Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

JUST IN🚨: $NBIS is increasing prices by 30% on the STANDARD on-demand pricing, effective June 1st.

The demand is INSANE and this price increase goes straight to the bottom line.

20 years ago Jane Street's entire compute cluster was six Dell boxes stacked on the floor at the end of an office row. They called it the Hive.

Last week they let Dwarkesh Patel walk through their new Texas data center. 4,032 GPUs. Each rack pulls 140 kilowatts. A normal data center rack pulls 10. 8,000 kilometers of fiber inside one building, and the fastest links are still copper because light moves more slowly through glass than electrons through metal.

Bookmark it tonight. Then read the article below.

Everyone repeat after me…

“Options on a 13F are reported with notional value as if each contract was 100 shares regardless of the actual delta of the contract”

Maybe we can avoid this next quarter (we won’t).

You should build your dream macOS app right now!

The "Build macOS App" plugin in Codex is wild. Used voice dictation to build an app I wanted for a while in <7 min (+6 min of tweaking). Couldn't believe how quickly it was done.

Prompt is in the video and in the tweet below.

BREAKING: The SEC is set to release its so-called "innovation exemption" for tokenized stocks which will pave the path for trading digital versions of securities, per Bloomberg.

Details include:

1. In a "surprise move," the SEC is leaning toward allowing the trading of tokenized assets

2. These tokenized assets would be tradeable on decentralized crypto platforms

3. The move could "reshape the landscape of the American stock market"

4. This would also be one of the US' biggest shifts into crypto infrastructure yet

Tokenized assets are rapidly expanding.

Inside an AI server today, the GPUs talk to each other through copper cables and small pluggable optical modules. Starting in the second half of 2026, that wiring gets replaced by lasers built directly into the chip package (CPO). Goldman thinks the market for that goes from roughly 0 to $91 billion inside 18 months.

That part the Serenity has right. What I’d slightly diverge on is who actually captures it. He says US names like Lumentum and Coherent are capped because they have to outgrow their own pluggable revenue getting cannibalized. True.

The usual response is to buy the pure plays i Taiwan, Europe, and Japan that have no legacy book. The cleaner version of that argument is to keep going one layer up. The laser is the visible part. The wafer the laser sits on is the invisible part, and it has zero legacy revenue.

CPO needs meaningfully more of that substrate per socket than plug-ins did. $SOI, which has the near-monopoly on silicon-on-insulator wafers for silicon photonics, still trades at a low multiple (attractive book value) while photonics peers trade at 5-8x sales.

$AXT and $IQE are the same setup on the indium phosphide side. There is also the supply question. Nvidia spent roughly $4 billion between Coherent and Lumentum, which effectively locks up their laser capacity.

Everybody else (AMD, Meta, Ayar, POET, Lightmatter) has to source elsewhere. Sivers is the small independent that catches that overflow.

And the layer nobody talks about is the assembly itself. Co-packaging an optical engine onto a chip is hybrid bonding. BESI just printed a record order quarter at €269.7 million with hybrid-bonding unit orders more than doubled sequentially.

The bottleneck for H2 2026 isn’t whether the optics work, it’s whether anyone in Taiwan can bond them onto the package fast enough.

The date I would put on the calendar is November 27, 2026. That’s when China’s export-control suspension on gallium, germanium, and antimony expires, about 6 weeks before the H2 2027 scale-up window.

If it gets re-imposed, the substrate names re-rate first, before anybody downstream sees a dollar of CPO revenue. Right gold rush. The interesting trade is one layer further up, where there is nothing to cannibalize and there is a date on the wall.

What if the Solana × Mastercard partnership was announced as a Lord of the Rings trailer?

I reimagined it. Starring @toly as Aragorn. @MiebachMichael as Elrond. @rajgokal as Gandalf. I believe Solana is the future of payments and this partnership just proved it.

this is INSANE

you can now VIBE CODE on your couch wearing a VR HEADSET

with 6 floating screens and no one can judge you

someone just built an app that connects VS Code and Claude Code on your mac

to your apple vision pro

BREAKING: AI can now automate daily options income with 78% win rate like professional theta traders (for free).

Here are 12 insane Claude prompts that generate consistent 0.5-2% daily returns (Save for later)

When building costs drop 90% but distribution costs stay flat, you get a gold rush where everyone digs and nobody sells.

That’s what this chart actually shows. New websites up 40%. iOS apps up 50%. GitHub pushes up 35%. Everyone read “barrier to building disappeared” and heard opportunity. The correct read is that 557,000 new apps hit the App Store last year, a 24% spike, flooding a discovery channel that was already dead on arrival. 90% of senior mobile professionals surveyed said organic App Store discovery was effectively over before this wave even hit. Half of all App Store searches are just people typing in brands they already know.

The supply side hockey-sticked. The demand side didn’t move.

This is why tech layoffs doubled to 264,000 in 2025 while code output simultaneously exploded. Companies don’t need more builders. They need people who can get the thing in front of someone who’ll pay for it. Distribution, positioning, audience, brand. The functions that never got the AI productivity boost.

Nicholas nails the conclusion that taste and knowing what to build are what matter now. But taste is only half of it. You also need the channel. The unsexy reality is that a mediocre app with 100,000 newsletter subscribers will outperform a beautiful app with zero distribution every single time. The apps winning in 2026 aren’t the best-built ones. They’re the ones attached to someone who already has an audience.

Building software used to be the moat. Now building software is the commodity. Distribution is the new moat, and unlike code, it doesn’t get cheaper with AI.

NVIDIA just printed a number that shouldn't be real.

$68.1 billion in one quarter.

That's more revenue in 90 days than the entire company made in fiscal year 2023.

The Data Center division alone did $62.3 billion.

In January 2020, that same division did $1 billion.

That's a 6,300% increase in six years.

No company in history has scaled revenue this fast.

But here's the part Wall Street is really focused on.

Not the record quarter, that's the past.

It's the guidance.

NVIDIA told the market to expect $79.6 billion next quarter.

They expect to make even more.

The gross margin is roughly 75%.

That means for every dollar that flows through NVIDIA, they keep 75 cents before even paying employees.

This is a hardware company with software economics.

There is no comparison in industrial history.

Free cash flow hit $34.9 billion.

Up $20 billion from the same quarter last year.

That's more cash generation in one quarter than Ford, GM, and Stellantis combined generate in a year.

From selling chips.

Here's what nobody is talking about.

NVIDIA said it has visibility to $500 billion in revenue from its Blackwell and Rubin platforms through the end of 2026.

The demand isn't slowing; it's accelerating.

The next-generation Rubin chip is already being fabricated at TSMC.

It arrives second half of this year.

NVIDIA isn't just winning the AI race.

They're lapping everyone else while designing the next track.

At current guidance, NVIDIA is on pace for $318 billion in annual revenue.

The company is now worth $4.76 trillion.

Five years ago it was worth $300 billion.

One company has captured the entire economic engine of artificial intelligence.

And they're just getting started.

I try not to make these comparisons often, but @aave looks very cheap compared to lenders in TradFi.

Price to sales:

$AAVE trades at 2.2x

Klarna trades at 8.9x

Figure 19x

Price to book

$AAVE trades at 2.8x

Klarna 4.1x

Affirm 6.8x

Figure 7.6x

Loans Outstanding

$AAVE $17b

Klarna $10b

Affirm $8.8b

Lending Club $6.5b

Net Interest

Lending Club 6%

Affirm 4%

Klarna 0.8%

$AAVE 0.6% (This is a competitive advantage imo)

TLDR: Aave trades at a lower valuation, the loanbook is significantly undervalued, can operate with lower margins, and continues to dominate.

This same point hit on by Gavin and Citadel Securities. It's a good one.

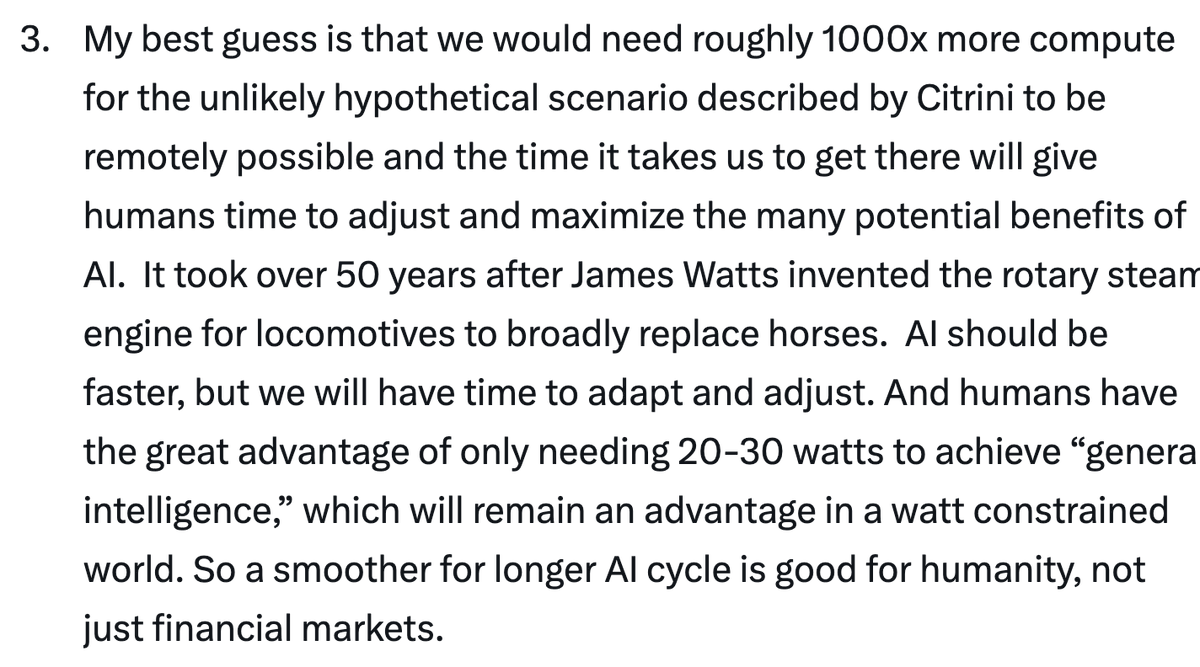

Gavin: "The world is fundamentally short both watts and wafers and it may take years to resolve these shortages. The shortage of watts and wafers may prevent an overbuild - hyperscalers would overbuild if they could, but they simply cannot... My best guess is that we would need roughly 1000x more compute for the unlikely hypothetical scenario described by Citrini to be remotely possible and the time it takes us to get there will give humans time to adjust and maximize the many potential benefits of AI."

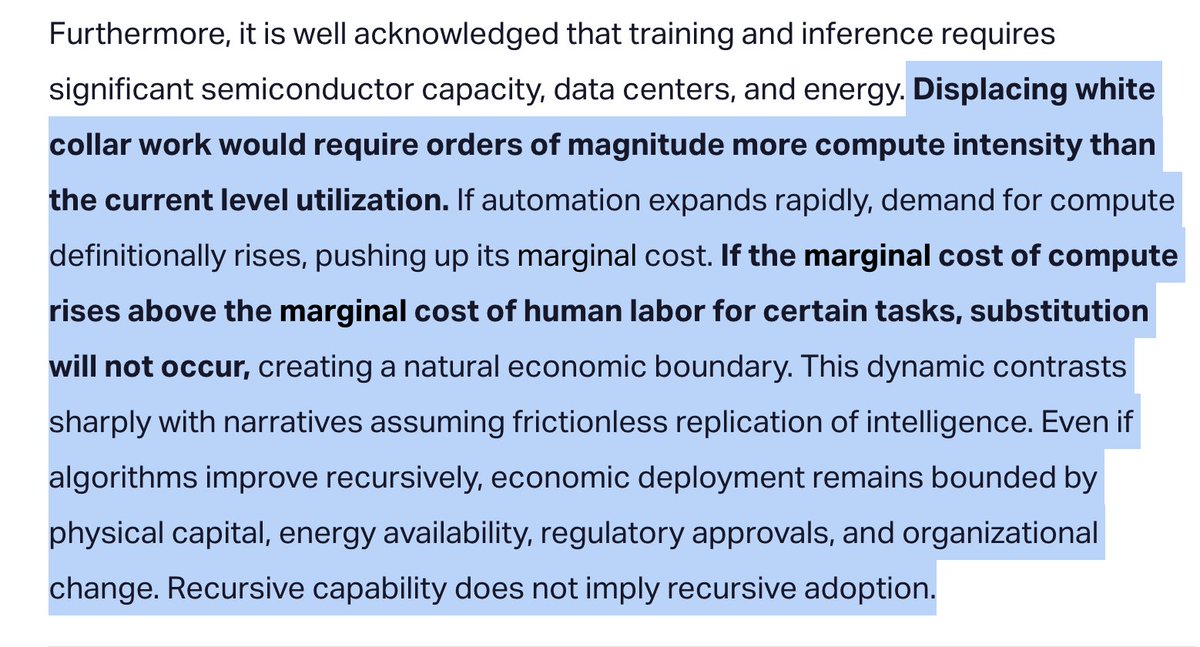

Citadel: "Displacing white collar work would require orders of magnitude more compute intensity than the current level utilization. If automation expands rapidly, demand for compute definitionally rises, pushing up its marginal cost. If the marginal cost of compute rises above the marginal cost of human labor for certain tasks, substitution will not occur, creating a natural economic boundary. This dynamic contrasts sharply with narratives assuming frictionless replication of intelligence. Even if algorithms improve recursively, economic deployment remains bounded by physical capital, energy availability, regulatory approvals, and organizational change. Recursive capability does not imply recursive adoption."