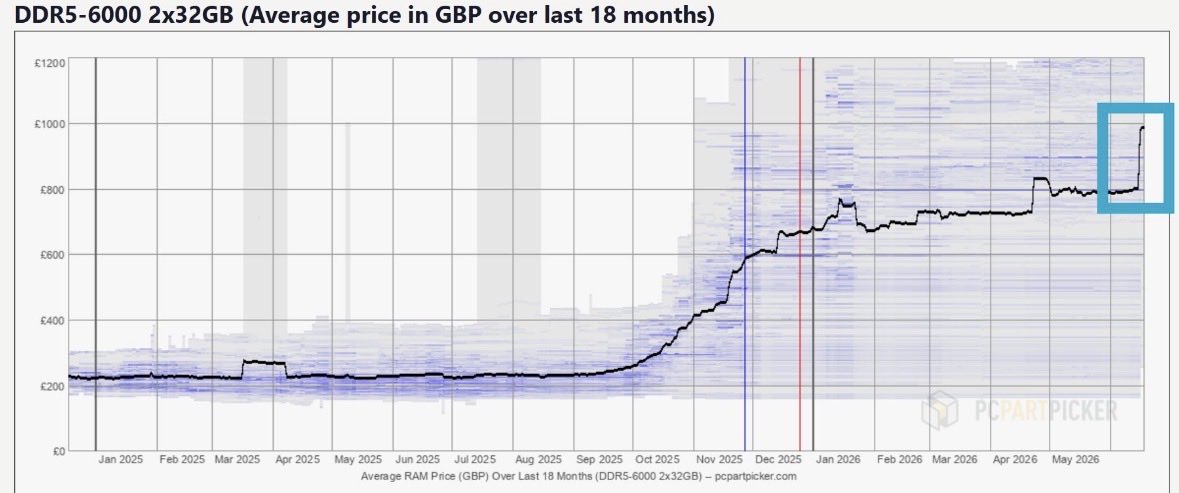

Wow! 64GB DDR5 prices have surged from £800 to £1,000 in just one week.

If elevated memory prices continues, new premium laptop prices are likely to rise, widening the gap with refurbished devices.

An interesting, under appreciated tailwind for GNG Electronics.

Kore Digital

Yesterday: Data Centre announcement.

Today: Proof of execution.

Management photos have already been migrated to the cloud from the PPT. Work on building ghost infra in full swing.

Wow! 64GB DDR5 prices have surged from £800 to £1,000 in just one week.

If elevated memory prices continues, new premium laptop prices are likely to rise, widening the gap with refurbished devices.

An interesting, under appreciated tailwind for GNG Electronics.

If Tritium executes, FY27 revenues could approach 2k Cr and FY28 3k Cr.

At 2-3x sales, Exicom could potentially be worth 6,000 - 9,000 Cr vs 2000 Cr today.

FY27 is the year to watch.

The market is skeptical. Management now has to prove it.

Can FY27 be Exicom Tele-Systems turnaround year?

At 2k Cr mcap, Exicom trades at 1x FY27 sales despite Q4 marking the first quarter of positive consolidated EBITDA.

The real upside lies in its subsidiary Tritium.

🌎 Management expects:

• 3x revenue growth in FY27

• EBITDA breakeven by Q4 FY27

FY28 could benefit from:

🔋 BESS

🖥️ AI data center power products

⚡ DC microgrids

🚗 Global fast charging

Execution is the key risk.

Classic dilemma!

Choice says BUY Yash Highvoltage with a target price of ₹1200.

Choice also says the target itself assumes 51x FY28 earnings.

So should I buy because of the target price or sell because even the target looks expensive? 🤔😂

Boy oh boy… IIFL just dropped a ₹10,000 TP on MTAR Technologies.

All the ‘overvalued MTAR’ experts need to take a long hike and rethink on those valuation lectures 😂