How did I know my best calls were going to run before they did? $BRUN $DGXX $SIVE $LPK $NBIS $LPTH $HIVE $EOS.AX

If you scroll my profile, you would think I like to do TA. But actually I love doing fundamental analysis as well.

I enjoy finding gems and digging through the company just as much as I enjoy the TA. That work takes weeks, and I'm super selective, that's why I don't spam tickers continuously. But when I do put out a thesis, you can bet that I have done the homework.

Here is my framework:

Question zero: enabler or beneficiary?

Before anything else.

Does this company build the foundation of the AI buildout, or just use AI to improve a service? Enablers are examples like semis, memory, neoclouds, photonics. The picks and shovels. Beneficiaries are fintech, SaaS, healthcare.

Enablers capture the most value right now because they can't be skipped. Demand is outstripping supply. The odds of picking a winner are higher. Beneficiaries fight in crowded markets, and at worst AI eats them. See the recent SaaS bloodbath. Pick enablers to be included in your portfolio want enablers.

1. Leadership.

Everything about a company stems from the top, the culture, the finances, the engineering, the technology, the customer relations etc.

> Does the founder have experience that actually maps to this company, or a resume from an unrelated field?

> How long has the CEO been in the seat?

> Is it founder led?

> Do they own real stock, and are they buying in the open market or quietly selling?

> Any history of missing their own guidance, related party deals, or restatements? And if so, why?

Unproven at this scale is fine if the credentials fit and their own money is on the line. Documented dishonesty is an instant fail.

2. Revenue Quality.

> Is it recurring, or a one time lump that won't repeat?

> Is it spread across many customers, or does one whale carry the whole number and could walk tomorrow?

> Where does it come from geographically? One country, or many? Heavy China exposure is a different risk than a diversified base across the US, Europe and Asia.

> Does the cash flowing in match the revenue being booked, or is the growth living on paper?

3. Revenue Growth.

This is crucial for finding 10 baggers

> Is there a credible inflection coming, or just a steady trailing rate?

> Is the capex already in the ground to support it? If not there are dilution risks.

> Is the customer pipeline named, or hand waved?

> Is there any guidance on revenue growth given by management?

A flat company with a real inflection ahead beats a steady grower with nothing coming.

4. Moat. The edge that protects them.

Extremely important to find winners in the long run as well.

> Is it an artificial moat, the Lululemon or Nike kind, built on brand and marketing that a competitor can erode with enough spend? Or is it something only this company can do?

> Switching costs, multi year qualification cycles, patents, sole supplier status?

> Has anyone with money and reputation on the line validated it? A named hyperscaler, a platform leader, a strategic investor on the board?

> External validators are hard evidence, not narrative. Counterparties don't sign off on weak operators.

5. Asymmetry. Risk to reward at today's price.

Most people get this backwards. It is not "the stock has run, I missed it." It's "does the upside still pay me for the downside."

> What's my floor? Cash on the balance sheet, trust value, book value?

> If the bear case hits, how far do I actually fall?

> If the thesis works, where does it go?

> Does the probability weighted upside still beat the downside by a wide margin?

A stock that has 5x'd and still pays you 2 to 1 is more asymmetric than one that has done nothing and pays you 1.3 to 1.

There are many ways to value a company, for me, the best way to value growth stocks is looking at their forward earnings/revenues and comparing it to peers. This is what I did with $BRUN to determine it was undervalued. Find your style.

6. Conviction Gap.

The space between what I can prove today and what the next catalysts will prove.

> What is genuinely unknown right now?

> Which way does the existing evidence lean?

> What specific event would convert the unknown into fact? When does that event happen?

A wide gap with evidence pointing the right way is the whole game. It means the market is pricing in uncertainty I have a reasoned view on. Thin analyst coverage isn't a red flag here. It's the opportunity.

I write the bear case out in full and pick at it before I ever post. If I can't convince myself first, I won't try to convince you.

To summarise

0. AI Enabler over beneficiary.

1. Leadership I trust.

2. Real revenue.

3. Forward growth.

4. A moat only they can build/is hard to replicate.

5. Asymmetry that pays me.

6. A gap with a catalyst to close it.

You can take these 6 criteria to come up with a composite score to decide whether you want to decide to invest in the company or not.

7. How I integrate TA into all of this.

The fundamentals tell me what to buy. The technicals tell me when.

The best setup is when both line up. Great fundamentals with a broken chart just means you bag hold while you wait, sometimes for years even! See $PATH. Arguably the right company, sadly the wrong tape. And this is huge opportunity cost.

So once a name clears my framework, I check the chart for confluence.

> Is the stock breaking out of a downtrend or a long consolidation?

> Are the EMAs stacked bullish, shorter over longer, all sloping up?

> Is there real volume driving the move, or is it drifting on nothing?

Each one on its own may be noise, but stacked together, they can be a signal. That confluence is the difference between catching the entry and riding the wave, or being early and bleeding.

Conclusion

I recently caught $HIVE, $EOS.AX and $LPTH using the fundamental and technical combination as laid out above, you can search my profile. It takes a lot of hard work and patience to find names like this. It's definitely an arduous but certainly rewarding process.

I typically don't share the full thesis as the engagement on them are typically lower, but an example of full theses are my articles on $BRUN and $SEYE.ST.

I really appreciate you taking the time to read this. I hope it inspires you to do your own fundamental analysis. These are just guidelines, and the actual research can go much deeper than this, but I think this is sufficient to give you a headstart! If you have any questions, please feel free to reach out.

Thanks once again :)

- Leki 🐵

$BRUN $DGXX $IQE $INFQ $SIVE $SIVE.ST $LPK 080626 TA Update

As always, just my 2c. 🙊

$SIVE $SIVEF $SIVE.ST $LPK TA Update 080626

10/20/50/200EMA => blue/purple/yellow/red

$SIVE

SIVE looks really good here, printing a bullish engulfing candle and holding the 10EMA (80.01), closed at 89.40 SEK. Exactly the kind of follow-through we wanted to see after the gap-down risk I flagged. As long as the 10EMA continues to hold, structure remains very clean. 10EMA at 80.01 and 20EMA at 70.40 are the cleanest add zones.

$LPK

LPK on the other hand not as good, closed at €21.10. It rejected the 0.618 level (€22.70) to the T and also the 10EMA (€22.30) and 20EMA (€22.10). It needs to reclaim all of these levels soon, otherwise we're risking the bearish 10/20 cross I mentioned and a deeper test of the €19.40 to €20 zone.

$AMPG TA Update 080625

Wow up 27% on the day and pushing $7 overnight. Today on the daily, it held the 10EMA and sliced through all fibs levels above which acted as resistance before.

Look at the weekly chart, it looks like it is just breaking out of the resistance level set in Dec 2024/Jan 2025. My targets are $9.62 and $14. With this momentum + imminent news drop of a partnership between $AMPG and $NVDA/$AMZN.

I wouldn’t be surprised we hit these targets soon.

Just my 2c 🙊

$BRUN shares unlocked and hit the market today. Green/flat close. Kinda weird huh? It was literally a nothing burger.

Let's do a quick recap here:

> $475M ARR guided for 2026, recurring not lumpy

> $1.45B contracted backlog as of Jun 1, up from $940M at the May listing

> NVIDIA Exemplar Cloud status on Blackwell, NVIDIA's top validation tier

> One of only a handful worldwide, alongside Azure, CoreWeave, Oracle, Nebius

> Dell and Fluidstack named. Thinking Machines Lab signed May 21. CDW in the channel

> 153MW of contracted compute

> Analyst targets to $45, up from $25

Insiders and the sponsor hold most of those unlocked shares. They were handed the right to sell into strength.

Put yourself in their shoes. You sit on the board. You see the pipeline and what's in store before retail does. Do you dump in the $30s if you think it is worth multiples more next year?

The unlock is a calendar event misrepresented as a negative catalyst. The backlog is a demand event. One is noise, one compounds. I have read every filing this company has put out. This is just short term noise, and it does not break the thesis.

Just my 2c.

- Leki the investing monkey 🐵

New ticker reveal:

The stock I have been looking into is $SILC. I'm not the first to write about it @PepInvestStocks and @WealthyReadings have written about it before, but I believe we're still early. Let's get into it.

To start, they have a big catalyst coming: H2 2026 proof of concept at a Tier 1 hyperscaler. PoC conversion brings tens of thousands of FPGA inference cards at multi-thousand-dollar prices per unit, mix-shifting consolidated revenue toward higher-margin product and triggering gross margin recovery from depressed 30% toward 2022 peak of 34%. It hit both revenue ramp + margin inflection, and forward EV/EBITDA prints 6.6x, below every direct networking peer. Cash + working capital covers ~50% of market cap, so the bear case is bounded while you wait.

Now that I have your attention, let me give you a brief rundown using my framework:

AI enabler or beneficiary? Enabler. Three AI product lines built on different chips. First, FPGA inference cards using chips from Intel and AMD (FPGAs are programmable chips, meaning they can be reconfigured as AI models change every few months) targeting cloud datacenter inference workloads. Second, NVIDIA GPU edge appliances (Marbella line, using NVIDIA's L4 chip designed specifically for video analytics and AI at the edge of the network rather than the cloud) for telecom and enterprise customers. Third, Hailo-8 AI appliances (Madrid line, using Intel's low-power CPU plus Hailo's specialty AI chip, 26 trillion AI operations per second using only 2.5 watts of power) for factory robots, security cameras, smart retail systems, and automated sorting. Three customer engagements stacked: a May 5 proof of concept targeting hyperscalers at multi-thousand-dollar prices per unit, two AI compute customers already shipping product, plus a third inference product co-developed. Mgmt has explicitly guided "significant" AI inference revenue in 2027. ✅

Leadership. CEO Liron Eizenman (since July 2022) built the Edge Networking division that became Silicom's primary growth driver pre-2022. The business is back to executing: Q4 25 +17% YoY, Q1 26 +33% YoY (materially ahead of the 18% guide). Two consecutive beat-and-raise quarters. 4 design wins booked in 4 months versus 7 to 9 annual target, running well ahead of pace. ✅

Revenue Quality. $61.9M FY25 real revenue. 200+ global customers, 400+ active design wins, 75% North America. Design-win driven business, i.e. each customer takes 6 to 18 months to onboard and re-qualify, meaning once a customer chooses SILC it's expensive and slow for them to switch away. Edge AI line opens diversification away from traditional telco/cybersecurity/cloud customer base into manufacturing, retail, security, smart cities, and robotics end markets. ✅

Revenue Growth. FY26 guide $82 to 83M (+33%). Layered growth engines: design-win compounding, AI inference across all three product lines, post-quantum cryptography (3 wins to date, $3 to 4B market by 2030, new encryption standards needed to defend against quantum computers cracking today's encryption), white-label switching ($6 to 7B market by 2030), edge AI appliances for robotics/security/retail. CAGR framework points FY28 to $130 to 140M baseline; mgmt's long-term target is $150 to 160M + $3+ EPS. Margin leg: current gross margin 30% vs 2022 peak of 34.5%. Mgmt's $3 EPS target implicitly requires recovery to ~34% -> each 1% of gross margin recovery on a $135M base = +$1.35M of operating income.✅

Moat. 20+ years of proprietary hardware and software engineering. Proprietary cybersecurity packet-capture technology running at 400 Gigabits per second on FPGA chips. Nanosecond timing technology used in 5G networks and high-frequency trading (where microseconds equal money). Physical fail-safe circuits that keep networks running when security appliances crash: cybersecurity vendors specifically design products around these. Plus multi-silicon platform engineering: integrating chips from Intel + NVIDIA + Hailo + AMD into single appliances with industrial-grade certifications. The moat lives in niches that silicon vendors don't find economic to integrate at SILC's scale.✅

Validator stack: NVIDIA (L4 GPU partnership for the Marbella line), Hailo (AI partnership since July 2023 across multiple product lines), Tier 1 cyber security ($5M switch family + $2M Edge system), European secure communications ($3M post-quantum cryptography deal), major streaming provider ($25 to 30M five-year contract), global networking + SaaS leader (raised expected spend from $3 to 4M to $8 to 10M annual), two AI compute customers, hyperscaler-focused inference proof of concept.

Asymmetry. EV ≈ $154M against $109M working capital + securities. Comp ladder: Bear $32 (Adtran/Ceragon at 1.5x EV/Sales), Base $71 (Radware at 2.5x — sister RAD Group), Bull $120 (RDWR premium at 3.5x), Moonshot $245 (specialty + AI capped at 5x — NOT silicon-designer multiples). Probability-weighted EV $85 vs spot $38 = 2.23x.✅✅

Forward EV/EBITDA:

> Base ($135M FY28, 32% gross margin): 10.4x

> Aspirational ($155M FY28, 34% gross margin = mgmt target): 6.6x

> Moonshot ($250M, 35% gross margin, PoC converts): 2.9x

Conviction Gap. Two discrete near-term catalysts: H2 2026 AI inference proof of concept outcome AND gross margin recovery trajectory. Q2 26 print (late July / early Aug) is the first checkpoint on both. Watch for the first quarter printing ≥31% gross margin imo, that's the structural inflection signal, more important than headline revenue beat. Single active analyst with stale $28 PT (April 2025) vs Morningstar quant fair value $96.38 = 3.4x dispersion. Thin coverage.✅

TL;DR. Forgotten Israeli RAD Group networking name printed a clean 33% Q1 inflection. Cash + working capital covers ~50% of market cap, the bear case is bounded. Three AI product lines across different chip vendors, FPGA cards for cloud datacenters, NVIDIA GPUs for telecom edge, Hailo specialty AI chips for industrial robotics/security/retail, which is genuine diversification away from telco-heavy historical mix. Real moat in 20+ years of proprietary networking and edge appliance engineering. Bull case has two legs: revenue ramp to mgmt's $155M target AND gross margin recovery to 2022 peak of 34%. Hit both and the multiple rerates from 10x to 6.6x EV/EBITDA, below every direct peer. Margin recovery is the leg that doesn't require a binary catalyst, mgmt's own EPS target is the receipt.

Technicals:

Chart looks like it is cooling down after a run from $18 to $50 recently. Coming down to test the 10EMA and 0.382 Fib level around $37 on lower volume. 50/200EMA golden cross occurring soon on weekly timeframe, indicating a bullish trend for the mid-long term. Still overall very bullish. ✅

I truly believe that despite the recent run up, we are still early. I won't be surprised if we are at $100 by EOY.

Just my 2c, as always.

- Leki the investing monkey 🐒

Goldman says CTA bought +$86 billion this week, which is top 5 all time.

they modelled that CTA could purchase an additional $70 billion of the next 5

sessions.

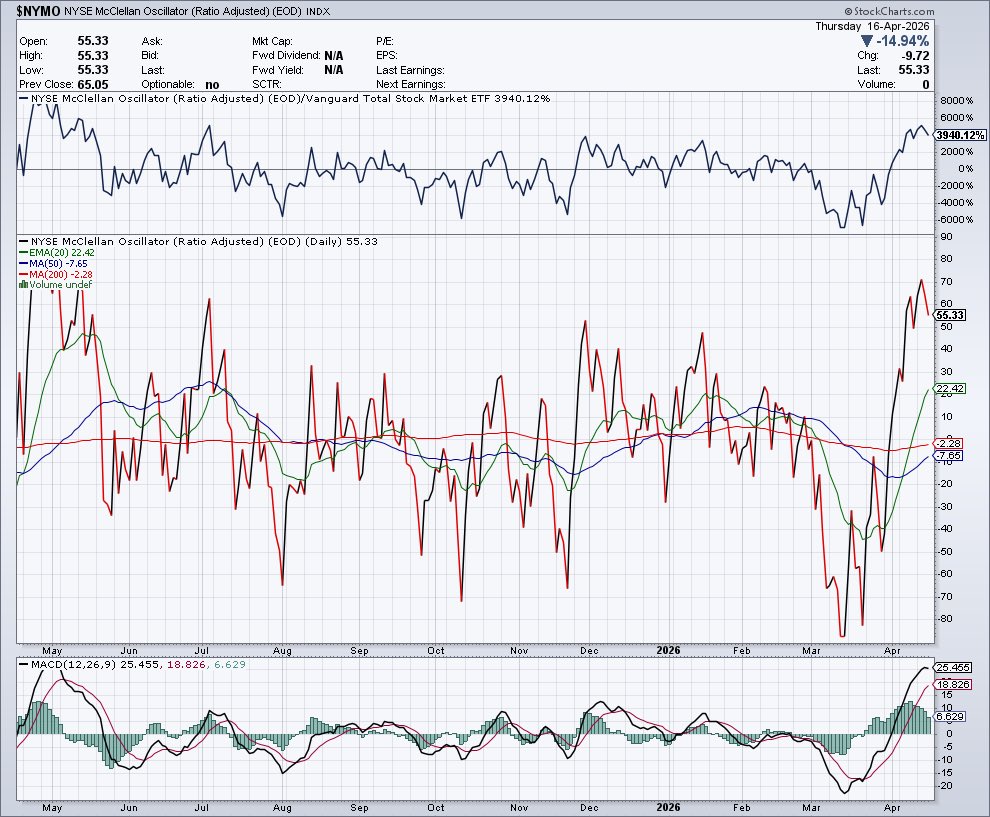

$NYMO breadth has been weak the past few sessions even as the market pushes to new highs. A lot of stocks have already started pulling back under the surface.