As I understand it: The tall tripod listens for radio signals between drones and their controllers and can identify what type of drone is being used without giving any signal itself -- this is $DRO.AU hardware. The C3PO looking mf on the right side is the Openworks radar+camera that finds drones without a radio signal. It's connected to It all gets combined into $DRO.AU DroneSentry-C2 software platform. Then it can produce counter-measures like jamming or notify other counter-systems.

Counter-drone solutions provider $DRO.AU catching a bid in AUS this morning. They signed a partnership to host Openworks optical sensing technologies on their DroneSentry-C2 platform.

This shows DroneSentry’s capabilities as a platform. $DRO.AU is the only pure play counter-drone listing I could find and I think it’s a solid way to play drone proliferation. Counter-drone defense will be essential and DroneShield is starting to make some headway to be a major player.

There’s clearly been flows between gold and oil paper. We see it in a literal sense here. Turkey selling $GLD reserves to buy likely $OIL-powered defense systems.

* Turkey Mulls Tapping $135 Billion Gold Reserves for Lira Defense

https://t.co/oSKAdukIDl

$FDX is out with some interesting commentary.

Regardless decent numbers:

- Revs +8% and mid-point of guide increased 75bps to 6-6.5% for FY 2026.

- Freight revs -5% worse than expected but Freight spin-off on track for 6/1.

- Operating income +7.2% higher than what I was looking for.

Good quarter for $FDX and I'll try to get out with less than a 5% loss. Live to fight again.

Already short $XPO, I think I'm going to add on to the Global Logistics short theme by shorting $FDX into tonight's print. It's their 3Q2026.

On top of disruptions in the Middle East, remember U.S. regulators grounded the MD-11 cargo fleet that UPS and FedEx use. I'm not sure we have a true estimate of costs there. That -- combined with LTL weakness & increased labor costs -- should pressure earnings.

I'll get bearish confirmation if:

- Total revs below FY guide of 5% would show lack of visibility and/or failure to execute transformation goals.

- Freight Revs decelerating from -2% LQ (Estimate is -1.7%)

- Adjusted Op Inc Growth decline shows Network 2.0 transformation aren't offsetting this flurry of headwinds

With about 30% cash available, I'll short $FDX with 3% of my gross available dollars.

Have to wonder what the hell is going on in China after these $BABA 4Q retail numbers:

Customer management growth down decel to +1% (+10% in 3Q) due to 'weaker transaction activities'. Ya no shit. Adjusted EBITA for ECommerce was -43%. After saying Q3 would be peak investment I was expecting that to be a bit closer to 0% -- but the weaker rev growth gave them little leverage.

Cloud Intelligence was a bit better than expected +36% so that may save them a bit.

Had to rely on anecdotal AI notes in their opening statements because the numbers sucked so bad. Never good. Qwen won't work if the customer isn't coming to the site.

After anecdotes, then GDP revision and now $TCEHY and $BABA retail weakness, one thing is clear: something is going on in #China. I'm getting out of $BABA at $128.44 and waiting for positive news.

Battery-agnostic energy storage maker $FLNC getting an upgrade from Oppenheimer. Don't have the report but hoping it brings some attention to the name.

$FLNC had a good 2H last year but has sold off on weaker 4Q numbers with $TSLA's megapack intensifying competition and potentially sparking a price war -- a major problem for the low margin Fluence.

My belief though is that there's plenty of demand to go around through 2028 and -- based on workforce data -- $FLNC now has hit labor capacity objectives after ramping up through 2025. This new mix of employees should be much more qualified to handle the data center buildout. That should allow them to get project issues under control.

P/S NTM at 0.9x is as cheap as anything in the Data Center ecosphere. Worth a shot here even considering the low margins and Tesla's jaunt into the space (they feel a bit spread thin -- no?).

Had about ~30% cash used 2.5% on $FLNC -- will give this one a decent leash.

On $WW:

So they blew out their sandbagged guide but still a shitty qtr. Rev growth worsens to -11.7% from -10.8% in 3Q. Both behavioral and clinical worsened. Lost over 200k behavioral subscribers (-18.9%) -- so much for the new app.

Segments:

Clinical revs do show nice acceleration to +44.7% up to 130k users. This is the GLP-1 segment. It was +35% in 3Q. 50% would have been nice. Also surprised to see monthly clinical pricing down 10$ (-12%) from last year.

EoP behavioral subscribers (ie their old WW points business) -18.9% slightly better than -20.2% in Q3 but guided to -26% YoY in Q1 -- so another 150k subscribers expected gone. Brutal. Was hoping for -15% with roll out of new app and specialized programs. No signs these are sticking.

$WW is not $AIRS which did show genuine signs of a turnaround and deserved its move up. The GLP-1 business is growing obviously but it's so small and now pricing is coming down. Hoping I can get out at even.

I’m out at $210.53 — will likely rip back in my face. Just feels like w/ them losing their contract and Don jr getting into drones they’re quickly losing the U.S. favor.

Prescient this morning with $AVAV -12% after losing SCAR contract and pushing several orders "by a quarter or 2".

AxS number strong but this print is a reminder why investing in Gov-contract companies is a tough life.

"Every day that goes [with] the budgets not being approved or a continuing resolution going forward or the dollars not hitting their accounts... it actually adds more risk for that not to happen this year, but it will happen the following year." -- $AVAV CEO on shutdown headwind

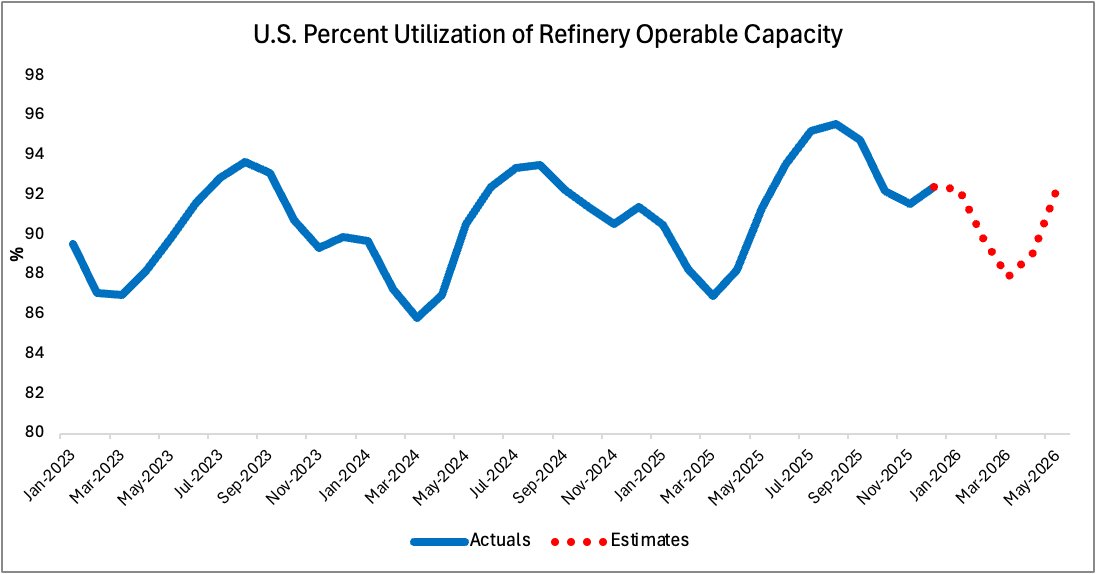

Bought some $MG March '26 puts. Will probably get smoked. Sucker always moves on the print (Ex 1). It's a company that continuously monitors then diagnoses problems in critical infra like nat gas pipelines, refineries, plane components. It's caught a bid because of **data centers**

I figured stock is up 35% since Q3 print on top of 21% on the print day itself. They're implementing a complex ERP system, natgas rolling a little.

They reported decent numbers though -- 91m FY EBITDA and rev probably checked box. Accelerating revs for A&D +24% and power gen +35% is solid. FCF ended positive after ERP implementation struggles in Q2/Q3.

The one thing I have going for me is they give guidance on call tomorrow morning. Gonna listen closely to hear how their thoughts on turnaround season activity (Ex. 2 from EIA) and if there's any shakiness in pushing the new integrated solutions business.

Got too cocky with this one. Had $15 puts for March. Tried selling at $2.20 even though stock had only gotten to 13.50 — stock gets back to 14.10 and marks crushed. Should’ve taken the $1.75 but now instead gonna be watching ticks of some random natgas company all day.

Is virality trade still working?

Bought $WEYS on the news that Trump gives out Florsheim shoes to staffers and guests after discovering them last year.

According to filings, Florsheim is about 1/3 of total Weyco sales. The brand has been gaining market share anyways as “refined casual” footwear sees traction. This may lift the American market a bit.

https://t.co/kUqPg7Tnkp

When you walk outside in New York City, you should be able to see the sky.

That’s why we’re putting forward new rules to make sure unnecessary sidewalk sheds are taken down and more don’t go up.

We’re focused on NYCHA tenants specifically — making $650M in facade repairs and taking down sheds at 40 developments, including Highbridge Gardens in the Bronx.