✳️ Trend Micro is Japan's cybersecurity play with USD1.3bn in ARR.

✳️ The SaaSpocalypse happened and Trend Micro share price dropped to its 5-year low.

✳️ Now that it’s relatively cheap, private equity might be interested again.

✳️ But what would private equity or activists do to create value? Let’s look at some levers:

1. Trend Micro has a legacy consumer anti-virus business with about USD60-70m revenue that could be divested.

2. It can also explore a rejuvenation of the management team which can drive better capital allocation and cost optimization. Importantly, an overhaul of its salesforce might be timely to reinvigorate revenue growth, which has been flat for a while.

3. The stock might be able to command a higher valuation if it lists on Nasdaq. So by taking it private and relisting the in the US, activists or private equity could extract some value.

More at:

https://t.co/MsqCcyd49n

✳️ Trend Micro was caught in the SaaSpocalypse a few months back,

✳️ Our portfolio added a position with the simple short term thesis that it will come back. It did!

✳️ We also have a long term thesis described below. It involves activists, take private and all the fun. Read on!

✳️ Before that, let’s look at the simple financials for next year since we are halfway done with 2026.

Financials (in USD, Dec 27)

==

- Net Sales: 2bn (ARR: 1.3bn)

- OP: 0.4bn, Net Income: 0.25bn

- EBITDA: 0.55bn, Free Cashflow (FCF): 0.5bn

- Sales CAGR: 3%, OP CAGR: 5%*

- Net Cash: c.1.5bn, Market Cap: c.5.9bn

* Trend Micro has disappointed on growth despite being a red-hot cybersecurity stock

Financial Ratios

==

- ROE: 30%, ROA: 10%

- GPM: 77%, OPM: 20%

- EV/EBITDA: 8.3x, EV/Sales: 2.3

- PER: 21.1x, PBR: 6.5x

- Dividend Yield: 2.8%, FCF Yield: 8.5%

https://t.co/MsqCcyd49n

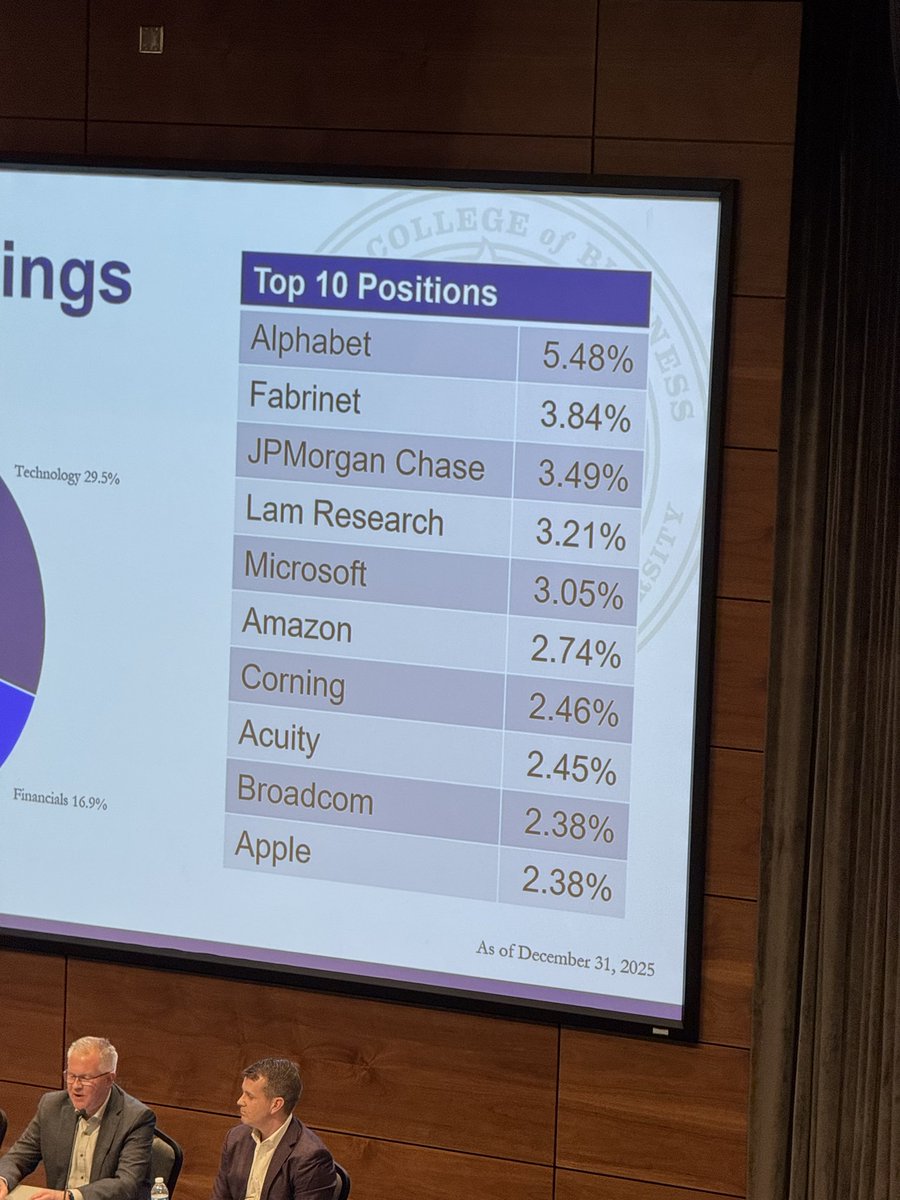

We have mapped both Japanese activist and global activist stock names and this is the final piece of the puzzle where we attempt to track prominent activists operating globally using publicly available information.

We have included the activists’ AUMs and track record estimates and highlights of their landmark activist campaigns. Screenshot below captures Effissimo:s All Green Portfolio. Enjoy!

https://t.co/9FdImR7fWF

Shareholder activist Elliott's 27 April 2026 case for Japanese HVAC company Daikin:

1. Technology edge in inverter systems, refrigerant systems, compressors

2. Has been growing market share from 10% in 2015 to 14% last year, suggesting brand strength

3. The global HVAC market grows ~5% annually

4. At the time of writing, Elliott thought Daikin's 18x P/E was a big discount to the peer group

5. However, the ROE had declined to 9%, and Elliott suggested heavy cost cuts, lower capex spend, consolidation of manufacturing plants, a JPY 1 trillion share buyback, and divesting non-core assets

6. Elliott saw a path to JPY 2,623 in EPS by FY2031, which would put the stock below 10x P/E. However, that would require action to improve the ROE

➡️Honda did a $7bn share buyback and its market cap is $36bn.

➡️After the buyback, the share price didn’t move. How does that even work?

➡️We dug a bit more into this.

➡️So the firm announced this massive buyback around Dec 2024 and bought up 20% of its market cap.

➡️Share price did well for a while but then fell back to where it was.

➡️Because, the company announced profit warning and its first ever annual loss since its IPO...

More below 👇

Japan's Record Share Buybacks; Bitesize Analysis on 7&I, Bridgestone, Honda, Sony https://t.co/WUhkS6syxv

➡️ We pulled out a share buyback EQS screen recently.

➡️ Multi-billion dollar share-buybacks in Japan are now the norm.

➡️ There are almost 30 corporates doing share buyback of more than $1bn.

➡️ This was a screen for $100mn and above buybacks. Guess how many co.s appeared?

👇Full Post:

Japan's Record Share Buybacks; Bitesize Analysis on 7&I, Bridgestone, Honda, Sony

https://t.co/WUhkS6syxv

✅ We are blindly accelerating through the AI hype, escalating wars, and $120 oil, yet investors seem to have no time for caution.

✅Nobody is pausing to ask what could actually bring the house down.

✅It is true that price-to-earnings multiples aren’t overly demanding.

✅Aside from the Nasdaq and the Nikkei, most markets are trading comfortably in the mid-teens.

✅Yet, instinct tells me this optimism is dangerously misplaced.

✅The global landscape is far more fragile than we care to admit.

✅"No Time for Caution" - 2026's Mid Year Review & Our Future Calendar https://t.co/hP822mU0MW

2026 Mid Year Review:

✅ 2026 will likely be the most bizarre year of the 21st century.

✅ Global markets are at all-time highs despite oil being up 80%.

✅The war in Iran, and strategic chokepoints strangling the global supply chain.

✅Yet, Mr. Market’s exuberance shows no sign of waning.

AI, War, No Time For Caution:

✅We are blindly accelerating through the AI hype, escalating wars, and $120 oil.

✅Yet investors seem to have no time for caution.

✅Nobody is pausing to ask what could actually bring the house down.

Full post:

https://t.co/hP822mU0MW

✳️ Most people do not think too much about sizing and I seldom read literature about sizing which is unclear why given its importance.

💡Here is what I have figured out over the course of my investment career. Sizing wrongly hurts a lot.

❓ The first question to ask is how much can you lose and not be affected psychologically? Is it $1k or $10k?

💰 Figure out your maximum bet size. Don’t mess with your mind. If losing $1,000 makes you unable to sleep, don’t play with higher stakes.

✳️ So start with the size that makes you comfortable.

🤔 Wait, if we only bet $1,000, how can we ever get rich? Well, it will take more than a few ten-baggers and home-runs.

🙏 Thankfully, low commissions today can make $1,000 bets go far.

💲 Back in the days when there is a minimum commission of $20 per trade, it was not feasible to bet $1,000.

✳️ Because you incur 4% transaction cost just by buying and selling. But today, we can do it!

👇The rest of the post below.

On Timing, Sizing and Sell Discipline (picture below shows the market pandemonium and subsequent recovery in Mar 2020).

https://t.co/SSm65ZgxED

📈 As of Apr 2026, roughly half of Japan and Southeast Asia’s listed stocks trade below book. 38% of all listed companies in Japan trade below book.

💹48% of Asean listed stocks or about 2,700 companies in 🇮🇩 Indonesia, 🇲🇾 Malaysia, 🇵🇭Philippines, 🇸🇬 Singapore, 🇹🇭 Thailand and 🇻🇳 Vietnam trades below book.

🇯🇵 Japan has 1,400 stocks trading below their net asset values. This was 1,600 about 12-18 months ago.

🔥Activists have brought up the share prices of about 200 Japanese companies.

Updated Hero Post - What Is 8% Value Activist About? https://t.co/q8TvTnrt1n