https://t.co/zXmjSEjAHM

Succinct but apt view of the current labor market in the US (and much of the developed world). The case for interest rate hikes this year in the US is still weak.

‘higher rates when Democrats were in power, and lower rates under Republicans’ (https://t.co/1DeBpmfk25) - Kevin Warsh’s views on rates. Market has overreacted to Warsh being a hawk when, in fact, he is not. He has and will politicize monetary policy (and surely lower rates)

Would not be surprised if the USD depreciates 10-20% this year against the other major currencies like Swiss Franc/Euro (far more than the 11% in 2025) and commodities rise drastically in response. Central banks and investors have a lot more room for dollar decoupling

A lot of focus on commodities/silver/gold at the moment and probably rightfully so, as the outlook is positive for them on a relative basis (to other assets) but can’t say so on an absolute basis. There are two factors which will weigh on metal commodity prices 1/2

How Trump behaves/geopolitical instability (positive for metallic commodities) and recessionary concerns (negative for metallic commodities). Key event to watch will be threats against Greenland which seems like the biggest source of geopolitical instability now. 2/2

A lot of focus on commodities/silver/gold at the moment and probably rightfully so, as the outlook is positive for them on a relative basis (to other assets) but can’t say so on an absolute basis. There are two factors which will weigh on metal commodity prices 1/2

Trump’s actions are a reminder that the Republican party is still dominated by NeoCon ideology, especially the Unitary Executive Theory. Dick Cheney’s legacy continues with the Trump-era policies and outright threats of military action to various nations.

Don’t forget that AI’s main uses cases presently are just data scraping from other sources (aka GOT/Gemini) and it has been proven highly unreliable for that (re: Deloitte AI scandal).

The economy overheats when investors over-invest needlessly. We’re getting there 2/2

If it isn’t blatantly obvious, we definitely are in AI bubble territory.

Ridiculous money being thrown at shoddy startups… lack of energy infrastructure to support the ecosystem (Google wants to set up a data centre in Space soon to resolve this —> unrealistic though!)… 1/2

Everyone almost always seem to blame the private sector for Pakistan’s problem. This seems to be more an issue of a big government (with a large fiscal deficit) that could not raise external debt + a lack of lending appetite (due to low growth) from the private sector.

Banks are booming—Pakistan’s economy is not. Wonder why?

The banking sector’s outsized profitability isn’t driven by innovation or risk-taking—it’s built on a system that rewards lending to the government at the expense of the private sector.

As of June 2025, the Investment-to-Deposit Ratio (IDR) stood at an astonishing 100.8%, meaning nearly all deposits are parked in risk-free government securities.

Meanwhile, the Advance-to-Deposit Ratio (ADR) had dropped to just 37%—a stark indicator of how little credit actually reaches businesses, especially SMEs.

This dynamic fuels bank profits but crowds out Pakistan’s real engines of growth: small and medium enterprises, startups, and industrial expansion.

It’s time for policymakers to ask: Are we financing growth—or just borrowing time?

#FinancialReform #CrowdingOut #PakistanEconomy #SMEFinance #Banking

𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐛𝐚𝐧𝐤𝐬 𝐫𝐞𝐦𝐚𝐢𝐧𝐞𝐝 𝐭𝐡𝐞 𝐭𝐨𝐩 𝐜𝐨𝐧𝐭𝐫𝐢𝐛𝐮𝐭𝐨𝐫 𝐭𝐨 𝐊𝐒𝐄-𝟏𝟎𝟎 𝐝𝐮𝐫𝐢𝐧𝐠 𝐅𝐘𝟐𝟓 (AKD Securities)

Trump tariffs are a net positive for Pakistan and Pakistani assets. My hunch is they will be reversed but the impact of it will endure with lower commodity prices. --> lower import bill (nullifying impact of lower exports) --> better current acct and external acct stability

A U.S recession can help Pakistan’s struggling real estate market by lowering global interest rates, reducing borrowing costs for developers, and decreasing commodity prices, which cuts construction expenses🧵

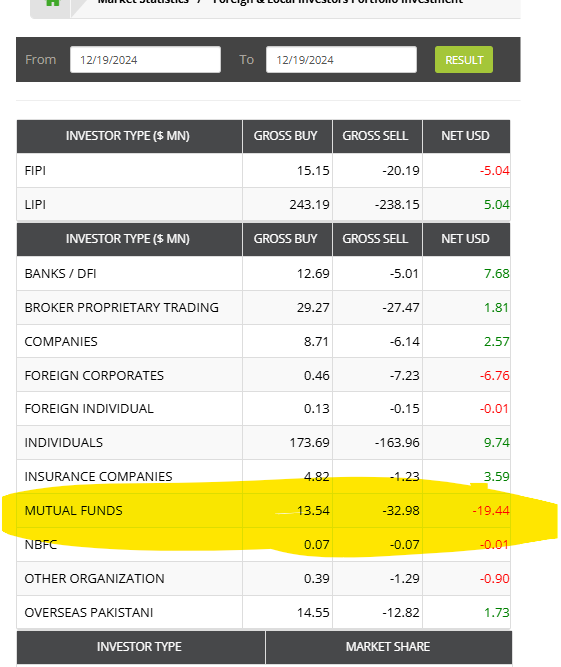

If true, why trust them with your money? Would you trust a bank which said: uhhh we don't know the trends of deposit outflows or how to model it and we love to put all our cash to work through loans. That bank wouldn't last very long would it? It's a choice, not a forced hand 3/3

The redemption story has mostly been BS. Reminds me of Peter Lynch's Beating The Street where he reveals he made the mistake of going too light on cash once and suffered by selling securities at prices he didn't want to due to large redemptions in the 90s. He says he 1/3

and other MFs rarely repeated such mistakes again. Mutual funds do have excess cash on hand to deal with redemptions. Or maybe Pakistan is just special eh? If they say it's all redemptions, they're saying: we don't learn from our mistakes. 2/3

Important to keep this perspective in mind when discussing growth prospects. Inflation has calmed down and IRs are coming down but the price level is too high relative to net incomes. Demand won't pick up without some positive shock - external debt relief/tax or tariff reductions

What has Pakistan’s record inflation wave done to prices

Gas prices +840%

Electricity tariffs over 110%

Pakistan’s finance minister said this last week

Inflation pace has dropped but a lot of damage has been done

In the recent banking rally, there's one bank (besides the the Islamic ones) which has seen little share price movement: SCBPL. Thought I'd share why I think it's the most undervalued bank (on a relative basis) right now: https://t.co/7KCFzQZ6ca

#KSE100

A key beneficiary of the rally in the bond and stock markets has been the insurance sector and it has really gone under the radar. Perhaps, valuations have not adjusted as readily due to the yearly payouts as opposed to the quarterly payouts in the banking sector #KSE100