En economía conductual lo del Brexit es un caso fantástico. El 56% de los británicos dice que fue un error, los mismos británicos que 10 años antes decían que sí, que Europa les robaba.

Biotech growth is the nature progression of the looksmaxxing trend is a healthmaxxing trend.

In short, there is no reason to be wealthy if you cant live longer and look better. AI data crunching, and eventually quantum, will help accelerate proteonomics, geonomics and cell therapies to make fatal disease chronic illnesses and some types of neoplasia detectible before they ever become metastatic or, potentially, even malignant.

I spent time in Shenzhen last year and when I saw Merz come back from China saying Germans need to work more I immediately knew what broke his brain because I lived the exact same cognitive shock

my first week in Huaqiangbei I burned through 4 prototype iterations of a motor controller board for less than a thousand bucks total, back home a friend was working on something similar and spent over 12 thousand for a single revision that took almost two months to arrive

when you live that contrast in your own hands with your own project something permanently shifts in how you see the world and it goes way deeper than speed & cost

what Shenzhen actually built is a collective learning organism, imagine 20 PCB fabs 15 injection mold shops 30 component distributors and a hundred firmware freelancers all within a 2km radius, looks insanely redundant from the outside until you realize redundancy is actually information density in disguise

I watched this firsthand with an injection mold supplier I was working with, this guy had seen a hundred founders iterate similar thermal designs over 6 months so he proactively modified his tooling before I even opened my mouth, he knew what I needed before I knew what I needed, the intelligence lives in the relationships between the nodes and it compounds daily

the west thinks about manufacturing as a cost center you optimize by centralizing…

China accidentally built a distributed neural network of manufacturing intelligence where knowledge diffuses horizontally across thousands of agents faster than any single western company can process internally

so when Merz comes back and says we need to work a bit more I think he saw the problem but COMPLETELY misdiagnosed the solution, telling Germans to work harder is like telling a horse to gallop faster when the other side built a combustion engine

the gap is ARCHITECTURAL

it’s ecosystem density, you need a custom connector in Shenzhen you walk 200 meters, in Munich you send an email and wait 3 weeks

it’s iteration speed, parallel search vs sequential optimization at the system level, it’s risk tolerance, Chinese founders ship something broken on Monday fix it Tuesday ship again Wednesday while European companies are still in the approval phase for the pilot program of the feasibility study…

and Merz only saw the surface, what he missed is the tier 2 cities like Hefei Chengdu Wuhan replicating the Shenzhen model at scale right now

BYD going from irrelevant to outselling every european automaker combined in roughly 5 years, Huawei building its own 7nm chip under maximum sanctions when every analyst said it was physically impossible & behind all of that a government that treats advanced manufacturing as an existential national priority while europe debates whether AI needs another ethics committee

I think what we’re watching is the most asymmetric economic competition in modern history and most western leaders are still framing it as a productivity problem when it’s actually an ontological one

Europe & America are optimizing variables that China stopped tracking years ago meanwhile China is compounding on dimensions the west has no framework to even measure

Merz at least had the courage to name

it out loud and I respect that genuinely but working a bit more inside a broken architecture just means you arrive at the wrong destination slightly faster

We have a new report out today, "Bayes and Base Rates: How History Can Guide Our Assessment of the Future."

-We place projected sales growth rates of some artificial intelligence (AI) businesses in the context of history.

- We review literature on success rates for big projects (% on budget, on time, deliver expected benefits).

-We discuss Michael Porter's work on plans to expand capital expenditures.

Link in comment

the host city for the Super Bowl is San Francisco (Spanish for "Saint Francis"), which was originally a mission founded by Spanish explorers, the Mission San Francisco de Asís, in 1776.

It then became a city, originally named Yerba Buena (Spanish for "Good Herb").

the game will actually be played in Santa Clara (Spanish for "Saint Clare"), which is closer to San Jose (Spanish for "Saint Joseph") than San Francisco and also began as a mission founded by Spanish priests, the Mission Santa Clara de Asís.

To get there you go through San Mateo (Spanish for "Saint Matthew") and Palo Alto (Spanish for "tall stick", its named after a thousand year old redwood in the area, the El Palo Alto, a landmark used by Spanish explorer Gaspar de Portolá, who discovered San Francisco Bay).

the stadium runs parallel to a 13 mile stream named San Tomas Aquino (Spanish for Saint Thomas Aquinas).

all of this is in California, a name that originates from a 16th-century Spanish romance novel, "Las Sergas de Esplandián" (The Adventures of Esplandián) by Garci Rodríguez de Montalvo, published in 1510, about a mythical island paradise ruled by Queen Calafia. The Spanish explorers who mapped all this "applied the name to the Baja Peninsula, believing it to be the island described in the book."

point being, go fuck yourself Danica.

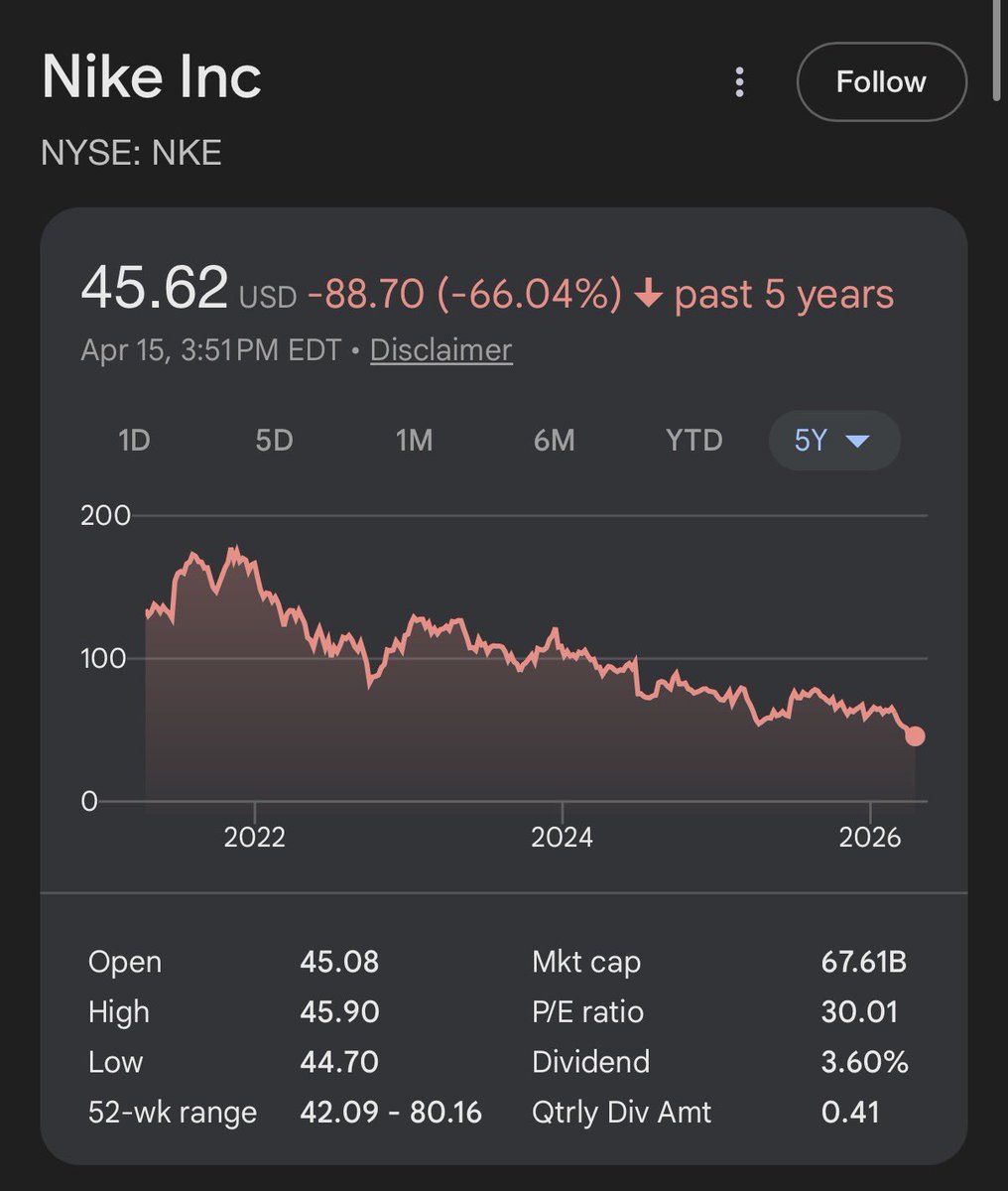

A few thoughts about PayPal, nearly 12 years after I left.

I woke up this morning to dozens of messages from former PayPal colleagues. It pushed me to finally speak up.

I never spoke publicly about the company after I left. Part of that was loyalty to John Donahoe, who gave me an unlikely opportunity, handing the reins of PayPal to a startup guy who, on paper, had no business running a then 15,000-person organization. But part of it was something else: I had left. I chose not to stay and fight for the changes I believed in. Speaking from the sidelines felt like armchair commentary. Easy opinions without the burden of execution. So I stayed quiet.

But twelve years of silence is long enough. And today's news makes it clear the pattern I've watched unfold isn't self-correcting.

I left PayPal in 2014 because I was deeply frustrated. We had executed a silent turnaround of a company that had lost its soul. We brought back engineering talent, shipped good products quickly, and acquired Braintree and Venmo. The company was on a tear. So much so that Carl Icahn felt compelled to accumulate a position in eBay and push for a PayPal spinoff. At the time, eBay decided to fight Icahn.

It was a difficult period for me, caught between what I felt was right for PayPal and my loyalty to the eBay team.

This is when Mark Zuckerberg approached me to join Facebook. The combination of his conviction that messaging would become foundational, the appeal of going back to building products at scale, and my growing exhaustion with the internal politics at PayPal and eBay eventually convinced me to leave and join one of the best teams in the world, one I had admired for a long time.

In the summer of 2014, I met John in a café in Portola Valley and told him I had decided to leave. During that conversation, he told me that Icahn had effectively won the fight, that PayPal was going to become an independent company, and he tried to convince me to stay on as CEO, but I had already said yes to Mark, and my word is my bond. There was no turning back.

After my departure, the board scrambled to find a replacement, and it took a few months for them to land on Dan Schulman. The leadership style shifted from product-led to financially-led. Over time, product conviction gave way to financial optimization.

Much of the momentum we had created still persisted and carried the company forward, mainly driven by Bill Ready, who came over in the Braintree acquisition and rose to COO. Under his leadership, Venmo grew exponentially, and total payment volume (TPV) accelerated quickly. But the shift under Schulman became more pronounced after Bill's departure at the end of 2019. With him went the product conviction that had defined the post-spinoff momentum. Then, for a period, COVID-fueled online shopping hid a lot of the company's new weaknesses.

During that period, the company made a fundamental miscalculation: it optimized for payment volume instead of margin and differentiation. It leaned into unbranded checkout, where PayPal had the least leverage, instead of branded checkout, where the margin, data, and customer relationship actually lived.

Visa masterfully structured a deal that effectively ended PayPal's ability to steer customers toward bank-funded transactions, which had been a core driver of PayPal's economics. Not long after, PayPal lost a significant portion of eBay's volume. Over time, it saw its share of checkout among its most profitable customers steadily erode as Apple Pay and others continued to execute well.

The same pattern repeated itself across lending, buy-now-pay-later (BNPL), and new rails.

On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else.

The missed opportunity in BNPL was even more striking. Klarna, Affirm, and Afterpay didn't just offer installment payments, they built consumer finance brands, persistent credit identities, and new shopping behaviors. PayPal saw the BNPL turn, entered the market, and had every advantage: distribution, trust, and merchant relationships. But BNPL was treated as a defensive checkout feature rather than an offensive category. There was no attempt to turn it into a core consumer relationship, no super-app behavior, and no meaningful differentiation for merchants. Others built platforms, PayPal added a feature.

The failure to lean into building and owning new rails followed the same logic. After the spinoff, PayPal had a once-in-a-generation opportunity to build a global, at scale payment network. Instead, the company focused on building on top of existing networks and third-party rails.

More recently, that mindset carried over to PYUSD. Technically, the product was sound. Strategically, it launched without a compelling transactional reason to exist. PYUSD had distribution, but no organic demand. It was not embedded deeply enough into flows to become a true settlement layer, a cross-border merchant rail, or a programmable money primitive. It sat adjacent to the product instead of inside the core of it.

Acquisitions during this period followed a similar pattern. Honey was not a strategic acquisition for PayPal. It added activity, but not leverage. It lived outside the transaction, monetized affiliate economics rather than payment economics, and never meaningfully strengthened PayPal's control of the customer or the checkout moment. Xoom solved a real problem in remittances, but it never compounded PayPal's advantage. It scaled volume without changing the underlying rails, identity graph, or settlement model, and as importantly, it didn’t cater to a high-value, high-margin customer archetype.

None of these were bad companies. They were just a wrong fit for PayPal and became unnecessary distractions.

The board eventually recognized the problem. In 2023, they brought in Alex Chriss, an Intuit veteran with a strong product background, explicitly to restore product conviction. It was the right instinct.

But Alex came from software, not payments. He understood SMB product development. He didn't have the muscle memory for transaction economics, network effects, or settlement infrastructure.

In hindsight, he also made an error: clearing out much of the leadership team that understood payments deeply. Executives with years of institutional knowledge departed within his first year.

This morning, Alex was removed as CEO. Branded checkout grew 1% last quarter. The board tapped another operator, Enrique Lores, the former HP CEO who's been on the PayPal board for five years.

I don’t know Enrique. And he might be a great leader, but on paper at least, he’s a hardware executive. For a payments company.

The common thread through all of this is incentive design. Once PayPal became independent, short/medium-term predictability beat long-term vision and ambition. Stock performance mattered more than platform risk and network opportunity. Financial optimization replaced product conviction.

I'm not claiming I would have made every call differently. Running a public company at scale involves tradeoffs I didn't have to make after I left. But the pattern, choosing predictability over platform risk, again and again, was a choice, not an inevitability.

Over time, the company that had every advantage and could’ve become the most consequential and relevant payments company of our time, lost its mojo, its product edge, and its ability to compete in a market that’s being rewired and reinvented in front of our eyes.

That's the part that's hardest to watch for a company I care so deeply about.

Well this sucks...

Senator Katie Britt just disclosed a purchase of JP Morgan $JPM while sitting on the Senate Banking committee

$JPM is up now up 27% since her purchase

But the worst part is you couldn't have even followed this.

Because she violated the STOCK Act by disclosing this trade hundreds days late

Her fine? $200

Less than the price of a speeding ticket in most states.