from 400 °C to 600 °C, well beyond SiC's performance dropoff, are targeted for commercialization by 2030.

This trajectory gained further momentum in March 2026 when $SOTK announced a technical collaboration with Diamond Quanta to integrate its precision ultrasonic coating technology into Diamond Quanta's manufacturing workflow, supporting repeatable thin-film deposition and multilayer integration across engineered diamond applications. The partnership is significant because it aims to strengthen process repeatability, film uniformity, and manufacturability as Diamond Quanta advances its materials platform toward OEM qualification and scalable manufacturing environments. In practical terms, the approach aligns with Diamond Quanta's broader strategy of commercializing defined process modules rather than raw materials, reinforcing its IP-led, fab-light model as it works toward OEM qualification and strategic manufacturing partnerships. For Sono-Tek, the collaboration extends its ultrasonic coating expertise into a high-growth advanced materials segment; for Diamond Quanta, it adds a proven precision deposition capability to its standardized process architecture, another concrete step toward making engineered diamond manufacturing compatible with existing semiconductor toolchains and, ultimately, toward Khan's stated goal of making diamond as accessible as silicon.

#QuantumComputing #CHIPSAct #SOTK #AdvancedManufacturing #Semiconductors #SmallCaps #DiamondSemiconductor #DeepTech #QuantumTechnology

$SOTK Why medical devices re-rate the whole business.

Another day, another $SOTK post. You might wonder: how can there be so much to say about a company with only $20 million in revenues?

The answer is that a lot is going on.

I've invested in microcaps for over 60 years; other people's money and my own. I've stuck with it because that's where the money is made.

What I post on X is what I've done for decades: find an idea that looks interesting, do the deep-dive due diligence, then stay on top of everything that touches the company.

For years I just filed my observations away. Then I started writing them down; it forced me to be thorough. X simply gave the notes somewhere to go.

Of all the high-conviction, all-in positions I've owned, $SOTK gives me the most to write about. That tells you something: a lot is happening, and this is not a one-trick pony.

I like that.

Obviously, I am long $SOTK. Do your own DD. If you find anything interesting, pass it along.

Maybe I am not "... so far off the trail that" ... I'm "somewhere between the f**king weeds and the woods."

A key question for my $SOTK thesis:

Is the knowledge moat built on accumulated process recipes, application data, and customer-tuned parameters across deployments proprietary enough to compound faster than a well-capitalized competitor could replicate it?

If yes, each deployment isn't just revenue. It's a data point that makes the platform more defensible.

This is the mechanism Thomas Laffont described for SpaceX at the All-In Liquidity Summit last week: valuation rises faster than launch frequency because each launch extends the perceived distance to saturation and deepens the monopoly position itself.

The SOTK analog is quite precise:

→ Semi/AI chip wins = $SPCX compounding launch monopoly (proven, recurring, entrenchment deepens with each node)

→ Medical device qualifications = the Starlink leg (higher ASP, FDA re-qualification barrier is 3–5 years vs. 18 months in semi, non-cyclical demand)

→ Clean energy /GaN/ diamond-on-glass for quantum represents option value that comes along for free

Laffont's centacorn data: once a company crosses a $100B valuation, it has a 31% chance of reaching $1T because the moat compounds faster than valuation does.

SOTK is orders of magnitude smaller. But the *structure* is identical. Winner-take-all at the process step level. Winner-take-most at the niche equipment level. Each medical device qualification is a local monopoly lasting at least a decade.

The market isn't going to price the system sold. It's going to price what that system reveals about how far the platform can compound before it saturates.

That's the re-rating thesis.

$SOTK $SPCX

"You're so far off the trail, you're somewhere between the f**king weeds and the woods."

That was the response I got from a senior semiconductor analyst at Alex Brown & Sons sometime in the early 1990s, when I phoned him with a speculative view on where the best technological advances were intersecting with the best investment opportunities in his coverage universe.

I thought his response was hilarious. After all, being a hunter and trapper raised on a fruit farm in the Mid-Hudson Valley, I know for certain that you can find some very interesting stuff somewhere between the weeds and the woods. It is the same when you are looking for investment opportunities.

He must have tried that response on someone who didn't find it funny, because he went missing from the firm a couple of months later.

In this vein, I give you this table.

$SOTK SpaceX

$AGX I would tread carefully here.

Global orders for heavy-duty gas turbines (greater than 30 MW) hovered between 45 GW and 56 GW annually from 2010 to 2016. In 2017, orders plunged to 34 GW, and by 2018, they hit a cyclical bottom of roughly 29 GW.

A reminder for gas turbine investors: this market can turn violent, fast.

GE (2016–2018): Overestimated thermal power demand → CEO ousted after 14 months → $23B write-down → 74% market cap wiped out ($193B gone)

Siemens (2017): Nearly 7,000 layoffs, 6,000+ in power & gas alone. A board member called the conventional power plant market "burning to the ground."

Right after this was the time to start accumulating $AGX and wait patiently for the big payoff (20-Bagger). Twenty X in 8 years. It is amazing how good companies get lucky.

The gas production lag (and #TTF price rise) and sulfur price spike are working together (possibly against each other) right now in $NRT ($7.86), and the interaction over the next 12 months is worth mapping out carefully.

Natural gas is roughly 90% of the royalty base, but NRT never receives today's gas price. Royalties are calculated using the German Border Import Gas Price index, a government-compiled figure that takes months to publish, with quarterly true-ups to reconcile. A price spike today does not hit NRT's accounts for 3 to 6 months. That lag is currently a significant tailwind. The strong European gas pricing of spring 2026 is still flowing through the system and will continue to do so into Q4 FY2026 and Q1 FY2027.

Sulfur works on completely different mechanics. The Mobil Agreement pays 2% of gross receipts with virtually no cost deductions, so price changes hit the Trust almost immediately with no lag buffer at all. When European sulfur moved from roughly 100 euros per tonne at the 2024 floor to 250+ euros now, driven by the Hormuz blockade, Chinese export bans, and contracting Western European refinery output, it dropped almost directly to NRT's bottom line. Sulfur royalties went from $70K in H1 2025 to $472K in H1 2026, up 572%, lifting sulfur's share of total income from 2.3% to 10.2%. The per-unit distribution went from $0.24 to $0.44 for the half-year.

Here is the counterintuitive dynamic sitting underneath all of this. Declining Oldenburg gas production physically reduces sulfur output because the two are molecularly inseparable. But that same production decline tightens local German sulfur supply, forcing industrial buyers who cannot source from the Middle East or China to bid aggressively for a shrinking domestic pool. The geological decline of the fields is simultaneously compressing volume and supporting the price premium. That is an unusual self-reinforcing setup for a royalty trust.

The Grossenkneten shutdown temporarily breaks that dynamic. 50 days starting August 1, 2026. Zero processing means zero sulfur royalties, and unlike gas, there is no lag to soften it. The hit is immediate. But the window splits across two fiscal quarters, 31 days into Q4 FY2026 and 19 days into Q1 FY2027, so neither distribution takes the full impact. Critically, both quarters will simultaneously be receiving delayed gas true-up payments from the spring and summer 2026 pricing peaks. The gas lag that built up during the year's strongest pricing period arrives in the Trust's accounts exactly when sulfur goes dark. That is not a coincidence of design; it is just how the timing falls, but the effect is a genuine cushion.

The 12-month picture from here: Q4 FY2026, paid in November 2026, absorbs the larger portion of the sulfur gap but receives the strongest gas true-up support. Q1 FY2027, paid in February 2027, captures the final 19 shutdown days, but the plant is back online by then, and late-summer gas lag begins to arrive. Q2 FY2027, paid in May 2027, is where the picture clarifies. If sulfur prices hold anywhere near current levels and gas benchmarks have not collapsed, that quarter should reflect a cleaner run rate with both streams flowing and the lag pipeline refilling from the back half of 2026.

Distributions could decelerate from the $0.22-per-quarter H1 pace, but then accelerate substantially (reaching over $0.35) out a few quarters. The question is by how much and for how long. The fiscal split and gas lag offset each other, arguing against a sharp drop. The key numbers to watch are the Q4 FY2026 royalty receipts reported in October/November 2026 and the September plant restart confirmation. Those two data points will tell you whether the H1 momentum can be rebuilt into next FY.

“This brings me to the point of this article: we have now entered the point of no return. Since the beginning of the conflict, my core thesis has been simple: every day that passes without a resolution increases the probability that there is no resolution.

Emotional and cognitive biases prevent people at the top from reaching a diplomatic resolution when the cost of anchoring becomes too great. From the US’s side, leaving now would look like a total strategic defeat, while for the Iranians, the cost of enduring the current conflict has already been spent; you will anchor down and outlast your adversary.

So to assume that the Strait of Hormuz will reopen by June 1 is just wishful thinking. I am somewhat relieved that the sellside community has not analyzed what it would do to oil prices if the Strait remains closed. When that day comes, it could be a contrarian signal to start exiting our oil long exposure. But judging by the reports I went through the past week, we are quite a ways from that scenario.”

"You're so far off the trail, you're somewhere between the f**king weeds and the woods."

That was the response I got from a senior semiconductor analyst at Alex Brown & Sons sometime in the early 1990s, when I phoned him with a speculative view on where the best technological advances were intersecting with the best investment opportunities in his coverage universe.

I thought his response was hilarious. After all, being a hunter and trapper raised on a fruit farm in the Mid-Hudson Valley, I know for certain that you can find some very interesting stuff somewhere between the weeds and the woods. It is the same when you are looking for investment opportunities.

He must have tried that response on someone who didn't find it funny, because he went missing from the firm a couple of months later.

In this vein, I give you this table.

$SOTK SpaceX

Nobody talks about the lonely part.

“People always talk about talent, but what they don’t wanna talk about is loneliness. The empty gym…”

- Larry Bird

Confidence.

Nobody gives it to you.

You build it rep by rep.

In the gym when no one’s watching. https://t.co/4zIilqfX40

As you likely know, John Boyd's Destruction and Creation is one of the most influential essays ever written on strategy, innovation, learning, and decision-making. It became the philosophical foundation for his later work on the OODA Loop and maneuver warfare.

In the essay, Boyd argued that to create a better understanding of reality, we must first destroy our existing mental models

The market punishes people whose mental models become stale.

Boyd concluded that no model can ever perfectly represent reality. Therefore, every model eventually requires revision or replacement.

The investor who clings to the old framework loses.

The investor who can destroy a formerly successful thesis and rebuild a better one gains an advantage.

Boyd would argue that the biggest enemy of performance is attachment to yesterday's mental model. So, do I.

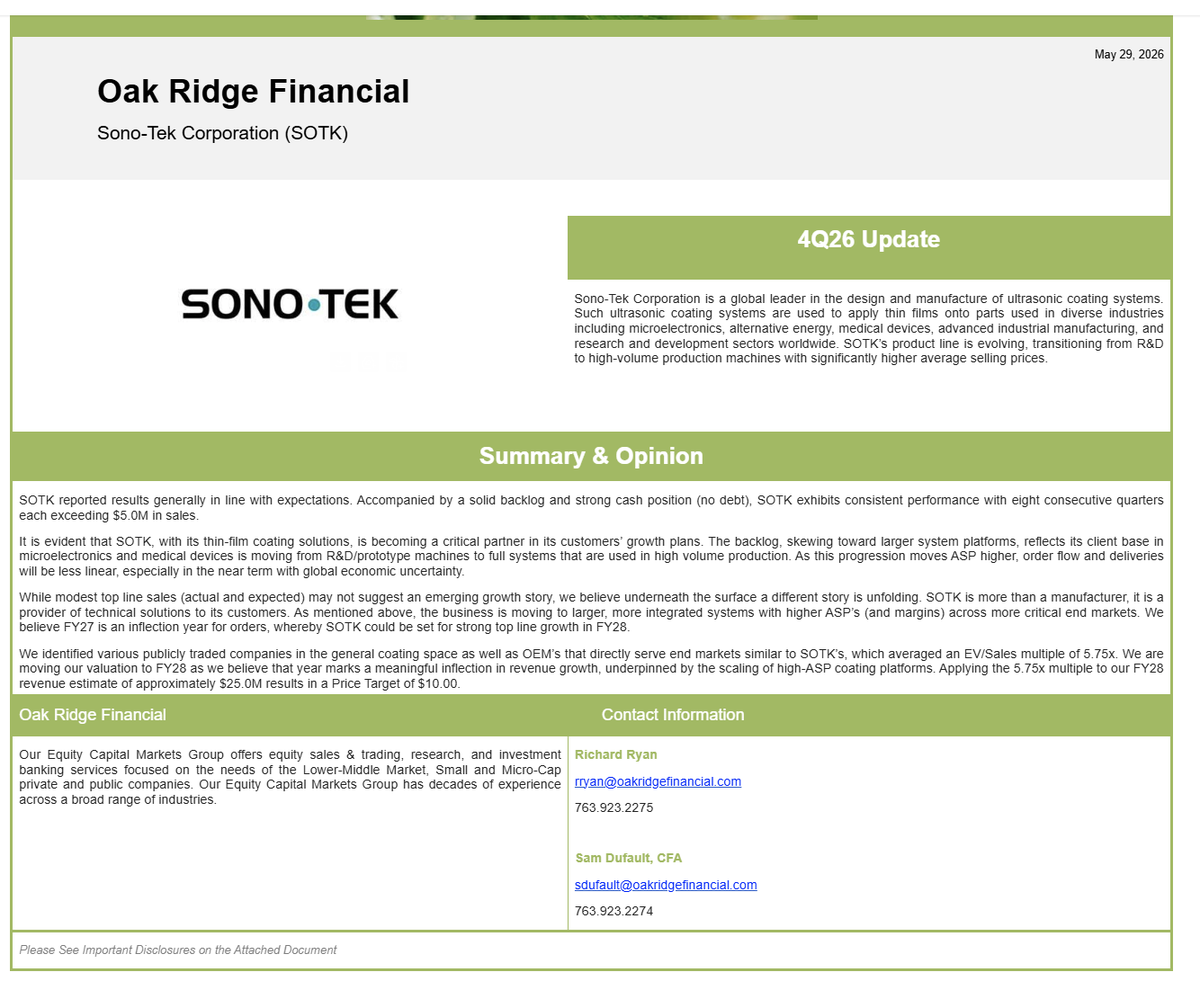

$SOTK price target RAISED to $10 from $8.50 by the analyst who knows the company's business best.

Dick Ryan has given me some of the best 10-baggers. He is highly experienced (feet on the ground) and knowledgeable.

"FY27 Guidance: Management anticipates continued revenue growth and profitability in 1H FY27 on a YoY basis, driven by expanding demand in the medical sector and continued adoption of high-ASP, production-scale coating systems across multiple end markets. Total FY27 revenue is currently projected to be relatively flat to modestly higher compared to FY26 as visibility beyond the first half remains limited due to continued uncertainty in certain clean energy sectors and the timing of high ASP customer orders, which can create significant shifts in quarterly delivery timing.

Valuation: Based on our estimates, we are affirming our Buy rating and increasing our PT to $10.00 from $8.50. Our revised PT is based on FY28 estimates (previously FY27 estimates) and an EV/Sales multiple of 5.75x, reflecting peer group valuations and our expectation that higher-ASP production systems will begin scaling meaningfully in FY28."

I have studied everything, Colonel John Boyd (OODA). I was never in the military. I worked at the Knolls Atomic Power Laboratory (KAPL), where I met Admiral Hyman Rickover (Father of the Nuclear Navy), who I believe made my draft notice disappear (4F medical without taking the exam) during the Vietnam War, but I will never know. Rickover shared a personality with Boyd, both determined, cantankerous, and brilliant.

I am not planning on buying anything today, not yet, so I will make another $SOTK post to get my point across: $SOTK's medical-device coating market is set for an expansion thrust.

Zwitterionic polymers are the next generation of blood-contacting device coatings | What's been missing is a deposition process that can apply these coatings uniformly, rapidly, and at scale to geometrically complex catheters without the webbing and thickness variability that make dip coating inadequate.

Here is the story: $SOTK is not a legacy industrial company. It's a high-technology platform business — one that happens to be embedded in some of the most sophisticated medical manufacturing on the planet.

Sono-Tek's ultrasonic coating systems are already the backbone of global drug-eluting stent production. A large share of the world's commercial coronary stents are coated on SOTK equipment. That's not trivial; that's a dominant market position in a life-critical manufacturing process.

What makes SOTK unusual is its span.

It operates across the entire innovation pipeline from the university lab bench to full-scale commercial production:

→ R&D: 1,000+ ExactaCoat systems installed at universities and research institutions worldwide. When scientists develop new coating chemistries, they often do so on SOTK equipment.

→ Process development: the same platform scales to pilot production, with parameters that transfer directly, meaning the regulatory validation work follows SOTK into the next stage.

→ Commercial manufacturing: the MediCoat production systems take those validated processes into ISO-classified, FDA-submission-ready high-volume production.

This R&D-to-production flywheel is not theoretical. It's how $SOTK became the stent coating standard. And it's how the next opportunity is already being seeded.

That next opportunity: zwitterionic antifouling coatings.

Zwitterionic polymers are the next generation of blood-contacting device coatings, achieving near-zero protein fouling by mimicking the chemistry of cell membranes. The science is mature. The clinical case is compelling. What's been missing is a deposition process that can apply these coatings uniformly, rapidly, and at scale to geometrically complex catheters without the webbing and thickness variability that make dip coating inadequate.

Ultrasonic spray is that process. And SOTK already lists zwitterionic antifouling coatings as a supported application on its MediCoat catheter coating systems.

The university labs working on these coatings today are almost certainly using SOTK equipment. When those coatings reach clinical and commercial stages, the process parameters and the regulatory validation follow SOTK into production.

Three converging tailwinds:

IVL market growing at ~15% CAGR (J&J/Shockwave alone has 30+ active catheter R&D programs)

Catheter coating market growing at ~10% CAGR, with zwitterionic coatings the fastest-growing segment.

FDA pressure on dip coating is structurally accelerating the shift to ultrasonic spray

A little more color on my thinking on the $SOTK semi exposure. I have long but rather thin experience with the semi-business; far from being an industry investment veteran. But have been an interested observer since the industry's inception.

Also, I managed a sizeable book of business at AB when Qualcomm's December 1991 IPO took place and received a nice allocation of stock for customers. Alex. Brown & Sons was the lead managing underwriter. Those were the good ole days.

I also had a bunch of clients who were in the semi business one way or another, and they taught me quite a bit. One of my favorite clients invented the cell phone, and I invested in his companies. Those were the good ole days, too.

My $SOTK bet, at the moment, is much more dependent on advances in medical devices and testing, which I have studied in great depth. That will surely carry the ball for the next few quarters. The amount of innovation taking place is amazing, and $SOTK is the enabler, from R&D to pilot lines, and full production equipment (everyone knows them, respects them, and is cheering them on). I expect a raft of orders over the next few months, fully in line with the "transformation" I have been posting about.

So, if Semi is big, and I agree that it is, then medical is gigantic, relative to the size of this company.

You nailed the semi-equipment aspect of $SOTK's business. They have deep customer relationships, and what is a narrow slice of their addressable market will broaden significantly and grow by leaps and bounds as offerings created by partnering arrangements already agreed to are ready to roll later this CY.

$SOTK

One of the most asymmetric small-cap semiconductor equipment stories I’ve found recently.

150$ stock chilling under $6. Testing 52 week highs.

Repost. Bookmark. Subscribe 1$.

Sono-Tek isn’t trying to compete head-on with $AMAT, $LRCX, $KLAC, $NDSN, $GGG or Tokyo Electron.

They’re attacking a niche those giants don’t dominate well.

High-aspect-ratio wafers.

MEMS.

Advanced sensors.

Complex 3D structures.

Advanced packaging.

Places where traditional spin coating struggles.

$SOTK’s ultrasonic spray technology can reduce photoresist and chemical usage by 70-95% while delivering more uniform coatings across trenches, sidewalls, deep wells, and difficult geometries.

That’s a major advantage as semiconductor manufacturers push toward increasingly complex structures.

The addressable market is large.

Photoresist processing equipment alone is a ~$2.4B market in 2026.

Broader wafer coating equipment exceeds $5B and is projected to continue growing throughout the decade.

Meanwhile wafer fab equipment overall remains a $100B+ annual industry being driven by AI infrastructure, advanced packaging, HPC chips, sensors, automotive electronics, and 300mm capacity expansion.

What’s interesting is management isn’t chasing low-dollar R&D orders anymore.

They’re actively pushing customers toward production-scale systems.

CEO Steve Harshbarger recently discussed customers initially evaluating $1M systems that eventually expand into $4M, $5M, and even $6M+ opportunities as additional capabilities are added.

At only ~$20.9M annual revenue, a single $5M-$10M order can completely reshape financial results.

Management literally stated that one significant order could increase revenue by 50%-80%.

That’s the kind of operating leverage microcap investors dream about.

Financially the company looks stronger than most names this size:

• $20.9M FY2026 revenue

• 51% gross margins

• Operating income up 81%

• Net income up 42%

• $14.8M cash

• Zero debt

• ~$9.1M backlog

• 16 consecutive years of profitability

The real catalyst may be the move toward 300mm semiconductor wafers.

Today Sono-Tek primarily serves 100mm-200mm applications.

Management is developing dedicated 300mm platforms with planned demonstrations at SEMICON Europa.

That’s where the larger semiconductor budgets live.

If they successfully qualify inside 300mm production environments, the addressable market expands dramatically.

And there are multiple AI infrastructure optionalities developing simultaneously:

• Fuel cell and electrolyzer manufacturing coatings used in next-generation power systems

• 300mm semiconductor wafer processing

• Advanced packaging and sensor production

• Diamond Quanta partnership focused on diamond-on-glass materials for semiconductor, optics, thermal management, and quantum applications

Diamond is one of the most thermally conductive materials on Earth.

As AI chips get hotter and power densities increase, advanced thermal management becomes increasingly valuable.

The market is still treating $SOTK like a niche coating company.

Management appears to be transforming it into a high-ASP production equipment provider serving medical, semiconductor, advanced materials, and industrial manufacturing customers.

This is still early.

Still risky.

Still a microcap.

But if the 300mm strategy works and a few of these larger production orders land, today’s valuation could look very different a couple years from now.

+5% today.

+14% this week.

Over $6 could get very interesting.

$UMC $POET $SIVE $MRAM $LTRX $AMD $MU $ADEA $NVDA $AMAT $COHR $OCC $MX $CODA $SMR $NVTS $INTC $TSM $AMKR

Keep eyes on this one x fam.

“Inspiration usually comes during work, rather than before it.” - Madeleine L'Engle

I came across this insight in Bespoke's Morning Lineup - June 5, 2026 edition: Weak End into the Weekend.

This quote reminds me why, at age 83, I am up at 5 a.m., 7 days a week: inspiration finds me when I'm already working.

“The financing extended by dealers to investors who want geared exposure to stocks has continued to ramp upwards this year after accelerating higher in 2025. Dealers’ balance sheet exposure to stocks in this way has tripled in only two years.” 👇🏼

- Bloomberg

$AGX I would tread carefully here.

Global orders for heavy-duty gas turbines (greater than 30 MW) hovered between 45 GW and 56 GW annually from 2010 to 2016. In 2017, orders plunged to 34 GW, and by 2018, they hit a cyclical bottom of roughly 29 GW.

A reminder for gas turbine investors: this market can turn violent, fast.

GE (2016–2018): Overestimated thermal power demand → CEO ousted after 14 months → $23B write-down → 74% market cap wiped out ($193B gone)

Siemens (2017): Nearly 7,000 layoffs, 6,000+ in power & gas alone. A board member called the conventional power plant market "burning to the ground."

Right after this was the time to start accumulating $AGX and wait patiently for the big payoff (20-Bagger). Twenty X in 8 years. It is amazing how good companies get lucky.

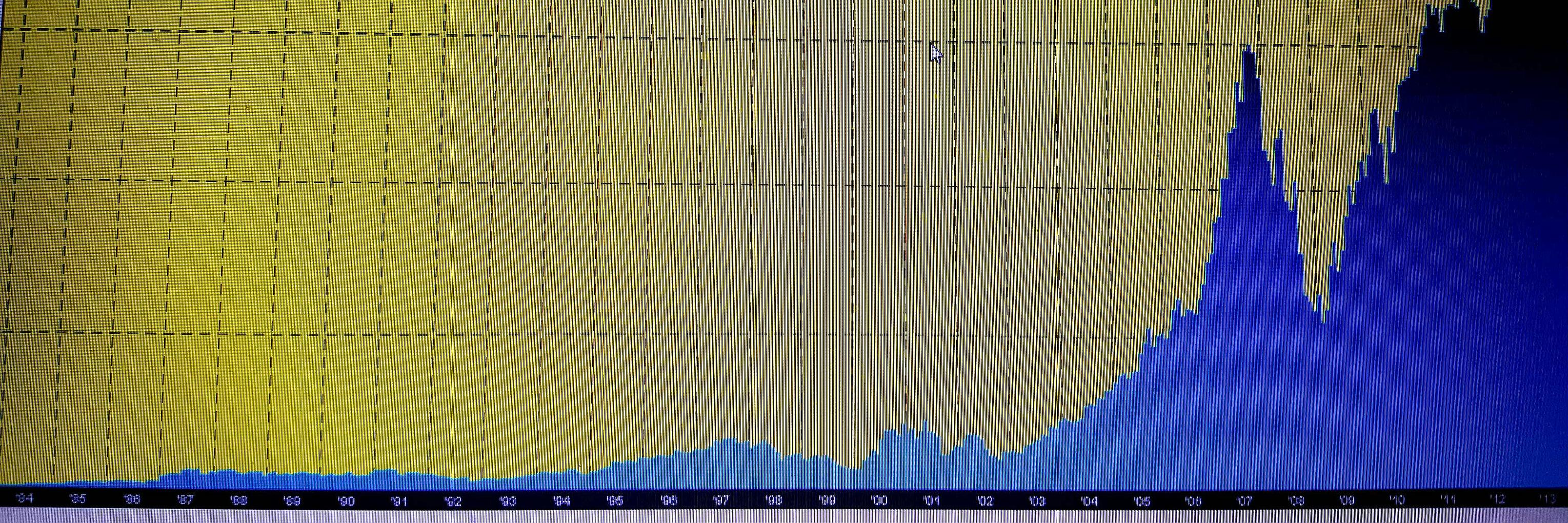

$AGX earnings just out. Annualized EARNINGS per share are now GREATER than the PRICE per share when I was buying the stock personally and professionally back in the 2009 to 2011 period. In after-hours trading, the stock is at a $750 bid, a 70-Bagger. I am happy for everyone involved. They deserve the wealth they have created.