منذ انطلاق Ghelaal غلال، عملنا على تطوير قاعدة بيانات لتقييم الأسعار المحلية، بهدف مساعدة كل من المشترين والبائعين على متابعة الأسواق داخل المملكة العربية السعودية (بالاضافة للأسواق العالمية).

وقد أدت التطورات الأخيرة في منطقة الشرق الأوسط إلى ارتفاع أسعار الذرة وكسبة الصويا والشعير، مع تسجيل زيادات اكبر في المنطقة الشرقية من المملكة. حيث اتجه عدد من المشتريين الى تأمين الإمدادات من المنطقة الغربية، مع تحمل تكاليف نقل داخلي أعلى بشكل كبير. في حين أصبح للعديد الحفاظ على استمرارية التشغيل أولوية تفوق اي اعتبار اخر.

خلال الأسابيع الأربعة الماضية، رصدنا التغيرات التالية في الأسعار الفورية:

المنطقة الشرقية (الخليج)

الذرة: +19.6%

الشعير: +8.3%

كسبة الصويا: 15.0%+

المنطقة الغربية (البحر الأحمر)

الذرة: +14.7%

الشعير: +3.6%

كسبة الصويا: +13.0%

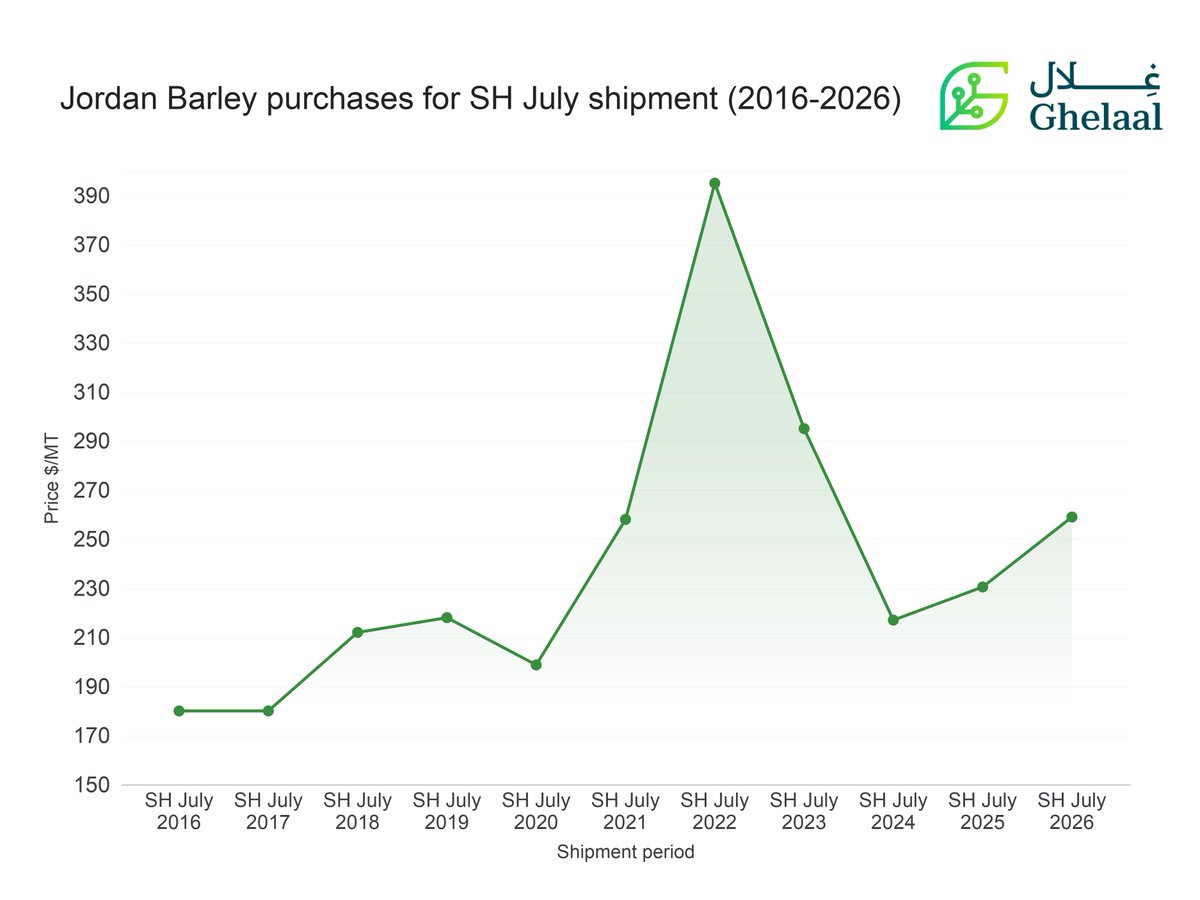

واصل الأردن وتيرة شراء الشعير، حيث تعاقد على 5 شحنات خلال الأسابيع الستة الماضية.

في مناقصة اليوم، قامت وزارة الصناعة والتجارة والتموين بتغطية شحن النصف الثاني من يوليو 2026 عند سعر 259 دولارا للطن، أي أقل بدولار واحد مقارنة بشراء الأسبوع الماضي لفترة النصف الاول من يوليو.

بالنسبة لشحنات النصف الثاني من يوليو ، يُعد هذا السعر ثالث أعلى مستوى تم تسجيله خلال الفترة من 2016 إلى 2026.

Week 15

Jordan MIT booked the following CNF Aqaba port

- 60k MT Wheat, FH Aug 25 shipment at $264 PMT (-$1 vs previous purchase)

- 60k MT Barley, SH July 25 shipment at $235 PMT (-$0.5 vs previous purchase)

This week, Jordan booked

- 50k MT Wheat SH Aug 25 shpt CNF Aqaba port at $265 PMT (-$0.25 vs previous purchase for FH Jun shpt)

- 60k MT Barley FH July 25 shpt CNF Aqaba port at $235.5 PMT (-$1 vs previous purchase for FH Aug shpt)

#OATT

USDA Barley update - March 2025

Imports: all kept same as Feb; except for Iran which was revised up by 400k MT (surprisingly KSA is still same at 2.6 MMT...)

Exports: a lot of changes here; Australia +1.2 MMT, Argentina -300k MT, Russia +400k MT, UK -50k MT and Turkey +200k MT

Production: Australia +1.565 MMT, both Ukraine and Argentina lower; -100k MT and -300k MT respectively.

#oatt

9 companies offered Barley at Jordan MIT tender today.

100k MT new crop Barley booked for FH/SH July 2025 shpt at $230.5 CNF Aqaba port.

The price is -$10.25 vs MIT’s last purchase for SH June shpt.

Jordan cancelled both Wheat and Barley tenders this week.

Since the beginning of the year MIT booked Wheat 4 times (230k MT) and cancelled twice. On Barley MIT booked once (100k MT) and cancelled 5 times.

Tendering again next week for Wheat and Barley on Tuesday 18th of Feb and Wednesday 19th of Feb respectively.

Conab this week increased Brazil's corn crop to 122mmt from 119.6mmt previously, but USDA reduced its outlook to 126mmt from 127mmt.

Note that the agencies are still 6.3mmt apart on last year's crop, so it is possible that one of the forecasts went the wrong direction this week.

Updated USDA Barley figures for 24/25 showed reduction in Morocco's imports by 100 MT rest unchanged; notably China and Saudi kept the same as Jan report where I think the latter should be revised up and probably the former down. On the export side, EU, Argentina and Ukraine reduced by 200k MT, 100k MT and 150k MT respectively, while Uruguay added 76k MT.

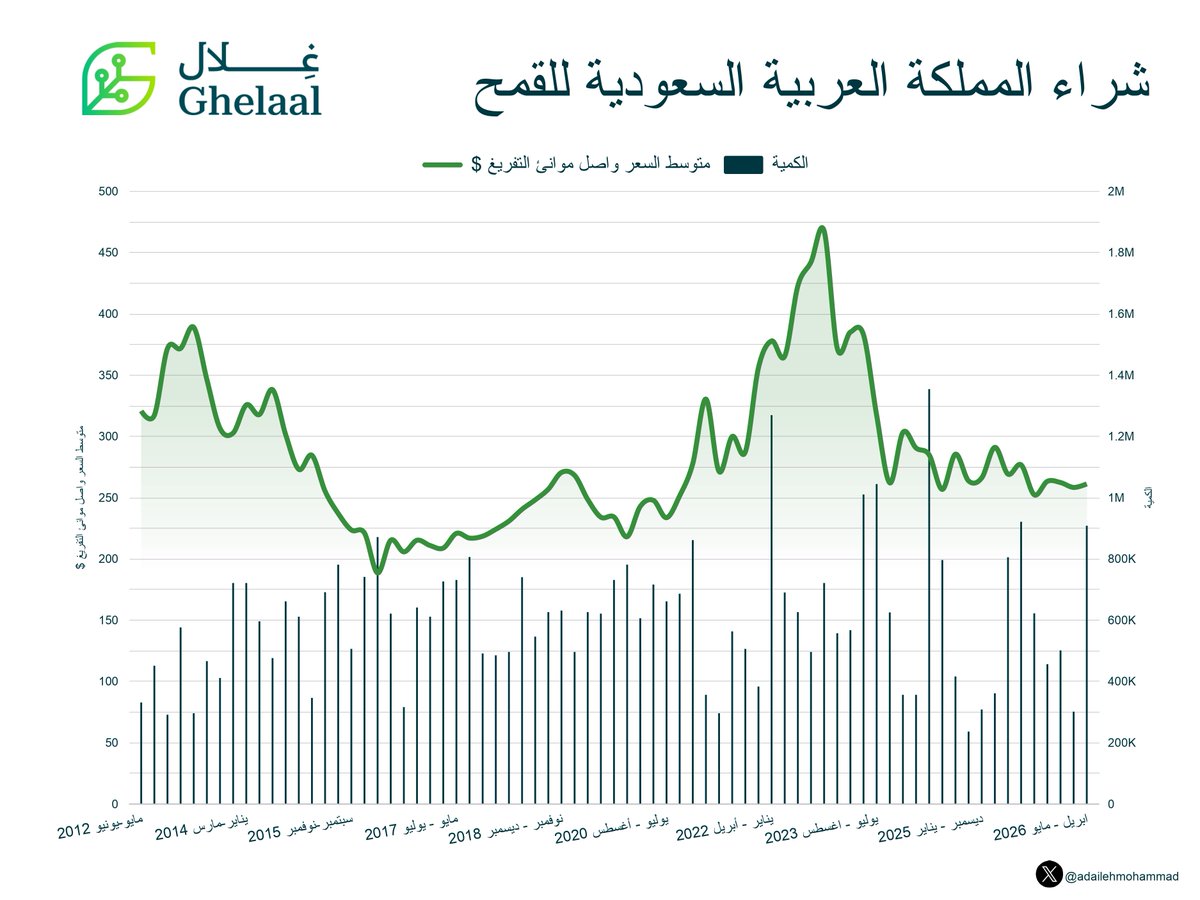

Saudi GFSA booked 804k MT of Wheat at average price of $268.87 for February - April 2025 delivery period

Vessels:

4 - Jeddah port

5 - Yanbu port

3 - Dammam port

1 - Jizan port