Pinned for anyone new here:

We’re a recruiting firm focused exclusively on financial planners and financial advisors.

We help:

- advisors explore new opportunities confidentially

- firms hire some of the best talent in the industry

If you’d like to join our talent network or discuss hiring needs, you can find everything here:

https://t.co/1Q5KJ1fptJ

It’s always interesting to see how many advisors on here build their marketing around attacking other fee models.

Lately, that seems to be a lot of flat fee and hourly advisors positioning themselves as the “affordable” alternative to AUM advisors.

The reality is more nuanced.

After many years in this industry and conversations with hundreds of advisors across the country, I’ve found that most of the highest quality advisors use an AUM model.

And interestingly, many of the top firms that offer both AUM and flat fee options actually charge more under their flat fee arrangement, not less.

Why?

Because good advice is expensive to deliver.

Financial planning is labor intensive. It requires expertise, experience, availability, judgment, and ongoing service.

Whether an advisor charges via AUM, a flat fee, or hourly billing, the economics of delivering great advice do not magically change.

The bigger question is not, “Which fee model is cheapest?”

It should be, “Am I getting value from the advisor I’m working with?”

At the end of the day, this is a relationship business.

There are exceptional advisors operating under every fee model, and there are mediocre advisors under every fee model.

The most important thing is not how your advisor gets paid.

It is finding someone you trust, building a sound plan, and sticking with it long enough for the plan to work.

I’ve seen this exact situation play out several times over the past month.

A next-gen advisor is working at a small or mid-sized firm. They know the senior partners are actively exploring an external sale.

They also know something else.

They’d rather be the one deciding where they work next than having that decision made for them.

When we talk, they usually think they have plenty of time.

“The search is still early.”

“I’m probably 3-6 months away from needing to make a decision.”

Then a week or two later, my phone rings again.

The senior partners finalized a deal.

The advisor now has a new employment agreement sitting in front of them and is being told they need to sign by the end of the week.

What felt like a strategic career decision suddenly becomes a fire drill.

One of the biggest misconceptions advisors have is that they should only reach out when they’re ready to make a move immediately.

In reality, it’s the opposite.

The best time to explore your options is long before you need them.

I’d much rather speak with an advisor a year before a potential transition than a week before a deadline.

Career decisions are stressful enough when you have time to evaluate your options, conduct due diligence, and make an informed choice.

When you’re operating under someone else’s timeline, your leverage and flexibility disappear quickly.

If you know your firm’s owners are exploring a sale and you’re not certain you want to be part of the acquiring firm, don’t wait for the announcement.

Interesting concept, but as always, execution is everything.

1000+ clients worth 7, 8, or 9 figures.

Every advisor has a finite capacity, including the ones capable of handling this level of clientele.

Those advisors are the ones already working with clients of a similar size/complexity. And their fees are already well below 1%.

This would realistically take, at a minimum, 25-50 advisors.

How many firms out there have 25-50 top tier advisors with the capacity to actually pull this off?

@markcecchini Agreed. Trying to force a highly personal, relationship-driven business into a cold transactional model is bound to end in some horror stories

If I were a young wealth advisor and wanted to better understand this industry, here's where I'd start:

I'd pull up my employment agreement.

Seriously.

Before you started at your current firm, you signed a document that outlines the rules of the road.

And I would bet the vast majority of advisors haven't looked at it since the day they signed it.

If you want to be intentional about your career, you need to understand the rules.

Who owns the client relationships?

What happens if you leave?

Are there non-solicit provisions?

Is there a non-acceptance clause?

The industry is full of opportunity.

But before you start thinking about where you might go next, you need understand exactly where you stand today.

About half the wealth advisors I talk to refuse to work as a W2 advisor.

Their reasoning is usually the same:

"I don't want someone else to have the ability to fire me."

The other half dismiss that concern almost entirely.

And honestly, I think there are valid arguments on both sides.

On one hand, this is one of the most relationship-driven businesses in the world.

Generally speaking, client loyalty resides with the advisor, not the firm.

Many advisors look at that reality and conclude they would rather own their clients, own their business, and control their own destiny.

On the other hand, there are plenty of advisors who are perfectly happy being employees.

They enjoy being part of a larger organization.

They value the support, infrastructure, brand, and resources that come with it.

And many build incredibly successful careers doing exactly that.

What makes this discussion interesting is the economics.

At many firms, inherited clients are paid at a lower payout rate than advisor-sourced clients.

In some cases, substantially lower.

Those inherited relationships are often highly valuable to the firm because they can continue generating revenue for decades regardless of who services them.

To be clear, I don't think many firms are actually doing this today....

...But it does create an interesting dynamic.

There are situations where a firm could economically benefit from having those same clients serviced by an advisor earning a much lower payout.

For some advisors, that possibility alone is enough to make client ownership a non-negotiable.

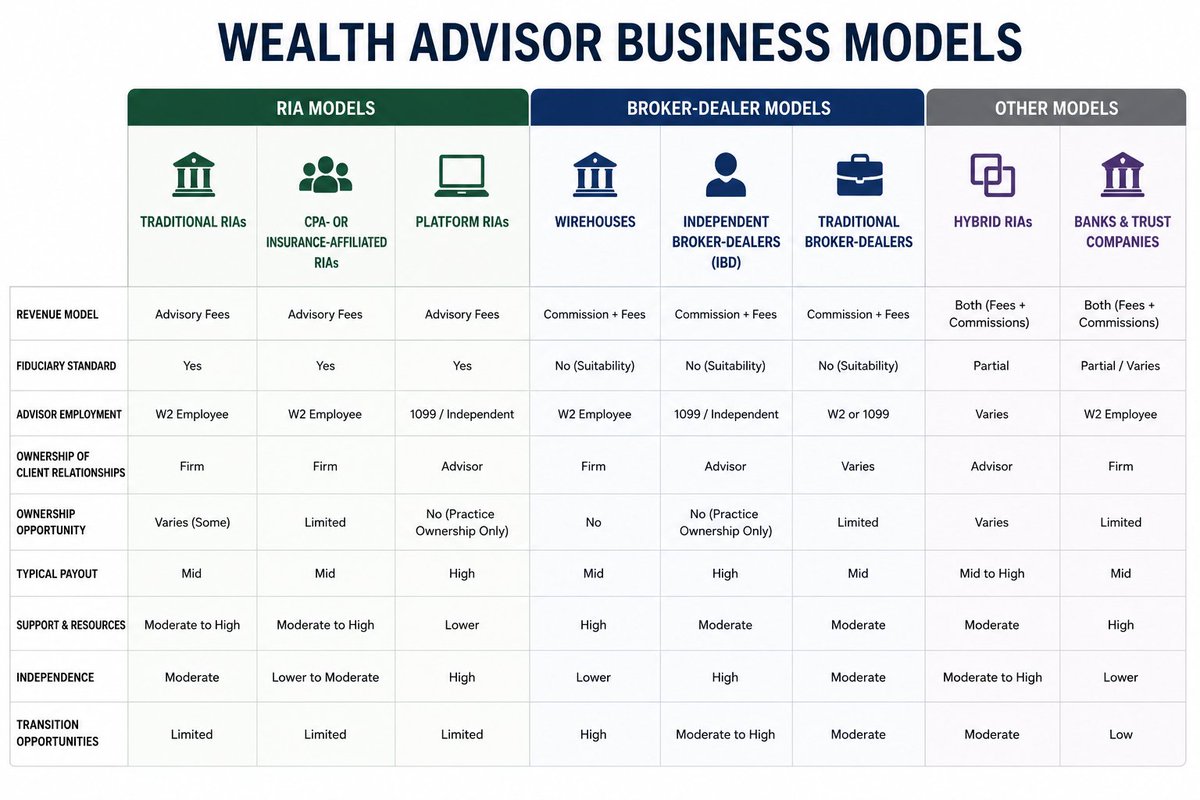

One of the most important career decisions a wealth advisor will ever make is choosing the right business model.

The challenge is that many advisors have only seen one or two models up close.

Before you can decide where you fit, you first need to understand what options actually exist.

At a very high level, most wealth management firms fall into one of two buckets:

RIAs and broker-dealers.

There are three main types of RIA models:

Traditional RIAs are what most people think of when they hear "RIA."

The firm charges advisory fees, operates under a fiduciary standard, and advisors are often W2 employees. Support, ownership opportunities, compensation structures, and service offerings can vary significantly from firm to firm.

CPA- or Insurance-Affiliated RIA firms often have a built-in referral engine through an accounting or insurance business. Advisors benefit from being integrated with other professionals, but usually operate within a more specialized ecosystem.

Platform RIAs firms provide the compliance, technology, and operational infrastructure while advisors build and own their practices on top of the platform. Typically higher payouts, greater independence, and less built-in support.

There are three main types of broker-dealer models:

Wirehouses are large national firms. Strong brands, substantial resources, and often significant transition packages. Advisors are typically employees operating within a more structured environment.

Independent Broker-Dealer (IBD) advisors generally own their client relationships and operate with a higher degree of independence while leveraging the broker-dealer's platform and infrastructure.

Traditional Broker-Dealers often fall somewhere between the wirehouse and independent models in terms of support, flexibility, and advisor autonomy.

Then there are a few models that don't fit perfectly into either bucket.

Hybrid RIAs combine an RIA with a broker-dealer relationship, allowing advisors to offer both fee-based and commission-based solutions.

Banks and Trust Companies typically provide a high level of institutional support and often generate referrals internally. Compensation structures tend to look very different from the independent side of the industry.

The reality is there is no universally "best" model.

The best model is the one that aligns with what you're trying to build.

Many advisors get their start in one business model and spend the rest of their career there by default.

The advisors who are most intentional about their careers tend to do the opposite.

They first get clear on what they want.

Then they find the business model that best supports it.

Understanding yourself is step one.

Understanding the right business model for you is step two.