Much has been written about the SpaceX S-1 and this Financial Times article really stood out for me. It reminds me of https://t.co/aCXxoe7TQS. It went public in February 2000, ringing the bell on the last Nasdaq peak that followed in March. It lost roughly $10 for every $1 of revenue and still managed to raise cash at 52x revenue.

It's worth watching the famous Sock Super Bowl commercial to understand the hype: https://t.co/oZBJEnajsK

Having now observed many cycles, I can say with confidence that every cycle eventually develops its own explanation for why traditional financial analysis no longer matters. The SpaceX issues are "flammable," as I like to say, in an outer-worldly level.

The most dangerous markets are usually the ones where investors have gradually forgotten to ask about cash flow, capital intensity, governance, dilution, accounting assumptions, and who is actually achieving liquidity from the enthusiasm. Those questions never go away. Investors just temporarily lose interest in the answers because everyone is making money.

In the meantime, it's getting hot in here…

Anyone else seeing similar examples out there right now?

https://t.co/VM3SbQwKa7

We're hiring!

As a Communications and Marketing Specialist, you will help edit newsletters, develop external marketing efforts, manage social media accounts and develop content marketing across the Veritas Group of Companies.

https://t.co/TdCsxMTFeh

We've been talking and writing about accounting red flags (what we call Flammable Items) at Nvidia Corp. for a couple of years now and let's just say they're not going away. In fact, they are becoming more obvious.

Our Special Situations Analyst, Ben Butler, CFA, CPA, wrote about Nvidia's circular cash flow again last week, where it invests in its customers in return for sales.

Disclosure has always been fuzzy on this item, but investors can infer how much NVDA invests in customers from its investments in non-marketable securities, which totalled $18.6 billion during Q1-F27, up from $12.8 billion in Q4-F26. Over the same three-month period, NVDA's total revenue increased sequentially by $13.5 billion, from $68.1 billion to $81.6 billion. Assuming 80% of equity investments in Q1-F27 flowed to direct customers, as precedent would suggest, NVDA's supplier-funded capital of ~$14.9 billion could have financed more than 100% of incremental revenue growth in Q1-F27, if we assume customers redeployed equity proceeds into GPU purchases.

As Ben wrote, GPU procurement this quarter could have been materially lower absent NVDA's equity investments.

The full report last week for our clients also delved into disclosure changes, actual free cash flows versus headline free cash flow, and more.

What other flammable items are investors seeing out there?

Notes on the table below: Investment in non-marketable securities of customers reflects 80% of total cash outflows related to non-marketable securities. Since 2023, we estimate at least 80% of NVDA equity investments have been in direct customers. Source: Company filings, Veritas

#accounting $NVDA

We'd like to welcome our summer intern at Veritas Investment Research, Matthew Fortier. He is pursuing a Bachelor of Engineering in Engineering Physics at McMaster University.

During COVID, the volatility in financial markets piqued his interest and the markets. He started reading investing books and diving into Warren Buffett's work. As an engineering student, he likes solving complex problems, and the stock market may be the most complex of all of them.

He is currently working with Will Guy, CPA, CFA, our Diversified Industrials Analyst, on freight volumes and with Liam Gallagher, our Communication Services & Information Technology Analyst, on sports valuations.

Welcome to the team!

We'd like to welcome our summer intern at Veritas Investment Research, Matthew Fortier. He is pursuing a Bachelor of Engineering in Engineering Physics at McMaster University.

During COVID, the volatility in financial markets piqued his interest and the markets. He started reading investing books and diving into Warren Buffett's work. As an engineering student, he likes solving complex problems, and the stock market may be the most complex of all of them.

He is currently working with Will Guy, CPA, CFA, our Diversified Industrials Analyst, on freight volumes and with Liam Gallagher, our Communication Services & Information Technology Analyst, on sports valuations.

Welcome to the team!

This is an excellent article about how AI is forcing accounting schools to quickly redesign their curricula, with students now learning to use automation tools to analyze transactions, generate audit workpapers, and review disclosures.

While the technology is impressive, it is worth reminding everyone that accounting failures rarely happen because data wasn't processed quickly enough or accurately. They happen because management incentives, aggressive assumptions, and weak skepticism go unnoticed or unchallenged. AI may make auditors more efficient, but it won't replace the judgment investors rely on to separate economic reality from financial storytelling.

Yes, AI can help identify anomalies in large datasets, but it cannot determine whether management's accounting choices and assumptions are reasonable or whether disclosures are intentionally selective. In fact, I think there is a risk that AI gives investors a false sense of confidence. After all, it is replacing the human "bean counters" who might make mistakes.

But that's not really what great auditors are all about. The accounting profession absolutely must embrace AI. But the most important skill for the next generation of accountants, not to mention analysts at Veritas, will still be the oldest one: professional skepticism.

I'd love to hear about the experiences of using AI in accounting schools from my academic acquaintances and former colleagues. What are your thoughts on it?

https://t.co/PmlvegDmOG

#accounting

Martin Pradier, our Materials Analyst, joined BNN Bloomberg to discuss Franco-Nevada Corp.'s Q1-F26 results. FNV benefited in the quarter from silver prices rising 165% and platinum rising 128% YoY, outpacing gold's 70% YoY increase.

Furthermore, the company has been buying more streams, and Martin expects the Cobre Panama mine to reopen this year, which could be a major catalyst for the stock. "We believe the mine [Cobre Panama] will be restarted because Panama needs that mine," he said.

https://t.co/WZAVnt01PF

$FNV $FNV.TO

We're hiring!

As a multi-sector Research Associate at Veritas, you will have the rare opportunity to support both our Consumer Staples & Discretionary and Mining & Materials analysts, gaining broad exposure across diverse industries, investment theses, and analytical approaches.

You will play a key role in fundamental, accounting, and valuation analysis, helping to assess business models, operations, financial reporting, and governance, while developing versatility and intellectual flexibility through cross-sector experience.

Join a team that thrives on collaboration, knowledge-sharing and independent thought.

https://t.co/nAVb63tiGa

Our Analyst, Liam Gallagher, was the only analyst going into the quarter with a Sell recommendation on Shopify Inc. As this Bloomberg article details, he put a Sell on the stock in August when it was trading at about 95 times forward earnings.

The article adds that he held the rating as Shopify rose through the fall, but the call proved prescient as the stock then plunged more than 30% from the peak.

Shopify is down a further 15% today after reporting Q1 results.

“It’s a really high quality business, but the cost of admission is too high,” Gallagher said in the article, published before the quarter. “I am not willing to pay that ticket to get into the concert.”

“With any investment the most important factor to determining your return is the price you pay,” he said in the article, adding that he sees the stock’s valuation as too expensive to generate a strong return over a long period. “Our recommendation was kind of to wait for a pullback to where we view it more reasonably.”

(Note: Liam hasn't updated his recommendation yet for our clients as of the time of this post.)

$SHOP $SHOP.TO

https://t.co/hX7dTGOL3L

Despite recent volatility, our Industrials Analyst, Will Guy, continues to call Canadian National Railway his TOP PICK, after the quarter.

“Capital intensity is resetting lower, while benefits from recent investments are beginning to emerge,” he told the Globe & Mail in this article, adding that railway-specific performance metrics, such as car velocity and gross ton-miles per train and engine, moved in the right direction in the first quarter.

“Our thesis rests on evidence of underlying operational and commercial momentum, even if near-term noise challenges headline figures."

$CNI $CNR.TO

https://t.co/9cYJlZ6Q9W

If you're an entrepreneur, founder, or leading a team, you probably know how hard it is to stay focused on what actually matters. In my experience, it doesn't get easier as you grow. If anything, the noise just gets louder and focused time management becomes paramount.

I had a very meaningful conversation about this on a recent Fact Finder podcast episode with George Rivera. George has been building and operating businesses for over 30 years and is the founder of Buy Back Time Formula. His whole approach is about helping leaders get back 10–20+ hours a week by cutting through the clutter. He helps rethink how decisions get made, remove low-value work, and be much more intentional about what stays on your plate.

Over his career, George has generated more than $400M in online sales, but what stuck with me most wasn't the numbers, it was this truth: You can always make more money, but you can't get time back.

In episode 136, he also shares a personal turning point about his son, Leo. His father, near the end of his life, told him, "Don't miss Leo's games. I missed too many of yours." Hearing George's story also reminded me of my work sessions with my dad when he played Harry Chapin's "Cat's in the Cradle". I didn't realize how powerful the lyrics were at the time.

One of the practical tools he talks about is doing a two-week time audit, tracking everything you do, then applying what he calls a "$10K per hour test" to figure out what you should eliminate, automate, or delegate. He realized he was spending 40 hours a week on $50/hour work.

This line really stayed with me: "It starts with holding that mirror in front of your face and being honest with what it says."

Do yourselves a favour, whether you listen to the podcast or not, listen to the song by Harry Chapin and let me know how you are approaching this age-old challenge.

https://t.co/E8XQnzRoj7

@GeorgeR76991

It's hard to think of anyone I have more fun talking about the housing market with than Ron Butler of Butler Mortgage. I was on his Angry Mortgage podcast again this week, this time discussing my latest condo mystery shop in Vancouver, government bailouts for developers and condo vulture funds.

If you're also wondering what a condo mystery shop is, we started them at Veritas 14 years ago. The premise was that the Toronto condo market was starting to take off, and we wanted to know why. I took a group of clients to visit a number of condo developments and went through the full process of buying a condo, only to return it before the 10-day cooling-off period. (Imagine…damn…)

It was on-the-ground research that we couldn't get from a real estate board report or Statistics Canada. Over the years, we started adding speakers after the mystery shop, then panels, and pretty soon, we had a full-day real estate conference (the next one is in October).

Looking back over the years, these mystery shops became more and more like visits to nightclubs or fashion shows. The hype kept growing, and nowhere was it more surreal than Vancouver.

Probably the most awakening moment for me was a few years ago, when, during a mystery shop in Vancouver, I asked the salesperson about rental income. My father had drilled it into me that cash coming in must always be higher than cash going out. That was the real estate golden rule.

But this salesperson looked at me like I had four eyes. Clearly, I wasn't familiar with the market. No one bothered with that question. Prices in Vancouver only went up!

Back to current market conditions. A year ago in Vancouver, developers were offering so-called "decorator allowances" to condo buyers. The arrangement allowed buyers to get the discount they were looking for, the developer moved the unit, and the existing owners in the building were happy that headline prices were holding up.

This year, we found that even steeper discounts were available as long as you signed a non-disclosure agreement. We also discovered that many more units were available than are listed.

As we wrote in a report for clients earlier this month, the shadow pricing and shadow inventories can only undermine price discovery. Buyers lose trust in price listings. Sellers grow more desperate. Buyers wait for more desperation. The spiral deepens.

Have a listen to the podcast (we do our best to lighten what are very challenging topics) and let me know if you've found similar shadowy "arrangements" happening in your housing market.

Also, a big shout-out to our good friend Steve Saretsky for organizing our Vancouver mystery shop.

https://t.co/wPrRVp5FrZ

@ronmortgageguy@ButlerMortgages@AngryMortgageCA@SteveSaretsky

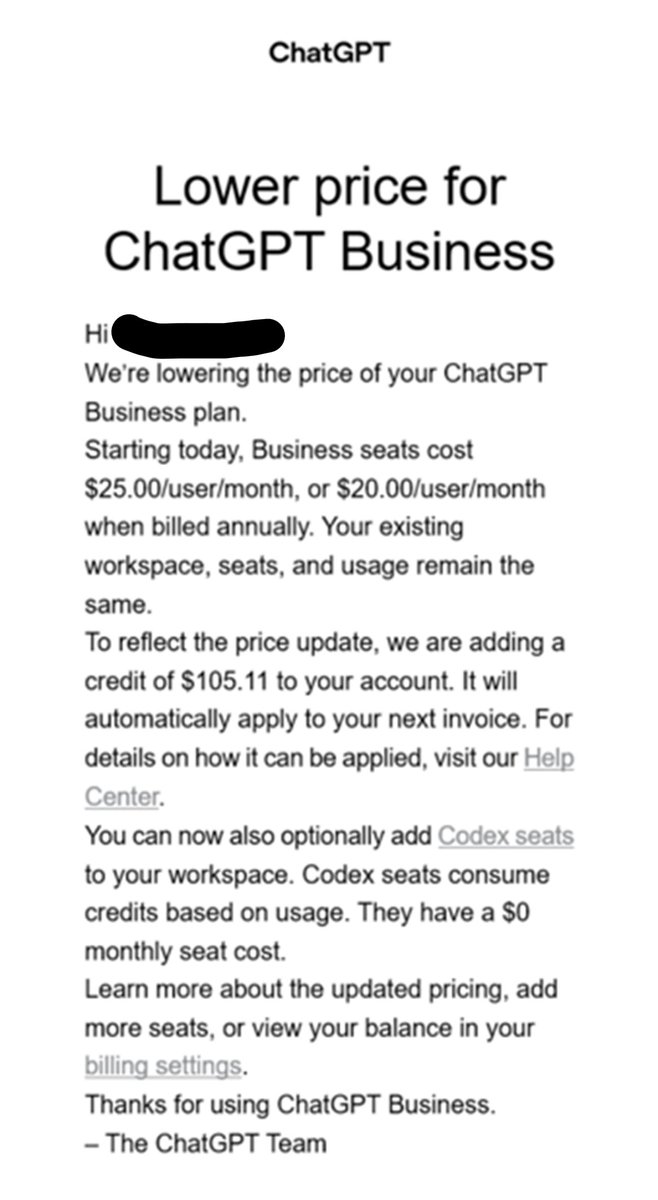

Demand for AI is insatiable, right? Well, has anyone else received one of these price-reduction notices from ChatGPT recently?

It's usually not a good sign when a company gives you an unasked-for 20% discount and a credit to boot.

We've written and spoken a lot about how the AI industry's financial engineering is driving unsustainable growth rates.

What if the forecast profits are pushed further and further into the future? What if the AI platforms have built out too much capacity and the market is unwilling to pay for access?

I'll follow up with more comments after I hear from you.

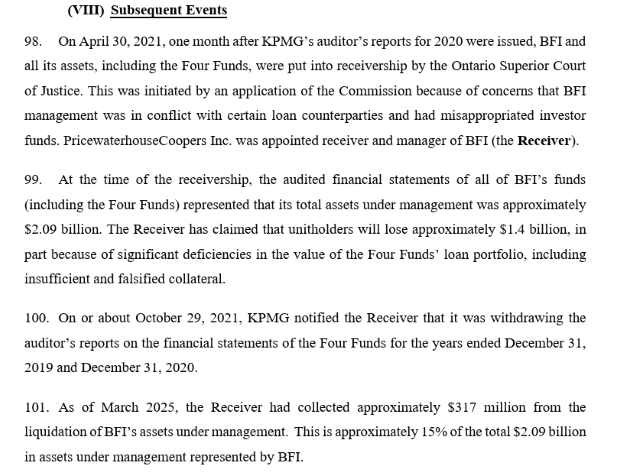

We hope everyone involved in the investment industry has read about the OSC's action against KPMG. It has ramifications for auditors, accountants, and investors in public and private securities.

The OSC's Application for Enforcement Proceedings makes for some interesting reading and reminds us of the complacency in the market that led us to found Veritas in 2000. During the dot-com bubble, auditors were doing less auditing, traditional sell-side analysts were doing less analyzing, and investors were making decisions based on fewer fundamentals. Sound familiar?

More to the point about Bridging, our concerns about private credit began almost a decade ago (remember Callidus Capital?). This Bridging case could set a precedent for other private credit and MIC structures that, based on our work, could face similar collateral shortfalls.

What's interesting about the OSC's approach is that it isn't just going after KMPG for technical auditing mistakes, but for failing to uphold auditing standards and for undermining public trust, a key tenet of the audit profession.

For instance, the document says KPMG failed to conduct the audit with "professional skepticism" and failed to subject Bridging Finance management's judgments and estimates to effective scrutiny. This, it claims, led investors to have a false sense of confidence in the funds' financial statements and the value of their investment. The OSC argues that auditors are "gatekeepers" to the integrity of capital markets and that they failed to uphold auditing standards.

"Auditors who falsely represent that they have complied with those standards harm investors and undermine the framework for proper disclosure and therefore undermine the public interest."

Strong words and in our opinion, very true.

We hope that this case serves as a good reminder to both auditors and their clients to take their fiduciary duties seriously. The investing public relies on it.

I look forward to your comments and will leave one interesting and, dare I say, "sad" snippet to mull over.

KPMG failed to properly audit private debt manager Bridging Finance, OSC says: https://t.co/tPnXnTTgdk

OSC Application for Enforcement Proceeding: https://t.co/m42l9KjM93

#auditing #accounting

We recently held one of our most popular accounting training sessions ever.

If you missed it, we're still offering the replay for sale. Our AI Sector Hallucinations seminar, led by President and CEO Anthony Scilipoti and Special Situations Analyst Ben Butler, CFA, CPA, took attendees through our proven Forensic Accounting Framework to uncover the true economic substance of the AI sector's performance.

It covered disclosures from the following companies:

• Meta Platforms Inc. (NYSE: META)

• NVIDIA Corp. (Nasdaq: NVDA)

• CoreWeave Inc. (Nasdaq: CRWV)

• OpenAI (Private)

• Microsoft Corp. (Nasdaq: MSFT)

100% of attendees of the live seminar said they would recommend a Veritas Accounting Training course to a colleague or co-worker

Visit our website to find out more and purchase the replay.

https://t.co/o2p0sor40Z

Darryl McCoubrey, VP and Senior Energy Analyst at Veritas, was on BNN Bloomberg to discuss #oil prices and the escalating war in the Middle East.

Leading up to the conflict, Darryl was in the camp believing the industry was facing a supply glut of about three million barrels per day of excess capacity, superimposed on about five million barrels per day of OPEC spare capacity.

Given the ongoing conflict, he raised his WTI oil price forecast this week to US$70/bbl from US$60/bbl and changed his recommendations and valuations accordingly. Of the four oil sands majors, he thinks Canadian Natural Resources and Cenovus Energy stand to benefit the most from higher oil prices. Of the two, he favours CVE.

"We increased both of those valuations by 30%," he said. "The difference is that CNQ's stock has performed relatively well compared to CVE over the past month or so, as signs were becoming clearer that this would escalate and last longer than people had first hoped. CVE is a name that stands out as relatively levered to the higher price environment for investors who see this lingering on for months rather than weeks."

He also discussed how Suncor Energy would be a better name if the conflict ends more quickly and oil normalizes.

https://t.co/z2yTjsRIsU

$CNQ $CNQ.TO $CVE $CVE.TO $SU $SU.TO

Nvidia dealt out a number of "flammable items" in its most recent quarter, the most notable of which is the $13B increase in non-marketable securities, or investments in customers. By our estimation, the advances account for approximately 90% of the sequential growth in revenue for the quarter.

That's up from approximately 30% in the previous quarter. It seems NVIDIA is providing more and more of a helping hand to ensure that its customers can purchase chips. There's so much more I could say, but we'll leave that for our upcoming accounting training.

Next Thursday, our Special Situations Analyst, Ben Butler, CFA, CPA, and I will be running an accounting training seminar called AI Sector Hallucinations. We've put months of work into this.

We'll cover what we call "flammable items" for Nvidia, META, CoreWeave, OpenAI, Microsoft and more. As I like to say, although it is difficult to identify the sparks that will eventually ignite flammable items, identifying them is the secret to capital preservation.

If you didn't know, Veritas has proudly been training our clients and investors with our forensic accounting framework for more than 20 years.

See our website for more details about our latest seminar, focusing on accounting in the AI sector. I hope you can join us.

https://t.co/vxXL2DltY4

$NVDA $META $CRWV $MSFT

Ben and I have put a ton of work into this training, drawing on experiences that go back to Nortel and the dot-com bust of 2000. Please join us.

#accounting

AI will change the world. Whether investors profit is a very different question. We are offering an exclusive forensic accounting training session built on our experience in the dot-com bubble that will take you to 2023, when we first identified early warning signs of stress beneath the AI boom. Since then, growth has been supported by increasingly complex structures that place greater weight on accounting judgment and interpretation.

In this seminar, attendees will learn about our proven Forensic Accounting Framework and key questions that are transferable across any sector, market, and point in the cycle.

Hosted by our CEO, Anthony Scilipoti, and Special Situations Analyst Ben Butler, the seminar will distill reported information to uncover the economic substance of the AI sector's performance, specifically:

• Separating business innovation from accounting innovation to assess earnings and cash flow quality and durability.

• Understanding the flammable items identified: Customer concentration, demand normalization, counterparty risk, and financing dependence.

• How circular financing works: Supplier-funded demand and the leakage of investing cash flows into operating results.

• Evaluate the impact of accounting choices on reported results, including depreciation lives in the face of shortening product cycles, ASC 606 (contra-revenue risk) and ASC 321 (equity accounting vs inter-company profit recognition).

• Understanding off-balance-sheet exposures: SPVs, VIEs, leases, guarantees, and purchase obligations.

We will use company disclosures from:

• Meta Platforms Inc. $META

• NVIDIA Corp. $NVDA

• CoreWeave Inc. $CRWV

• OpenAI (Private)

• Microsoft Corp. $MSFT

Accounting Training

AI Sector Hallucinations

Webinar

Thursday, March 5, 2026

2:00-4:00 PM ET

(1.5 hours presentation and 30 minutes for questions)

Visit our website for pricing and signup:

https://t.co/o2p0sor40Z

@ASclipoti