Growth, Innovation and Value investing | Top 7 in Portfolio: $ABCL, $TSLA, $HIMS, $DLO, $AMD, $DUOL, $RKLB | Long Term Investor | No financial advice. DYOR.

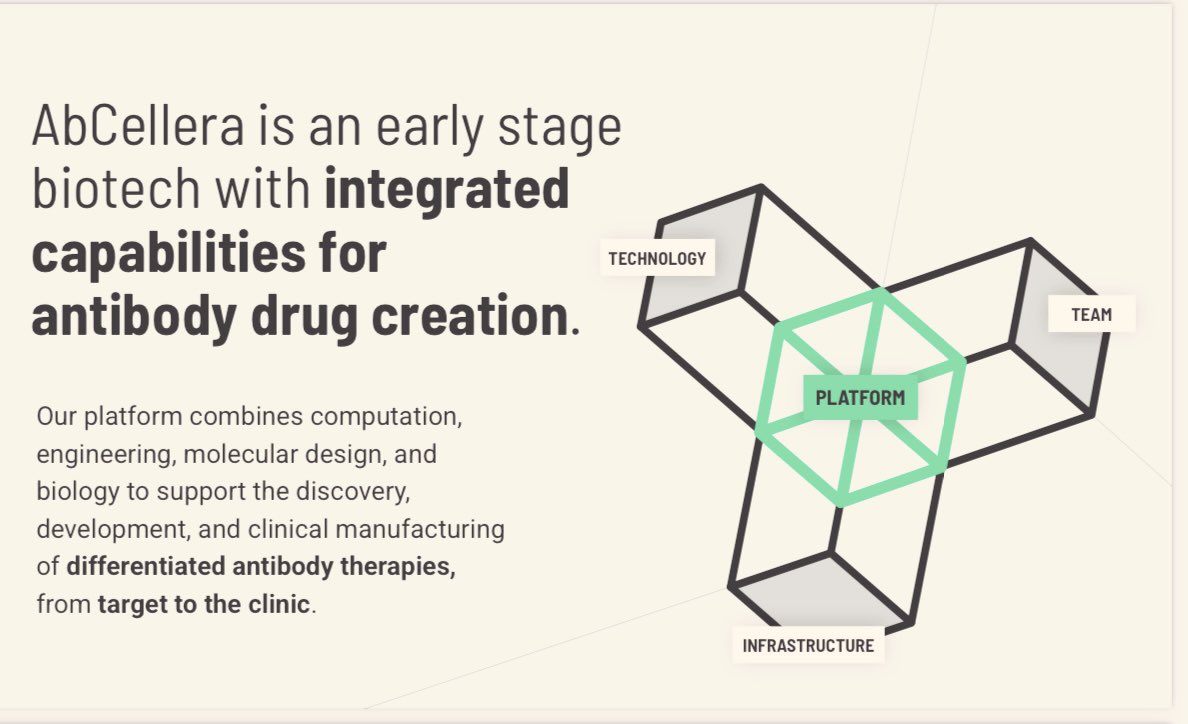

Most biotechs live or die on one drug.

$ABCL is building a platform that can discover hundreds.

Every drug they touch - win or fail - makes the platform smarter. This is software compounding applied to biotech.

Let me share 7 mental models that make $ABCL wildly misunderstood🧵

how much room does $duol have for growth from here? let’s look in to their total addressable market by starting from their target market.

$duol primarily targets:

1. language learners worldwide

2. education platforms targeting schools and universities

3. adults & professionals learning languages for work/travel

i would just be focusing on consumer market since this is the largest driver.

step 1 : population and internet penetration

a. world population (2025 estimate): 8 billion

b. internet users: 5 billion

c. smartphone users: 5 billion

step 2. targetable population:

people likely to learn a language online (students, professionals, hobbyists): 2.5 - 3 billion globally.

step 3 : affordability and willingness to pay

$duol ‘s subscription: $6 - $12/month (Duolingo Plus).

likely paying users: middle class and above. let’s assume 20–25% of targetable population can afford and are willing to pay.

paying TAM: 3 billion * 0.25 ~ 750 million paying subscribers

step 4 : penetration

even if $duol just 10-20% of this paying TAM, it will have 150 million paying subscribers. ( $spot and $nflx have approximately 300 million paying subscribers so this is realistic)

currently $duol just have approx 11 million paying subscribers. if it captures 150 million paying subscribers, that is a 15x growth from here. if it reaches 300 million paying subscribers, that is a 30x growth.

given $duol ‘s strong focus on language learning and digital education (we will see multiple verticals getting added in the app) and the world is accelerating shift toward online learning from traditional models, it is easy to imagine a future where every internet using household has at least one paying Duolingo subscriber.

feel free to pitch in/correct me wherever i am wrong.

ps: this write up is for educational purpose and should not be considered a financial advice. i am invested in $duol and it is my top position as of today.

$ABCL Just now @ BoA - @AbCelleraBio CEO Carl Hansen when asked about what the market is overlooking:

“I believe we now have best in class or best in world capabilities for some very important specific applications in therapeutic antibodies. So GPCRs and ion channels has been a heavy focus. Our first program, which I am sure we are going to talk about, ABCL635, is emblematic of that capability.

We also have developed capabilities in Multispecific and more recently in ADCs. So the platform build is highly differentiated. We can make molecules that are not ‘me too’, but are getting to some new space where there is not much competition. It is integrated all the way from discovery through now to manutacturing. That is a very unusual setup for a company.

The market I think rightly does not want you to talk about a platform. They want to see what is the outcome of the platform. So for the last two years we have been setting that up. 635 is the first example. Next year we expect another two programs of a similar profile ABCL688 and ABCL386 to come forward.

I believe over time we are going to be judged on the differentiation of the platform as seen in the assets as well as perception that we are taking that capital and that capability and directing it to bets that are going to have high return on investment.”

2026 is proving to be a defining year at Hims & Hers. More and more, we are the partner people rely on for a simpler, more personal path to feeling great.

Our Q1 2026 results are now live and they make it clear that we aren’t just growing. We’re showing the world what happens when you focus on transforming what people believe is possible in healthcare.

Here’s what to know from today’s numbers:

- We’re building momentum in the US. There are more ways than ever for customers to start – and stay – with Hims & Hers. That’s driving momentum across all of our specialties, especially weight loss, where we’re seeing near-record adoption levels since March. Our strategic shift is paying off.

- Our global reach is multiplying our impact. As we expand globally, we’ll bring more data points into our ecosystem and extend the network effects of our platform. This isn’t just good for our customers. It’s good for our partners, too, who are starting to see the potential in a high-touch, personal platform experience designed to help customers stick to their treatment plans longer and achieve their goals better than with medication alone.

- We have deeper-than-ever relationships with our customers. We’re moving beyond simply responding to symptoms by investing in areas like diagnostics that make it easier for anyone to feel their best. We’re now a trusted, comprehensive health partner that’s helping customers proactively discover early signs of conditions that may not be symptomatic yet.

- Our platform is getting harder to replicate. Our technology and data infrastructure is getting more agile and more intelligent with tens of millions of customer touchpoints. We power the end-to-end customer experience, which means we’re constantly growing a closed-loop, proprietary data flywheel that we believe is unmatched.

I’ve never been more confident in the future of health – and I’ve never been more sure that we’re the ones building it.

More on this quarter’s results: https://t.co/O44El2nhen

Important info here:

https://t.co/nCW7KGtVNJ

https://t.co/0hfWRjJdgb

$ABCL

1. 635 Phase 1 : zero liver toxicity (this is critical as liver safety has killed nk3r competitors in the past)

2. GPCR platform validated (proven in human)

3. revenue doubled (doesn’t matter for now)

4. 688, 386 IND, 575 still in the clinic

Tomorrow, $ABCL has its first Phase 1 readout for ABCL635. Most of the upside is priced in IMO. However, tomorrow's data will show: (i) if the mAb engages the target and it is not excluded by the blood-brain barrier; and (ii) preliminary safety which is very important (see below).

The next milestone will be efficacy. I am doing a long article about ABCL635 for after the ph1 readout, but I wanted to share something.

ABCL635 engages NK3r, same target as Fezolinetant (Veozah) from Astellas. The oral pill Veozah has made ~$234M in sales in the 9 months since launch in 2025, in a $4B VMS non-hormonal treatment market.

REMEMBER that this molecule has a BLACK BOX WARNING for Hepatotoxicity!!! AND $234M in 9 months!

The table below shows the results from Fezolinetant in ph 2b and ph3s. In phase 2 they tested QD (one pill a day) vs BID (two pills a day) each at high and low doses (30 and 120 mg for QD and 15 and 90 for BID).

The endpoint was the difference in VMS frequency from baseline at 12 weeks. This means the reduction of episodes that the woman had of hot flashes compared to baseline (w/o the treatment). Example: -3 is better than -1, since -3 means they experienced 3 episodes less than baseline, while -1 means they experienced only 1 less.

The trend is clear for ph2 and ph3. The molecule clearly works and engages the target (p-value < 0.05 in most cases) and higher doses resulted in fewer VMS episodes. GOOD!!

However, they chose 45 mg of Fezolinetant for the Veozah pill, even if ph2 showed more reduction of VMS episodes at higher doses, WHY?? Higher dosage = Hepatotoxicity.

🚨My point: THERE IS A LOT OF EFFICIACY LEFT ON THE TABLE for ABCL635!!!

The hepatotoxicity is most probably due to the Fezolinetant compound, not the NK3r target engaged. IF this is true and ABCL635 doesn't have toxicity and is safe, AbCellera could trial a safer higher dosing resulting in HIGHER EFFICACY!!

If ABCL635 is safer and has more efficacy than Fezolinetant they would only compete over how convenient it is to have one pill a day or one shot a month, that is not up to me to decide.

But still, it will be a clear contender for the $6B non-hormonal treatment VMS market projected for 2030 and could maaaaaaaaaybe prey on the Hormone replacement therapy market of $26.5B by 2030. Big IF, I know, but there is a good chance.

$ABCL

if ABCL635 phase 2 hits, this would not be $10 story anymore. re-rating toward $20+ becomes logical to me and still i would consider cheap (GPCR platform validation). :)

NFA. DYOR.

Dr. Stephen Quake (now on $ABCL’s board) just shared new work on single-cell + data-driven biology in PNAS.

This isn’t random research.

https://t.co/hhh7f2ZXGV

It’s the exact scientific direction

@Investinc_Intel i am still optimistic as i believe it will eventually become a digital learning platform. habit formation with gamification is one of the strongest behavioural moat for $duol. i know AI has introduced some structural uncertainty but i still believe in current management team!

even though everyone is pessimistic about these names, these are the ones i would keep accumulating irrespective of the narratives.

$ABCL

$DUOL

$HIMS

it always gets tempting to switch yourself to different zones based on narratives but always stick to your conviction :)

i love how the narrative for $DUOL has been framed as a simple language learning app and the take from most of the FinX investors (even great ones that i admire) is that AI will cannibalize it.

when this company started, it started to solve a straightforward problem:

“teach people languages digitally. faster, cheaper, accessible.”

and, they did it in a surprisingly elegant way via gamification, habit loops, social proof, difficulty ramp, personalization, streaks, instant feedback, which worked.

the amusing hallucination that most investors currently have as one category (language learning) is the destination for this company. one should be looking out for those hidden clues that a company shows you in hindsight and update their mental model as the company evolves.

this is the same intellectual trap that once made investors believe:

$amzn = bookstore

$tsla = car company

$meta = college app

$googl = search engine

$nvda = graphics card gaming

the mistake was not that these takes were wrong in prior decades. the mistake is that they stayed frozen in those decades while the companies moved toward 2035. even i made those mistakes but i am learning and enhancing my decade forward thinking mindset and giving less emphasis to instant gratification.

i believe currently same thing is happening with below companies

$abcl = drug discovery

$hims = boner pill company

$duol = language learning app

the mistake with us as an investor is category freeze. they freeze a company in the category it started in.

most important things that an investor should look for to identify a great company

are boring fundamentals. these are the important ones :

a) management : integrity, clarity, honesty, mission

b) culture : do employees love building here?

c) innovation velocity : can the company ship?

d) TAM expandability : not just size, but elasticity

e) proof of execution : did solving the initial problem worked?

f) strategic pivot : now that they have already achieved something more foundational that is the “user habit” , they would unlock education, once they will unlock education, they will unlock curriculum then credentialing and so on and so forth. the distribution engine comes before the business engine. this is how platforms are born.

as an investor my goal is identify a competent, honest, innovative and a great company and management team that can “pivot” to more avenues as per the future needs. $duol already have a management team that:

a) cares relentlessly about innovation

b) iterates relentlessly

c) experiments constantly

d) has zero complacency

e) expands TAM thoughtfully

f) moving into credentialing, curriculum, AI tutoring

g) has platform optionality

as an investor, i am asking a simple question: “do i really think this business will die?” i do not think so.

$duol ‘s management is continuously evolving and doing the strategic pivot as per the need. expanded to math,

expansion to music, launched credentialing (TOEFL competitor), built an AI tutoring layer, built a kids ecosystem, made IP memetic, improved unit economics and continued execution without losing culture

this is not how a dying company behaves.

this is how a platform behaves in formation. i had seen these almost similar narratives with $tsla , $amzn , $googl $nflx etc. so, i am not worried at all.

ps: i feel currently the money is flowing toward other narratives and themes - compute, memory, semiconductors, space, defense, energy, frontier AI and anything apart from that is getting intellectually discounted. that is fine. i have seen this before as capital cycles keep rotating as per the themes. i do hold $rklb, $asts and $iren as these are great businesses but $duol, $hims, $abcl is in the same category of durable optionality and the bear thesis for them looks ridiculous so just wanted to call that out.

NFA. DYOR.

how much room does $duol have for growth from here? let’s look in to their total addressable market by starting from their target market.

$duol primarily targets:

1. language learners worldwide

2. education platforms targeting schools and universities

3. adults & professionals learning languages for work/travel

i would just be focusing on consumer market since this is the largest driver.

step 1 : population and internet penetration

a. world population (2025 estimate): 8 billion

b. internet users: 5 billion

c. smartphone users: 5 billion

step 2. targetable population:

people likely to learn a language online (students, professionals, hobbyists): 2.5 - 3 billion globally.

step 3 : affordability and willingness to pay

$duol ‘s subscription: $6 - $12/month (Duolingo Plus).

likely paying users: middle class and above. let’s assume 20–25% of targetable population can afford and are willing to pay.

paying TAM: 3 billion * 0.25 ~ 750 million paying subscribers

step 4 : penetration

even if $duol just 10-20% of this paying TAM, it will have 150 million paying subscribers. ( $spot and $nflx have approximately 300 million paying subscribers so this is realistic)

currently $duol just have approx 11 million paying subscribers. if it captures 150 million paying subscribers, that is a 15x growth from here. if it reaches 300 million paying subscribers, that is a 30x growth.

given $duol ‘s strong focus on language learning and digital education (we will see multiple verticals getting added in the app) and the world is accelerating shift toward online learning from traditional models, it is easy to imagine a future where every internet using household has at least one paying Duolingo subscriber.

feel free to pitch in/correct me wherever i am wrong.

ps: this write up is for educational purpose and should not be considered a financial advice. i am invested in $duol and it is my top position as of today.