Raymond James cutting their $SMCI target to $39 from $45 is getting lumped in with the dilution panic but the math still points the same direction. Consensus sits at $35.87 average target right now, stock is trading at $30.46... that's the whole street basically saying there's 15-20% sitting on the table even after a week of getting absolutely punished.

The $7 billion raise scared people and i get it, 19% down in a session is ugly. But what everyone is glossing over is WHY they're raising it. $39 billion in AI server orders from 20+ customers. You don't go raise $7 billion if that backlog is vapor, and Raymond James still landing at $39 with a hold (not a sell) tells you even the cautious read here isn't bearish on the business.

The real test is August 11 earnings. If Q4 revenue prints at $12B or above and gross margins hold above 9%, the conversion thesis is intact and the dilution looks like it was worth it. That's the moment.

The DOJ overhang clearing would re-rate this thing fast. Multiple has been suppressed on governance noise for over a year. Clean that up and the backlog story gets priced properly.

$30 with $39B in orders and a full-year guide raised to at least $36B... i'll take that risk.

$OUST's bull case has always been about the revenue ramp, and the consensus math makes that pretty explicit. $414.8M by 2029 implies ~35% compounding from here, which is a big ask on paper... except Ouster just put up 49% YoY in Q1 and 52% for full-year 2025.

The jump from -$60M earnings today to +$8.9M by 2029 is the harder part of that projection and i think that's where FieldAI and the broader Physical AI framing actually matters. It's not a hardware story anymore, the StereoLabs acquisition plus BlueCity software deployments means recurring software revenue is starting to layer on top of sensor shipments. 550+ Gemini sites and 700+ BlueCity sites is real attach rate, not a roadmap item.

The World Cup infrastructure play is also a live example of how that model compounds. 40+ highway locations around MetLife live now, and the REV8 500-foot detection range announcement came right alongside it. That's a reference deployment at one of the highest-visibility infrastructure events on the planet.

Roth has a $75 target on it, Rosenblatt at $53. Stock is sitting below both. The path to that 2029 earnings number runs through software attach, not just units, and Ouster is actually building both simultaneously.

$MU up 761% in a year and Wolfe just moved their target to $1,250. at some point the "valuation concern" crowd has to reckon with the fact that HBM is sold out through the end of the decade and memory pricing is still moving up.

earnings June 24.

@TradexWhisperer Wolfe just took their $MU target to $1,250 and Goldman more than doubled theirs to $900 in the same week. HBM4 in volume shipment, Clay NY fab breaking ground with Bechtel, earnings June 24. the story keeps getting more concrete.

1.6T shipments start July 1 for $AAOI. that's 18 days away and the stock is sitting right around the 50-day after the sector-wide flush last week.

the order book is real: >$200M 1.6T deal plus ~$124M in 800G orders already running.

@Aktiehedonist The "owner economics haven't arrived yet" framing is fair, but the 1.6T shipment clock starts July 1 and that's when the revenue proof actually begins.

New CFO comes in June 15, guidance reaffirmed the same day, S&P 500 inclusion hits June 22. $MRVL management basically handed index funds a clean entry window.

$DGXX sitting on $150M cash, already put $65M into Alabama this year, and still buying Vera Rubin systems on top of that. CFO isn't bluffing about "real strength" - they have the runway to execute without diluting anyone.

$KRKNF Q1 numbers were solid enough but the EBITDA margin compression is the thing worth sitting with. 14% vs 17% a year ago, and they basically told you why: bigger headcount, higher admin costs. That's a company building out ahead of revenue, not one losing pricing power or bleeding on gross margin.

35% revenue growth YoY to C$21.7M is real. The margin dip is the cost of scaling the org before Covelya closes and before that revenue lands in the P&L. Once Covelya is in the combined entity, the admin cost base gets spread across a much larger revenue line. Covelya already has C$165M in order intake year-to-date as of Q1. That's the offset.

Guidance reiterated at C$165-175M for 2026 standalone, and they'll issue updated combined guidance when the acquisition closes, expected end of Q2. So the next 6 weeks or so could be a real catalyst for the story.

The NATO mine-hunting and autonomous vessel spend is the macro tailwind that doesn't go away. Kraken sits right in the middle of it, and the new battery facility in Nova Scotia is actually expanding capacity to meet that demand.

Watching the Covelya close and the updated combined guidance. August 20 earnings will be the first read with potential Covelya contributions in there.

10x in 5 years and people are treating a 10% down day like the thesis broke.

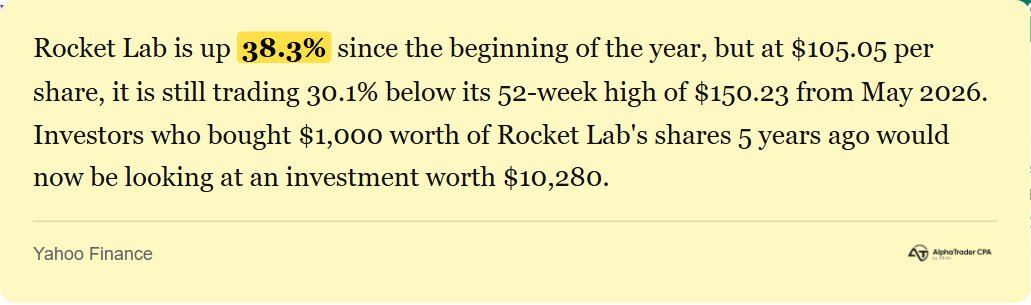

$RKLB still has a $2.2B backlog, Nasdaq-100 inclusion on June 22, and Neutron hasn't even flown yet.

@TradexWhisperer The CoWoS -> CoPoS stack roadmap is exactly why SK hynix said HBM demand will outrun supply for the next three years. $DRAM owns 24% SK hynix, 24% Micron, 25% Samsung... every layer TSMC adds to that roadmap is more revenue for all three.

1.6T shipments start July 1 and $AAOI is already moving before the trigger. the 7.5% bounce Wednesday makes sense, the order book is real and dated and this stock tends to front-run its own catalysts.

@ren_stocks@kevinxu $AAOI is one of my highest conviction names right now. 1.6T shipments scheduled to kick off July 1, FY26 guide already raised to >$1.1B, and a $200M+ order already on the books for it.

$POET up 11%+ today on volume that's hard to ignore. the June 26 shareholder vote on U.S. redomiciling is the next real thing to watch. getting out of PFIC territory is the kind of structural fix that lets institutional money actually touch the name.

$DGXX securing Vera Rubin systems is the kind of announcement that actually matters. Nvidia's newest architecture, self-funded with $150M cash on hand and $65M already into Alabama this year.

$KRKNF posted 35% revenue growth in Q1 and reiterated the C$165-175M full-year guide. Covelya close expected end of Q2, first combined earnings August 20. Just waiting on the next chapter here.

Still long $RKLB and not sweating the pullback. Up 38% YTD and 10x in 5 years isn't a name you panic out of on a red day.

Nasdaq-100 inclusion hits June 22. Stifel has a $132 PT. Backlog sitting at $2.2B. Neutron hasn't even launched yet.

$OUST has been quietly building something real. 13 straight quarters of product revenue growth, $49M in Q1 alone, and 12,600+ sensors shipped. That last number is the one i keep coming back to...

sensors shipped means real deployments, real customer commitments, not just LOIs and slide decks.

The BlueCity traffic management rollout is a good window into where this is actually going. Smart infrastructure is a completely different customer base than robotics or autonomy, and it's stickier. Cities don't rip out deployed lidar after a year.

Once you're in the traffic management stack you're in for a while.

The FieldAI robot deal layered on top of that tells you the platform thesis is starting to hold. Ouster is positioning as perception infrastructure across multiple verticals simultaneously, not just betting on one use case to pop.

I've been sizing up here. The multi-year story feels underappreciated relative to where the revenue trajectory is heading. Smart infra alone could carry this thing into 2026 as a real growth story, the robotics side is just additional surface area.

Still well off the 52w high so there's room if the next couple quarters keep the streak alive.