SaaS rebound?

The current 2026 SaaS rebound is the most aggressive in a decade: +38% in just 34 trading days off the April low.

But it's also the narrowest — just 10 companies drove ~80% of all the market cap regained (CRWD, DDOG, PLTR, SNOW, PANW, etc…).

The median stock? The company still trades at 3.3x NTM revenue. Analysis below thanks for @ausw2000:

The profitable SaaS IPO is back? 📈

Entrata just filed: $574M implied ARR, +23% growth, and GAAP-profitable (18% operating margin, +11% net income). They offer a leading property management software solution and are PE-owned (founded in 2003).

It's the largest software company ever to IPO while growing 20%+ and GAAP operating-profitable.

Every name that filed at this scale — Snowflake, Palantir, Figma, Dropbox — was losing money. The last profitable-growth SaaS IPO like it was Veeva, at half the size. We looked back at over 150 SaaS IPOs.

It will be an interesting case study on what's possible for valuation for Cloud 1.0 companies vs. AI-native...likely at least $5 billion.

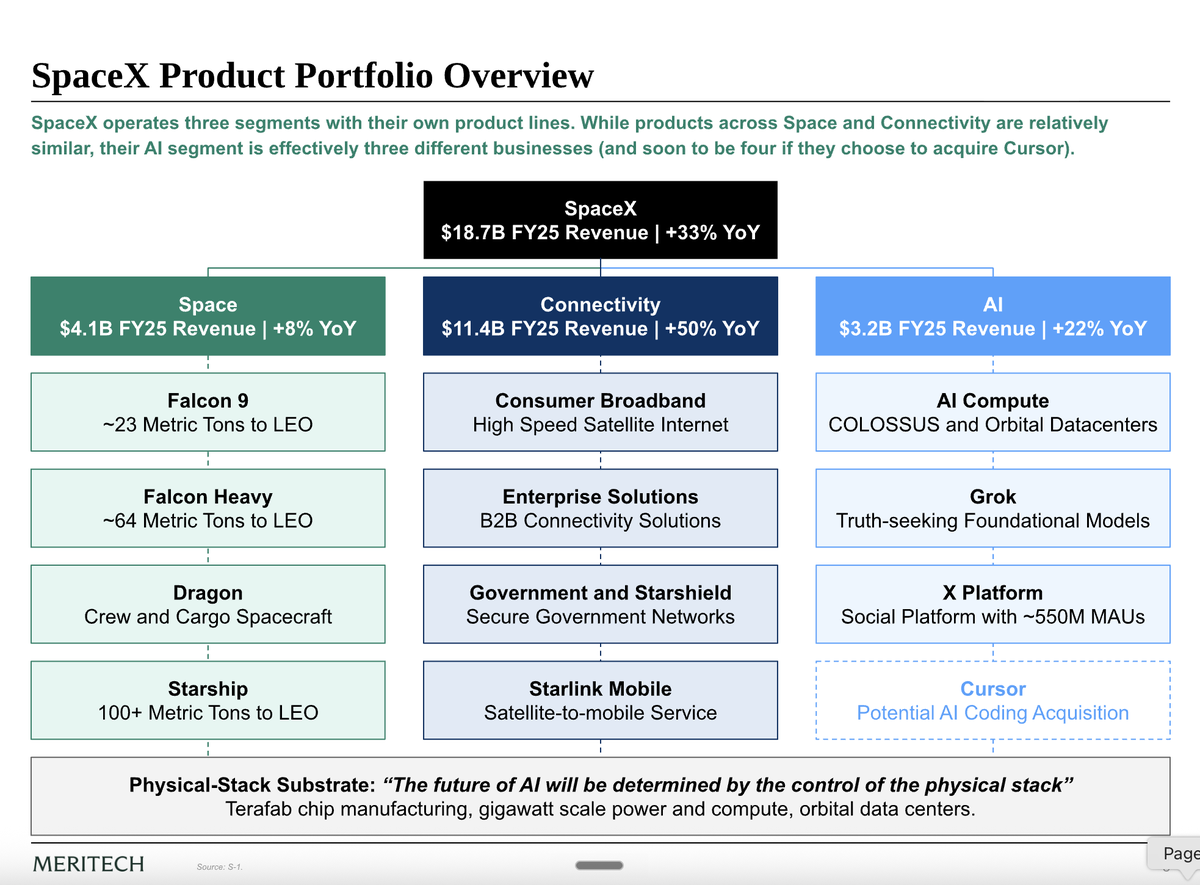

SpaceX filed its S-1 last week, and my partner @ausw2000 read all 318 pages (and made all the charts) so you don’t have to. The result: three businesses in one — Space, Connectivity (Starlink), and AI. AI is set to become the largest revenue segment within a year.

The company did $18.7B in FY25 revenue, up 33% YoY, and is reportedly expecting a $1.75T valuation that would make it a top-10 company globally.

Success in software is diverging…the AI cohort (perceived AI tailwinds) trades at >3x premium on a median NTM revenue multiple basis (8.8x vs 2.8x).

On a free cash flow multiple basis, it's slightly wider: 43x vs 12.7x.

And the gap is widest on profitability — on a non-GAAP EBIT multiple basis, it's 66x vs 15x, a ~4x premium. The market isn't just paying for growth anymore, it's paying for the durability of earnings in an uncertain future for software.

@sethweathers@nikitabier@rahul Do you use any Google or Meta products? Or do you use the internet? Not only does Flock NOT sell your data like those companies do, but they also delete it every 30 days. There is no backdoor. Just do a bit of research on how Google or Meta treats your data...

Public safety should be a human right in America, and @Flock_Safety and @glangley are leading the way. There has been a shocking level of disinformation and propaganda spread about the company and its technology over the past 12 months.

The most insidious part of this campaign is that it has hurt the very people its perpetrators claim to protect — the less fortunate Americans who cannot afford private security, live in gated communities, or who don't have to worry about the devastating effects of crime on their doorsteps. Citizens should be demanding objectivity over bias from their state and local governments, and that is exactly what Flock provides.

Flock is and always will be on the right side of public safety by prioritizing objectivity over bias in law enforcement.

Yesterday, 12 shootings reported across Austin led to a manhunt that involved 200 officers including SWAT, air and canine support over several hours. The suspects were found and arrested as they entered Flock-supported Manor. If @Flock_Safety wasn’t able to aid Manor PD and Austin PD in this case, how many more could have been harmed?

50% of murders to walk free in America. Privacy in public is an ill-informed position if it allows an active shooter several hours to escape and harm more and actively ignores public safety results where Flock is present.

Austin ended its contract with Flock. Its homicide rate is +36% its pre-pandemic baseline, per the Council on Criminal Justice. That doesn’t just put the people of Austin at risk. I’m glad we could help stop the spread of this kind of senseless violence before it affected neighboring communities like Manor.

When Austin is ready to prioritize safety for everyone, we welcome the chance to speak with the City Council about reversing their decision.

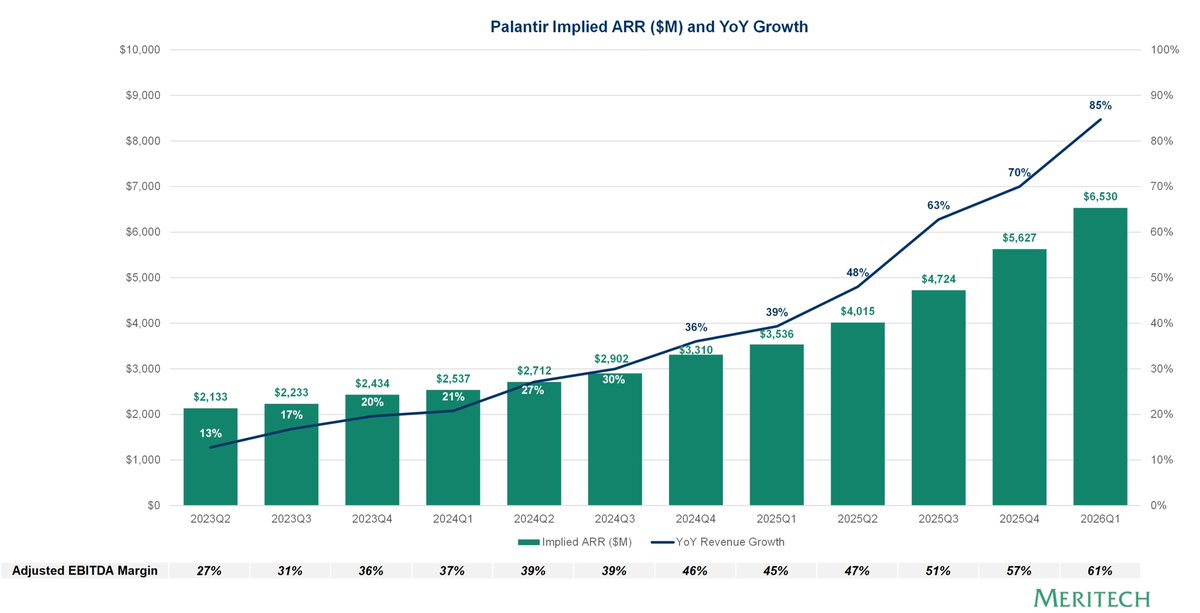

Palantir ($PLTR) has just done what no other technology company has ever done.

We track 300+ companies with trading data going back to 1989 (17,000+ reported quarters), and only one company has had an 11-quarter revenue acceleration streak, and that is Palantir ($PLTR).

Palantir has gone from $2.1B of ARR, growing 13%, to $6.5B, growing 85%. Adjusted EBITDA margins have also more than doubled to 61% over the past 3 years.

Atlassian's ($TEAM) stock was up 30% today. The company reported revenue growth accelerating to 32% year over year to $7.1B in ARR.

Most importantly, they reported credit usage: tokens were growing rapidly.

"In AI, we continue to add millions of monthly active users to Rovo and our AI Rovo credit usage is growing more than 20% month-over-month. Customers using Rovo are also growing their ARR at roughly 2x the rate of customers who are not using Rovo, contributing to our strong cloud outperformance and expansion in the quarter...."

Every public software company should figure out how to get into the token flow to accelerate growth.

I'm excited to share that @getavoca has raised over $125M across Seed to Series B at a $1B valuation, backed by Kleiner Perkins, Meritech, General Catalyst, Amplify, and more to build AI agents for the services economy. Thank you to @FortuneMagazine for the exclusive cover.

https://t.co/sjAxVKCLGm

Chart of the Day — Collaboration with @arakharazian and @tryramp

AI labs: 74% consumption-based pricing.

Traditional SaaS: 96% seat/platform — largely static over the past 11 months.

AI reprices software around consumption — SaaS incumbents have not yet transitioned.

Source: Ramp, Coatue Analysis as of April 2026