Crypto tax is not a niche anymore. It's a real and growing part of how a lot of people are building wealth, and the IRS is paying attention whether your CPA is or not.

Every wallet transaction, every staking reward, every token swap, every NFT sale is a potentially taxable event. Staking income is taxable the moment you receive it, not when you cash out. Token swaps are treated as disposals, meaning capital gains apply even if you never touched a dollar. And if your CPA's first question is "what's a wallet," that's a problem.

The crypto space moves fast. The tax implications move with it. You need someone who understands both.

If your portfolio has grown and your tax strategy hasn't kept up, let's talk.

This one stuck with us.

A lot of businesses are asking whether they should be using AI. The better question is what they're actually trying to solve, and whether AI is the right tool to solve it. The technology is only as useful as the thinking behind it.

Still on Small Business Month, and still on the stats that don't get talked about enough.

Nearly half of all small businesses close before they reach year five. By year ten, about two thirds are gone.

The difference between the ones that make it and the ones that don't usually isn't the idea. It's the infrastructure behind it. Financial visibility, clean books, someone who can tell you where you actually stand before the problem shows up on your bank statement.

That's the work we do every day.

May is Small Business Month, so we're spending it talking about the stuff that actually matters.

According to the U.S. Bureau of Labor Statistics, only about 35% of businesses born in 2013 were still operating a decade later. And 82% of the ones that close do so because of cash flow problems, not a bad product, not a bad team, not bad timing.

Most business owners know something feels off before they can name it. The numbers get fuzzy, the margins don't add up, the runway shrinks. That's usually not a strategy problem. It's a visibility problem.

Having the right financial partner in your corner changes that. You can't fix what you can't see.

Today we're taking a moment to celebrate the moms in the Alpine Mar family. The ones who show up every day, give everything they have at work, and somehow still have more to give when they get home.

We see you. We appreciate you. Happy Mother's Day.

We learn your systems, your data flow, and your operations, so nothing gets lost between your accounting team and your tax team. That’s just how we work.

The accounting industry is in the middle of a real shift, and we're not sitting on the sidelines.

77% of accounting firms are planning to increase their AI investment, and 35% are already using AI tools daily. The firms that move intentionally are the ones that come out ahead, and that's exactly how we're approaching it.

Here's what that looks like at Alpine Mar right now:

We've started deploying AI agents directly into QuickBooks Online. What that means practically: faster month-end closes, more timely posting to ledgers, and cleaner data that's as close to real-time as possible. That last part matters more than it used to, because savvy business owners are pulling directly from their general ledger to build their own dashboards. The data has to be current for that to actually be useful.

We're also using AI for analytics and reporting, which means we can deliver sharper insights to more clients, not just more spreadsheets.

Our tax team is in early days with workpaper prep agents, building trust with the tools before leaning in fully. That's the right way to do it.

More efficient operations. More value delivered. Same team you already know.

Tax season is officially a wrap.

The IRS expected around 164 million individual returns filed this season, and the average refund came in at $3,571, up more than 10% from last year.

For our team, busy season is the reason we do what we do. Every return, every extension, every question answered is a client who didn't have to figure it out alone.

Now that the dust has settled, we're catching our breath and getting ready to be just as useful for whatever comes next.

(The IRS hasn't published final filing totals yet since the deadline just passed. We'll be back with the real number once they do.)

Got questions about what this season meant for your business? We're here.

Private equity is reshaping accounting and fast.

Firms are getting bigger, combining forces, and building out “everything under one roof” models.

The upside is real: more firepower and broader services.

The tradeoff can be too. More complexity, higher fees, and a little more distance from your actual team.

That’s exactly why we built Alpine Mar differently.

Big firm capability. Small team attention. No tradeoff required.

A lot of people assume inheritance tax isn’t something to worry about.

At the federal level, that’s true. But at the state level, it’s a different story.

Five states still impose inheritance taxes and depending on who inherits what, rates can go as high as 16%. The catch? It’s not paid by the estate. It’s paid by the person receiving the assets. Which means without planning, beneficiaries can end up with unexpected tax bills or worse, forced to sell assets to cover them.

There are ways to plan around this. Lifetime gifting, trusts, and even properly structured life insurance can make a significant difference.

We broke it all down in our latest blog post https://t.co/HxWpqakF1d

Big financial moments move fast. A sale closes, a windfall lands, and suddenly you're making decisions that will shape your taxes, your estate, and your future whether you're ready or not.

At Alpine Mar we work with clients to make sure the right people are at the table before those decisions get made. Your CPA, your investment broker, your estate attorney — they all need to be in sync, and someone has to make sure that's actually happening.

That's the work. And if you've had a life event and don't know where to start, reach out. We can help you figure out who you need and what comes next.

If you’re on a board or managing an association, this is one of those things you really don’t want to guess on.

In Florida, financial reporting requirements depend on your annual revenue:

$150K–$300K → Compilation

$300K–$500K → Review

$500K+ → Audit

These reports are required every year and must be prepared by an independent CPA, typically within 90 days of your fiscal year-end.

There are cases where members can vote to waive or reduce the level of reporting, but that depends on your governing documents and specific rules.

Basically, it’s not one-size-fits-all, and it’s easy to get wrong.

Good news: we handle HOA and condo audits now.

April Fools.

Too soon? Probably.

If you missed the saga: BOI reporting was a federal requirement that had small business owners scrambling… then paused… then back on… then off again.

As of 2025, U.S. businesses are no longer required to file BOI reports after FinCEN rolled it back for domestic companies.

So no, it’s not back.

But if it ever is, we’ll be the first to tell you. Calmly.

This Women's History Month, we're spotlighting someone who's been quietly doing extraordinary things in an industry that wasn't built for her.

Veronica Querales is the President, CEO, and Co-Founder of Kohtler Elevator Industries, a Miami-based manufacturer that exports elevator products across the U.S., Caribbean, and Virgin Islands. She got her start in the elevator industry in high school, working for her family's business. Decades later, she built her own company in a country that wasn't hers, in an industry dominated by men, driven by a promise she made to herself and the memory of her father.

The growth has been real. Kohtler sold out of production capacity three months before the end of 2025. They're now moving into a larger facility, investing in new heavy machinery, and expanding aggressively.

That kind of growth is exciting. It also demands serious financial discipline.

Alpine Mar has been working alongside Veronica and the Kohtler team improving accounting processes, handling taxes, and providing Fractional CFO support to help leadership stay close to their cash flow as they scale. When you're making big investments in space and equipment, knowing exactly where you stand financially isn't optional.

#WomensMonth #WomensHistoryMonth

Meet Ashley, a Tax Director at Alpine Mar!

Ashley brings over a decade of experience to the team, with a career that started at Cherry Bekaert in 2014 and grew into a deep specialization in some of the more complex areas of tax. Her expertise spans real estate investment and pass-through entities, closely-held businesses, high-net-worth individuals, and US compliance for outbound international investments.

She holds a BS in Accounting from the University of Florida and an MS in Accounting with a specialization in Taxation from Florida International University. Safe to say, tax is kind of her thing.

Outside of work, Ashley is a true Florida Gator through and through. During her time at UF, she made it to every single home football game and stayed until the final whistle. Every. Single. One. 🐊🏈

We're thrilled to have her help leading the tax practice at Alpine Mar.

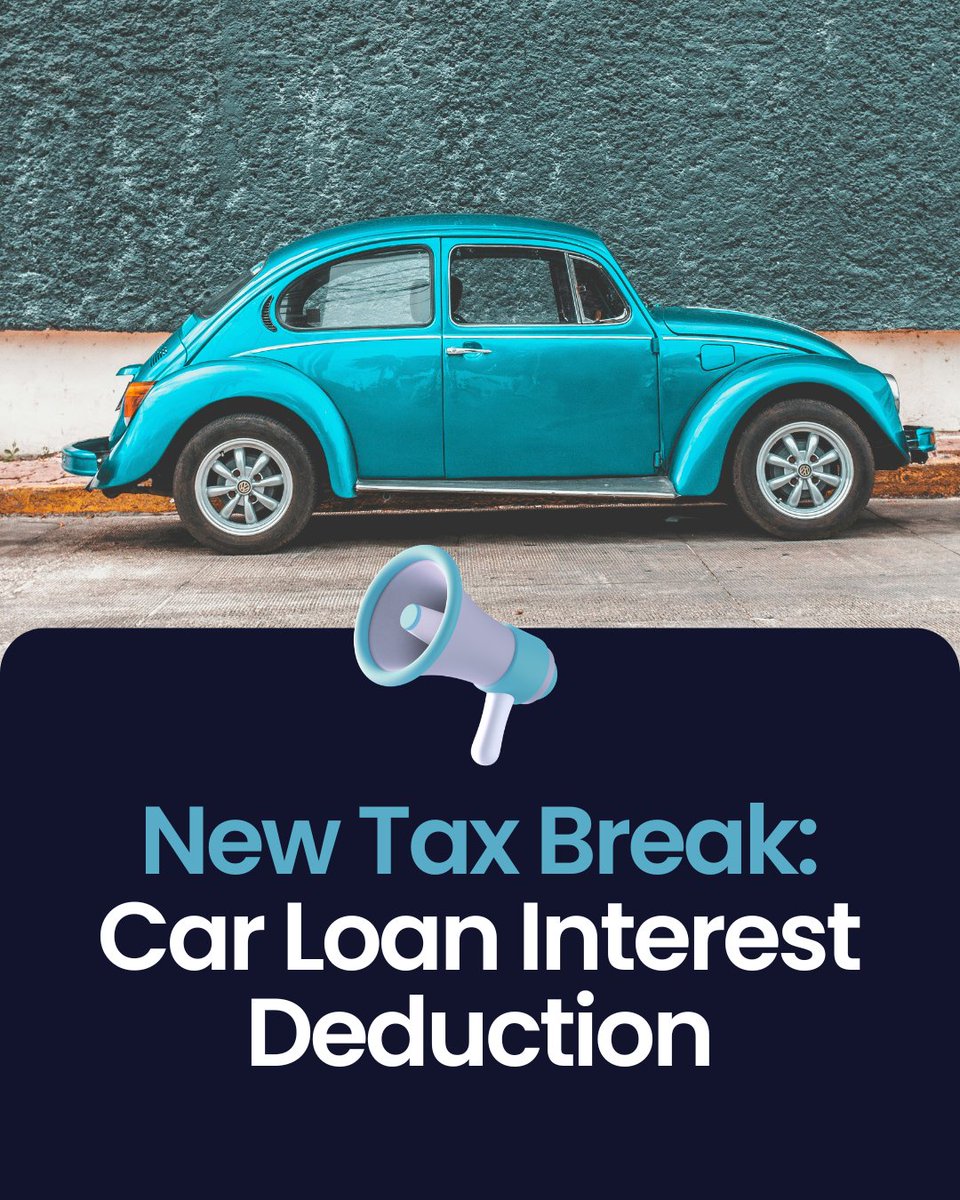

If you bought a new car in 2025, there's a deduction you should know about.

Starting this year, eligible taxpayers can deduct up to $10,000 in car loan interest. What makes this one interesting is that it's available whether you itemize your taxes or not, which isn't always the case.

To qualify, the vehicle needs to be new, assembled in the U.S., and used for personal purposes. Your loan also needs to have started after December 31, 2024. The deduction phases out if your modified adjusted gross income is over $100,000 (or $200,000 if you file jointly), and it applies through the 2028 tax year.

Not sure if it applies to you? That's what we're here for.

If you’ve got a capital gain and you’re thinking long-term, Qualified Opportunity Zones (QOZs) are one of the most impactful tools in the tax code.

What is an Opportunity Zone? Opportunity Zones are designated economically distressed communities meant to spur investment, economic growth, and job creation, with tax benefits offered to investors.

How the incentive works (in plain English):

When you roll eligible capital gains into a Qualified Opportunity Fund (QOF) that invests in Opportunity Zones, you can unlock two major advantages:

✅ Now: Temporary tax deferral on the capital gains you reinvest. In general, the deferred gain is recognized when you sell the QOF investment.

✅ Later: Potential tax-free appreciation on the QOF investment itself. If you hold the QOF investment long enough (often 10 years), you may be able to exclude the capital gains on the investment’s growth when you sell.

Why it matters: It’s one of the rare strategies where you can defer taxes today and potentially wipe out taxes on future growth, but the rules are technical and the timeline matters.

If you’re a business owner or investor sitting on a gain, this is worth a conversation before you make your next move.

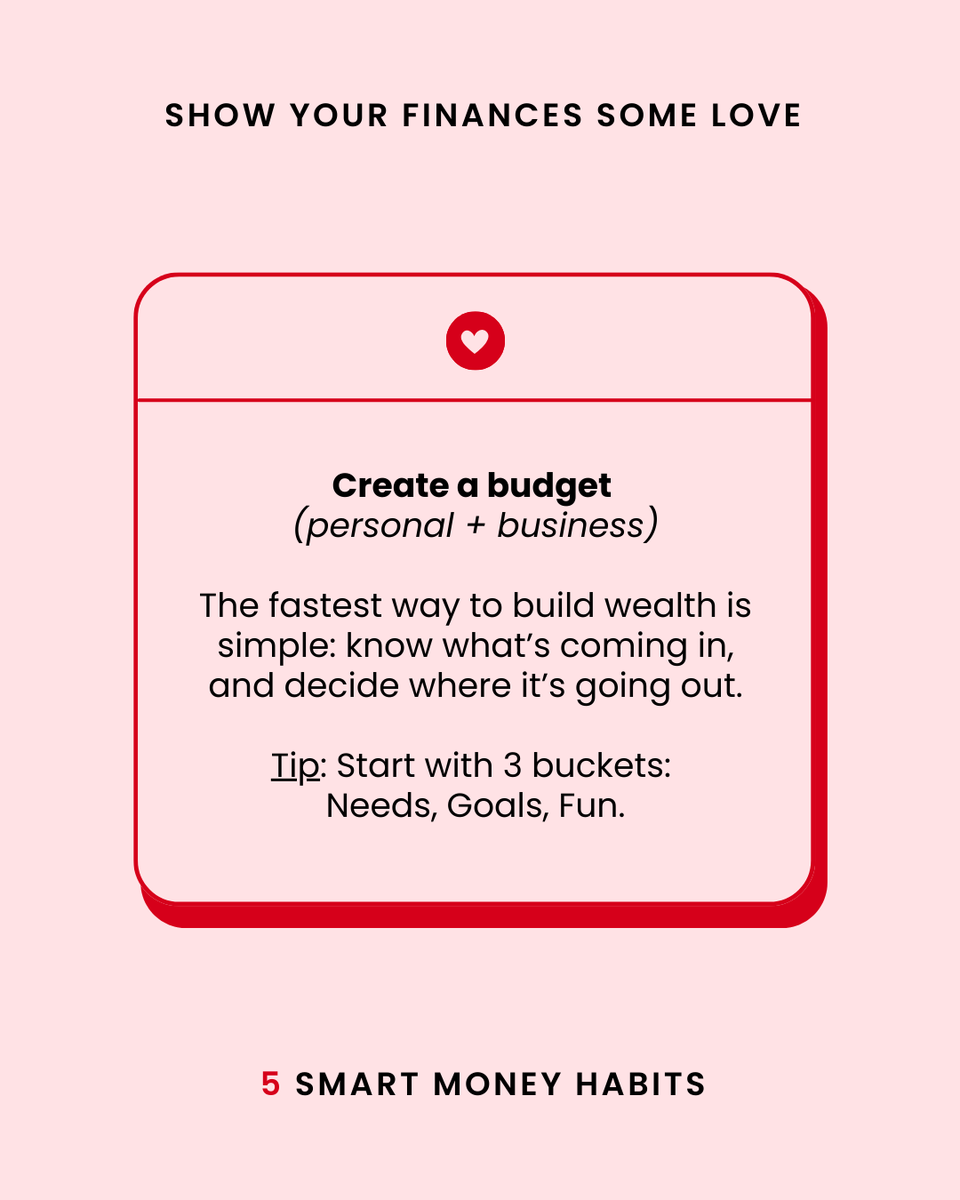

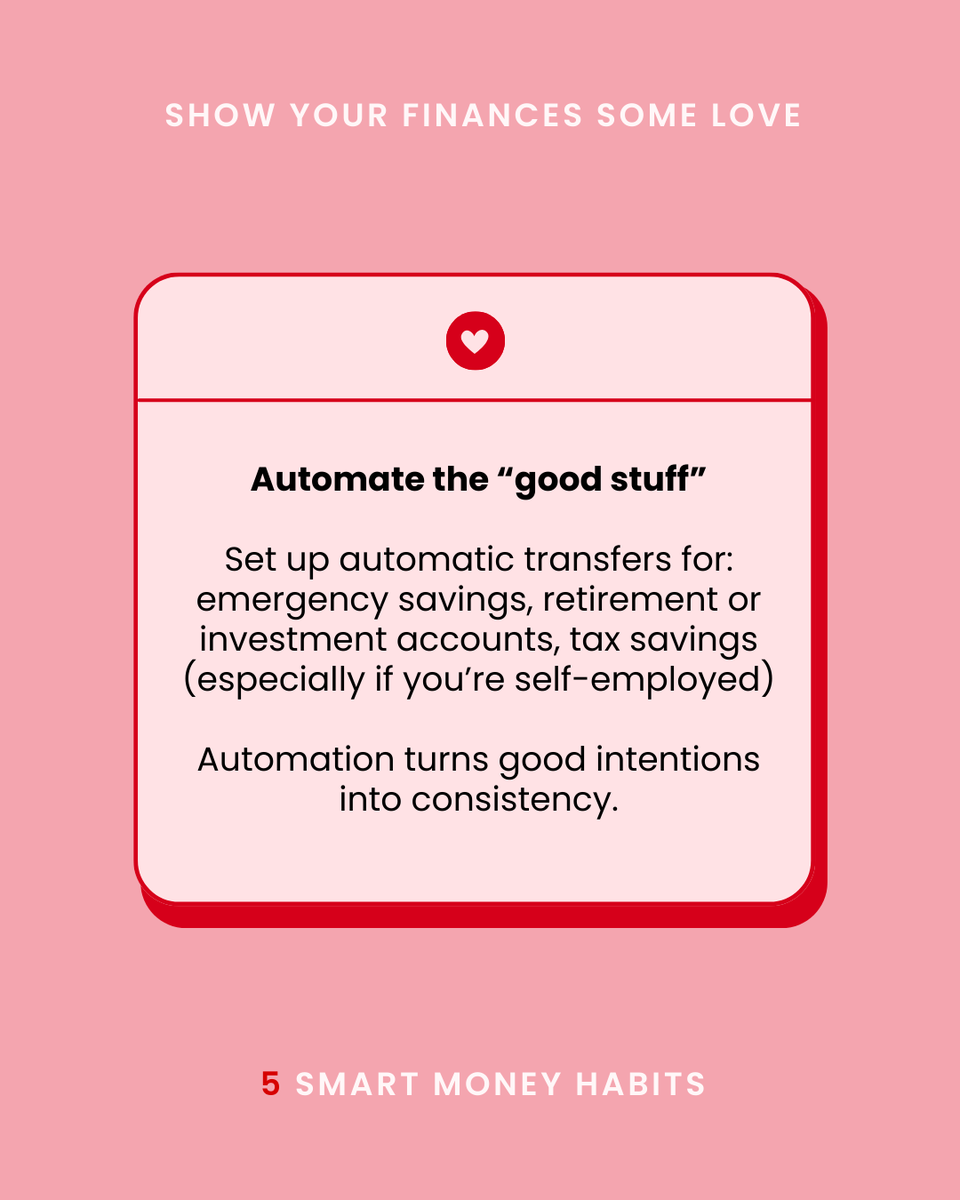

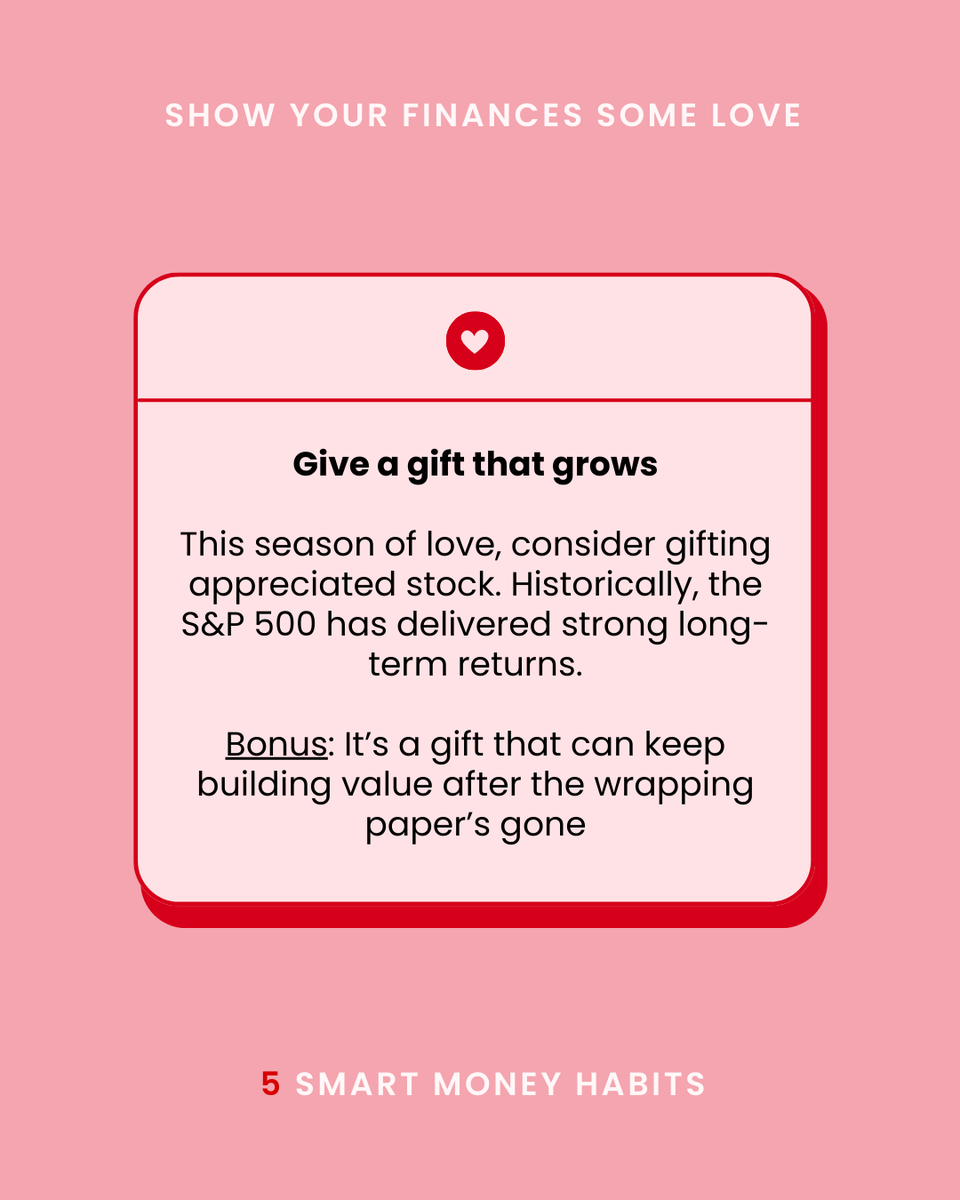

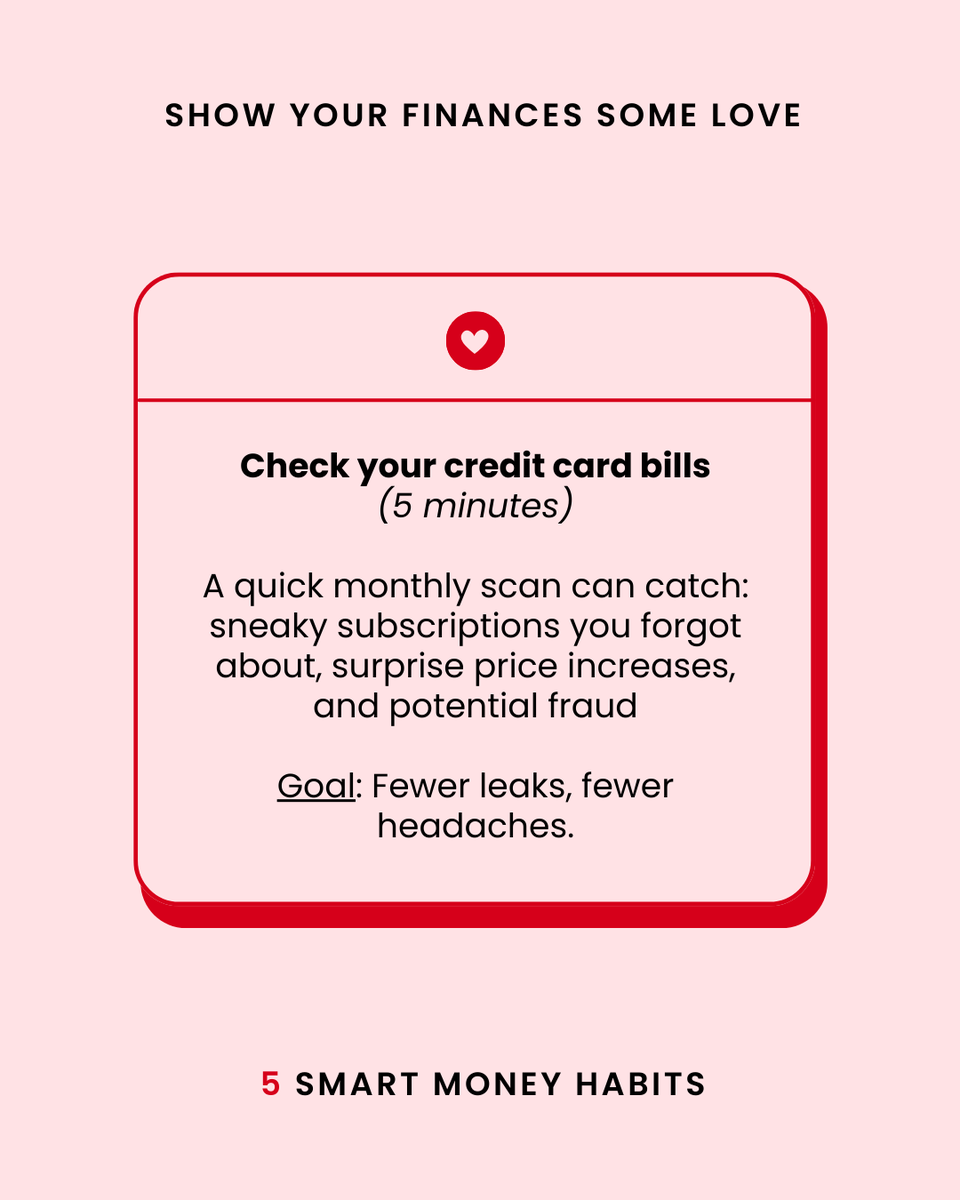

Roses are red. Violets are blue. Your finances deserve attention too. 💘

Here are 5 habits that make money feel less stressful and a lot more intentional, whether you’re running a business, managing a household, or both.

Save this for your next “money date.” And if you want help tightening up your budget, building a cash flow routine, or setting up a tax-smart system, Alpine Mar’s got you.

Which habit are you starting this month: 1, 2, 3, 4, or 5?

Charitable giving is still a win. The tax rules around it are shifting in 2026. Here are three changes to know before you map out your giving strategy:

1) A new $1,000 charitable deduction for standard-deduction filers

If you don’t itemize, you may be able to deduct up to $1,000 in qualifying cash donations ($2,000 if married filing jointly) starting in 2026.

2) A new 0.5% AGI “floor” for itemizers

If you do itemize, charitable deductions generally only apply to the portion of donations that exceeds 0.5% of your adjusted gross income (AGI).

3) A new 35% cap for high-income donors

For higher-income taxpayers, the tax value of certain charitable deductions is expected to be capped at 35% starting in 2026 (even if your marginal rate is higher).

💡 Why it matters: the “best” way to give for taxes may look different depending on whether you itemize, your income, and how you donate.

Want help pressure-testing your 2026 giving plan (personal or business)? That’s what we do.