Sovereign Gold Bonds 2021-22 Series II were issued on June 1, 2021 at a price of ₹4,842( Online applicants got another ₹50 discount, so the price for Online applicants was ₹4,792)

While the tenure is 8 years, there is a provision of early redemption after 5 years for which the price notified is ₹15,672.

The return including the 2.50% annual interest comes to 28.53% for an annual applicant. For offline applicants the XIRR stands at 28.25%.

What massive return.

Note: If held till maturity, redemption proceeds will be exempt from Capital Gains. Premature redemption/selling will be subject to capital gains though.

Moody’s Ratings has upgraded the credit ratings of four major Indian non-financial corporates following an update to its sovereign linkages methodology.

• TCS & Infosys: Long-term local currency issuer rating upgraded to A2 from Baa1

• Reliance Industries: Upgraded to Baa1 from Baa2

• Tata Steel: Upgraded to Baa2 from Baa3

Outlook on all ratings remains stable.

A positive reflection of the improving credit quality of leading Indian companies.

#Moody’s #IndianEconomy

Great share, @Nithin0dha

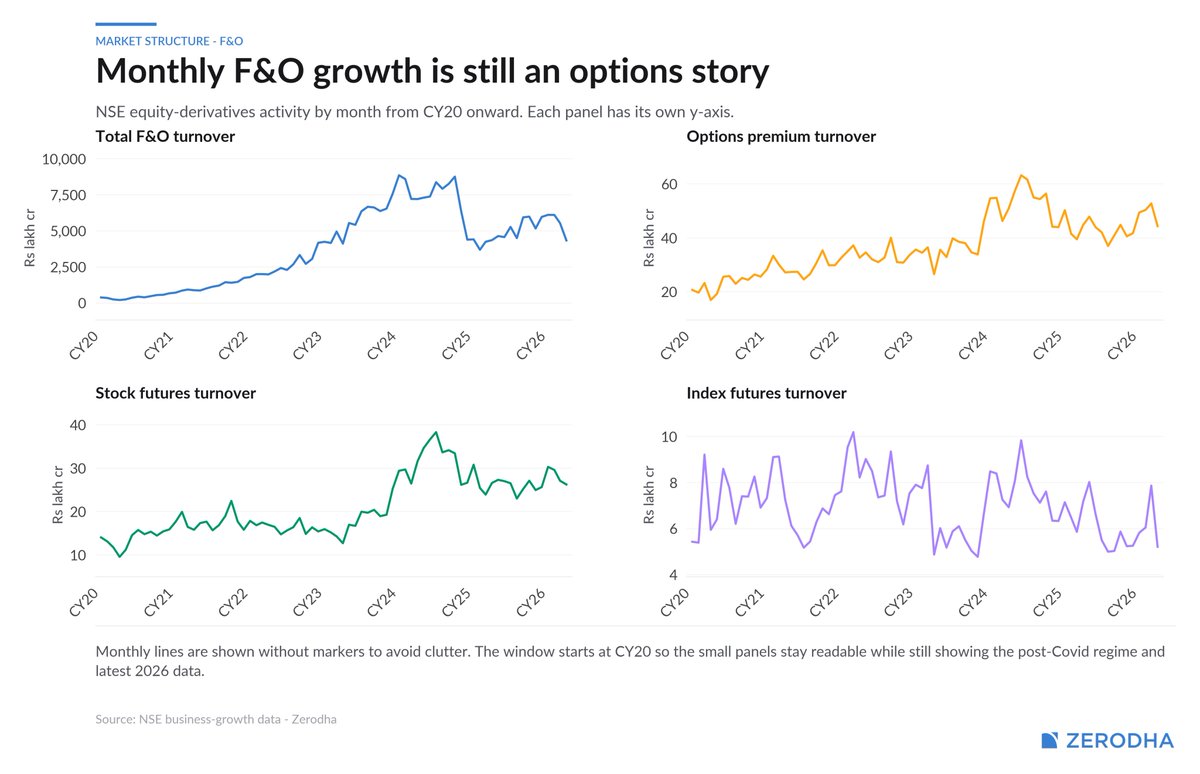

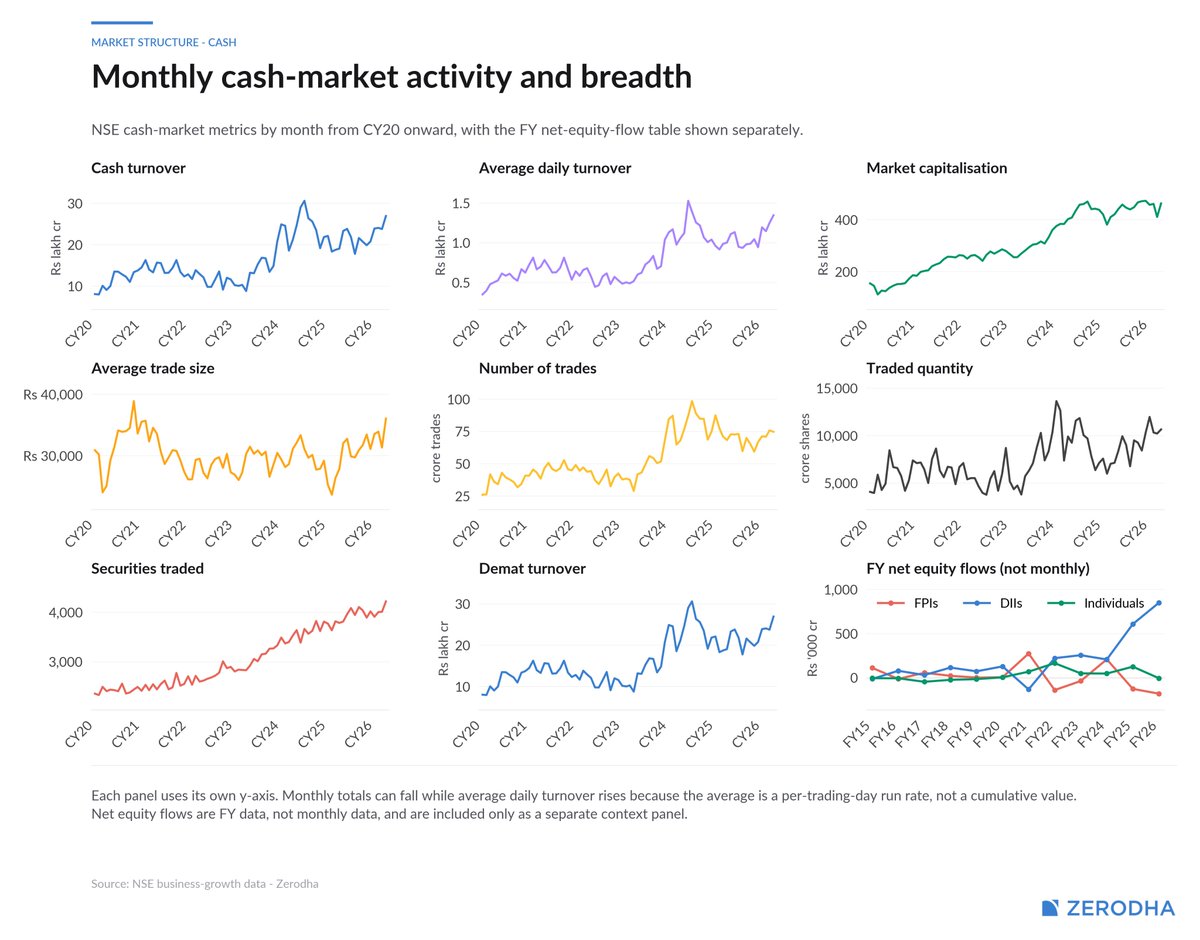

This is a classic case of “price vs. participation” divergence in the Indian markets.

The charts paint a clear picture:

•Cash turnover hasn’t reclaimed its late-2024 highs despite the index grind higher.

•Average trade size and number of trades showing exhaustion.

•Net equity inflows turning negative (first time since FY19) is particularly striking — retail and DII/FII flows telling a different story than headline Nifty/Sensex levels.

It feels like a narrow, liquidity-driven rally where a handful of large-caps are doing most of the heavy lifting, while broader market breadth is weakening. Demat turnover and securities traded are still elevated but the quality of participation (turnover + inflows) is deteriorating.

Questions this raises:

1How sustainable is this without retail conviction returning?

2Are we seeing early signs of “smart money” rotating out or just profit-booking after a strong multi-year run?

3Any particular sectors where you’re seeing the disconnect most sharply (IT/Banks vs. mid/small caps)?

Would love your updated take as we move through May/June. Markets can stay irrational longer than we expect, but when the data and price decouple this much, it usually doesn’t end quietly.

Thanks for consistently putting out these data-driven threads — super valuable in the noise.

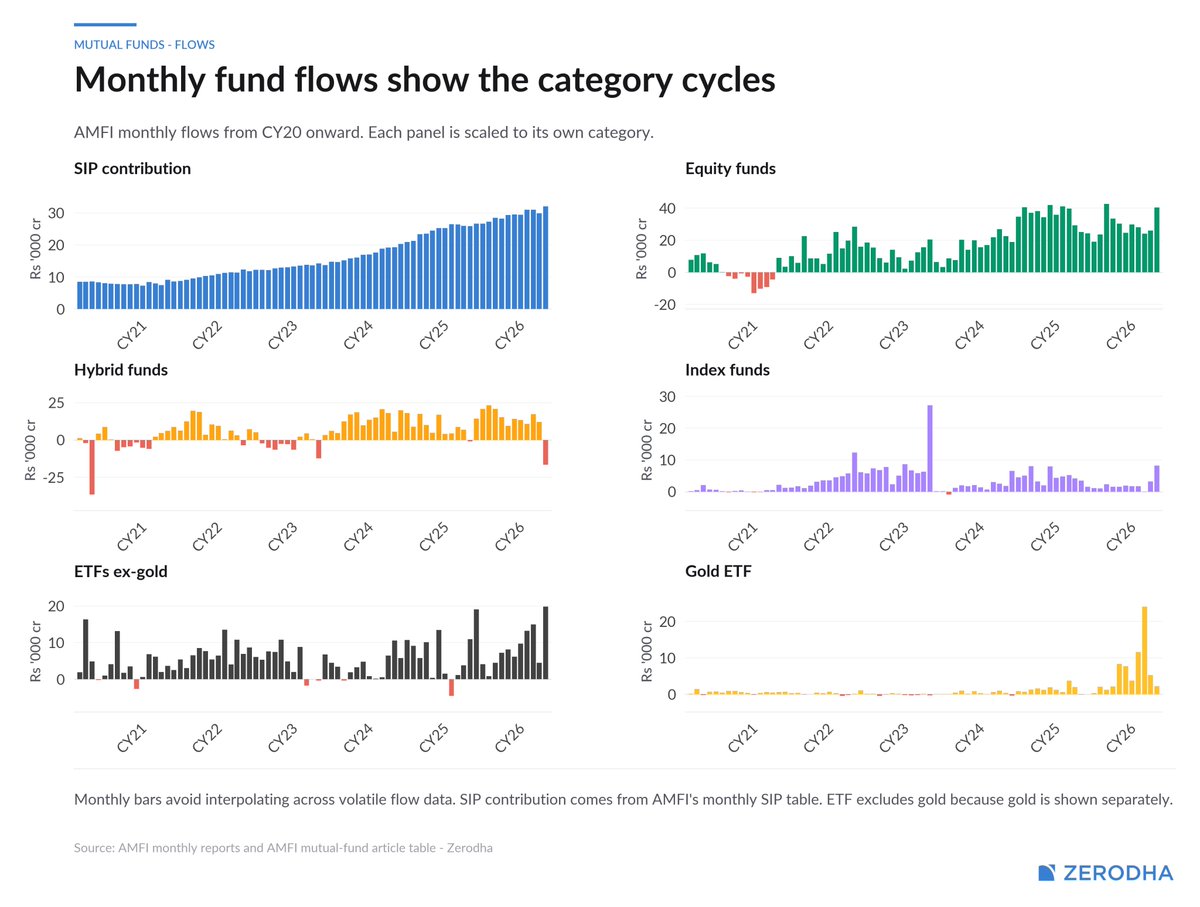

If you look at listed brokers, you’d probably think we are in a bull market, but the data shows something else. In fact, there are a lot of conflicting signals. Cash market turnover is still below where it peaked in late 2024. Net direct equity inflows, for example, are negative for the first time since FY19.

So where is there so much enthusiasm around capital markets related investment themes?

Could be the strong equity mutual fund flows and SIP flows. Gross SIP flows are at a record ~32,000 crores. But the major brokers offer direct mutual funds, so they don’t make anything, including us.

Speculative activity has held up despite everything. The MTF book across the industry has grown significantly. Our own book has grown from 0 to ~7000 crores in about 1.5 years.

Brokerage income as a ratio of client float for most listed brokers is around 40% or above. With us, it’s sub 9%. That means clients are trading far more with these platforms relative to the funds they hold there. Could be all triggers and nudges to trade?

Our own philosophy has always been to not push or induce customers to trade. In trading, for most people, fewer trades are always better. That means leaving a lot of revenue on the table. Whether that’s the right call, time will tell.

So is it a bull market? The answer is it depends on where you are looking.

In the heart of Chandigarh Press Club — standing shoulder to shoulder with Shri Dushyant Chautala Ji, former Deputy Chief Minister of Haryana.

Today’s press conference was all about raising the real issues of Haryana — unapologetically and fearlessly.

No pressure. No compromise. Just the truth and the voice of the people.

Jai Haryana! 🇮🇳 @Dchautala@DVJChautala

#DushyantChautala #ChandigarhPressClub #HaryanaPolitics #PressConference #JJP #VoiceOfHaryana

The writing in The Pitt Season 2 has taken a nose dive!

A 10/10 First Season seems to be hijacked with now the obvious 'lead' taking most of the screentime!

“Exactly @iamrakeshbansal This isn’t some border skirmish,it’s the biggest supply shock since 1973. Crude cracking $150 is very much on the table if Hormuz gets messy.

For India it’s double-edged: CAD blow, rupee pain, inflation spike… but a rocket for ONGC, Reliance, Oil India and the entire energy/PSU basket.

Markets will gap down on fear, then rotate hard into domestic energy names. Classic “buy the panic” setup.

Question is — does this finally wake us up to build our own hard energy/tech muscle, or will we keep importing both oil and geopolitics?

Your move on Nifty next 2 weeks?”

There is debate about Iran lying about their nuclear program, but there is already proof they lied about having / building long range ballistic missiles. The attacks on Diego Garcia were not possible without them.

Interesting leverage idea, @1shankarsharma.Hostage diplomacy has historically forced face-saving exits (think 1979-81). But in today’s hyper-escalated environment, Iran pulling off a clean capture of 5-20 US personnel without triggering immediate airstrikes feels like a high-wire act. Still, anything that prevents a nuclear exchange is worth considering. Fingers crossed for de-escalation before it gets hotter

@2RubinaSingla When the “Why me?” hits hardest, the simplest shift is to look around and count the blessings we already have. Gratitude doesn’t remove the pain, but it reminds us we’re never truly alone in it.

Beautiful thought!