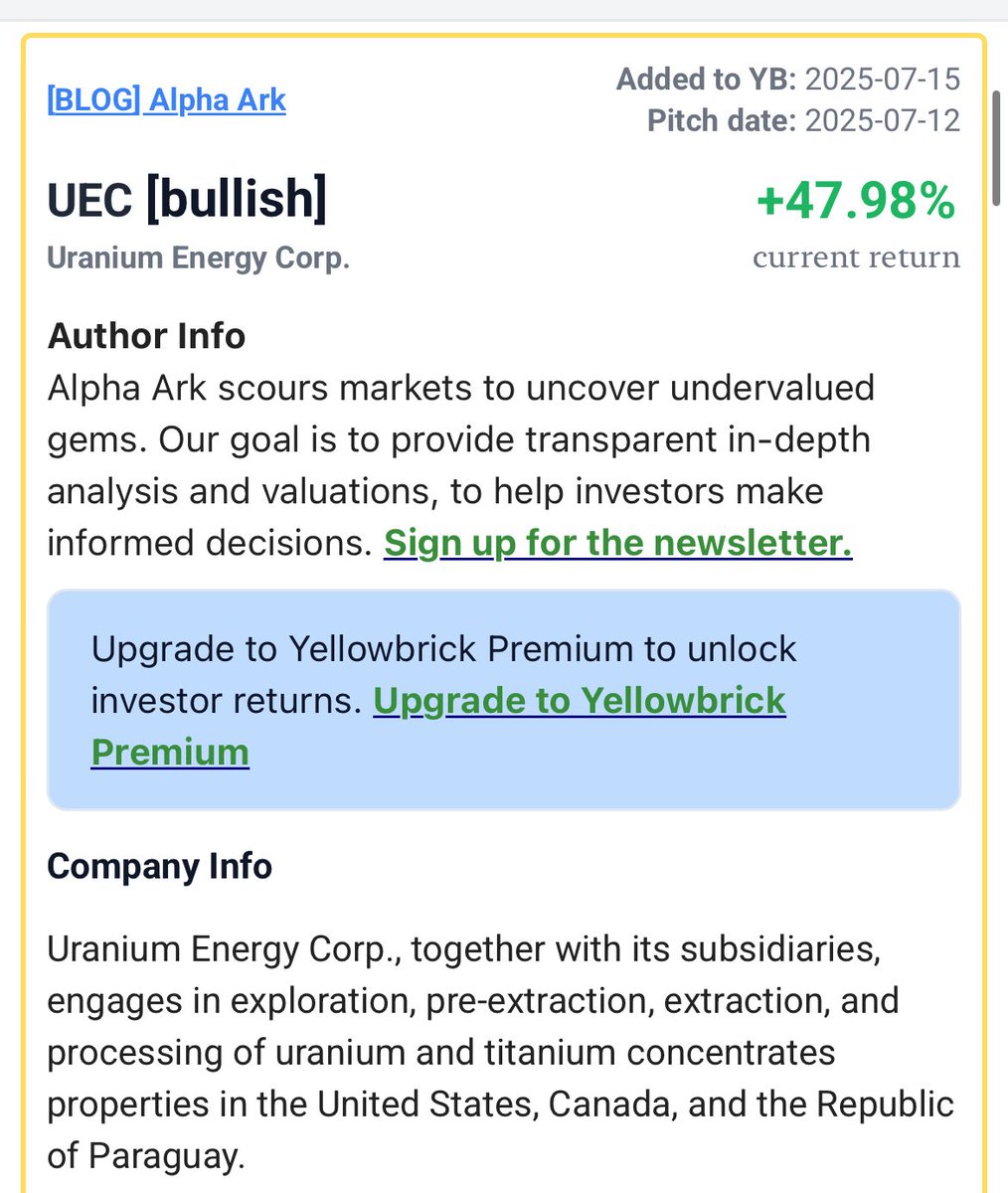

We just published our new free write-up on Uranium Energy Corp $UEC! It's a rapidly growing uranium miner poised to benefit from the massive and widening supply-demand gap in the uranium market. Here's why we like it:

- Persistent Supply-Demand Imbalance: ~15mmlbs of uranium supply gap, only projected to grow. This combined with now depleted inventories will put a lot of pressure on uranium prices.

- World-Class Asset: Holds one of the largest uranium portfolios globally, with over 230 mmbs M&I resources, supporting a projected 14-fold production increase by 2027.

- Undervaluation: Our NAV valuation of ~$13.65/share suggests a 118% upside potential at a projected $100/lb uranium price in three years (26% share price IRR). Even at current $80/lb uranium prices, UEC is undervalued with an estimated upside of 73%.

- Wide Moat: $UEC has captured one of the best assets in North America and is ramping up its stake in $ANLDF among other extremely well executed investments. These together with no debt and ~$250mm of fairly liquid assets (net cash and highly desired uranium inventories) provide a safety net.

- Key Catalysts Approaching: Rapid production ramp-up from Wyoming and Texas operations in within a year, and long-awaited resupply purchases from nuclear power producers.

- Strategic Positioning: Focus on U.S. and Canadian production aligns with Western energy independence goals, potentially benefiting from future government support and prolonged tariffs on Russian uranium.

For more details see our writeup!

Uranium Energy Corp (UEC) - Uranium Growth Story at a 54% Discount https://t.co/aJXUFBvdUr

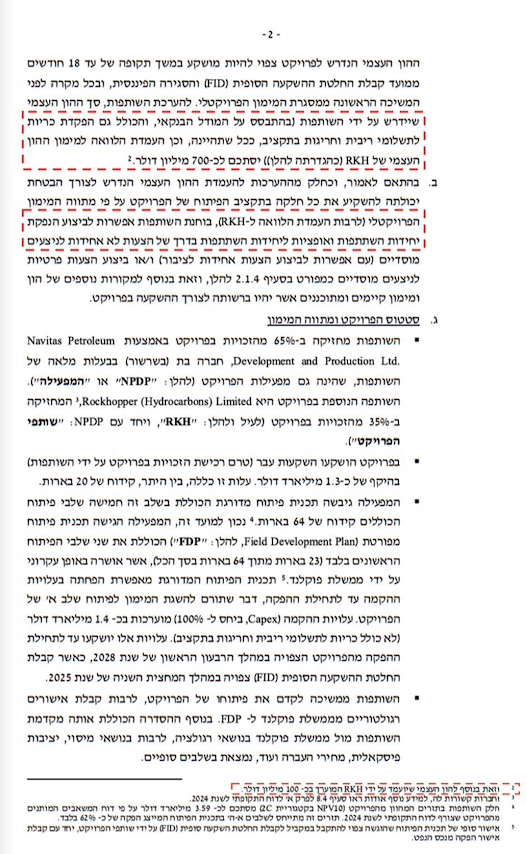

$RKH.L | Rockhopper benefits from $NVPT.TA capital raise (see attached post), as it reduces the project's financial risk, and shows another step towards FID in Sea-Lion.

Holding $RKH. Not advice or recommendation. For information Purposes only.

$RKH.L | $RKH | Rockhopper announces it has successfully received €31 million in insurance proceeds.

Rockhopper is preparing to file a new ICSID arbitration against Italy. The costs for this process are covered by a dedicated monetisation funder, ensuring no additional cash burn. The recovery will first repay insurers, with any remaining funds going to RKH and its funder (without impacting the company's cash position).

ANOTHER STEP TOWARDS FID IN SEA-LION

Holding. For information purposes only. Not a recommendation, advice, or call for action.

$ELAL flew 725,305 passengers during July 2025 (+10% compared to July 2024).

A massive increase in monthly passengers, which can indicate a high load factor during July 2025, might make up for the decrease in June 2025 caused by the war.

Holding $ELAL.TA. For information only.

And that's why just 3-6 months before that we will start rotating part of the capital from $VAL to $RIG. Their fleet is superior and they are the only large provider for harsh environments with little competition.

Eventually, we think a 50-50 offshore drilling capital split between $VAL and $RIG should be fair

I think if someone’s told $VAL and $RIG investors they will have 90% utilization in 2026 two years ago they would laugh and close him in a mental hospital

I think it is time to start looking at calls. Short-term price action is largely driven by analysts' earnings revisions for 3-6 months. Why not benefit from that

Holding not FA

$RIG Expects 90% util rate in late 2026/early 2027 – same as VAL. RIG prioritizing price discipline while others may accept softer terms in the current market

Constructive outlook for multiyear work including 3 Mozambique LNG projects progressing after delays due to geopol risk

$TDW stealing the show this AM w/ new repurchase program and + performance. $HYG RIG is more debt-friendly in 2025 as they pay down debt with their strong contract book. Goal is to be ~3.5x leverage in late 2026 which they believe will help enable shareholder returns but not there yet -- currently ~4.9x Net Leverage

Too much focus on RIG's sidelined fleet. Focus should be on warm fleet, specifically >75% of EBITDA is from their unique 7G+/8G drillships and Norway Harsh Environment semisub fleet which is why I like their credit. They expect Conqueror and Proteus to be re-contracted in late 2026 -- those are high spec rigs that IOC's will want

Expects to reduce onshore op expenses by $50mm by sometime in 2026

The slippage on projects to the right appears to be near an end although the market will want to see evidence

$BP Bumerangue discovery underscores the long-term case for deepwater, where reserve replacement will increasingly come from. However, it’s unlikely to impact the rig market near term—these projects have long lead times, and follow-up work is typically short in duration. Focus should remain on multi-year development drilling programs starting over the next ~18 months

Nothing on Shenandoah South FID -- something to follow in near-term regarding potential "contingent" work being picked up on 8G Altas but we'll see

נאוויטס לקראת אסיפה בה תעלה החלטה להנפקת מניות (עד 9 מיליון ערך נקוב). מדיניות התמחור שנבחרה ברוקהופר קבעה מחיר הנפקה לפי ממוצע 30 ימי מסחר קודמים. האם נוח שמחיר המניה יורד? יתכן שהמשא ומתן עם המוסדיים כבר התחיל. יש עניין. לא המלצה. דעה בלבד. $NVPT.TA. $RKH.L.