Only looking at the numbers for analysis is what gets you in trouble, PSU banks are prone to pressures for disbursing loans (to suit government policies); having a high chance of becoming NPA (happened many times before).

Otherwise why would it be available at such heavy discount!!

Bank of Maharashtra 🏦

I posted about it at ₹60.

Posting again at a market cap of ₹62,000 Cr.

Reading the Q1 FY27 investor presentation is a treat.

Imagine a bank available at <1.5x P/B and ~7x P/E with:

• 10Y PAT CAGR: 50%

• 3Y PAT CAGR: 39%

• ROE maintained at 23% for the last 3 years which is one of the highest even among private banks. ROE of HDFC Bank is 14% While that of ICICI BANK is 16%.

• Q1 FY27 ROE: 26%

• FY26 ROA: 1.86%

• Q1 FY27 ROA: 1.97%

• Net NPA: just 0.13%

• CASA maintained around 50% for several quarters hence cost of deposit is just 4.38%

• Advances CAGR of 21% over the last 5 years

• FY26 advances growth: 27%

Debt waiver to be announced by Maharashtra government will have positive impact as bank holds 1700cr

provision against the impact of 450/500cr

NIM will be maintained at 3.75% Any rate hike will benefits the bank significantly as Bank has 53% of book linked to repo rate.

A bank with strong growth, high ROE, excellent asset quality and a robust CASA franchise is available at mouthwatering valuation.

The market or I may be missing something. 📈

I will be applying for Milworks Tech IPO under HNI category. For one lot Rs 2.64L is required. If anyone wants to know the process of applying under HNI category can DM me at https://t.co/RUG9U0Ou1R

Millworks Technologies IPO

It is a Bengaluru-based precision engineering company manufacturing high-accuracy components and assemblies for aerospace, defence, railways and semiconductor industries.

Its ₹160.34 crore BSE SME IPO, entirely a fresh issue, is priced at ₹315–331 per share and closes on 16 July 2026.

Investors should consider customer concentration, SME-platform liquidity risk, execution challenges and the aggressive valuation after recent growth.

Strong subscription demand and grey-market activity indicate listing interest.

Kusumgar IPO has delivered a strong post-listing performance. Against the issue price of ₹419, the stock is trading near ₹600, generating returns of around 43.2%. Investors who received allotment have earned impressive gains. However, fresh buying should be considered only after evaluating valuation, liquidity, business outlook and post-listing volatility.

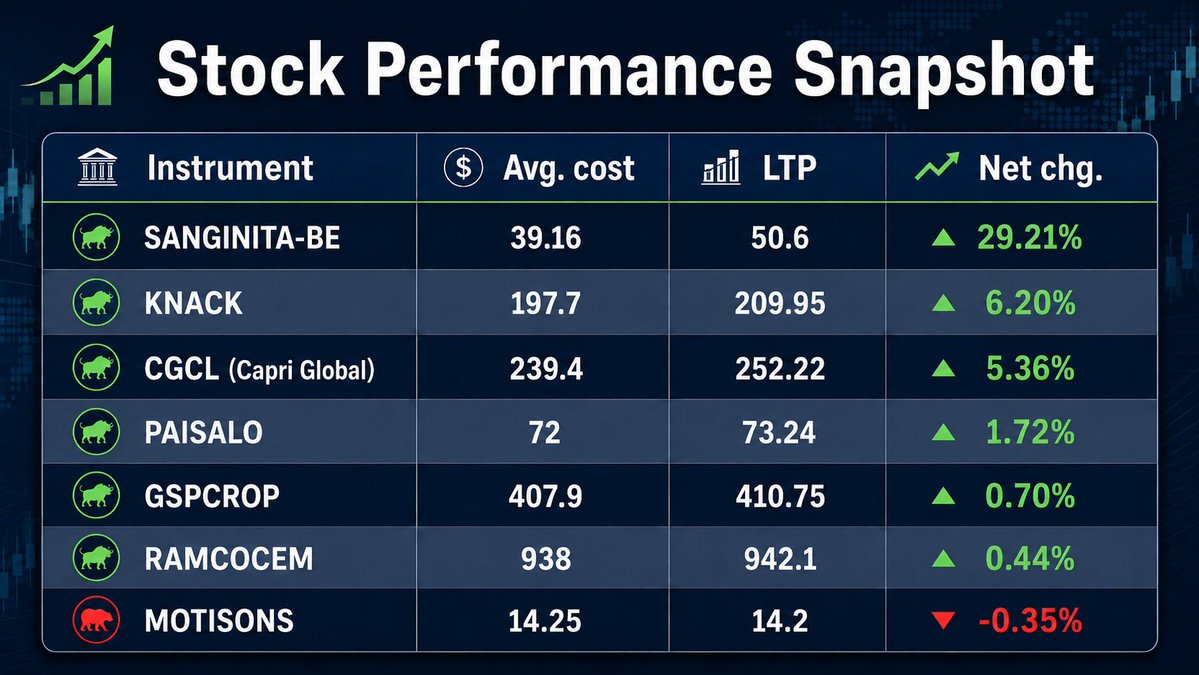

Recently started investing small amounts based on data from large/bulk deals. Result is below. All orders were AMO (with market protection) puched in the evening after analysing the data. Will be exiting motison.

Large Purchase for today.

Capri Global (Money Matter F S) which got Rs 123 cr of net purchase amount was 6.57% up today. Polunin EM fund invested Rs 38.8 cr in Unichem shares today and it rose 13.6%. Knack packaging which was listed this week saw net purchase of Rs 17cr yesterday and Rs 13 cr today.

Kusumgar IPO may attract listing gain interest, mainly because of strong GMP and subscription demand. However, from a long-term investment point of view, I would remain cautious at current valuations. FY26 revenue and profit have declined, and the IPO is a complete OFS, so no fresh money is coming into the company.

On similar lines

Amara Raja Energy & Mobility is moving beyond traditional lead-acid batteries and building a strong future-ready platform. Its Telangana Giga Corridor plans lithium-ion cell capacity of up to 16 GWh and battery pack capacity of up to 5 GWh, backed by a proposed ₹9,500 crore investment over 10 years. This can position the company in EVs, energy storage and industrial mobility solutions. Key monitorables are execution timelines, technology partnerships, customer tie-ups, capex discipline and margins. For long-term investors, Amara Raja is transforming from an auto-battery company into a clean-energy storage play. Not a recommendation. Please do your own research first

Exide Industries is quietly positioning itself for India’s energy transition. Through Exide Energy Solutions, the company is building a lithium-ion cell gigafactory in Bengaluru, with Phase 1 capacity of 6 GWh and potential ramp-up to 12 GWh. This expansion can open opportunities across EVs, industrial batteries and energy-storage systems, while reducing dependence on imported cells.

Key monitorables: timely commissioning, capacity utilisation, technology stability, margins and customer tie-ups.

For long-term investors, Exide is no longer just a traditional battery play—it is becoming a serious participant in India’s future battery ecosystem.

Not a recommendation. I have already invested in the company.

Exide Industries is quietly positioning itself for India’s energy transition. Through Exide Energy Solutions, the company is building a lithium-ion cell gigafactory in Bengaluru, with Phase 1 capacity of 6 GWh and potential ramp-up to 12 GWh. This expansion can open opportunities across EVs, industrial batteries and energy-storage systems, while reducing dependence on imported cells.

Key monitorables: timely commissioning, capacity utilisation, technology stability, margins and customer tie-ups.

For long-term investors, Exide is no longer just a traditional battery play—it is becoming a serious participant in India’s future battery ecosystem.

Not a recommendation. I have already invested in the company.

IBULLS LTD a brief research summary.

Disclosure : Me and my family members have bought the shares.

The forgotten merger story quietly building a ₹21,366 Cr real estate pipeline. Here's what my analysis of the Q4 FY26 & Q3 FY26 filings revealed 🧵👇

THE TRANSFORMATION

Dhani Services + Indiabulls Enterprises merged into Yaari Digital (NCLT-approved, Oct 2025) and rebranded as Indiabulls Limited. The result: a real estate-led company with financial services diversification — stock broking, ARC, UPI payments, and an SMB fintech stake.

FY26 NUMBERS

▪️ Revenue: ₹880.7 Cr | PAT: ₹346.1 Cr (39.3% margin)

▪️ Q4 alone: Revenue ₹418.3 Cr, PAT ₹194.2 Cr

▪️ RE Sales Booked: ₹2,752 Cr (909 units, 21.6 lakh sqft)

▪️ Collections: ₹400 Cr

THE BULL CASE 🐂

✅ ₹2,493 Cr of already-booked sales yet to hit the P&L — FY27–28 earnings growth is substantially pre-sold, not speculative

✅ ₹21,366 Cr GDV pipeline across 110.5 lakh sqft, concentrated on Dwarka Expressway — Gurugram's share of tier-1 residential sales jumped from 6.1% (CY21) to 14.6% (CY25)

✅ Capital-efficient JV model: ~40% net margin to Indiabulls on the full pipeline

✅ Free options: 16.4% stake in Spring Cash (US AI-SMB lender, $102M funded), TPAP-UPI rollout, ARC with ₹3,794 Cr under collection

✅ DII holding just 0.16% — institutional discovery itself is a re-rating trigger

THE BEAR CASE 🐻

⚠️ Single micro-market concentration: 86% of portfolio in NCR; every major developer is now crowding the same ₹2–6 Cr Gurugram band

⚠️ GRAP construction halts are structural — Q3 revenue collapsed to ₹102.6 Cr for exactly this reason

⚠️ Broking paradox: new clients up ~88%, yet FY26 broking revenue FELL 5% (₹131→₹124 Cr). Discount broking is diluting economics

⚠️ Consolidated debt & cash flow NOT disclosed in investor materials — the story is being told from the P&L only

RED FLAGS I NOTICED 🚩

1️⃣ GDV restated: ₹23,042 Cr (Q3 deck) → ₹21,366 Cr (Q4 deck); Ludhiana re-scoped from 43.2 to 12.7 lakh sqft

2️⃣ Q3 FY26 PAT (₹78.4 Cr) was 76% of revenue — implies non-operating support

3️⃣ Spring Cash held "jointly with promoter entities" — governance watch item

MY TAKE

This is a high-risk, high-visibility turnaround. Pre-sold revenue gives 2–3x earnings potential over 3–5 years, but thin balance-sheet disclosure and single-market cyclicality mean position sizing must respect a possible 50% drawdown. Suitable ONLY for risk-tolerant investors with a long horizon. Watch: FY27 launch approvals (Sec 104 Ph-3, Ludhiana), the annual report's debt disclosure, and quarterly booking run-rate vs the ₹3,000 Cr target.

Detailed Research Report https://t.co/ZyKnEE1ZaY

Telegram Channel https://t.co/qFELPPWEU3

⚠️ Disclaimer: For education only. Not a buy/sell recommendation. Investment in securities market is subject to market risks; read all related documents carefully before investing. Registration granted by SEBI and NISM certification do not guarantee performance or assure returns. Please consult your financial advisor. #StockMarket #EquityResearch #Indiabulls #IBULLSLTD #Investing