$ENPH

Enphase has an ironclad balance sheet.

Liquidity: Enphase boasts a current ratio of 3.80 and a quick ratio of 3.20. They hold substantial cash reserves and are highly capital-efficient, generating $95.9 million in positive free cash flow even during a severe residential.

Survival Risk: They generate stable profits and do not rely on capital markets or toxic high-interest debt to float their daily operations. They can survive an extended multi-year residential market freeze without diluting a single share

Enphase at sub-$45 gives you an incredibly resilient business trading at an institutional hardware multiple (~21x Forward P/E) with massive cash on hand. You are buying a coiled spring that will explode upward the moment global interest rates cut and residential solar demand normalizes.

$FLNC | $TE | $BE

The Long-Term Takeaway:

Fluence (FLNC) is a company with a cheap valuation (0.8x P/S) that has the backlog but faces minor near-term cash-flow friction.

T1 Energy (TE) is a highly speculative, pre-profit factory buildout that faces extreme dilution and survival risks.

Bloom Energy (BE) is a financial powerhouse with incredible execution, actual net profits, and no survival risk—but it is priced to absolute perfection. A triple-digit forward P/E means any hiccups in the AI data center buildout or supply chain issues will cause swift pullbacks.

Is it theoretically possible that $BE is lying about scandium and that Brookfield, Oracle and Nebius all failed to uncover a fatal supply constraint before committing to multibillion dollar projects? Yes. It’s also extraordinarily unlikely.

Bloom has now stated in an SEC filing that it has sufficient non-China scandium supply for its current demand and backlog, with visibility to support 25 GW of annual production. Brookfield just expanded its partnership to $25B. Nebius committed up to $2.6B. Oracle contracted an initial 1.2 GW under an agreement covering up to 2.8 GW.

Outside scandium estimates are not precision exercises. Bloom’s material intensity, manufacturing yields, inventory, supplier contracts and future efficiency gains are not publicly known.

Read the short report. Read Bloom’s response. Use AI. Do your own work. Make your own decision.

I’m not selling.

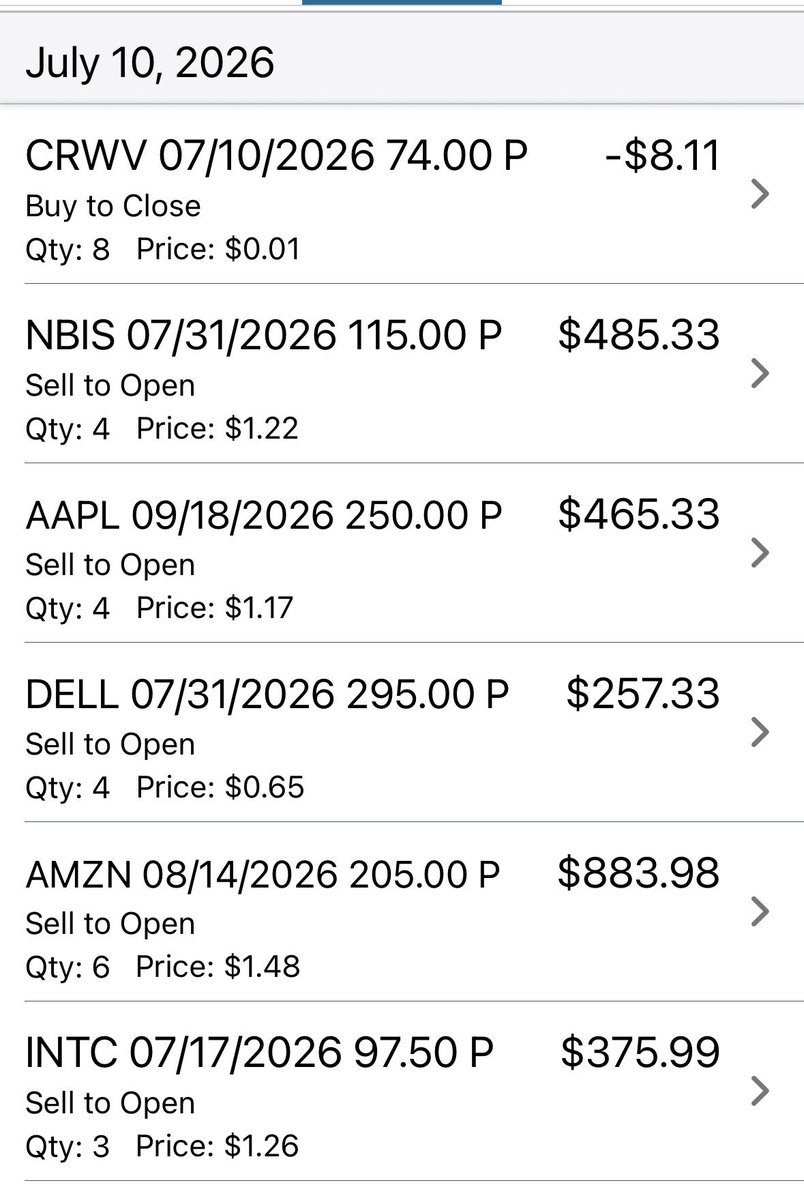

@Biking_Chef73@DevotedDividend Yes and yes. Look at my page, I post trades all the time. Start with selling cash secured puts. Start with selling 1 contract on one stock that you like. Thankfully we live in 2026, plenty of information available online. Educate yourself.

Didn’t realize the tax advantage with $SPYI.

JEPI/JEPQ:

The premiums generated by JPMorgan's ELNs are distributed and taxed as Ordinary Income. If you hold these in a taxable brokerage account, you pay your maximum income tax bracket rate on every distribution check.

SPYI:

SPYI uses Section 1256 contracts (SPX Index options), which are legally subject to a blended 60% long-term and 40% short-term capital gains tax rate, regardless of how long you hold the fund. Furthermore, NEOS uses tax-loss harvesting and accounting structures that categorize a massive portion of the distribution as Return of Capital (ROC). ROC lowers your cost basis rather than triggering immediate tax, allowing you to defer major tax burdens until you sell the shares.

I’m now familiar with the “wash” rule:

“A wash sale occurs when you sell a security at a loss and then purchase that same security or "substantially identical" securities within 30 days (before or after the sale date). if you end up being affected by the wash-sale rule, your loss will be disallowed and added to the cost basis of the securities you repurchased.”