🚩LESSONS FROM A RECENT IPP BANKRUPTCY🚩

A lender was told one of its solar projects was underwater.

The lender pushed back. Its financing position was solid.

The response: the project was literally underwater.

The site had flooded because the drainage had not been properly built. Water was inches from the inverters.

That story captures a problem hiding across renewable portfolios. Developers are rewarded for reaching COD and moving to the next project. Far less attention is paid to protecting the value of assets already operating.

But after COD, returns depend on daily production monitoring, cash reconciliation, preventive maintenance and enforcement of EPC, equipment and O&M rights.

The best warranty package in the market is worthless if no one identifies the defect, preserves the claim and forces corrective work.

Development creates the asset.

Asset management determines whether it performs like the model.

Lazard’s new LCOE+ report captures an apparent contradiction in today’s power market.

Solar and onshore wind remain the cheapest forms of new generation.

Yet announced gas buildout is surging even though gas LCOE is at its highest level in 15 years.

Those facts only appear inconsistent if LCOE is treated as a complete measure of project value.

LCOE estimates the cost of each MWh over the life of an asset. It does not measure whether the resource is dispatchable, whether power can be delivered where it is needed or whether the project can be completed before the load arrives.

Gas is attracting investment because the system needs firm, dispatchable capacity. Not because gas has suddenly become cheap or fast. Lazard specifically notes that turbine shortages are extending gas development timelines.

Speed to power is driving a separate trend: the growing value of existing plants, nuclear restarts, brownfield sites and powered land.

These assets can reuse interconnections, sites and infrastructure that may take years to replicate. Their premium reflects time saved, not necessarily cheaper generation.

The market is therefore optimizing for three variables:

Cost.

Firmness.

Delivery date.

LCOE captures only the first.

The answer is not gas instead of renewables. It is a portfolio that uses low cost renewables where possible, firm resources where necessary and existing infrastructure wherever it can compress the schedule.

🌟CONTRACT TIP OF THE DAY🌟

Six words that let your counterparty rewrite the deal:

“Contractor shall comply with Owner’s policies and procedures as updated from time to time.”

The trap is in the last six words.

At signing, Contractor can price and schedule compliance with policies it has reviewed. But “as updated from time to time” lets Owner change Contractor’s obligations after execution without issuing a change order.

A revised cybersecurity policy could require new software and staffing. A site access policy could reduce productive hours. A safety policy could require different equipment or training.

Contractor may have to absorb every resulting cost because it already agreed to comply.

The fix is not to delete the policy requirement. Tie it to identified policies delivered before signing, require advance notice of updates, and provide that any update materially affecting cost or schedule is handled through the change order process.

A contract should not contain a unilateral scope amendment disguised as a compliance covenant.

@CNBC ⚡ The overlooked part is what Meta’s 5 GW campus makes financeable.

Its demand is supporting more than 5.2 GW of new generation and about 240 miles of transmission, plus storage and nuclear uprates.

At this scale, a hyperscaler becomes the anchor tenant for a power system.

@FoxBusiness Entergy says Meta will pay its full cost of service and projects $2.65B in benefits to other customers.

That is the real model: create enough contracted value to finance a system expansion and withstand regulatory scrutiny.

@FoxBusiness Meta’s $50B Louisiana expansion is really a utility financing deal.

Meta will fund 7 gas plants, 240 miles of transmission, batteries, nuclear uprates and 2.5 GW of solar.

At 5 GW, a hyperscaler is no longer just a customer. It is an anchor tenant for an entire power system.

The White House wants to expand its pledge that AI data centers will not raise power bills for everyone else.

That is a sensible goal. It is also much harder to put into practice than it sounds.

Reuters reports that utilities, data center developers and governors may soon join the technology companies that signed the original Ratepayer Protection Pledge.

Their participation matters because a hyperscaler cannot allocate these costs by itself.

It can pay for the substation and other facilities built specifically for its campus. It can post security for reserved capacity and accept liability if the project is cancelled or the load never arrives.

The harder question is how to treat a transmission or generation investment that serves the data center but also benefits the wider grid. That requires the utility, its regulators and an actual tariff or service agreement.

The basic allocation should be straightforward. Dedicated facilities follow the load. The customer reserving capacity bears the risk that it goes unused. Broader system improvements are paid for by the parties that benefit from them.

If that line is drawn poorly, existing customers can end up underwriting speculative demand. Draw it too aggressively in the other direction and every data center is pushed toward its own duplicative power solution.

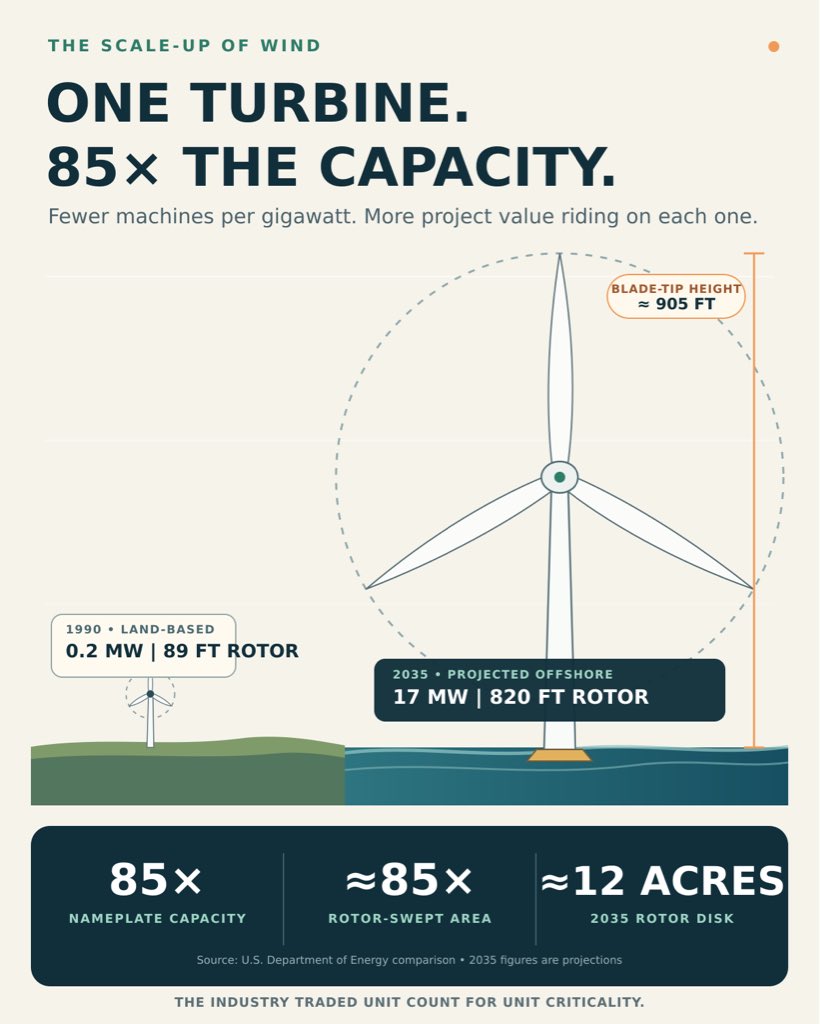

From 85 wind turbines to one.

A single 17 MW offshore turbine projected for 2035 carries the same nameplate capacity as 85 of the 0.2 MW machines shown for 1990.

Hub height increases about fivefold. But rotor diameter grows from 89 feet to 820 feet. Because swept area increases with the square of diameter, the new rotor covers roughly 85 times the area: about 12 acres.

That creates compelling economics. Fewer foundations, cable connections and maintenance positions per gigawatt.

It also changes the risk.

One outage removes 17 MW. A serial defect affects project output in much larger increments. Vessel access, crane availability and spare parts become part of the availability strategy.

Wind has traded unit count for unit criticality.

At this scale, warranties and service terms are not contractual footnotes. They are part of the power plant.

The AI power queue is moving inside the factory.

A developer can control the land, secure a utility commitment and sign a data-center customer. If the required transformer will not arrive for three years, the schedule still fails.

The numbers are getting extreme:

• Generator step-up transformer lead times now exceed 160 weeks

• High-voltage circuit breakers are taking 125 weeks, up from 77 weeks in 2023

• Some utilities are buying equipment five years before they expect to need it

• Data centers could represent up to 40% of the U.S. electrical-equipment market by 2030, up from less than 2% in 2020

This is changing more than procurement. It is changing how power and data-center projects need to be developed and contracted.

The traditional assumption that major equipment procurement can wait until full notice to proceed is increasingly untenable. By then, the delivery date may already be incompatible with the targeted COD.

Utilities and developers are responding by reserving factory capacity years in advance, placing orders before designs are final, refurbishing older transformers, using multiple suppliers and asking large-load customers to fund long-lead equipment upfront.

That moves procurement risk earlier in the project lifecycle.

Who owns the factory slot before the project reaches FID? Can it be assigned to a project buyer, lender or replacement contractor? Who bears the cost if the design changes after the order is placed? What happens to the deposit if the load does not materialize? Who absorbs tariffs, escalation or the cost of qualifying a substitute supplier?

Those questions used to sit below the headline commercial terms. They now determine whether the project can be built on schedule.

The domestic supply-chain problem makes the tradeoffs harder. One California utility told Reuters that roughly three-fourths of its recent equipment bids came from overseas suppliers, including manufacturers in China and South Korea. Domestic suppliers generally quoted higher prices and longer lead times.

Developers are therefore being forced to balance schedule, cost, bankability and country-of-origin requirements at the moment when project specifications may still be evolving.

The most valuable item in an AI power project may no longer be only the interconnection position.

It may also be the production slot for the equipment required to use it.

The AI infrastructure race is becoming a race for factory capacity.

Bitcoin mining may be the least valuable use of a Bitcoin miner’s power.

MARA’s stock jumped nearly 10% after it agreed to acquire a 1,200-acre powered site in Matagorda County, Texas.

The site is expected to provide 1 GW of grid capacity by October 2027 and 2 GW by April 2028. MARA plans to develop it with Starwood Digital Ventures for high-performance computing and Bitcoin mining.

The important part is what MARA did not announce.

No new mining machine. No improvement in hash rate. No major reduction in mining cost.

It acquired a path to 2 GW of power.

The market rewarded MARA because a large, grid-connected site now has more than one potential use. Bitcoin mining can generate revenue while the campus is developed, but the larger upside may come from converting that power into long-term AI infrastructure.

That makes mining an unusually effective bridge business.

Mining equipment can be installed quickly, curtailed when power prices rise and removed when a higher-value customer arrives. The land, substations, transmission rights and interconnection work remain.

But investors should be careful with the word “power.”

Two gigawatts expected on a development schedule is not the same as 2 GW available today. The value depends on whether the capacity is contractually committed, what upgrades remain, who funds them, what security has been posted and whether the energization dates are enforceable.

It also depends on whether the site has the fiber, water, cooling infrastructure and reliability required for AI workloads. A good Bitcoin site is not automatically a good AI campus.

Still, the strategic direction is becoming difficult to ignore.

Some publicly traded miners are evolving into power-development platforms with mining revenue attached. Hash rate measures what those companies produce today. Deliverable megawatts determine what they could become tomorrow.

The winners will be the miners that can convert speculative grid capacity into date-certain, financeable AI infrastructure.

The others will remain commodity businesses tied to the price of Bitcoin.

The most valuable thing some Bitcoin miners can do may be to stop mining Bitcoin.

An aluminum smelter in Kentucky was idled because electricity became too expensive.

Anthropic just signed a $19 billion lease to turn the same site into an AI campus.

Century Aluminum’s Hawesville facility was once the second-largest aluminum smelter in the United States. It shut down in 2022 after power prices surged and was never restarted, even after aluminum import tariffs were increased to 50%.

TeraWulf acquired the 750-acre site in February. The property came with something far more valuable than the old industrial buildings: approximately 480 MW of existing power availability.

Anthropic has now leased 401 MW of critical IT capacity there for 20 years. The data center is expected to begin operating in the second half of 2027 and reach full capacity in early 2028.

The grid connection that could no longer support competitive aluminum production is now expected to support $19 billion of contracted AI-infrastructure revenue.

That is a remarkable change in the economic value of electricity.

AI companies are not only creating new power demand. They are beginning to compete with manufacturers for the industrial sites where large amounts of power can already be delivered.

Former smelters, steel mills and other heavy-industrial properties often have exactly what data-center developers need: large substations, transmission access, industrial zoning, water infrastructure and enough land to build at scale.

They also offer something that cannot be manufactured quickly: time.

Tariffs can increase the price of imported aluminum. They cannot create a new 400 MW grid connection or make electricity cheap enough for an energy-intensive plant to restart.

If the same powered site can support either commodity manufacturing or a 20-year AI lease, capital will predictably move toward the higher-value use.

The United States wants both an AI buildout and a manufacturing renaissance. Hawesville shows why those goals eventually collide if power supply does not grow with them.

America cannot treat electricity as a fixed resource while promising unlimited expansion of both compute and industry.

#AI #datacenters #power #Anthropic

Carlyle just made more than 5x on the least glamorous part of the AI boom: getting electricity to the site.

It created Copia Power in 2021. EQT is now buying the business for $2.6 billion.

Copia has:

• 2.6 GW of generation and storage operating or under construction

• Another 20 GW of power projects in development

• 9 GW of power intended to support planned data-center campuses

The interesting part is not just the return. It is that the asset class changed underneath Copia.

Five years ago, a power-development pipeline was valued primarily based on interconnection rights, construction maturity and its prospects for securing an offtake contract.

Today, that same pipeline also carries option value based on how many data-center campuses it can unlock and how quickly it can deliver power to them.

That helps explain why EQT is the buyer. It already owns EdgeConneX, a major global data-center developer. Adding Copia gives it the ability to assemble land, interconnection, generation, storage and data-center capacity within the same investment ecosystem.

AI has created a basic timing mismatch. Demand for compute can materialize in months. The power infrastructure needed to serve it can take years.

A data-center developer that depends entirely on the utility cannot control that schedule. A platform that can develop the load and its power supply together can.

The same megawatt is worth more when it unlocks an AI campus than when it is simply another generation project waiting for an offtaker.

Carlyle’s 5x return is the market putting a number on that difference.

CATL was supposed to supply all 19 GWh of storage for the largest solar-plus-storage project ever attempted.

Eighteen months later, its TENER platform appears to have disappeared from the project.

Masdar’s Abu Dhabi RTC project combines 5.2 GW of solar with 19 GWh of storage to deliver up to 1 GW of renewable power around the clock. When the project was announced in January 2025, Masdar named CATL as the preferred supplier for the entire BESS scope.

The supplier mix now looks very different.

Sungrow signed an agreement in May to provide 7.5 GWh of PowerTitan 3.0 systems. BYD has now signed for another 11.275 GWh using its Haohan platform.

Together, those announcements cover 18.775 GWh, effectively the project’s stated 19 GWh once rounding and potentially different measurement conventions are taken into account.

That is a major reversal for CATL. But I would be careful calling it the loss of a signed 19 GWh award.

Masdar originally described CATL as the “preferred supplier.” In the same announcement, it expressly stated that letters of award had been signed with the two EPC contractors, but did not say the same about CATL. CATL later described the relationship more definitively, but the public record does not establish that it ever had a final supply contract for the full project.

That distinction is not merely semantic. On a $6 billion project, naming a preferred BESS supplier is only the beginning. The bankable commitment comes when the supply and long-term service arrangements are executed and their pricing, schedule, performance guarantees, remedies and interface obligations are coordinated with the applicable balance-of-plant EPC contract. Nothing publicly available shows that CATL ever reached that point.

The new supplier split also looks more connected to the project’s packaging than the simple explanation that Masdar wanted to diversify.

Masdar divided the project between two EPC contractors and two module suppliers from the outset. Sungrow’s package combines 7.5 GWh of storage with 2.6 GW of PV inverters, exactly half of the project’s solar capacity. BYD’s scope is described separately as a 1.644 GW / 11.275 GWh battery station.

That suggests Masdar may be procuring integrated technology packages around separate plant or EPC scopes, rather than merely replacing one supplier with two.

Diversification is not free at this scale. Two BESS platforms mean two degradation profiles, safety cases, control architectures, warranty regimes, augmentation strategies and commissioning programs. All of that must ultimately support a single obligation to deliver up to 1 GW of power continuously.

The commercial question is therefore not just who supplies the cheapest cells. It is who takes responsibility for the complete system and its interfaces.

Sungrow is supplying an integrated AC-block platform together with the PV inverters. Its system is designed to operate at up to 55°C without derating and includes the PCS and plant-level controls. BYD brings its own cells, BMS, storage platform and EMS.

Masdar may be buying two different packages of performance responsibility, not simply two piles of batteries.

Why CATL’s TENER platform fell out of the named scope is still unclear. It could be price, technology, schedule, EPC alignment, performance guarantees, financing requirements or broader commercial negotiations. The public announcements do not provide enough evidence to choose among them.

The other important development is where this is happening.

The Gulf is no longer simply an attractive export market for battery suppliers. It is becoming the place where new storage platforms are proven at a scale that can influence product design, warranty standards and future financing precedent.

Amazon is committing roughly $7.5 billion of rent over 15 years to Cipher, a company best known as a Bitcoin miner. At first glance, the economics look extreme. The delivery schedule explains a lot of them.

Cipher signed the Black Pearl lease on October 28, 2025. The first halls are supposed to be rack-ready by September 30, 2026, with rent starting the next day. That is an eleven-month schedule for a major AI data-center project.

Cipher can move that quickly because much of the difficult grid work was already done. Black Pearl’s substation was energized in June 2025 for a Bitcoin operation that eventually reached 150 MW. Amazon signed later that year, and mining stopped in February. At Stingray, Amazon committed while the site was still dirt, more than six months before scheduled energization.

In practical terms, Bitcoin mining allowed Cipher to generate revenue from its interconnection while it waited for a more valuable use. Amazon is not really paying for a former mine. It is paying to avoid spending years securing the same grid position somewhere else.

The rent reflects that value. The two campuses will provide 286 MW of critical IT capacity within a 400 MW development program. Blended effective rent is approximately $146 per kW-month, with a triple-net structure, a 3% annual escalator and an Amazon parent guarantee.

Cipher’s development cost is capped at $9.5 million per critical IT megawatt at Black Pearl and $10.5 million at Stingray. Costs above those caps are Amazon’s responsibility.

That produces a projected 14.6% unlevered yield on cost for Cipher. The projects are also being financed at essentially full loan-to-cost through bonds priced at 6.0% and 6.125%, and Cipher gets reimbursed for the equity it invested before financing.

Those are unusually favorable landlord economics. But they make more sense if the product is viewed as capacity on a date certain, rather than simply land and buildings.

West Texas power is not especially cheap on an average-price basis, either. Over the trailing twelve months, ERCOT’s West Load Zone had the highest mean day-ahead price among Texas’s four major load zones at approximately $39.80/MWh.

The same zone had negative prices in roughly 6% of all hours, about eight times the frequency in any other major zone. That volatility is useful for a Bitcoin miner that can quickly reduce or increase its load. An AI campus is not designed to rely on curtailment in the same way.

Because the leases are triple net, Amazon bears the power cost. It signed both deals anyway. That suggests availability mattered more than finding the lowest average energy price.

The value of an existing grid position should only increase under ERCOT’s new review process for loads of 75 MW or more, which requires security and fees of $50,000 per MW. A company that already controls an energized site is not just ahead in the queue. It may be avoiding the queue altogether.

This is an interesting middle ground between a hyperscaler self-build and a fully outsourced data-center lease. Cipher controls the land, interconnection and construction process. Amazon provides the long-term credit commitment and assumes some of the development risk. The bond market funds most of the conversion.

I suspect we will see more miners pursue this model. Their advantage is not necessarily that they know how to build AI data centers. It is that some of them already control the part of the project that takes the longest to replicate: large amounts of energized land.

Everyone says the U.S. needs a lot more power for AI.

Then we make 92 GW of wind, solar and storage projects wait longer for permits.

That is the part that makes no sense.

Reuters reports that stalled federal permits are putting more than $121B of clean energy investment at risk. Wood Mackenzie says about one third of the early stage U.S. renewables pipeline now faces extra federal review.

This is not just about projects on federal land.

A solar project on private land can still need federal approvals for wetlands, endangered species, wildlife habitat, access roads, transmission crossings or other pieces of the site plan.

Wind has another layer: airspace review. If the Department of Defense or FAA process slows down, the project slows down too.

So the headline number is not really the issue.

The issue is that a project can have a willing landowner, a developer, a tax credit plan, a buyer, a lender and equipment lined up, and still sit because one federal approval is stuck.

That matters because clean energy projects are not static while they wait.

Modules, turbines, transformers and batteries have procurement windows. Interconnection studies have milestones. Tax credit assumptions depend on timing and eligibility. Power purchase agreements often have deadlines. Financing commitments are not open ended forever.

Delay one piece and the whole deal can start to wobble.

That is why permitting is not a paperwork problem.

It is a financing problem.

If the U.S. wants to power data centers, factories and electrification, it needs new generation that can actually get built.

Planned megawatts are nice.

Permitted megawatts are what count.

#EnergyTransition #Renewables #ProjectFinance #Permitting #DataCenters

MasTec is one of the largest infrastructure engineering and construction companies in North America, with businesses across power delivery, communications, clean energy, pipeline infrastructure and civil construction.

Its agreement to buy The Superior Group for about $1.65B is not just another AI infrastructure acquisition.

It is a bet that the next bottleneck is execution capacity.

Superior brings roughly 3,000 employees, one of the largest scaled self perform electrical workforces in the U.S., and projected 2026 revenue of $1.6B to $1.7B with $225M to $250M of adjusted EBITDA.

That is not a small tuck in.

It is MasTec buying a major piece of the labor and electrical execution layer behind the data center buildout.

The strategic logic is clear.

MasTec already had much of the outside the fence stack: power generation, natural gas infrastructure, transmission, substations, communications and site civil work.

Superior brings the inside the fence stack: electrical systems, integrated building systems, prefabrication, modular manufacturing, project management, maintenance and retrofit services.

In plain English:

MasTec is trying to connect the grid side of the data center problem to the building side of the data center problem.

That matters because the AI buildout is no longer constrained only by capital, land or power procurement.

It is increasingly constrained by who can actually deliver complex electrical work at scale.

Superior reportedly grew from about 800 to 3,000 employees in three years. MasTec expects it to contribute $800M to $900M of revenue for the rest of 2026 and $2.2B to $2.5B in 2027.

That growth tells you where demand is going.

Everyone talks about megawatts.

But megawatts still need substations, switchgear, cable, integrated systems, prefabrication, field labor, commissioning and maintenance.

The scarce asset is not just power.

It is the ability to turn power into an operating facility.

That is why this deal is interesting.

MasTec is not just buying exposure to data centers.

It is buying the capability to self perform more of the critical path.

In the AI infrastructure market, the winners will not be the firms that announce the most capacity.

They will be the firms that can actually energize it.

#DataCenters #PowerDelivery #EnergyInfrastructure #MasTec