As we reflect on 2025, we are thrilled to share the exceptional achievement of the Agatis Public Equity Portfolio. Through disciplined capital allocation, and a commitment to long-term value creation, 2025 stands out as a landmark year for our investments.

https://t.co/sDD0nwNRZR

As we reflect on 2025, we are thrilled to share the exceptional achievement of the Agatis Public Equity Portfolio. Through disciplined capital allocation, and a commitment to long-term value creation, 2025 stands out as a landmark year for our investments.

https://t.co/sDD0nwNRZR

🎉 We’re turning 3! 🎉

Today marks our 3rd anniversary, and we couldn’t have done it without YOU! Thank you to our amazing customers, dedicated team, and supportive community for being part of our journey. Here’s to more growth, innovation, and success ahead! 🚀

Three tables/charts that caught my attention in Michael Mauboussin’s @mjmauboussin latest piece, “Valuation Multiples What They Miss, Why They Differ, and the Link to Fundamentals”

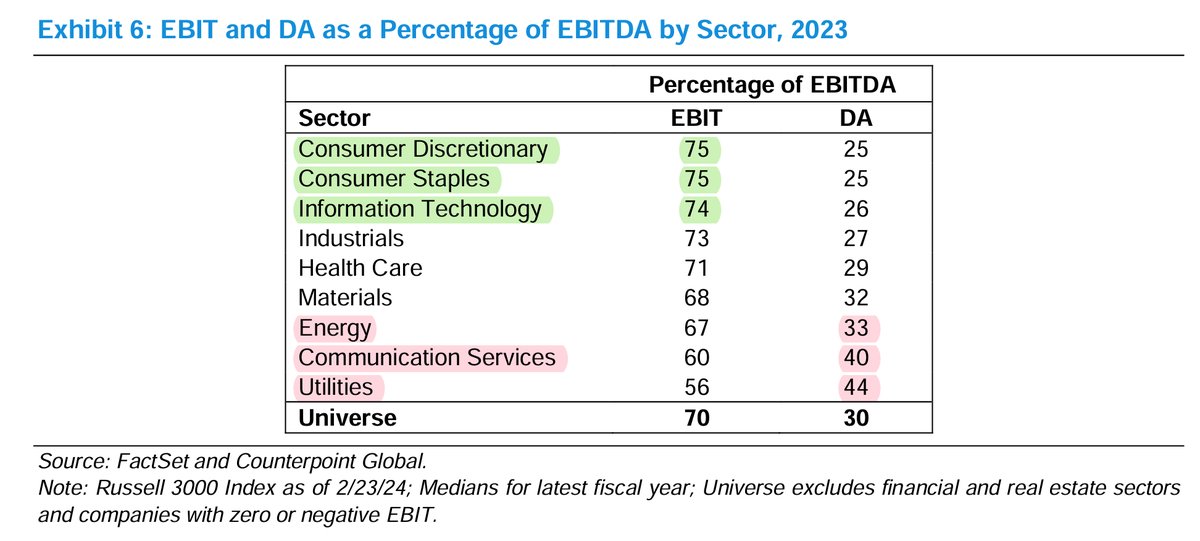

1 | For the same EBITDA, companies with lower DA, higher EBIT should have higher EV/EBITDA valuation multiples

Depreciation & amortisation (DA) is a proxy for maintenance CAPEX that a business requires to sustain its business.

For two firms with the same EBITDA, the one with a higher EBIT (lower DA) will more FCF and thus should have a higher EV/EBITDA multiple.

Notably certain sectors that we tend to prefer investing in also aligns broadly with this. Consumer discretionary, consumer staples and IT tend to have lower DA and higher EBIT, versus energy, communication services and utilities.

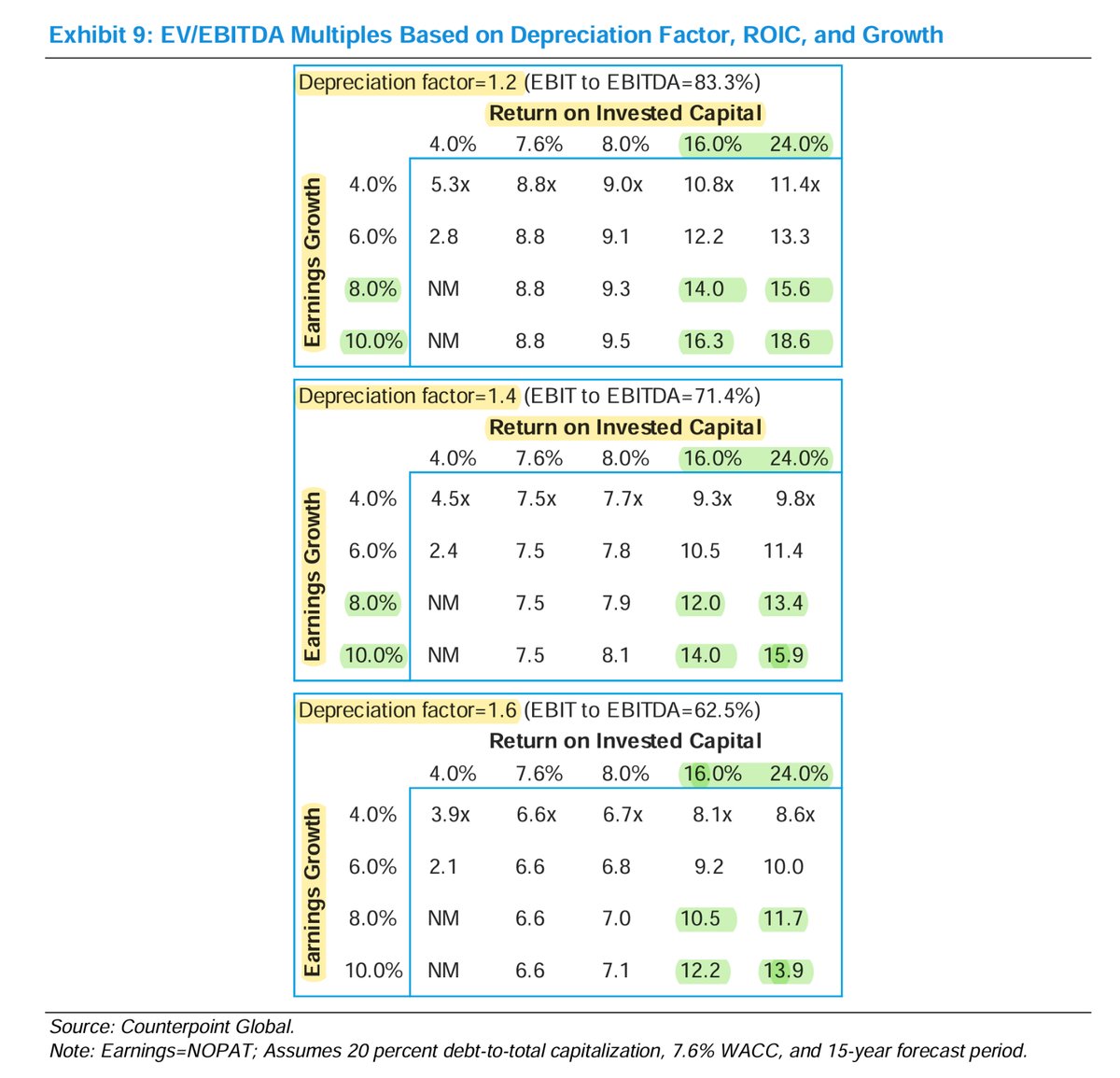

2 | Companies with lower DA, higher ROIC and higher earnings growth companies should have higher EV/EBITDA valuation multiples

Again not all valuation multiples are the same. They depend on the ROIC and the earnings growth, and also the depreciation factor.

The lower DA, the lower the depreciation factor, the higher the ROIC, the higher the earnings, the EV/EBITDA valuation multiples should be higher.

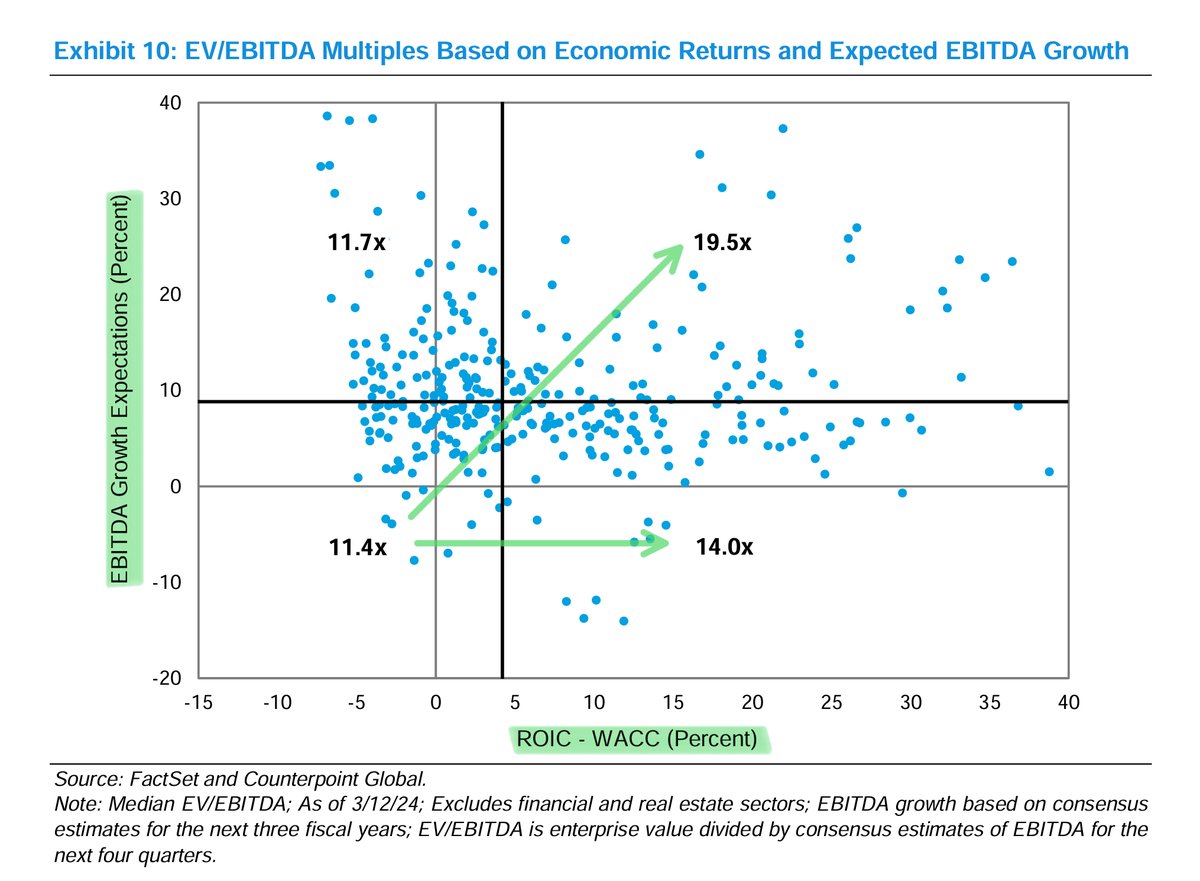

3 | Companies with higher ROIC and higher EBITDA growth expectations should have higher EV/EBITDA valuation multiples

It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price. A great investment opportunity occurs when a marvelous business encounters a one-time huge, but solvable problem.

- Warren Buffett

When the overall market is strong, the rising tide lifts most ships. But as Warren Buffett said, "you can't tell who's swimming naked till the tide goes out."