If early signs of interest rate stabilization hold, brokers widely believe that 2026 could mark the beginning of renewed momentum across key sectors—especially for buyers and sellers who have been stuck in a wait-and-see cycle throughout 2024 and 2025.

The 2026 broker forecast suggests that confidence is returning, though slowly. With most respondents expecting improvement and few anticipating deterioration, the mood across the market is one of guarded optimism.

A recent survey of San Antonio–area commercial real estate brokers reveals a market outlook that is generally positive, though tempered by caution, heading into 2026

5. The Mood: Cautious, Not Exuberant

The commentary reflects neither distressed sentiment nor runaway optimism. Instead, brokers appear measured and hopeful that 2026 will be a turning point, but aware that recovery hinges on broader economic shifts.

4. Industrial and Retail Remain Bright Spots

Comments highlighted continued strength in industrial and pockets of retail, especially service-oriented and necessity retail. These sectors were often referenced as stabilizing forces heading into 2026.

3. Mixed Signals in the Multifamily Sector

A few brokers expressed concern about continued softness in apartments, pointing to oversupply, high concessions, or pressure on valuations. This was the most frequently cited reason among those predicting a “same” or “worse” scenario.

2. Buyers Ready but Waiting

Several brokers mentioned active buyers who are currently paused due to pricing gaps, debt costs, or uncertainty. Many believe that once rates settle and sellers adjust expectations, deal activity will pick up.

1. Anticipation of Interest Rate Relief

Many brokers noted that even modest rate cuts, or simply stability after two volatile years, could unlock pent-up transactions. Improved financing conditions were one of the most commonly cited reasons for predicting a better year.

I am the program manager for the CRE Launch Program and I love seeing it all come together. We run our program during the summer, which can make scheduling speakers a challenge. That's why I have already started and have over half of our schedule confirmed!

Momentum is already building across the retail market, with investor activity beginning to accelerate. Those waiting for more favorable interest rates or certain economic outcomes may risk missing near-term opportunities as pricing and competition continue to intensify.

Cap rates for closed deals in San Antonio compressed, while Austin experienced a notable increase. Although total transaction volume for 2025 finished 8% below 2024 levels, nearly half of all transactions occurred during the 4th qtr, signaling renewed market activity.

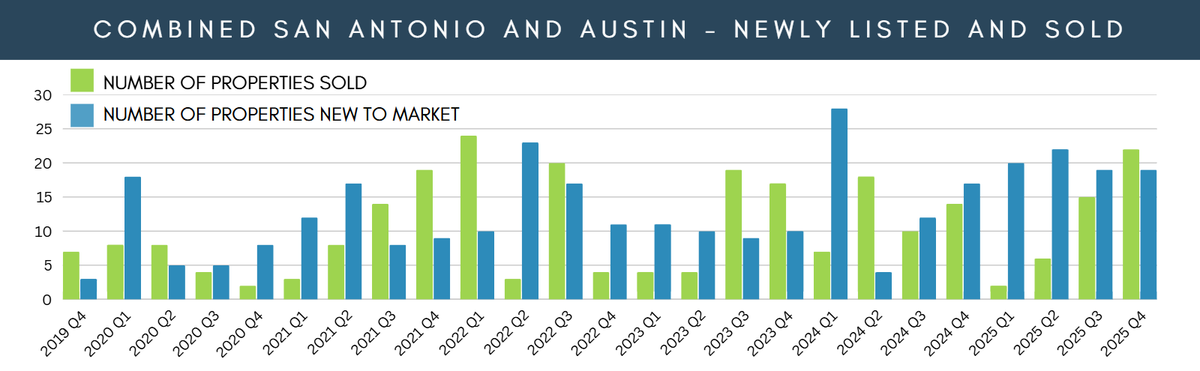

Look at the green bars during 2025 marking the number of properties sold each quarter. Sales increased every quarter. This momentum carried through the year, and the market is already hot entering 2026.

This chart tracks the new listings that come to market during the quarter. There were 19 new listings in Q4, priced about 35 basis points higher than the 19 that came to market in Q3.

At a glance, listing activity looks similar to last year, but with 10 fewer properties available, new listings and under-contract activity made up a much higher percentage of available inventory. Nearly half of all 2025 transactions occurred in Q4.

For all the strip centers publicly listed during the fourth quarter..

The average asking cap rate for Class A shopping centers in San Antonio was 6.47%. For Class B - 6.90%

The average asking cap rate for Class A shopping centers in Austin was 6.01%. For Class B - 6.42%

In 2024, many listings were removed at year end after sitting on the market for a long period of time with limited activity. That was not the case in 2025. There were many closings in Dec. Year-end activity reflected stronger demand and improved market momentum going into 2026.