Nifty vs Gold (INR) (Update) 📊

Almost 3 months ago I said: don’t be bullish on gold, be bullish on stocks.

The ratio chart was sitting at a major bottom, which meant only one thing “equities were ready to start outperforming gold.”

And that’s exactly what happened. Look at the sharp rebound in the ratio chart. 📈

For new followers, let me keep it simple:

For the next 1–2 years, your stocks are likely to do much better than your gold.

Now lets send ratio to median line at 2.60

32 Mainboard Leaders & Their SME Counterparts - Hidden Opportunities You Can’t Ignore to study once 🔥🔥👇

Waaree Energies → Alpex Solar

KRN Heat Exchanger → Shree Refrigerations

Syrma SGS → Aimtron Electronics

Garden Reach Shipbuilders → Krishna Defence (Recently Migrated)

GE Vernova T&D → Viviana Power

Yatharth Hospital → Unihealth Hospitals

Cupid → Anondita Medicare

Polycab → JD Cables / Prime Cables

Shilchar Technologies → Danish Power

Bharat Forge → OBSC Perfection

Jeena Sikho → KRM Ayurveda

Amara Raja Energy → Maxvolt Energy

Interarch Building → Sathlokhar Synergys

ACME Solar → Oriana Power

Gravita India → Baheti Recycling / Namo eWaste

Aditya Infotech → Prizor Viztech

Netweb Technologies → Unified Data-Tech Solutions

Hitachi Energy → Quality Power

Container Corporation Of India → Afcom Holdings

Interglobe Aviation → FlySBS Aviation

Suzlon Energy → KP Green Engineering

KPI Green → Oriana Power / Ganesh Green Bharat

Clean Science → Neochem Bio

PG Electroplast → Osel Devices

ABB India → Advait Energy

KEI Industries → Systematic Industries

CG Power → Supreme Power

PVR Inox → Connplex Cinemas

KPIT Technologies → TechD Cybersecurity

Cochin Shipyard → ABS Marine

Ahluwalia Contracts → Goel Construction

Kalyan Jewellers → Utssav CZ Gold

The interesting thing about SME companies is that many of them operate in the same sectors where established mainboard leaders are already creating massive wealth.

Sometimes SMEs become suppliers.

Sometimes niche competitors.

And sometimes future industry leaders themselves.

The biggest wealth creation often happens before the broader market fully recognizes these businesses.

This is why studying SMEs deeply can become extremely important in the coming decade.

Let’s continue building this list further - feel free to add more interesting mainboard and SME counterpart below 👇

Disclaimer:

This is for educational purposes only and not investment advice. Please do your own research before investing.

Lithium imports have risen tenfold in 8 years.

₹3,532 cr in FY18 to ₹37,624 cr in just the first 11 months of FY26.

The April-February number is already 48% higher than full FY25 (₹25,458.6 cr).

And here is the part nobody is pricing in.

India barely imports "lithium."

What India actually imports is finished lithium-ion cells. The bulk comes from one country. China.

Every electric scooter, every grid storage tender, every BESS contract riding the energy transition story is, at the cell level, a payment to a Chinese supplier.

The government saw this in 2021 and threw over ₹54,000 cr at the problem.

₹18,100 cr ACC PLI scheme.

₹34,300 cr National Critical Mineral Mission.

₹1,500 cr Critical Mineral Recycling Incentive Scheme.

Four years in, here is the scoreboard.

🔹 Only Ola Electric has commissioned cells. About 1.5 GWh against its 20 GWh allocated target.

🔹 In Q3 FY26, Ola produced 72,418 cells. Cell segment revenue ₹9 crore. Cell segment EBITDA loss ₹39 crore. 🔹 Reliance New Energy and Rajesh Exports are yet to meaningfully operationalise.

🔹 EV penetration has already crossed 8.5% and the 2030 target is 30%. Demand has run far ahead of supply.

And the upstream story?

The 5.9 million tonne lithium reserve announced with great fanfare in Reasi, J&K in February 2023 has gone to auction twice. Both times scrapped. Zero qualified bidders. The Mines Ministry has ordered re-exploration before the next attempt.

So, the real question for FY27 to FY30 is not whether India will import less lithium.

It is which listed names will actually be standing when the domestic ecosystem finally lands at scale. Demand is locked in. The supply side is finally moving.

Three buckets worth tracking.

✍️ Cell and battery pack manufacturers

🔸Exide Industries. 6 GWh Bengaluru plant, SVOLT-licensed, commercial production targeted FY26-end.

🔸Amara Raja Energy & Mobility. 16 GWh Telangana gigafactory, ₹9,500 cr capex, NMC start by FY27-end.

🔸Waaree Energies. 20 GWh integrated lithium-ion cell and BESS facility approved, ₹8,175 cr Andhra Pradesh greenfield. Largest planned integrated player.

🔸JSW Energy. 10 GWh by 2026 scaling to 50 GWh by 2030, with downstream lithium refining plans.

🔸Reliance Industries. PLI awardee for 10 GWh, Jamnagar gigafactory ramping up.

🔸Ola Electric. The only one actually making cells today. Watch whether Bharat Cell economics improve.

✍️ Cathode, anode and electrolyte chemistry plays

🔸Himadri Speciality Chemical. India's first commercial anode plant commissioned April 2026 at Mahistikry. ₹1,125 cr LFP cathode project Phase 1 of 40,000 MTPA by Q3 FY27. Long-term vision 2,00,000 MTPA LFP, the largest non-China supplier globally.

🔸Graphite India. ₹4,330 cr committed for synthetic graphite anode materials.

🔸HEG (via TACC Limited). Large-scale anode plant in pipeline.

🔸Gujarat Fluorochemicals. LiPF6 electrolyte salt plant commissioned, ~$1 bn earmarked through GCFL EV Products.

🔸Neogen Chemicals. 30,000 MT electrolyte and 5,500 MT electrolyte salts plant in Gujarat, Mitsubishi Chemical tech partnership.

🔸Ami Organics. First company outside China to develop electrolyte salts for Li-ion and solid-state batteries. ₹300 cr Gujarat facility.

🔸Tata Chemicals. Cathode active materials, cells and recycling at Dholera with ISRO, CSIR-CECRI partnerships.

✍️ Battery recyclers and circular economy plays

India is expected to generate 128 GWh of end-of-life batteries by 2030. Recycling recovers 18 to 30 kg of lithium per tonne. Fresh ore yields just 2 to 7 kg. The economics favour recycling, and the ₹1,500 cr Critical Mineral Recycling Incentive Scheme is the policy tailwind.

🔸Gravita India. Listed lead recycler expanding into lithium-ion.

🔸Exide Industries. Greenfield battery recycling plant already commissioned.

🔸Amara Raja. Recycling arm operational, integrated with its cell strategy.

🔸Tata Chemicals. Commercial Li-ion recycling at Palghar since 2019, recovery purity claimed at 99%+. Scaling to 500 tonnes annually.

📌The next phase of India’s lithium story will not be judged by EV sales alone.

It will be judged by how much of the cell value chain shifts inside India.

Cells, cathodes, anodes, electrolytes and recycling are where the real battle sits.

The import bill is already warning us.

Demand has arrived before the ecosystem.

📌Disclaimer: For educational purposes only. Not a buy or sell recommendation.

Before posting, maybe first check who the biggest compressor manufacturers in the world are 😅

Do they have manufacturing unit in India or not ? Are they investing more in India ?

Tata and Reliance are big companies… but they don’t have to manufacture every single thing on the planet 🤪

Here are world 4 biggest compressor manufacturers in world

Nuclear is the loudest theme in Indian markets right now. The harder question is which of the listed names actually has the orders, and which are riding the headline.

The order books say something interesting.

🔹 KSB Ltd

Total order book: ₹2,585 cr (Dec 2025). Nuclear: ₹1,282 cr - 49.5%.

First Indian company in the pump industry to be accredited with ISO 19443:2018. Effective monopoly on primary coolant pumps for India's PHWR fleet. Confirmed on most reactors under construction.

Nuclear revenue in CY25 was under ₹50 cr because of testbed delays at Tarapur; management guides ₹300-400 cr in CY26.

🔹 MTAR Technologies

Total order book: ₹2,394.9 cr (Dec 2025). 3.5x annual revenue, the highest in company history.

₹504 cr of nuclear orders bagged for Kaiga 5 and 6 in December 2025 alone. Nuclear contributed only ₹16.6 cr to 9MFY26 revenue (3%). Means the order book has barely started flowing through.

Management guiding 50% revenue growth in FY27.

🔹 BHEL

Total order book: ₹2.4 lakh crore (Mar 2026). FY26 inflows: ₹75,000 cr. Lone domestic supplier of nuclear steam turbines in India. ~75% of PHWR units operate with BHEL turbine and generator sets. Won the ₹10,800 cr turbine island package for six 700 MWe PHWRs and ₹1,400 cr steam generator order under fleet mode procurement. Signed MoU with EDF in Nov 2023 for Jaitapur localisation (six EPRs of 1,650 MW each).

🔹 L&T Heavy Engineering

Has manufactured and dispatched 42+ steam generators across India's nuclear programme. Joint venture with NPCIL at Hazira is the only Indian facility capable of forgings up to 120 MT. Just dispatched the 7th 700 MWe steam generator to NPCIL. Management has guided for 3 to 3.5x nuclear revenue growth over the next 5 years.

🔹 Hindustan Construction Company (HCC)

Total order book: ₹13,148 cr (Dec 2025). Bid pipeline: ~₹53,820 cr.

HCC's own concall: built 65%+ of India's nuclear power plant capacity. Nuclear is only 3% of the current order book - the rest is transportation (63%), hydropower (22%), water (12%). Currently executing BARC reactor labs in Maharashtra and IGCAR Kalpakkam FRFCF. Just disclosed plans to enter LWR civil works.

🔹 Kirloskar Brothers (KBL)

Power segment order book: ₹495 cr (22% of standalone). Made the primary and secondary heat transport pumps for the Kalpakkam Fast Breeder Reactor. Each pump weighs 135 tonnes, handles liquid sodium at 500°C+. Per KBL, only 4 companies globally can manufacture these. Q3FY26 concall disclosure: 4 PHWR primary circuit pump types now developed in-house and qualified by NPCIL. Direct challenger to KSB on the next PHWR fleet order.

🔹 Walchandnagar Industries

Total order book: ₹670 cr, primarily nuclear. Quietly turned the corner in Q3 FY26: net profit of ₹4.66 cr (vs loss of ₹17.13 cr YoY), revenue ₹80.95 cr (+37% YoY), EBITDA margin 22%. Two consecutive quarters of positive EBITDA. Management called it "a turning point, not a peak". The full-year FY25 was still a ₹86 cr loss. Promoters have pledged 49.2% of holding — that's the live overhang.

The pattern that nobody is calling out:

The order books are split into 3 distinct groups, and they don't deserve the same multiple.

Group 1: Order book and revenue both compounding: MTAR, KSB, L&T, BHEL.

Group 2: Order book is strong, nuclear is a small slice of it: HCC.

Group 3: Order book exists, turn happening, balance sheet still recovering: Walchandnagar.

Group 4: Order book modest, but the technical moat is real: KBL.

The market is currently pricing all of them as one story.

They're not.

⚡️Disclaimer: The above data should not be considered as a buy or sell recommendation. The analysis has been done for educational and learning purposes only.

INDIA IS RAPIDLY EXPANDING ITS NUCLEAR ENERGY CAPACITY TO SECURE A CLEANER, RELIABLE, AND SELF-DEPENDENT FUTURE📊🔥

🔹Larsen & Toubro

👉 Nuclear reactors के heavy components और EPC contracts

🔹KSB Limited

👉 Nuclear-grade pumps & valves

🔹Walchandnagar Industries

👉 Reactor components manufacturing

🔹MTAR Technologies

👉 Nuclear & space components

🔹Bharat Heavy Electricals Limited

👉 Turbines, generators for nuclear plants

🔹Hindustan Construction Company

👉 Nuclear plant construction

🔹Kirloskar Brothers Limited

👉 Specialized pumps for nuclear plants

🔹NTPC Limited

👉 Future nuclear projects

🔹Power Corporation of India Limited

👉 Transmission support for nuclear power

🔹Thermax Limited

👉 Heat exchangers, boilers (indirect use)

🔹Data Patterns India

👉 Control systems (indirect high-tech supply chain)

🔹Power Mech Projects

👉 Turbine island & mechanical works

Dis - Not Buy/ Sell Reco

Thousands of crores worth of solar panels are installed across Rajasthan right now. Generating power. With NOWHERE to send it.

India's most expensive electricity isn't the kind that costs more. It's the kind that's already been made and has no road.

I went back and studied the entire transmission value chain. What I found changes how you should think about the power theme.

India just crossed 283 GW of non-fossil installed capacity. 274 GW of renewable + hydro. 8.78 GW of nuclear. Total generation capacity crossed 513 GW as of December 2025.

The numbers look great on paper. The problem is on the ground.

Rajasthan alone has 130 GW of grid connection applications. Transmission systems planned or under implementation? 73 GW. That leaves roughly 60 GW of renewable projects just sitting there waiting for a wire.

If one state has this gap, imagine the national picture.

India doesn't have a generation problem anymore. It has a delivery problem.

The government knows this. The National Electricity Plan lays it out clearly:

🔹 Transmission network: 5.04 lakh circuit km today → 6.48 lakh ckm by 2032

🔹 Transformation capacity: 1,429 GVA → 2,345 GVA

🔹 Inter-regional transfer capacity: 120 GW → 168 GW

🔹 Just for 2027-2032: 50,890 ckm of new lines + 433,575 MVA of new transformation capacity

This is not a projection from a broker report. This is formal government planning with budget allocation behind it.

And it's already showing up in execution. FY25 alone, 8,830 circuit km of transmission lines added and 86,433 MVA of transformation capacity commissioned.

Now here's what most investors get wrong. They treat "transmission" as one trade. It isn't. The value chain has very different economics at each layer, and the gap in return quality is massive.

Think of it as a 5-layer stack:

🔹 Layer 1: Lines and conductors

This is the volume layer. Towers, conductors, insulators, fittings. Demand is huge but margins are more commodity-linked. Raw material prices and bidding intensity drive outcomes more than capability moats.

🔹 Layer 2: EPC execution

Project ordering and pace of execution drive this layer. Strong revenue torque when cycle is up. But working capital is heavy, receivables can stretch, and right-of-way delays are constant.

🔹 Layer 3: Substations and electrical equipment

This is where it gets interesting. A transmission line mainly drives towers and wire. A substation drives transformers, reactors, GIS, switchgear, metering, protection, and controls, all at once. With 86,433 MVA added in FY25 and much more planned, this may be the richest layer in the cycle. Rising demand from data centres, metros, manufacturing, and commercial load centres makes this even more relevant.

🔹 Layer 4: Transformers and switchgear

These sit inside both the renewable pooling story and the urban grid strengthening story. Higher product complexity, longer approval cycles, stronger technical barriers. Better operating leverage if utilization tightens.

🔹 Layer 5: HVDC and advanced grid technology

This is the highest-moat layer. Standard AC handles most expansion. But long-distance renewable evacuation from Rajasthan, Gujarat, and Ladakh increasingly needs HVDC.

The Bhadla-Fatehpur corridor: ±800 kV, 6,000 MW, ~950 km. Hitachi Energy and BHEL are involved. Targeted by 2029. It's part of the backbone for India's 500 GW renewable ambition.

HVDC involves converter stations, converter transformers, thyristor valves, and complex integration. Qualified vendors globally are fewer than 10. Pricing power sits here.

👉This is the important part: not all beneficiaries in this chain will generate the same quality of earnings.

Volume players benefit from demand, but margins stay thin. Equipment makers with capacity constraints and qualification barriers are where operating leverage shows up. Technology players with HVDC and digital grid capability sit in the widest moat.

The grid is getting more complex, higher voltage, GIS adoption, digital substations, renewable pooling, HVDC corridors. Every step narrows the field of credible participants. That's the rerating trigger.

Risks are real. Execution delays, right-of-way issues, working capital stress in EPC, import dependence in advanced systems, and overbidding in commoditized packages. Study this in layers, not as one trade.

India's renewable story cannot scale without a much larger grid. The generation side gets the headlines. The transmission side determines whether any of it actually works.

In this cycle, the silent grid may capture more value than the louder generation story.

Listed companies by layer:

🔶Grid owners and developers

🔹Power Grid Corporation: India's central transmission utility, owns 90%+ of inter-state network

🔹Adani Energy Solutions: fastest-growing private transmission developer

🔶EPC contractors

🔹KEC International: RPG Group, present across T&D, railways, civil

🔹Kalpataru Projects International: strong T&D order book, international presence

🔹Bajel Projects: focused play on transmission towers and EPC

🔶Conductors, cables, line materials

🔹Apar Industries: Exports fibre optic and conductors to 50+ countries

🔹KEI Industries: power cables, scaling distribution presence

🔹Polycab India: wires, cables, and emerging FMEG play

🔹Dynamic Cables: smaller, focused on HT/LT cables and conductors

🔶 Transformers and substation equipment

🔹Hitachi Energy India: GIS, transformers, HVDC, grid automation

🔹CG Power: transformers, switchgear, motors, strong industrial base

🔹Transformers & Rectifiers India: direct play on transformer capex cycle

🔹Indo Tech Transformers: niche, high-voltage transformers

🔹Bharat Bijlee: transformers and motors

🔹BHEL: power equipment, HVDC involvement, diversified

🔹GE Vernova T&D India: ₹12,000 crore order inflows in one quarter on HVDC wins

🔶HVDC and grid technology (highest moat)

🔹Hitachi Energy India: only listed pure-play on HVDC in India

🔹GE Vernova T&D India: HVDC corridors, grid automation

🔹Siemens India: energy automation, digital substations

🔹ABB India: UPS, power distribution, data centre grid play

🔶Smart metering and grid digitisation

🔹Genus Power: smart meter specialist

🔹HPL Electric: metering and switchgear

Transmission is no longer a support sector. It is becoming the core enabler of India’s next power cycle.

⚡️ Disclaimer: The above data should not be considered a buy or sell recommendation. This analysis is shared only for educational and learning purposes.

India's ₹9 Trillion Power Transmission Play — The Full Value Chain Breakdown

India is building the world's most ambitious power grid.

₹9.15 Trillion to be invested in transmission infrastructure by 2032.

Every rupee flows through a value chain of ~20 listed companies.

Here's who wins at each layer 🧵

@niveyshak@caniravkaria@niraj_shah@VijayThk@Vismaya9999

Technicals for power transmission space are turning back...

The fundamental view point for the same:-

India's power sector is entering a multi-year expansion supercycle, shifting from an installed base of ~525 GW to over 800 GW. While the long-term narrative heavily favors renewables, near-term capital is flowing predominantly toward conventional thermal and transmission due to physical grid constraints and baseload realities

India ranks #3 globally in renewable additions (~45 GW added last year). The aggressive runway targets 50 GW/year over the next 5 years (~250 GW total). In contrast, conventional thermal power will add a steady 8-10 GW/year, led primarily by NTPC and Adani Power

The Unit Economics & Capex Math -

1) Solar: ~₹5 Cr/MW with a 1-2 year build time. India boasts a Levelized Cost of Energy (LCOE) of ~$30/MWh (₹2.5/unit), making it one of the cheapest globally due to high solar irradiance

2) Thermal (Coal): ~₹15 Cr/MW with a 5-year build time for greenfield projects

3) Nuclear: ~₹25 Cr/MW with a rigid 10-year build time. France serves as a historical parallel for India's nuclear ambitions, with long-term goals scaling from the current 8 GW to 100 GW by 2047

There is an under penetration in electrification currently, electricity comprises only ~18% of India's total energy mix, compared to ~30% in China and the low-20s globally. To achieve energy self-sufficiency amidst geopolitical volatility, power demand growth is projected to stabilize at a 1x multiplier to real GDP (~6% long-term growth)

Coming to a big tailwind of data centre capex, Current capacity sits at 1.5 GW, but is estimated to ramp up to 5-8 GW by 2030, driven by favorable grid access and clean energy mandates. This will incrementally consume ~2% of India’s overall electricity mix.

But what is the primary bottleneck with all this here? Transmission capacity… While India operates an efficient synchronous grid, a solar plant takes 1 year to build, whereas high-voltage transmission lines require ~3 years due to land acquisition and permitting. This lag will inevitably cap the realistic absorption of new solar capacity.

There might be a case where pure play renewable power generators might be in headwinds due to margin pressures and transmission bottlenecks which will make a investment case a little stronger for conventional power generators, power transmission value chain, new power infra such as nuclear energy and others and high quality/ top-tier EPC players.

Just quick note on few of the industry giants on this value chain -

1) NTPC - Operating as a highly defensive core holding. NTPC is leading the thermal capacity charge (17 GW under construction), spearheading future nuclear JVs, and incubating what will likely become India's largest renewable subsidiary

2) Power Grid - A direct beneficiary of the electrification and transmission theme, though near-term execution has been dragged by land acquisition hurdles. This one player drives compelete transmission value chain in the country

3) Larsen & Tubro - Largest EPC player present in multiple parts of the power value chain. The fundamental metrics are incredibly solid where ROEs are inching toward 17-19% with high-teens EPS visibility. However, the stock currently trades as a call on geopolitical stability, given that the Middle East accounts for a massive 37% of its order book.

4) PFC & REC - Their historical rerating was driven by the broad power theme, but loan book growth has fundamentally decelerated as Discom health improves and tier-1 banks chip away at market share. However, a potential merger between the two would be highly accretive—eliminating the ~50% holdco discount for PFC and forging a top-10 profitable Indian entity

5) Solar PV Manufacturers - Massive supply-side additions for solar cell manufacturing are coming online, which, coupled with transmission-capped demand, creates a high probability of margin compression over the next 12 months

6) IEX - Despite bottom-barrel valuations, structural and regulatory overhangs persist. Aside from the threat of market coupling, the exchange's transaction fees (~4 paise) are nearly 5x the global average (~1%), creating sustained headline risks

Disclaimer - not a recommendation to buy/sell

Custome index chart - https://t.co/90umyj9rtK (@stockscansin)

Know Your Fund #1: Parag Parikh Flexi Cap Fund

Key highlights:

1. 5 out of 6 risk ratios are better than the category; upside capture is the exception at 82% vs 105%.

2. 3Y rolling returns beat the benchmark 98% of the time; 5Y rolling returns do so 100% of the time: a sign of good consistency.

3. Active share is 71%: not a closet indexer.

4. 10.6% international exposure: a differentiator among flexi caps.

5. Max drawdown was −17.9% vs category average −20.5%: a shallower drawdown.

6. Expense ratio is 0.62% vs category 0.74%.

7. Downside capture is 37% vs category 97%: it absorbed only about a third of market falls.

Next on 'Know Your Fund' - HDFC Flexi Cap Fund.

For methodology and fund selection, check the link in the comments. 🔗

India Diabetes market is ~₹14,500–15,000 Cr

These are the key player who can be expected to win the GLP-1 race

Tier-1 Leaders- Novo, Lilly, Sanofi, Sun Pharma, USV

Tier-2 Large players- Torrent, Eris, Abbott, Biocon

Tier-3 Mid- tier playersLupin, Dr Reddy’s, Cipla

Emerging/niche- Zydus, Mankind, Glenmark, Natco

If you're eligible to create an HUF but haven't yet, you're leaving tax savings on the table. If you have trading, investing, or business income, an HUF gives you a separate PAN, separate tax slabs, and 80C limits, but very few actually make use of them.

We've supported HUF accounts at Zerodha for over a decade now, but the onboarding was quite cumbersome and required physical paperwork. It's now fully online.

25 #Monopoly Stocks in India for investment!📊

1. #CAMS (70% within the mutual fund industry)

2. Praj Industries (60% in ethanol plant installation industry)

3. ITC (77% in cigarettes)

4. #Borosil Renewables (India's only solar glass maker for over a decade)

5. APL Apollo (50% share in pre-galvanised and structural tube industry)

6. IRCTC (100% in the ticketing business)

7. Syngene (50% of the contract research and manufacturing services (CRAMS) market in India)

8. #Coal India (82% in coal production)

9. Nestle (96.5% share in cerelac industry)

10. NOCIL (largest rubber chemical manufacturing company with 40% market share in India)

11. HAL (100% in defense manufacturing)

12. Hindustan Zinc (78% in zinc industry)

13. MCX (92% of India’s commodities exchange sector)

14. Asahi India Glass (77% of the automotive glass market and 50% of the architectural glass market in India)

15. BHEL (67% in the power equipment sector)

16. IEX (95% of short-term electricity contracts in India)

17. BKT (6% of the global off-highway tire market and 30% of the Indian market)

18. Marico (73% in oil products)

19. CONCOR (68.52% in cargo carrier)

20. CDSL (59% in depository business)

21. DreamFolks (India's largest airport service aggregator)

22. Pidilite (70% share in adhesive)

Which stock are you holding? 📊

#stocks #investing

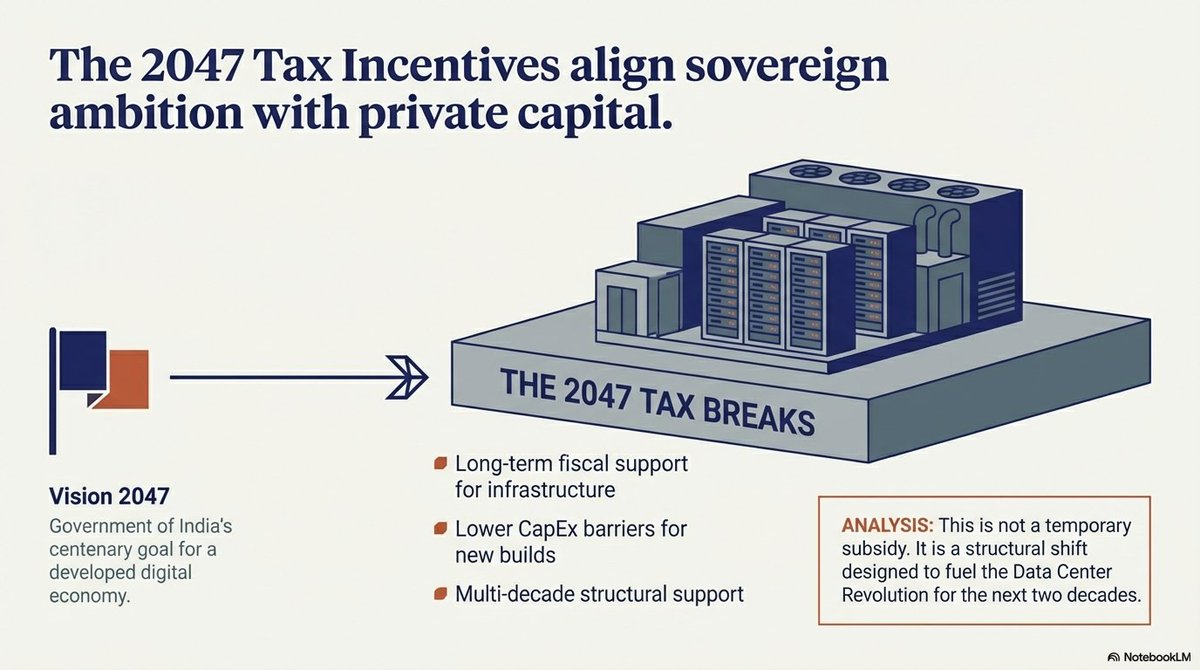

MEGA DATA CENTRE BREAKDOWN POST 🔥🔥🔥

2047 Tax Breaks & 15% Safe Harbour: India’s Data Centre Mega Opportunity 🔥🔥

Top 40 Data Center & Proxy Stocks Powering India’s Data Center Expansion 🔥👇

1⃣ Core Infrastructure & Connectivity

Anant Raj: Rapidly pivoting from real estate to a tech-giant by aiming for 300MW+ capacity, with major operational hubs already live in Manesar and Panchkula.

Netweb Technologies: India’s premier high-end computing player, designing the AI-ready servers and liquid-cooled racks that form the "brains" of modern data centres.

RailTel: Building a unique "Edge Data Centre" network at 100+ railway stations to bring high-speed processing closer to Tier-2 and Tier-3 cities.

Tata Communications: Owns one of the world’s largest subsea cable networks, providing the critical international "highways" for exporting data from Indian shores.

Bharti Airtel (Nxtra): Their DC arm, Nxtra, is investing heavily to hit a 1 GW capacity target, making them one of the largest co-location providers for global hyperscalers.

Black Box: A global leader in digital infrastructure integration, helping hyperscalers design and deploy complex internal networking and cabling for massive DC campuses.

Techno Electric: A strategic play that combines EPC expertise with data centre ownership, recently partnering with RailTel to develop green-energy-powered edge sites.

HFCL: Supplies the high-density fiber optic cables required to connect server racks within data centres and provide last-mile connectivity to the grid.

2⃣ Power, Electrical & Grid Infrastructure

Hitachi Energy: Provides the high-voltage grid automation and substations necessary to stabilize the massive, uninterrupted power loads required by AI-heavy data centres.

GE Vernova T&D: A specialist in extra-high voltage transformers and grid solutions that allow data centres to draw power efficiently from the national grid.

Cummins India: The gold standard for mission-critical backup power, supplying the massive diesel/gas generators that ensure DCs stay online during grid failures.

TD Power: Manufactures specialized AC generators used in captive power plants and backup systems specifically designed for the continuous load of a data centre.

Siemens India: Offers end-to-end Data Centre Infrastructure Management (DCIM) software and hardware for automated power distribution and fire safety.

CG Power: Recently secured major export orders for power transformers specifically designed for global data centre projects, showcasing their high-spec manufacturing.

Kirloskar Oil Engines: Provides robust high-capacity power-gen sets that serve as the last line of defense for data centre "Tier-4" uptime certifications.

3⃣ Cables, Wires & Electrical Components

Polycab: Dominates the supply of fire-retardant, low-smoke (FRLS) cables that are mission-critical for the safety and wiring of dense server environments.

KEI Industries: Focuses on extra-high voltage (EHV) cables required to bring power from the utility substation directly to the data centre campus.

Finolex Cables: Expanding its fiber-draw capacity to meet the dual demand for both electrical power and high-speed telecom cabling within DC facilities.

Apar Industries: Innovating with E-beam irradiated wires that handle higher temperatures (up to 105°C), allowing for more power in space-constrained server racks.

RR Kabel: Supplies specialized building wires and power cables with superior heat resistance, essential for the high-density power distribution units (PDUs) in DCs.

4⃣ Cooling, HVAC & Thermal Management

Blue Star: Developed a specialized range of centrifugal chillers that can restart in just 15 seconds, ensuring servers never overheat during power transitions.

Voltas: A major EPC player for large-scale HVAC projects, managing the complex air-flow and cooling designs required for massive server halls.

KRN Heat Exchanger: A key beneficiary of the AI shift, manufacturing the coils and heat exchangers essential for "liquid cooling" systems in high-density DCs.

Amber Enterprises: Expanding its R&D into commercial HVAC and precision cooling, targeting the high-margin market for maintaining exact DC temperatures.

Thermax: Provides sustainable water-cooling solutions and waste-heat recovery systems, helping data centres reduce their "Power Usage Effectiveness" (PUE) ratios.

5⃣ EMS, Electronics & Hardware Manufacturing

Syrma SGS: A leading electronics manufacturer providing the PCBAs and controllers used in power management and cooling systems for data centres.

Dixon Technologies: Moving aggressively into server manufacturing, aiming to become the local production partner for global hardware giants.

Kaynes Technology: Setting up high-tech plants for semiconductor OSAT and PCB assembly, critical for the local production of server-grade electronics.

Avalon Technologies: Provides specialized hardware for power and communications, including the complex sub-assemblies found in high-speed server switches.

6⃣ EPC, Infra Execution & System Integration

Bondada Engineering: Recently signed MoUs to develop "Green Data Centres", combining renewable energy expertise with rapid-deployment telecom infrastructure.

Orient Technologies: Acts as a specialized IT infrastructure integrator, helping banks and enterprises set up their private clouds within third-party data centres.

Larsen & Toubro (L&T): The heavyweight of DC construction, offering "turnkey" services from civil engineering to the installation of complex electrical and mechanical systems.

KEC International: Leveraging its global footprint to build the transmission lines and civil structures required to bring power to remote data centre parks.

NCC: Involved in the heavy civil construction of massive "Data Park" shells, providing the physical scale required for India's 40-DC push.

7⃣ IT Services & Cloud Enablement

Persistent Systems: Specializes in modernizing legacy applications so they can run efficiently on the new-age cloud infrastructure being built today.

Coforge: Focuses on cloud migration and AI-powered optimization, helping global clients move workloads into Indian data centres to benefit from Budget 2026 incentives.

Aurionpro Solutions: Offers a "single-window" DC solution, from design engineering to 24x7 operations, recently securing major contracts for bank data centre upgrades.

Allied Digital Services: A global player in Managed Services (MSP), handling the day-to-day IT infrastructure management and remote monitoring for DCs.

HCL Technologies: Their "CloudSmart" strategy helps global Fortune 500 firms architect their hybrid-cloud setups using India as a primary data processing hub.

Tech Mahindra: Integrating 5G and Edge Computing, they build the software platforms that allow industries to use DC capacity for real-time AI applications.

India’s data centre build-out is no longer just a tech story - it’s becoming a long-term infrastructure cycle backed by policy support, capital access, and structural digital demand.

The real opportunity lies in identifying which players across the value chain can execute consistently as this multi-year expansion unfolds.

✅ Study the ecosystem. Track execution. Let numbers guide conviction.

Disclaimer: This post is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. The stocks mentioned are shared for research and tracking purposes.