Andrew Casertano, Financial Advisor Securities offered through Cetera Advisor Networks LLC, member FINRA/SIPC. Advisory Services offered through Cetera Investment Advisers LLC, a registered investment adviser. Cetera is under separate ownership from any other named entity.

TERM LADDERING — MAXIMUM COVERAGE WHEN YOU NEED IT MOST

Most people buy one large life insurance policy for one term length. There's a smarter approach.

Term laddering uses multiple smaller policies with staggered expirations — aligned with your actual declining obligations over time.

The illustration shows why: at peak obligation years, you need coverage for income replacement, the full mortgage, children's college, and outstanding debts. As time passes, each obligation shrinks or disappears.

A ladder structure means:

→ More total coverage during the highest-risk years

→ Shorter policies expire as those obligations are met

→ Premiums drop naturally as your need for coverage decreases

This typically produces significant premium savings over a 20–30 year horizon compared to buying one large long-term policy — while actually providing more protection during the years it matters most.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03LwnWou

THREE TYPES OF PERMANENT LIFE INSURANCE — AND WHEN EACH MAKES SENSE

Permanent life insurance is often oversold — and sometimes sold dishonestly. I've sat with clients who were promised "no downside" returns and "bank on yourself" strategies that looked nothing like reality years later.

The three main types:

Whole Life — consistent, scheduled growth. Dividends are possible but not guaranteed. Stable and predictable.

Universal / Indexed Universal Life — floor on losses, ceiling on gains. You don't lose when the market drops, but caps and participation rates limit how much you earn when it rises.

Variable Life — participates directly in market performance. Higher potential growth, but full exposure to market losses.

Here's what I tell clients: permanent insurance can be a powerful final layer in a well-structured plan — especially for high-income earners, estate planning, or long-term care needs. But it needs to be structured by someone who's being transparent about the trade-offs, not chasing a commission.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03Lwoue2

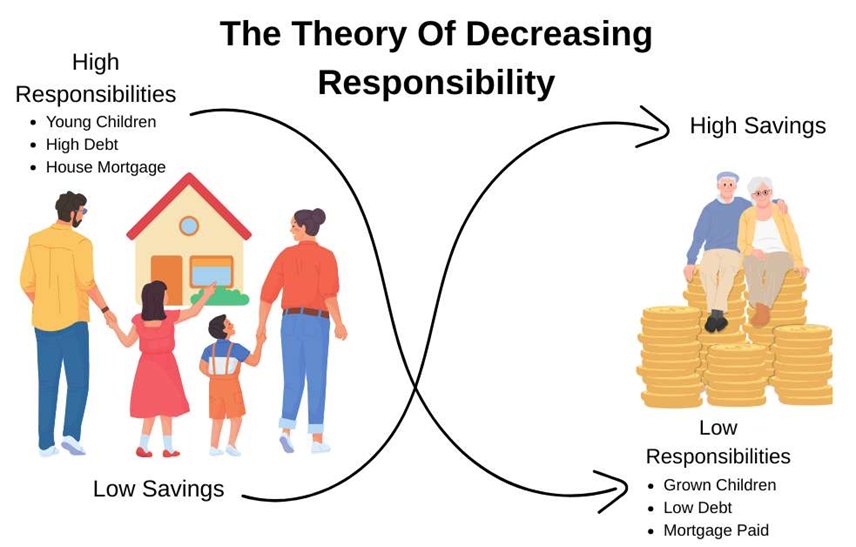

LIFE INSURANCE IS A LOVE LETTER

When I work with a family on life insurance, I don't start with policy types or premium amounts.

I start with a question: If something happened to you tomorrow, would your family be okay?

The theory of decreasing responsibility makes the math clear. Early in life: high obligations — young children, mortgage, high debt, low savings. Later in life: those obligations decrease as savings grow and debts are paid.

Coverage needs are highest when obligations are highest — when children are young, the mortgage balance is large, and personal savings haven't had time to build. That time is typically now.

Life insurance is the promise that even if you're not there, the people who depend on you won't have to figure it out alone. I've seen what happens when families have it. I've seen what happens when they don't. The difference is devastating.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03LwnWou

A SMARTER WAY TO OWN THE INDEX

ETFs and index funds democratized investing. But they come with a limitation most people don't think about: you own the entire bundle, including positions you may not want.

Direct indexing offers an alternative. Instead of buying a fund, you buy the individual stocks that make up the index — tailored to your specific situation.

ETF or Mutual Fund → you own the whole bundle

Direct Indexing → you buy individual shares of what's best for you

The advantages are meaningful:

→ Tax-loss harvesting at the individual security level — sell specific losers to offset gains

→ Customization — exclude sectors, companies, or positions based on personal values or concentration

→ Potentially superior after-tax returns for higher-bracket investors

The disadvantages are also worth understanding:

→ Higher cost than a standard index fund

→ Higher minimum investment required

→ Tax benefits may diminish over time

→ Greater administrative burden

This used to require institutional minimums. Technology has made it increasingly accessible. If you have significant taxable accounts and you're in a higher bracket, it's worth a serious conversation.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03LwnWou

DIVIDENDS AREN'T FREE MONEY

One of the most persistent myths in retail investing: dividend stocks are a reliable, low-risk income machine.

Here's the reality. When a company pays a dividend, the stock price drops by approximately the same amount. The dividend isn't extra money that appears from nowhere — it's a transfer from the company's value to the shareholder's hand.

The chart makes it visual: before the dividend, the stock has a certain value. After the dividend is paid, the stock portion shrinks by that amount. Total wealth is essentially unchanged — but now you've created a taxable event.

That forced taxable event is the hidden cost most dividend investors never account for. I'm not saying dividends are bad. I'm saying don't confuse a dividend for a gift. Understand what you're actually getting.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03Lwoue2

THE INVESTMENT UNIVERSE MOST PEOPLE NEVER ACCESS

For most of my career, alternative investments required a $1 million net worth minimum just to participate. Private equity, private credit, hedge funds, real assets — tools reserved for the wealthy.

That's changing.

Regulatory changes have opened new access points, and at Kinnect Advisors I now help eligible clients participate in alternatives that can potentially reduce volatility and improve risk-adjusted returns.

The four main categories:

→ Private Equity / Venture Capital — investing in the 99% of companies that aren't public (Chambers, D., Dimson, E., & Kaffe, C. (2024). "Seventy-Five Years of Investing for Future Generations." Journal of Alternative Investments. ScienceDirect.)

→ Private Credit — lending to private companies, generating stable income

→ Hedge Funds — unique return streams with advanced risk management

→ Real Estate — physical assets with income and appreciation potential

Studies consistently show that higher-net-worth investors allocate significantly more to alternatives. (Chambers, D., Dimson, E., & Kaffe, C. (2024). "Seventy-Five Years of Investing for Future Generations." Journal of Alternative Investments. ScienceDirect.) The wealthy have understood for decades that public markets are just a fraction of what's available.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03Lwoue2

DIVERSIFICATION IS THE ONLY FREE LUNCH IN INVESTING

Nobel Prize winner Harry Markowitz called it clearly: "Diversification is the only free lunch in investing."

A non-diversified portfolio is like dangling from a single rope. One bad outcome — one company failure, one sector collapse — and you fall.

A truly diversified portfolio builds in redundancy. Different asset classes move differently under different conditions. When one falls, others may hold or rise. The volatility of the whole is less than the sum of its parts.

If a man with his entire net worth in a single employer's stock diversified just before that stock crashed, he would walk away in a better position than colleagues who didn't plan.

Less than 1% of companies are publicly traded. (Chambers, D., Dimson, E., & Kaffe, C. (2024). "Seventy-Five Years of Investing for Future Generations." Journal of Alternative Investments. ScienceDirect.) A truly diversified portfolio reaches beyond public markets.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03Lwoue2

RISK TOLERANCE ISN'T A BINARY CHOICE

Most people think investment risk works like a dial: more safety OR more growth. You pick one side. In reality, it's more nuanced.

A well-structured, diversified portfolio — incorporating equities for growth, fixed income for income and stability, and other strategies such as structured notes or alternatives — may help investors pursue growth while managing risk and enhancing diversification.

The goal isn't to eliminate risk. It's to thoughtfully manage it by aligning the types and levels of risk with your specific situation, time horizon, and goals.

I've had clients come to me holding 100% cash because they were afraid of the market. What they didn't realize is that inflation was eroding their purchasing power every single day. Doing nothing is also a risk.

Diversification and asset allocation do not ensure a profit or protect against loss and are intended to help manage risk based on an investor's objectives.

Excerpt from my book: Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03LwnWou

TIME IS YOUR GREATEST ASSET

Divide 72 by your expected rate of return, and you'll know approximately how many years it takes for your money to double.

At 3%: doubles every 24 years.

At 6%: doubles every 12 years.

At 12%: doubles every 6 years.

Start early, and this math works in your favor in a way almost nothing else can replicate.

But here's the dark side: the same math applies to debt. A 24% credit card rate means your balance doubles every 3 years.

Compound interest is either your greatest ally or your most relentless enemy — depending entirely on which side of the equation you're standing on.

Excerpt from my book Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03LwnWou

Everyone is always rooting for you. Your parents want you to be a great son. Wife wants you to be a great husband. Your boss wants you to be a slam dunk hire. Every first date you’ve ever been on they’ve been rooting for you to get laid. Every time you started to tell a joke people hoped it would have a hilarious punch line. Your proximity to anyone is a reflection of themself, meaning the deck is never stacked against you, and your failures are completely your own

THE BEHAVIOR GAP — WHY MOST INVESTORS UNDERPERFORM

The average investor earned 3.6% per year over a 20-year period. The S&P 500 returned 9.5% over the same period. (Source: J.P. Morgan Asset Management, 2022 — please verify this is the most current data available.)

That nearly 6% gap isn't explained by bad stock picks. It's explained by behavior.

Investors panic and sell at the bottom. They chase performance and buy at the top. They watch financial news obsessively and make reactive decisions based on headlines designed to trigger emotion.

I've seen brilliant, disciplined people make terrible investment decisions because their emotions got involved. One of the most valuable things I do as an advisor isn't portfolio construction — it's keeping clients from making fear-based moves that permanently damage their long-term outcomes.

Excerpt from my book Game of Wealth

Complimentary consultation and physical copy of the book at my expense! https://t.co/hd03Lwoue2

BUILD YOUR FINANCIAL HOUSE IN THE RIGHT ORDER

One of the most expensive financial mistakes I see isn't the wrong investment — it's the wrong sequence.

Jumping straight to aggressive investing while carrying high-interest debt and no life insurance is like building a house without a foundation. Everything you build on top is at risk.

The right order, every time:

1. Insurance & estate planning — it holds up everything else

2. Debt management — stop bleeding to interest

3. Emergency fund — your safety net

4. Retirement investing — build for the future

5. Goals & dreams — easier to reach once the rest is solid

Each step creates a base for the next. Skipping any one of them doesn't accelerate progress. It creates hidden vulnerability.

Complimentary consultation and book at our expense! https://t.co/hd03Lwoue2

I use a football analogy with nearly every client I work with — because it clicks immediately.

You need both offense and defense to win. Most people I meet have an offense strategy. Very few have a real defense.

Offense helps builds wealth — income, business equity, 401(k), IRA, HSA, taxable accounts, real estate.

Defense helps protects what you've built — tax planning, insurance, emergency funds, estate documents, debt repayment.

The families who build lasting wealth play both sides of the field simultaneously. I've never met a financially resilient family that only played offense.

Complimentary consultation and book copy at our expense! https://t.co/hd03LwnWou

In 2023, financial illiteracy cost Americans $388 billion. (Source: NFEC Survey, 2023)

That number isn't abstract to me. I've sat across from real families who made painful financial decisions — not because they were careless, but because no one ever gave them the right tools.

I wrote Game of Wealth because I believe every family deserves access to a complete financial roadmap — not just the wealthy, not just those with sophisticated backgrounds. Everyone.

The six pillars of a complete plan — cash flow, protection, investments, taxes, retirement, and legacy — must work together. Miss one, and the whole structure is weaker than it looks.

Complimentary consultation and copy of the book at our expense! https://t.co/hd03LwnWou